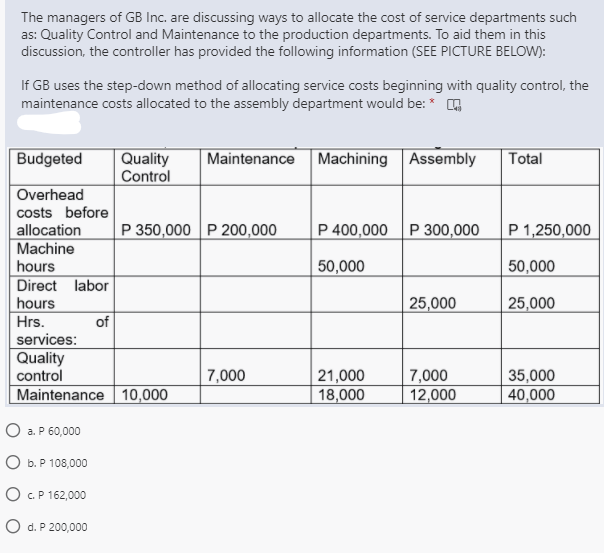

The managers of GB Inc. are discussing ways to allocate the cost of service departments such as: Quality Control and Maintenance to the production departments. To aid them in this discussion, the controller has provided the following information (SEE PICTURE BELOW): If GB uses the step-down method of allocating service costs beginning with quality control, the maintenance costs allocated to the assembly department would be: * Budgeted Quality Control Maintenance Machining Assembly Total Overhead costs before P 350,000 P 200,000 P 400,000 P 300,000 P 1,250,000 allocation Machine hours Direct labor hours 50,000 50,000 25,000 25,000

The managers of GB Inc. are discussing ways to allocate the cost of service departments such as: Quality Control and Maintenance to the production departments. To aid them in this discussion, the controller has provided the following information (SEE PICTURE BELOW): If GB uses the step-down method of allocating service costs beginning with quality control, the maintenance costs allocated to the assembly department would be: * Budgeted Quality Control Maintenance Machining Assembly Total Overhead costs before P 350,000 P 200,000 P 400,000 P 300,000 P 1,250,000 allocation Machine hours Direct labor hours 50,000 50,000 25,000 25,000

Managerial Accounting

15th Edition

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:Carl Warren, Ph.d. Cma William B. Tayler

Chapter5: Support Department And Joint Cost Allocation

Section: Chapter Questions

Problem 8E

Related questions

Question

100%

QUESTION 38

Cost Accounting

Choose the answer from the choices

Transcribed Image Text:The managers of GB Inc. are discussing ways to allocate the cost of service departments such

as: Quality Control and Maintenance to the production departments. To aid them in this

discussion, the controller has provided the following information (SEE PICTURE BELOW):

If GB uses the step-down method of allocating service costs beginning with quality control, the

maintenance costs allocated to the assembly department would be: *

Quality

Control

Maintenance Machining Assembly

Budgeted

Total

Overhead

costs before

allocation

Machine

P 350,000 P 200,000

P 400,000 P300,000

P 1,250,000

hours

50,000

50,000

Direct labor

hours

Hrs.

services:

Quality

control

Maintenance 10,000

| 25,000

25,000

of

| 7,000

12,000

7,000

21,000

18,000

35,000

40,000

O a. P 60,000

ОБ.Р 108,000

O C.P 162,000

O d. P 200,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning