ADV.FIN.ACCT. CONNECT+PROCTORIO PLUS

12th Edition

ISBN: 9781266379017

Author: Christensen

Publisher: INTER MCG

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 1, Problem 1.13E

Acquisition Using Debentures

Planter Corporation used debentures with a par value of $625,000 to acquire 100 percent of Sorden Company’s net assets on January 1, 20X2. On that date, the fair

Required

Required

Give the

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Required information

On January 1, 20X2, Power Company acquired 80 percent of Strong Company's outstanding stock for cash. The fair value

of the noncontrolling interest was equal to a proportionate share of the book value of Strong Company's net assets at the

date of acquisition. Selected balance sheet data at December 31, 20X2 are as follows:

Total Assets

Liabilities

Common Stock

Retained Earnings

Total Liabilities & Stockholders' Equity

Multiple Choice

O

$35,200

Based on the preceding information, what amount should be reported as noncontrolling interest in net assets in Power Company's December 31, 20X2, consolidated balance sheet?

$48,200

$76,800

Power

$ 564,000

O $112,800

180,000

150,000

234,000

$ 564,000

Strong

$ 216,000

65,000

80,000

96,000

$ 241,000

On October 1, Dennis Company purchased ₱200,000 face value, 12% bonds at 98 plus accrued interestand brokerage fees and classified them as amortized cost assets. Interest is paid semiannually on January1 and July 1. Brokerage fees for this transaction were ₱700. At what amount should this acquisition ofbonds be recorded?

Sony Co. issued bonds payable amounting to P500,000 for the new assets of JBL Corp. At the time of the acquisition Sony incurred transaction costs of P20,000 in issuing bonds. The followinginformation was available related to JBL’s financial position.

Book Value Fair ValueCurrent Assets 250,000 250,000Inventories 400,000 500,000Equipment 200,000 250,000Liabilities 150,000 150,000

What is the amount of gain or loss on disposal of should the acquiree recognized?

Chapter 1 Solutions

ADV.FIN.ACCT. CONNECT+PROCTORIO PLUS

Ch. 1 - What types of circumstances would encourage...Ch. 1 - How would the decision to dispose of a segment of...Ch. 1 - Prob. 1.3QCh. 1 - Prob. 1.4QCh. 1 - Prob. 1.5QCh. 1 - Prob. 1.6QCh. 1 - Prob. 1.7QCh. 1 - Prob. 1.8QCh. 1 - Prob. 1.9QCh. 1 - Prob. 1.10Q

Ch. 1 - Prob. 1.11QCh. 1 - Prob. 1.12QCh. 1 - Prob. 1.13QCh. 1 - Prob. 1.14QCh. 1 - Within the measurement period following a business...Ch. 1 - Prob. 1.16QCh. 1 - Prob. 1.1CCh. 1 - Prob. 1.2CCh. 1 - Prob. 1.3CCh. 1 - Prob. 1.4CCh. 1 - Risks Associated with Acquisitions Not all...Ch. 1 - Prob. 1.6CCh. 1 - Prob. 1.1.1ECh. 1 - Prob. 1.1.2ECh. 1 - Prob. 1.1.3ECh. 1 - Multiple-Choice Questions on Complex Organizations...Ch. 1 - Prob. 1.1.5ECh. 1 - Prob. 1.2.1ECh. 1 - Prob. 1.2.2ECh. 1 - Multiple-Choice Questions on Recording Business...Ch. 1 - Prob. 1.2.4ECh. 1 - Multiple-Choice Questions on Recording Business...Ch. 1 - Multiple-Choice Questions on Reported Balances...Ch. 1 - Multiple-Choice Questions on Reported Balances...Ch. 1 - Prob. 1.3.3ECh. 1 - Prob. 1.3.4ECh. 1 - Prob. 1.4.1ECh. 1 - Prob. 1.4.2ECh. 1 - Prob. 1.4.3ECh. 1 - Multiple-Choice Questions Involving Account...Ch. 1 - Prob. 1.4.5ECh. 1 - Prob. 1.5ECh. 1 - Prob. 1.6ECh. 1 - Prob. 1.7ECh. 1 - Prob. 1.8ECh. 1 - Prob. 1.9ECh. 1 - Prob. 1.10ECh. 1 - Balances Reported Following Combination Palm...Ch. 1 - Goodwill Recognition Spur Corporation reported the...Ch. 1 - Acquisition Using Debentures Planter Corporation...Ch. 1 - Bargain Purchase Using the data resented in E1-13,...Ch. 1 - Prob. 1.15ECh. 1 - Prob. 1.16ECh. 1 - Prob. 1.17ECh. 1 - Prob. 1.18ECh. 1 - Prob. 1.19ECh. 1 - Prob. 1.20ECh. 1 - Prob. 1.21ECh. 1 - Prob. 1.22ECh. 1 - Prob. 1.23ECh. 1 - Prob. 1.24PCh. 1 - Prob. 1.25PCh. 1 - Prob. 1.26PCh. 1 - Acquisition in Multiple Steps Peal Corporation...Ch. 1 - Prob. 1.28PCh. 1 - Prob. 1.29PCh. 1 - Prob. 1.30PCh. 1 - Prob. 1.31PCh. 1 - Computation of Account Balances Saspro Division is...Ch. 1 - Prob. 1.33PCh. 1 - Prob. 1.34PCh. 1 - Prob. 1.35PCh. 1 - Business Combination Following are the balance...Ch. 1 - Prob. 1.37PCh. 1 - Prob. 1.38PCh. 1 - Prob. 1.39PCh. 1 - Prob. 1.40P

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

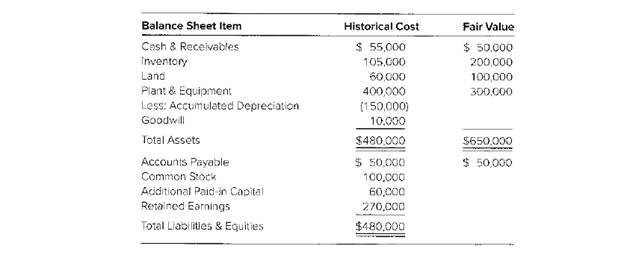

- Transfer between Categories On December 31, 2018, Leslie Company held an investment in bonds of Kaufmann Company which it categorized as being held to maturity. At that time, the 8%, 100,000 face value bonds had a carrying value of 107,023.56 and were being amortized using the effective interest method based on a market rate of 7%. Interest on these bonds is paid annually each December 31. On December 31, 2019, after recording the interest earned, Leslie decided to reclassify the Kaufmann bonds to its available-for-sale category in anticipation of a major restructuring. At that time, the ending quoted market price for the bonds was 105,000. Required: Prepare the journal entries on December 31, 2019, to record the interest earned and the reclassification.arrow_forwardParilo Company acquired 170,000 of Makofske Co., 5% bonds on May 1, 2016, at their face amount. Interest is paid semiannually on May 1 and November 1. On November 1, 2016, Parilo Company sold 50,000 of the bonds for 96. Journalize entries to record the following: a. The initial acquisition of the bonds on May 1. b. The semiannual interest received on November 1. c. The sale of the bonds on November 1. d. The accrual of 1,000 interest on December 31, 2016.arrow_forwardPlanter Corporation used debentures with a par value of $644,000 to acquire 100 percent of Sorden Company's net assets on January 1, 20X2. On that date, the fair value of the bonds issued by Planter was $627,000. The following balance sheet data were reported by Sorden: Balance Sheet Item Assets Cash and Receivables Inventory Land Plant and Equipment Less: Accumulated Depreciation Goodwill Total Assets Liabilities and Equities Accounts Payable Common Stock Additional Paid-In Capital Retained Earnings Total Liabilities and Equities Historical Cost $ 56,000 114,000 64,000 414,000 (154,000) 12,000 $ 506,000 $ 49,000 84,000 57,000 316,000 $ 506,000 Fair Value $ 48,000 182,000 92,000 290,000 $ 612,000 $ 49,000 Required: Prepare the journal entry that Planter recorded at the time of exchange. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field.arrow_forward

- HELP MEarrow_forwardPeace Company issued common shares with a par value of $58,000 and a market value of $165,300 in exchange for 30 percent ownership of Symbol Corporation on January 1, 20X2. Symbol reported the following balances on that date: Assets Cash Accounts Receivable Inventory (FIFO basis) Land Buildings & Equipment Less: Accumulated Depreciation Patent Total Assets Liabilities & Equities Accounts Payable SYMBOL CORPORATION Balance Sheet January 1, 20X2 Bonds Payable Common Stock Additional Paid-In Capital Retained Earnings Total Liabilities & Equities Book Value Fair Value $ 57,000 $ 57,000 97,000 97,000 133,000 163,000 55,000 70,000 505,000 326,000 (245,000) Investment income (loss) Balance in the investment account $ 602,000 $ 22,000 172,000 148,000 12,000 248,000 $ 602,000 32,000 $ 745,000 $ 22,000 172,000 The estimated economic life of the patents held by Symbol is 10 years. The buildings and equipment are expected to last 12 more years on average. Symbol paid dividends of $18,000 during…arrow_forwardIf CARDO Co purchases the net assets of SYANO Co by issuing 5,000 shares of their P20 par valueshares with a fair value of P40 per share, incurs a mortgage loan for P90,000, pays P150,000 cash andpaying direct, indirect and stock issue costs of P75,000, P50,000 and P40,000 respective. REQUIREMENTS:A. GoodwillB. Consolidated Total Assets at the date of acquisitionarrow_forward

- In business combination, the fair value of combinee bonds payable was $ 120,000 and the carrying amount of bonds payable was $ 100,000. The journal entry to allocate liquidated company to identifiable assets and liabilities with remainder to goodwill includes: а. Credit to premium on bonds payable $ 20,000. b. Debit to discount on bonds payable $ 20,000. C. Credit to bonds payable $ 120,000. d. Debit to premium on bonds payable $ 20,000arrow_forwardOn January 1, 20x1, ABC Co. acquired 10%, P1,000,000 bonds for P827,135. The bonds mature on December 31, 20x3 and pay annual interest every December 31. ABC Co. incurred transaction costs P80,000 on the acquisition. The effective interest rate adjusted for the effect of the transaction costs is 14%. The bonds are to be held under a "hold to collect and sell" business model. Information on fair values is as follows: December 31, 20x1...............98 December 31, 20x2..............102 December 31, 20x3..............100 9.How much is the carrying amount of the investment on December 31, 20x1? a. 935,134 b. 1,002,000 c. 980,000 d. 965,443 10. How much is the unrealized gain (loss) recognized in other comprehensive income on December 31, 20x1? a. 45,866 b. (45,866) c. (37,899) d. 0 11. How much is the interest income recognized in 20x2? a. 126,999 c. 135,088 b. 130,779 d. 144,388arrow_forwardAcquirer Company purchased the net asset of Acquiree Company (excluding cash) by paying P250,000 cash, issuing shares with a fair value of P1,810,000 and issuing a bond debenture with a fair value of P380,000 on January 2, 2022. The financial statements of Acquirer and Acquiree as of this date were as follows (see image below).The book value reflected the fair value of the assets and liabilities except that the inventory of Acquirer had a fair value of 1,500,000 and the inventory and equipment of Acquiree had fair values of P750,000 and P1,400,000 respectively. Acquirer also incurred the following costs: Finder’s fee – P10,000; Accountant’s fee – P15,000; Legal fees – P7,500; Printing of stock certificates – P5,000; and Audit and accountant’s fee related to stock issuance – P20,000. Acquirer only paid 50% of the said acquisition related costs. Answer the following: a. How much is the Consolidated Equity? b. How much is the Goodwill/Gain on Bargain Purchase? c. How much is the…arrow_forward

- In business combination, the fair value of combinee bonds payable was $ 90,000 and the carrying amount of bonds payable was $ 110,000. The journal entry to allocate liquidated company to identifiable assets and liabilities with remainder to goodwill includes: а. Debit to discount on bonds payable $ 20,000. b. Credit to bonds payable $ 90,000. С. Debit to discount on bonds payable $ 110,000. d. Debit to discount on bonds payable $ 90,000.arrow_forwardAccounting for Asset and Stock Purchases Assume an investor purchases an investee's net assets with a cash payment of $800 and issuance to the investee's shareholders of 160 shares of $1 par value common stock with a current fair value of $19.00 per share. In addition, we assume the purchaser paid an additional $40 of transaction costs to a third party (e.g., appraiser or broker) and provided the seller with contingent consideration with a fair value of $160 at the date of acquisition. The investee has the following net assets at current appraised fair value and historical book value: Plant and equipment Land Patent Total Required Investee Fair Value Investee Book Value $320 $600 840 600 960 80 $2,400 $1,000 a. Provide the journal entry on the investor's books for the purchase of the individual net assets of the investee. Assume the acquired net assets do not qualify as a business. b. Provide the journal entry on the investor's books for the purchase of the individual net assets of the…arrow_forwardBronze Corporation agrees to acquire the net assets of Wall Corporation on January 1, 20X1. Wall has the following balance sheet on the date of acquisition: Wall Corporation Balance Sheet January 1, 20X1 Assets Liabilities and Equity Accounts receivable . . . . . . . . . $ 79,000 Current liabilities . . . . . . . . . . . . . . $145,000 Inventory . . . . . . . . . . . . . . . . . . 112,000 Bonds payable . . . . . . . . . . . . . . . 100,000 Other current assets . . . . . . . . . . 55,000 Common stock . . . . . . . . . . . . . . . . 200,000 Equipment (net) . . . . . . . . . . . . . 294,000 Paid-in capital in excess of par . . . 50,000 Trademark . . . . . . . . . . . . . . . . . 30,000 Retained earnings . . . . . . . . . . . . . 75,000 Total assets. . . . . . . . . . . . . . . $570,000 Total liabilities and equity . . . . . $570,000 An appraiser determines that in-process R&D exists and has an estimated value of $14,000. The appraisal indicates that the following assets have fair…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

Financial Accounting

Accounting

ISBN:9781305088436

Author:Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:Cengage Learning

Financial instruments products; Author: fi-compass;https://www.youtube.com/watch?v=gvxozM3TUIg;License: Standard Youtube License