PRINCIPLES OF TAXATION F/BUS...(LL)

23rd Edition

ISBN: 9781260433197

Author: Jones

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 10, Problem 5AP

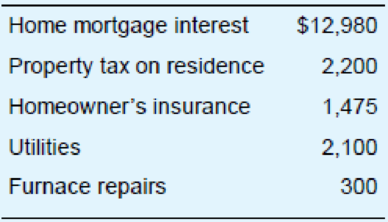

Colin, a self-employed consultant, uses a room of his home as a business office. This room represents 10 percent of the home’s square footage. This year, Colin incurred the following expenses in connection with his home.

Colin purchased the home in 2000 for $225,000. For MACRS

- a. If Colin’s gross business income exceeded his operating expenses by $75,000, compute his net profit for the year.

- b. If Colin’s gross business income exceeded his operating expenses by $1,800, compute his net profit for the year.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Jos is a Sales Manager. He uses his own car to travel to various locations. He acquired the car on 1 October 2021 for $60,000. The acquisition cost was funded entirely by a loan at an interest rate of 15%. He has determined that the depreciation deduction on the car would be $2,300 for the year. In addition, Jos incurred the following expenses during the year:

Registration and insurance = $2,000;

Repairs and maintenance = $1,000; and

Oil and fuel costs = $1,500.

For the period 1 October 2021 to 30 June 2022, Jos estimates that the car travelled 15,000 kilometres, 12,000 of which were for business purposes. You may assume that Jos has maintained all necessary records and a logbook.

Required:

Calculate Jos's deduction for car expenses under the two methods (cent per kilometre rate 0.72 and logbook) in Div 28 of Income Tax Assessment Act 1997. Assume that depreciation has been adjusted for part-year use and the impact of the car limit

Chapter 10 Solutions

PRINCIPLES OF TAXATION F/BUS...(LL)

Ch. 10 - Can a sole proprietorship be described as a...Ch. 10 - Mrs. Liu owns a business as a sole proprietor....Ch. 10 - This year, Mr. Pitts sole proprietorship generated...Ch. 10 - This year, Firm Q, a cash basis taxpayer, remitted...Ch. 10 - Prob. 5QPDCh. 10 - Define the tax base for the self-employment tax....Ch. 10 - Prob. 7QPDCh. 10 - Prob. 8QPDCh. 10 - Prob. 9QPDCh. 10 - Prob. 10QPD

Ch. 10 - Prob. 11QPDCh. 10 - Prob. 12QPDCh. 10 - Prob. 13QPDCh. 10 - Prob. 14QPDCh. 10 - Prob. 2APCh. 10 - Prob. 3APCh. 10 - Prob. 4APCh. 10 - Colin, a self-employed consultant, uses a room of...Ch. 10 - Prob. 6APCh. 10 - Prob. 7APCh. 10 - For 2019, Ms. Deming earned wages totaling...Ch. 10 - Calculate the total Social Security and Medicare...Ch. 10 - Prob. 11APCh. 10 - Prob. 12APCh. 10 - Jane is a self-employed attorney. This year, her...Ch. 10 - Prob. 14APCh. 10 - Prob. 15APCh. 10 - Amit is a limited partner in Reynolds Partnership....Ch. 10 - Kari is a limited partner in Lizard Partnership....Ch. 10 - Rochelle is a limited partner in Megawatt...Ch. 10 - Prob. 19APCh. 10 - Prob. 20APCh. 10 - Prob. 21APCh. 10 - Prob. 23APCh. 10 - AV Inc. is a member of an LLC. This year, AV...Ch. 10 - Prob. 25APCh. 10 - Prob. 26APCh. 10 - Prob. 27APCh. 10 - Prob. 28APCh. 10 - Prob. 29APCh. 10 - Refer to the facts in the preceding problem. BLS...Ch. 10 - Refer to the facts in part (c) of the preceding...Ch. 10 - For each of the following situations, indicate...Ch. 10 - a. If Video Associates is a partnership, and her...Ch. 10 - Prob. 34APCh. 10 - Prob. 1IRPCh. 10 - Javier is a full-time employee of B Inc. and...Ch. 10 - Mr. and Mrs. Chou file a joint income tax return....Ch. 10 - Travis is a professional writer who maintains his...Ch. 10 - Prob. 5IRPCh. 10 - Prob. 6IRPCh. 10 - Prob. 7IRPCh. 10 - Prob. 8IRPCh. 10 - Prob. 9IRPCh. 10 - Paulas Schedule K-1 from an LLC reported a 12,000...Ch. 10 - Marcus, a cash basis individual, is a general...Ch. 10 - Prob. 12IRPCh. 10 - Mr. and Mrs. West are the only shareholders in WW,...Ch. 10 - Prob. 14IRPCh. 10 - Prob. 15IRPCh. 10 - Prob. 16IRPCh. 10 - Prob. 17IRPCh. 10 - Prob. 1RPCh. 10 - Prob. 2RPCh. 10 - Herold had been a calendar year S corporation...Ch. 10 - Prob. 4RPCh. 10 - Mr. and Mrs. Janus operate a restaurant business...Ch. 10 - Prob. 2TPCCh. 10 - Prob. 3TPCCh. 10 - Marla recently inherited 50,000 and is considering...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Lew is a practicing CPA who decides to raise bonsai as a business. Lew engages in the activity and has the following revenue and expenses: Sales $ 5,000 Depreciation on greenhouse 10,000 Fertilizer, soil, pots 1,500 What are the factors that the IRS will consider when evaluating whether the activity is a business or a hobby? ___________________________________________________________________________ ___________________________________________________________________________ ___________________________________________________________________________ If the activity is deemed to be a regular business, what is the amount of Lew's loss from the activity? $_____________ If the activity is deemed to be a hobby, what is the amount of Lew's expenses (if any) from the activity that may be deducted? $_____________arrow_forwardJohn owns a second home in Palm Springs, CA. During the year, he rented the house for $5,000 for 56 days and used the house for 14 days during the summer. The house remained vacant during the remainder of the year. The expenses for the home included $5,000 in mortgage interest, $850 in property taxes, $900 for utilities and maintenance, and $3,500 of depreciation. What is John's deductible rental loss, before considering the passive loss limitations? $200 $875 $2,500 $3,200 $0arrow_forward

Recommended textbooks for you

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income Taxes

Accounting

ISBN:9780357109731

Author:Hoffman

Publisher:CENGAGE LEARNING - CONSIGNMENT

Operating Loss Carryback and Carryforward; Author: SuperfastCPA;https://www.youtube.com/watch?v=XiYhgzSGDAk;License: Standard Youtube License