a.

Prepare the general

a.

Explanation of Solution

Journal entry:

Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Accounting rules for Journal entries:

- To record increase balance of account: Debit assets, expenses, losses and credit liabilities, capital, revenue and gains.

- To record decrease balance of account: Credit assets, expenses, losses and debit liabilities, capital, revenue and gains.

Prepare the general journal entry of Incorporation PSS as follows:

| Event | Account title and explanation | Debit | Credit |

| 1 | Sales Tax Payable | 390 | |

| Cash | 390 | ||

| (To record cash paid to sales tax) | |||

| 2 | Employee Income Tax Payable | 1,000 | |

| FICA – Social Security Tax Payable | 840 | ||

| FICA – Medicare Tax Payable | 210 | ||

| 945 | |||

| Cash | 2,995 | ||

| (To record cash paid to the payroll liabilities) | |||

| 3a. | Cash (5,000 x $8) | 40,000 | |

| Common Stock (5,000 x $5) | 25,000 | ||

| PIC in Excess of Par CS | 15,000 | ||

| (To record common stock issued in excess of par value of $8 per share) | |||

| 3b. | Cash (1,000 x $52) | 52,000 | |

| 50,000 | |||

|

Paid in capital in excess of par, Preferred stock | 2,000 | ||

| (To record preferred stock issued in excess of par value of $50 per share) | |||

| 4 | Supplies | 500 | |

| Accounts Payable | 500 | ||

| (To record supplies purchased on accounts) | |||

| 5 | Merchandise Inventory (190 x $310) | 58,900 | |

| Cash | 58,900 | ||

| (To record merchandise inventory purchased on accounts) | |||

| 6 | Allowance for Doubtful Accounts | 3,670 | |

| 3,670 | |||

| (To reverse the write off of Company 's accounts) | |||

| 7a. | Accounts Receivable | 132,300 | |

| Alarm Sales Revenue (210 x $600) | 126,000 | ||

| Sales Tax Payable (210 x $600 x5%) | 6,300 | ||

| (To record the sale of alarm system on account plus sales tax) | |||

| 7b. | Cost of Goods Sold (1) | 64,620 | |

| Merchandise Inventory | 64,620 | ||

| (To record merchandise inventory transferred to the production) | |||

| 8 | Accounts Receivable – Credit Card | 55,680 | |

| Accounts Receivable | 67,000 | ||

| Credit Card Expense (58,000 x 4%) | 2,320 | ||

| Monitoring Service Revenue | 125,000 | ||

| (To record service revenue received on account, and credit cards) | |||

| 9 | Maintenance Expense | 75 | |

| Office Supplies Expense | 15 | ||

| Cash | 90 | ||

| (To record maintenance and office supplies expense paid in cash) | |||

| 10 | Cash | 55,680 | |

| Accounts Receivable – Credit Card | 55,680 | ||

| (To record cash received from the credit card customers) | |||

| 11 | Sales Tax Payable ($105,000 x 5%) | 5,250 | |

| Cash | 5,250 | ||

| (To record sale tax paid in cash) | |||

| 12 | Cash | 198,000 | |

| Accounts Receivable | 198,000 | ||

| (To record cash received from the credit customers) | |||

| 13 | Salaries Expense | 96,000 | |

| Employee Income Tax Payable | 10,600 | ||

| FICA Tax – Social Security Tax Payable (2) | 5,760 | ||

| FICA Tax – Medicare Payable (3) | 1,440 | ||

| Cash | 78,200 | ||

| (To record salaries expense paid to employees) | |||

| 14 | Dividends (4) | 17,500 | |

| Dividends Payable | 17,500 | ||

| (To record dividends declared to the shareholders) | |||

| 15 | Warranty Payable | 1,625 | |

| Cash | 1,625 | ||

| (To record warranty paid for repairs) | |||

| 16 | Dividends Payable | 17,500 | |

| Cash | 17,500 | ||

| (To record cash dividends paid to shareholders) | |||

| 17 | Advertising Expense | 18,500 | |

| Cash | 18,500 | ||

| (To record advertising expense paid in cash) | |||

| 18 | Utilities Expense | 6,100 | |

| Cash | 6,100 | ||

| (To record utilities expense paid in cash) | |||

| 19 | Payroll Tax Expense (5) | 6,600 | |

| Employee Income Tax Payable | 9,200 | ||

| FICA Tax – Social Security Tax Payable (6) | 5,280 | ||

| FICA Tax – Medicare Tax Payable (7) | 1,320 | ||

| Cash | 22,400 | ||

| (To record payroll tax and employee income tax paid in cash) | |||

| 20 | Accounts Payable | 500 | |

| Cash | 500 | ||

| (To record cash paid to suppliers) | |||

| 21 | Interest Expense | 3,200 | |

| Discount on Bonds Payable (1,000 ÷ 5) | 200 | ||

| Cash ($50,000 x 6%) | 3,000 | ||

| (To record interest expense paid in cash, and discount adjusted with the interest expense) | |||

| 22 | Interest Expense ($92,762 x 7%) | 6,493 | |

| Notes Payable | 7,745 | ||

| Cash | 14,238 | ||

| (To record principle and interest amount paid in cash) | |||

| 23 | Supplies Expense ($210 + $500 - $190) | 520 | |

| Supplies | 520 | ||

| (To record supplies expense incurred at the end of the accounting year) | |||

| 24 | Uncollectible Accounts Expense (8) | 1,993 | |

| Allowance for Doubtful Accounts | 1,993 | ||

| (To record uncollectible accounts expense incurred at the end of the accounting year) | |||

| 25 | 4,275 | ||

| 4,275 | |||

| (To record depreciation expense incurred at the end of the accounting year) | |||

| 26 | Warranty Expense | 2,520 | |

| Warranty Payable | 2,520 | ||

| (To record warranty expense paid to customers) | |||

| 27 | Payroll Tax Expense ($21,000 x 4.5%) | 945 | |

| Unemployment Tax Payable | 945 | ||

| (To record unemployment tax incurred at the end of the accounting year, and adjusted with the payroll tax expense) | |||

| 28 | Payroll Tax Expense | 600 | |

| FICA – Social Security Tax Payable (8,000 x 6%) | 480 | ||

| FICA – Medicare Tax Payable (8,000 x 1.5%) | 120 | ||

| (To record social and medical payroll tax incurred at the end of the accounting year and adjusted with the payroll tax expense) |

Table (1)

Working notes:

Calculate the cost of goods sold for transaction 7b:

| Cost of goods sold | ||

| Unit (A) |

Cost per unit ($) (B) | Total |

| 48 | 300 | $14,400 |

| 162 | 310 | $50,220 |

| Total Cost of goods sold | $64,620 | |

Table (2) (1)

Calculate FICA– Social security tax payable for transaction 13:

Calculate FICA – Medicare tax payable for transaction 13:

Calculate the amount of dividend declared in transaction 14.

| Dividend: | Amount |

|

Declared dividend on preferred stock | $2,500 |

|

Dividend declared on common stock | $15,000 |

| Total dividends | $17,500 |

Table (3) (4)

Calculate payroll tax expense for transaction 19:

Calculate FICA – Social security tax payable for transaction 19:

Calculate FICA – Medicare tax payable for transaction 19:

Calculate uncollectible accounts expense for transaction 24:

| Particulars | Amount |

| Alarm sales on account | $132,300 |

| Add: Monitoring service revenue | $67,000 |

| Total credit sales (A) | $199,300 |

| Estimated uncollectible percent (B) | 1% |

| Uncollectible Account expense (A÷B) | $1,993 |

Table (4) (8)

Calculate the depreciation expense for equipment using straight line method:

Calculate depreciation expense of building using straight line method:

Calculation of total depreciation expense for transaction 25:

b.

Post the transactions of T-Accounts for Incorporation PSS.

b.

Explanation of Solution

T-account:

T-account is the form of the ledger account, where the journal

The components of the T-account are as follows:

a) The title of the account

b) The left or debit side

c) The right or credit side

Post the transactions of T-Accounts for Incorporation PSS as follows:

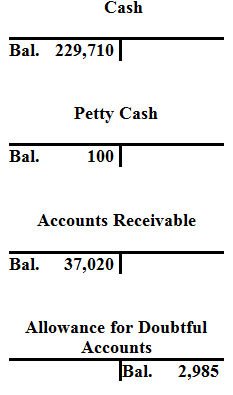

| Cash | |||

| Bal. | 113,718 | 1 | 390 |

| 3a. | 40,000 | 2 | 2,995 |

| 3b. | 52,000 | 5 | 58,900 |

| 10 | 55,680 | 9 | 90 |

| 12 | 198,000 | 11 | 5,250 |

| 13 | 78,200 | ||

| 15 | 1,625 | ||

| 16 | 17,500 | ||

| 17 | 18,500 | ||

| 18 | 6,100 | ||

| 19 | 22,400 | ||

| 20 | 500 | ||

| 21 | 3,000 | ||

| 22 | 14,238 | ||

| Bal. | 229,710 | ||

| Petty Cash | |||

| Bal. | 100 | ||

| Accounts Receivable | |||

| Bal. | 39,390 | ||

| 7a. | 132,300 | 6 | 3,670 |

| 8 | 67,000 | 12 | 198,000 |

| Bal. | 37,020 | ||

| Accounts Receivable Credit Cards | |||

| 8 | 55,680 | 10 | 55,680 |

| Bal. | -0- | ||

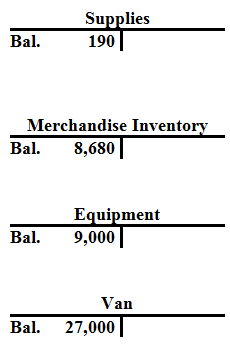

| Supplies | |||

| Bal. | 210 | ||

| 4 | 500 | 23 | 520 |

| Bal. | 190 | ||

| Merchandise Inventory | |||

| Bal. | 14,400 | 7b. | 64,620 |

| 5 | 58,900 | ||

| Bal. | 8,680 | ||

| Equipment | |||

| Bal. | 9,000 | ||

| Van | |||

| Bal. | 27,000 | ||

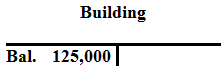

| Building | |||

| Bal. | 125,000 | ||

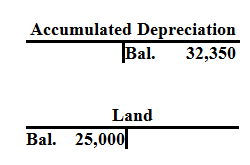

| Accumulated Depreciation | |||

| Bal. | 28,075 | ||

| 25 | 4,275 | ||

| Bal. | 32,350 | ||

| Land | |||

| Bal. | 25,000 | ||

| Accounts Payable | |||

| 20 | 500 | 4 | 500 |

| Bal. | -0- | ||

| Dividends Payable | |||

| 16 | 17,500 | 14 | 17,500 |

| Bal. | -0- | ||

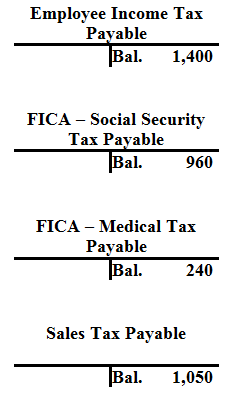

| Employee Income Tax Payable | |||

| Bal. | 1,000 | ||

| 2 | 1,000 | 13 | 10,600 |

| 19 | 9,200 | ||

| Bal. | 1,400 | ||

| FICA - Social Security Tax Payable | |||

| Bal. | 840 | ||

| 2 | 840 | 13 | 5,760 |

| 19 | 5,280 | 28 | 480 |

| Bal. | 960 | ||

| FICA - Medical Tax Payable | |||

| Bal. | 210 | ||

| 2 | 210 | 13 | 1,440 |

| 19 | 1,320 | 28 | 120 |

| Bal. | 240 | ||

| Sales Tax Payable | |||

| Bal. | 390 | ||

| 1 | 390 | 7a. | 6,300 |

| 11 | 5,250 | ||

| Bal. | 1,050 | ||

| Warranty Payable | |||

| Bal. | 918 | ||

| 15 | 1,625 | 26 | 2,520 |

| Bal. | 1,813 | ||

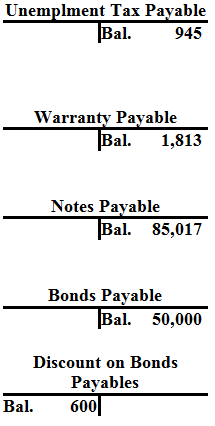

| Unemployment Tax Payable | |||

| Bal. | 945 | ||

| 2 | 945 | 27 | 945 |

| Bal. | 945 | ||

| Notes Payable | |||

| Bal. | 92,762 | ||

| 22 | 7,745 | ||

| Bal. | 85,017 | ||

| Bonds Payable | ||||||

| Bal. | 50,000 | |||||

| Discount on Bonds Payable | ||||||

| Bal. | 800 | 21 | 200 | |||

| Bal. | 600 | |||||

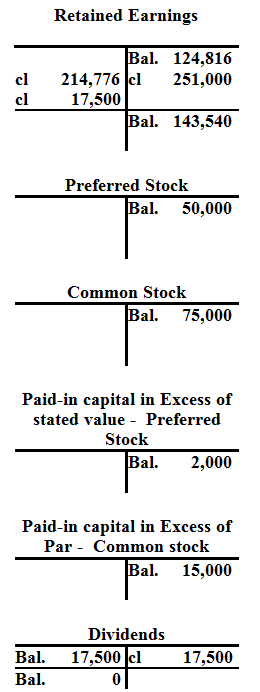

| Bal. | 124,816 | ||

| Preferred Stock | |||

| 3b. | 50,000 | ||

| Bal. | 50,000 | ||

| Common Stock | |||

| Bal. | 50,000 | ||

| 3a. | 25,000 | ||

| Bal. | 75,000 | ||

| Paid in capital in Excess Common stock | |||

| 3a. | 15,000 | ||

| Bal. | 15,000 | ||

| Paid in capital in Excess Preferred stock | |||

| 3b. | 2,000 | ||

| Bal. | 2,000 | ||

| Dividends | |||

| 14 | 17,500 | ||

| Bal. | 17,500 | ||

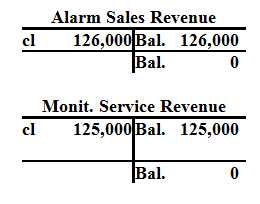

| Alarm Sales Revenue | |||

| 7a. | 126,000 | ||

| Bal. | 126,000 | ||

| Monitoring Service Revenue | |||

| 8 | 125,000 | ||

| Bal. | 125,000 | ||

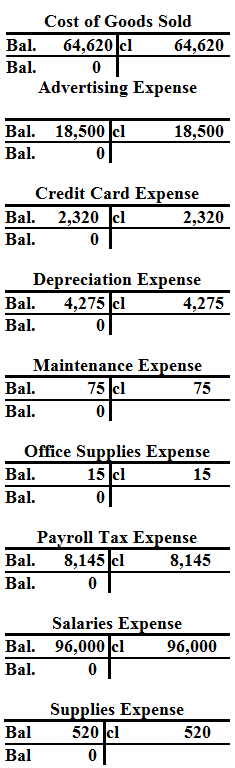

| Cost of Goods Sold | |||

| 7b. | 64,620 | ||

| Bal. | 64,620 | ||

| Advertising Expense | |||

| 17 | 18,500 | ||

| Bal. | 18,500 | ||

| Credit Card Expense | |||

| 8 | 2,320 | ||

| Bal. | 2,320 | ||

| Depreciation Expense | |||

| 25 | 4,275 | ||

| Bal. | 4,275 | ||

| Maintenance Expense | |||

| 9 | 75 | ||

| Bal. | 75 | ||

| Payroll Tax Expense | ||||

| 19. | 6,600 | |||

| 27. | 945 | |||

| 28. | 600 | |||

| Bal. | 8,145 | |||

| Office Supplies Expense | |||

| 9. | 15 | ||

| Bal. | 15 | ||

| Salaries Expense | ||||

| 13. | 96,000 | |||

| Bal. | 96,000 | |||

| Supplies Expense | |||

| 23. | 520 | ||

| Bal. | 520 | ||

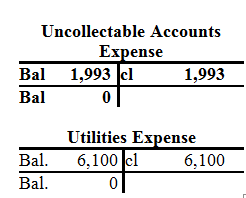

| Uncollectible Accounts Expense | |||

| 24. | 1,993 | ||

| Bal. | 1,993 | ||

| Utilities Expense | |||

| 18. | 6,100 | ||

| Bal. | 6,100 | ||

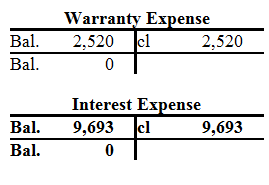

| Warranty Expense | |||

| 26. | 2,520 | ||

| Bal. | 2,520 | ||

| Interest Expense | |||

| 21. | 3,200 | ||

| 22. | 6,493 | ||

| Bal. | 9,693 | ||

c.

Prepare trail balance of Incorporation PSS.

c.

Explanation of Solution

Trial balance:

A trial balance is the summary of all the ledger accounts. The trial balance is prepared to check the total balance of the debit column with the total of the balance of the credit column, which must be equal. The trial balance is usually prepared to check accuracy of ledger accounts balances before the preparation of financial statements.

Prepare trial balance of Incorporation PSS as follows:

| Incorporation PSS | ||

| Trial Balance | ||

| December 31, Year 11 | ||

| Account title | Amount | Amount |

| Cash | $229,710 | |

| Petty Cash | 100 | |

| Accounts Receivable | 37,020 | |

| Allowance for Doubtful Accounts | $2,985 | |

| Supplies | 190 | |

| Merchandise Inventory | 8,680 | |

| Equipment | 9,000 | |

| Van | 27,000 | |

| Building | 125,000 | |

| Accumulated Depreciation | 32,350 | |

| Land | 25,000 | |

| Employee Income Tax Payable | 1,400 | |

| FICA – Social Security Tax Payable | 960 | |

| FICA – Medicare Tax Payable | 240 | |

| Sales Tax Payable | 1,050 | |

| Warranty Payable | 1,813 | |

| Unemployment Tax Payable | 945 | |

| Notes Payable | 85,017 | |

| Bonds Payable | 50,000 | |

| Discount on Bonds Payable | 600 | |

| Preferred Stock | 50,000 | |

| Common Stock | 75,000 | |

| Paid in capital in Excess of Stated Value Preferred Stock | 2,000 | |

| Paid in capital in Excess of Par Common Stock | 15,000 | |

| Retained Earnings | 124,816 | |

| Dividends | 17,500 | |

| Alarms Sales Revenue | 126,000 | |

| Monitoring Service Revenue | 125,000 | |

| Cost of Goods Sold | 64,620 | |

| Advertising Expense | 18,500 | |

| Credit Card Expense | 2,320 | |

| Depreciation Expense | 4,275 | |

| Maintenance Expense | 75 | |

| Payroll Tax Expense | 8,145 | |

| Office Supplies Expense | 15 | |

| Salaries Expense | 96,000 | |

| Supplies Expense | 520 | |

| Uncollectible Accounts Expense | 1,993 | |

| Utilities Expense | 6,100 | |

| Warranty Expense | 2,520 | |

| Interest Expense | 9,693 | |

| Totals | $694,576 | $694,576 |

Table (5)

d.

Prepare an income statement, balance sheet, and statement of cash flows of Incorporation PSS.

d.

Explanation of Solution

Income statement:

Income statement is a financial statement that shows the net income or net loss by deducting the expenses from the revenues.

Prepare the income statement of Incorporation PSS as follows:

| Incorporation PSS | ||

| Income Statement | ||

| December 31, Year 11 | ||

| Revenues | ||

| Monitoring Service Revenue | $125,000 | |

| Alarm Sales Revenue | 126,000 | |

| Less: Cost of Goods Sold | -64,620 | |

| Gross Margin | 186,380 | |

| Less: Operating Expenses | ||

| Advertising Expense | $18,500 | |

| Credit Card Expense | 2,320 | |

| Depreciation Expense | 4,275 | |

| Maintenance Expense | 75 | |

| Office Supplies Expense | 15 | |

| Payroll Tax Expense | 8,145 | |

| Salaries Expense | 96,000 | |

| Supplies Expense | 520 | |

| Uncollectible Accounts Expense | 1,993 | |

| Utilities Expense | 6,100 | |

| Warranty Expense | 2,520 | |

| Total Operating Expenses | 140,463 | |

| Net Operating Income | 45,917 | |

| Non-Operating Expense: | ||

| Interest Expense | -9,693 | |

| Net Income | $36,224 | |

Table (6)

Balance Sheet:

Balance Sheet summarizes the assets, the liabilities, and the Shareholder’s equity of a company at a given date. It is also known as the statement of financial status of the business.

Prepare the Balance sheet of Incorporation PSS as follows:

| Incorporation PSS | ||

| Balance sheet | ||

| December 31, Year 11 | ||

| Assets | Amount | Amount |

| Cash | $229,710 | |

| Petty Cash | 100 | |

| Accounts Receivable | $37,020 | |

| Allowance for Doubtful Accounts | -2,985 | 34,035 |

| Supplies | 190 | |

| Merchandise Inventory | 8,680 | |

| Equipment | 9,000 | |

| Van | 27,000 | |

| Building | 125,000 | |

| Accumulated Depreciation | -32,350 | 128,650 |

| Land | 25,000 | |

| Total Assets | $426,365 | |

| Liabilities and stockholders' equity | Amount | Amount |

| Liabilities: | ||

| Employee Tax Payable | $1,400 | |

| FICA -Social Security Tax Payable | 960 | |

| FICA - Medicare Tax Payable | 240 | |

| Sales Tax Payable | 1,050 | |

| Unemployment Tax Payable | 945 | |

| Warranty Payable | 1,813 | |

| Notes Payable | 85,017 | |

| Bonds Payable | $50,000 | |

| Discount on Bonds Payable | -600 | 49,400 |

| Total Liabilities | $140,825 | |

| Stockholders’ Equity: | ||

| Preferred Stock, $50 Stated Value, 5% Cumulative, 1,000 shares issued and outstanding | $50,000 | |

| Common Stock, $5 par value, 15,000 shares issued and outstanding | 75,000 | |

| Paid-in Capital in Excess of Stated Value, Preferred | 2,000 | |

| Pain-in Capital in Excess of Par, Common Stock | 15,000 | |

| Total Paid-in Capital | 142,000 | |

| Retained Earnings | 143,540 | |

| Total Stockholders’ Equity | 285,540 | |

| Total Liabilities and Stockholders’ Equity | $426,365 | |

Table (7)

Statement of cash flows:

Statement of cash flows reports all the cash transactions which are responsible for inflow and outflow of cash and result of these transactions is reported as ending balance of cash at the end of reported period.

Prepare the statement of cash flows for Incorporation PSS as follows:

| Incorporation PSS | ||

| Statement of Cash Flows | ||

| For the Year Ended December 31, Year 11 | ||

| Cash Flows From Operating Activities: | ||

| Cash Receipts from Customers (12) | $253,680 | |

| Cash Payment for Expenses (13) | -189,310 | |

| Cash Payment for Sales Tax Payable | -5,640 | |

| Cash Payment for Interest | -9,493 | |

| Net Cash Flow from Operating Activities | $49,237 | |

| Cash Flows From Investing Activities | 0 | 0 |

| Cash Flows From Financing Activities: | ||

| Cash Inflow from Stock Issue | $92,000 | |

| Cash Payment on Notes Payable | -7,745 | |

| Cash Payments for Dividends | -17,500 | |

| Net Cash Flow from Financing Activities | 66,755 | |

| Net Increase in Cash | 115,992 | |

| Plus: Beginning Cash Balance | 113,718 | |

| Ending Cash Balance | $229,710 | |

Table (8)

Working notes:

Calculate total cash from customers.

| Particulars | Amount |

| Collection of Accounts Receivable | $198,000 |

| Add: Collection of credit cards | $55,680 |

| Total cash from customers | $253,680 |

Table (9) (12)

Calculate total cash payment for expenses.

| Particulars | Amount |

| Payment of compensation and related taxes | $103,595 |

| Payment of inventory | $58,900 |

| Payment of accounts payable | $500 |

| Payment of advertising | $18,500 |

| Payment for Utilities expense | $6,100 |

| Payment for warranty expense | $1,625 |

| Payment for Expense from petty cash | $90 |

| Total cash payment for expenses | $189,310 |

Table (10) (13)

e.

Prepare journal entry to close the temporary accounts to retained earnings of Incorporation PSS.

e.

Explanation of Solution

Closing entries:

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Prepare to close the temporary accounts to retained earnings of Incorporation PSS as follows:

| Date | Account titles and Explanation | Debit | Credit |

| December 31 | Alarm sales revenue | 126,000 | |

| Monitoring service revenue | 125,000 | ||

| Retained earnings | 251,000 | ||

| (To close all revenue accounts) | |||

| December 31 | Retained earnings | 214,776 | |

| Cost of goods sold | 64,620 | ||

| Advertising expense | 18,500 | ||

| Credit card expense | 2,320 | ||

| Depreciation expense | 4,275 | ||

| Maintenance expense | 75 | ||

| Office supplies expense | 15 | ||

| Payroll tax expense | 8,145 | ||

| Salaries expense | 96,000 | ||

| Supplies expense | 520 | ||

| Uncollectible accounts expense | 1,993 | ||

| Utilities expense | 6,100 | ||

| Warranty expense | 2,520 | ||

| Interest Expense | 9,693 | ||

| (To close all expenses accounts) | |||

| December 31 | Retained earnings | $17,500 | |

| Dividends | $17,500 | ||

| (To record dividend account) |

Table (11)

f.

Post the closing entries to the T-Accounts and prepare an after closing trail balance of Incorporation PSS.

f.

Explanation of Solution

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

Post the closing entries to the T- Accounts of Incorporation PSS as follows:

Prepare post -closing trail balance of Incorporation PSS as follows:

| Incorporation PSS | ||

| Post-Closing Trial Balance | ||

| December 31, Year 11 | ||

| Account Titles | Debit | Credit |

| Cash | $229,710 | |

| Petty Cash | 100 | |

| Accounts Receivable | 37,020 | |

| Allowance for Doubtful Accounts | $2,985 | |

| Supplies | 190 | |

| Merchandise Inventory | 8,680 | |

| Equipment | 9,000 | |

| Van | 27,000 | |

| Building | 125,000 | |

| Accumulated Depreciation | 32,350 | |

| Land | 25,000 | |

| Employee Income Tax Payable | 1,400 | |

| FICA – Social Security Tax Payable | 960 | |

| FICA – Medicare Tax Payable | 240 | |

| Sales Tax Payable | 1,050 | |

| Warranty Payable | 1,813 | |

| Unemployment Tax Payable | 945 | |

| Notes Payable | 85,017 | |

| Bonds Payable | 50,000 | |

| Discount on Bonds Payable | 600 | |

| Preferred Stock | 50,000 | |

| Common Stock | 75,000 | |

| Paid-in Capital in Excess of Stated value, Preferred stock | 2,000 | |

| Paid-in Capital in Excess of Par, Common stock | 15,000 | |

| Retained Earnings | 143,540 | |

| Totals | $462,300 | $462,300 |

Table (12)

Want to see more full solutions like this?

Chapter 11 Solutions

Connect Access Card for Fundamental Financial Accounting Concepts

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education