Concept explainers

Videos

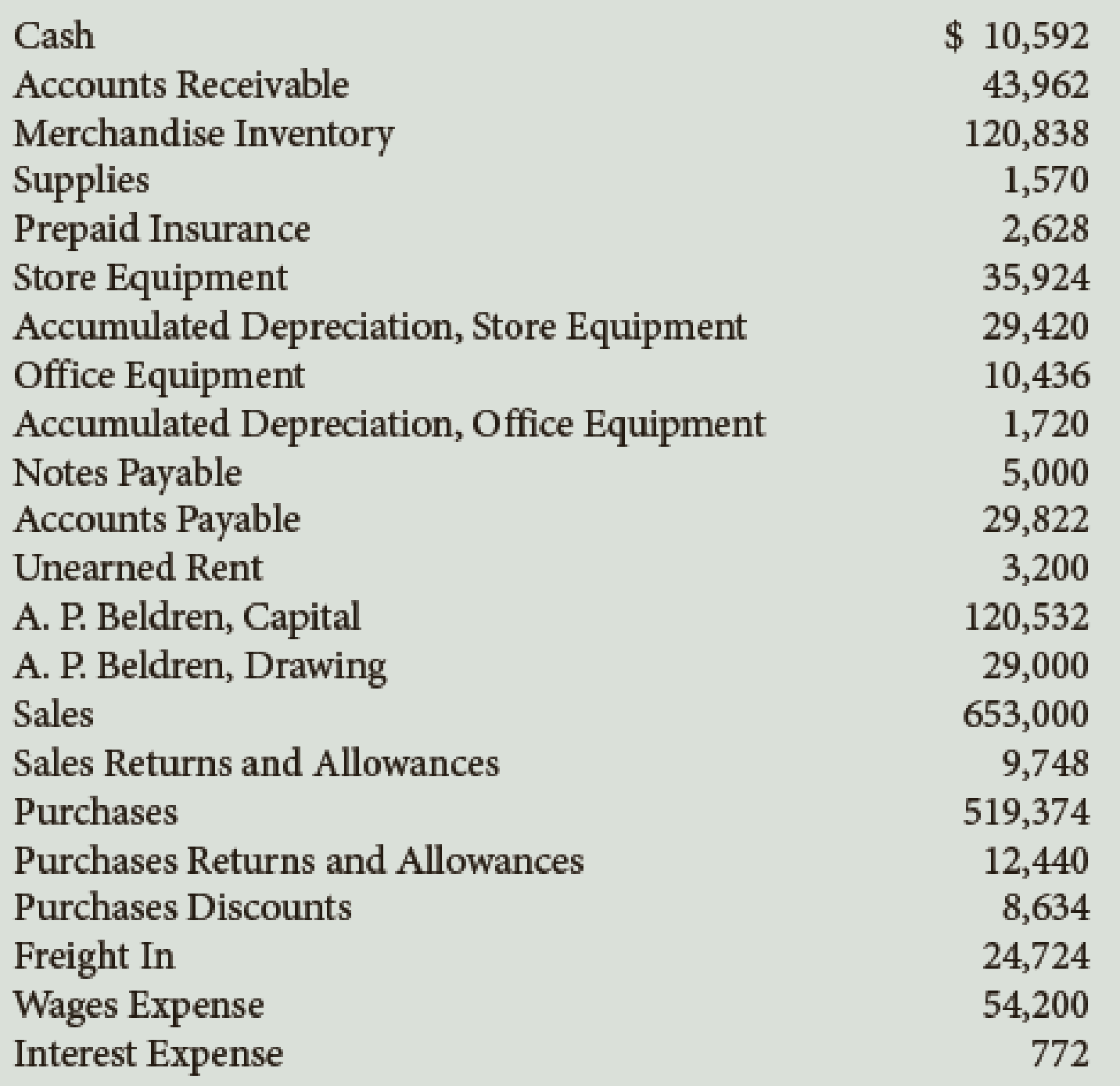

The balances of the ledger accounts of Beldren Home Center as of December 31, the end of its fiscal year, are as follows:

Data for the adjustments are as follows:

a–b. Merchandise Inventory at December 31, $102,765.

c. Wages accrued at December 31, $1,834.

d. Supplies inventory (on hand) at December 31, $645.

e.

f. Depreciation of office equipment, $1,791.

g. Insurance expired during the year, $845.

h. Rent earned, $2,500.

Required

- 1. Complete the work sheet after entering the account names and balances onto the work sheet. Ignore this step if using CLGL.

- 2. Journalize the

adjusting entries . If using manual working papers, record adjusting entries on journal page 16.

Trending nowThis is a popular solution!

Chapter 11 Solutions

Bundle: College Accounting: A Career Approach (with QuickBooks Online), Loose-leaf Version, 13th + LMS Integrated CengageNOWV2, 1 term (6 months) Printed Access

Additional Business Textbook Solutions

Financial Accounting

Managerial Accounting (5th Edition)

Advanced Financial Accounting

Managerial Accounting: Tools for Business Decision Making

Accounting for Governmental & Nonprofit Entities

- The following accounts appear in the ledger of Celso and Company as of June 30, the end of this fiscal year. The data needed for the adjustments on June 30 are as follows: ab.Merchandise inventory, June 30, 54,600. c.Insurance expired for the year, 475. d.Depreciation for the year, 4,380. e.Accrued wages on June 30, 1,492. f.Supplies on hand at the end of the year, 100. Required 1. Prepare a work sheet for the fiscal year ended June 30. Ignore this step if using CLGL. 2. Prepare an income statement. 3. Prepare a statement of owners equity. No additional investments were made during the year. 4. Prepare a balance sheet. 5. Journalize the adjusting entries. 6. Journalize the closing entries. 7. Journalize the reversing entry as of July 1, for the wages that were accrued in the June adjusting entry. Check Figure Net income, 14,066arrow_forwardThe following accounts appear in the ledger of Sheldon Company on January 31, the end of this fiscal year. The data needed for adjustments on January 31 are as follows: ab.Merchandise inventory, January 31, 55,750. c.Insurance expired for the year, 1,285. d.Depreciation for the year, 5,482. e.Accrued wages on January 31, 1,556. f.Supplies used during the year 1,503. Required 1. Prepare a work sheet for the fiscal year ended January 31. Ignore this step if using QuickBooks or general ledger. 2. Prepare an income statement. 3. Prepare a statement of owners equity. No additional investments were made during the year. Ignore this step if using CLGL. 4. Prepare a balance sheet. 5. Journalize the adjusting entries. 6. Journalize the closing entries. Check Figure Net loss, 1,737arrow_forwardHere are the accounts in the ledger of Mishas Jewel Box, with the balances as of December 31, the end of its fiscal year. Here are the data for the adjustments. Assume that Mishas Jewel Box uses the perpetual inventory system. a. Merchandise Inventory at December 31, 124,630. b. Insurance expired during the year, 1,294. c. Depreciation of building, 3,300. d. Depreciation of store equipment, 6,470. e. Salaries accrued at December 31, 2,470. f. Store supplies inventory (on hand) at December 31, 1,959. Required 1. Complete the work sheet after entering the account names and balances onto the work sheet. Ignore this step if using CLGL. 2. Journalize the adjusting entries. If using manual working papers, record adjusting entries on journal page 63.arrow_forward

- On December 31, Pitts Manufacturing Company reports the following assets: What is the total amount of Pitts inventory at year-end?arrow_forwardThe balances of the ledger accounts of Pelango Furniture as of December 31, the end of its fiscal year, are as follows: Data for the adjustments are as follows: ab. Merchandise Inventory at December 31, 104,565. c. Wages accrued at December 31, 934. d. Supplies inventory (on hand) at December 31, 755. e. Depreciation of store equipment, 4,982. f. Depreciation of office equipment, 1,531. g. Insurance expired during the year, 935. h. Rent earned, 2,450. Required 1. Complete the work sheet after entering the account names and balances onto the work sheet. Ignore this step if using CLGL. 2. Journalize the adjusting entries. If using manual working papers, record adjusting entries on journal page 16.arrow_forwardThe following selected information is taken from the financial statements of Arnn Company for its most recent year of operations: During the year, Arnn had net sales of 2.45 million. The cost of goods sold was 1.3 million. Required: Note: Round all answers to two decimal places. 1. Compute the current ratio. 2. Compute the quick or acid-test ratio. 3. Compute the accounts receivable turnover ratio. 4. Compute the accounts receivable turnover in days. 5. Compute the inventory turnover ratio. 6. Compute the inventory turnover in days.arrow_forward

- Based on the following data for the current year, what is the inventory turnover (rounded to one decimal place)? Sales on account during year $471,903 Cost of merchandise sold during year 217,752 Accounts receivable, beginning of year 46,168 Accounts receivable, end of year 54,621 Merchandise inventory, beginning of year 34,350 Merchandise inventory, end of year 42,090arrow_forwardValley Company's adjusted account balances from its general ledger on August 31, its fiscal year-end, follows. It categorizes the following accounts as selling expenses: sales salaries expense, rent expense-selling space, store supplies expense, and advertising expense. It categorizes the remaining expenses as general and administrative. Adjusted Account Balances Debit Credit Merchandise inventory (ending) $ 34,000 Other (non-inventory) assets 136,000 Total liabilities $ 39,270 Common stock 67,851 Retained earnings 45, 768 Dividends 8,000 Sales 232, 560 Sales discounts 3,558 Sales returns and allowances 15,349 Cost of goods sold 90, 401 Sales salaries expense 31,861 Rent expense-Selling space 10, 930 Store supplies expense 2, 791 Advertising expense 19,768 Office salaries expense 29,070 Rent expense-Office space 2,791 Office supplies expense 930 Totals $385, 449 $385, 449 Beginning merchandise inventory was $27,438. Supplementary records of merchandising activities for the year ended…arrow_forwardHarvest, Inc., a retail company, reported inventories of $1,020,240 at the beginning of the year, and $1,050,480 at the end of the year. The annual income statement reported cost of goods sold of $8,760,240. a. Compute the amount of inventory purchased during the year. $ a. Prepare journal entries to record (1) inventory purchases and (2) cost of goods sold. Assume all purchases were made on account. Ref. (1) (2) Account To record purchases. To record cost of goods sold. Debit Creditarrow_forward

- Chloe Company employs the perpetual inventory system. Cost of Goods Sold for the year before any adjustment is $275,450. The computer record shows the amount of ending inventory to be $55,382, while the physical count shows ending inventory to be $51,405. Record the adjustment into T accounts and then journalize the adjusting entry.arrow_forwardOn December 31, Pitts Manufacturing Company reports the following assets: what is the total amount of Pitts’ inventory at year-end?arrow_forwardBased on the following data for the current year, what is the inventory turnover (rounded to one decimal place)? Sales on account during year $575,056 Cost of goods sold during year 202,401 Accounts receivable, beginning of year 47,751 Accounts receivable, end of year 51,613 Inventory, beginning of year 31,348 Inventory, end of year 44,744 a.15.1 b.4.3 c.5.3 d.20.4arrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning