Videos

a.

To determine: The Expected Return and Standard Deviation for each Security.

Introduction: Expected Return is a process of estimating the

a.

Answer to Problem 35QP

The Expected Return is 12.50%, Variance is 0.002125 and Standard Deviation for Asset 1 is 4.61%. The Expected Return is 12.50%, Variance is 0.002125 and Standard Deviation for Asset 2 is 4.61%. The Expected Return is 12.50%, Variance is 0.002125 and Standard Deviation for Asset 3 is 4.61%.

Explanation of Solution

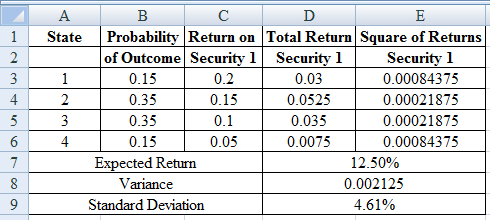

Determine the Expected Return, Variance and Standard Deviation for Asset 1

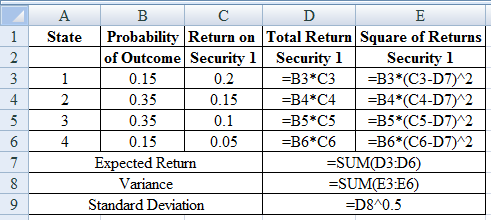

Using excel spreadsheet we calculate the expected return, variance and standard deviation as,

Excel Spreadsheet:

Excel Workings:

Therefore the Expected Return is 12.50%, Variance is 0.002125 and Standard Deviation for Asset 1 is 4.61%

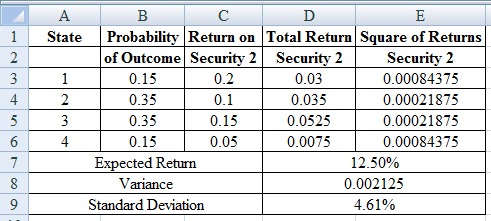

Determine the Expected Return, Variance and Standard Deviation for Asset 2

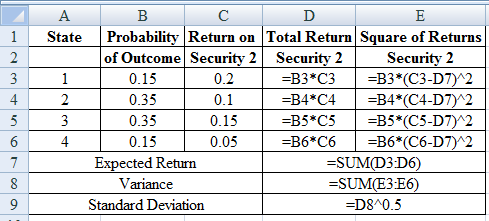

Using excel spreadsheet we calculate the expected return, variance and standard deviation as,

Excel Spreadsheet:

Excel Workings:

Therefore the Expected Return is 12.50%, Variance is 0.002125 and Standard Deviation for Asset 2 is 4.61%

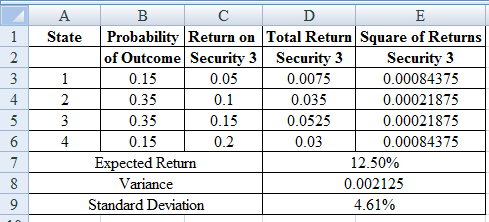

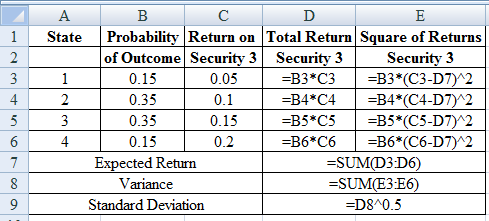

Determine the Expected Return, Variance and Standard Deviation for Asset 3

Using excel spreadsheet we calculate the expected return, variance and standard deviation as,

Excel Spreadsheet:

Excel Workings:

Therefore the Expected Return is 12.50%, Variance is 0.002125 and Standard Deviation for Asset 3 is 4.61%

b.

To determine: The Covariance and Correlation for each pair of security.

b.

Answer to Problem 35QP

Solution: The Covariance is 0.00125 and Correlation is 0.5882 for Security 1 and 2. The Covariance is -0.002125 and Correlation is -1 for Security 1 and 3. The Covariance is -0.00125 and Correlation is -0.5882 for Security 2 and 3.

Explanation of Solution

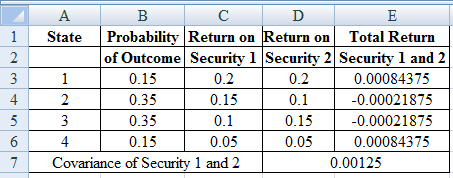

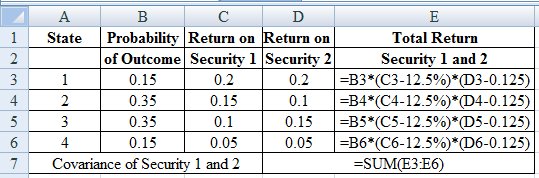

Determine the Covariance for Security 1 and 2

Using excel we find the covariance and correlation for security 1 and 2 as,

Excel Spreadsheet:

Excel Workings:

Therefore the Covariance for Security 1 and 2 is 0.00125

Determine the Correlation for Security 1 and 2

Therefore the Correlation for Security 1 and 2 is 0.5882

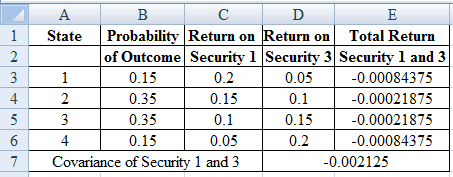

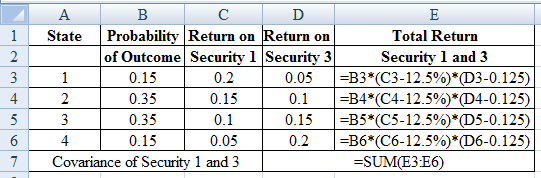

Determine the Covariance for Security 1 and 3

Using excel we find the covariance and correlation for security 1 and 3 as,

Excel Spreadsheet:

Excel Workings:

Therefore the Covariance for Security 1 and 3 is -0.00125

Determine the Correlation for Security 1 and 3

Therefore the Correlation for Security 1 and 3 is -1

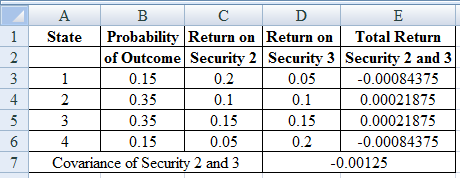

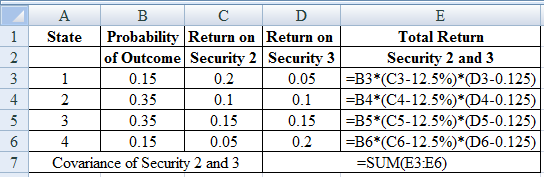

Determine the Covariance for Security 2 and 3

Using excel we find the covariance and correlation for security 2 and 3 as,

Excel Spreadsheet:

Excel Workings:

Therefore the Covariance for Security 2 and 3 is -0.00125

Determine the Correlation for Security 2 and 3

Therefore the Correlation for Security 2 and 3 is -0.5882.

c.

To determine: The Expected Return and Standard Deviation of Portfolio of Security 1 and Security 2.

c.

Answer to Problem 35QP

Solution: The Expected Return is 12.50% and Standard Deviation of Portfolio of Security 1 and Security 2 is 4.11%.

Explanation of Solution

Determine the Expected Return on Portfolio of Security 1 and 2

Therefore the Expected Return on Portfolio of Security 1 and 2 is 12.50%

Determine the Variance on Portfolio of Security 1 and 2

Therefore the Variance on Portfolio of Security 1 and 2 is 0.001687

Determine the Standard Deviation on Portfolio of Security 1 and 2

Therefore the Standard Deviation on Portfolio of Security 1 and 2 is 4.11%.

d.

To determine: The Expected Return and Standard Deviation of Portfolio of Security 1 and Security 3.

d.

Answer to Problem 35QP

The Expected Return is 12.50% and Standard Deviation of Portfolio of Security 1 and Security 3 is 0%.

Explanation of Solution

Determine the Expected Return on Portfolio of Security 1 and 3

Therefore the Expected Return on Portfolio of Security 1 and 3 is 12.50%

Determine the Variance on Portfolio of Security 1 and 3

Therefore the Variance on Portfolio of Security 1 and 3 is 0

Determine the Standard Deviation on Portfolio of Security 1 and 3

Therefore the Standard Deviation is 0%.

e.

To determine: The Expected Return and Standard Deviation of Portfolio of Security 2 and Security 3.

e.

Answer to Problem 35QP

The Expected Return is 12.50% and Standard Deviation of Portfolio of Security 2 and Security 3 is 2.09%.

Explanation of Solution

Determine the Expected Return on Portfolio of Security 2 and 3

Therefore the Expected Return on Portfolio of Security 2 and 3 is 12.50%

Determine the Variance on Portfolio of Security 2 and 3

Therefore the Variance on Portfolio of Security 2 and 3 is 0.000438

Determine the Standard Deviation on Portfolio of Security 2 and 3 is 0

Therefore the Standard Deviation is 2.09%.

f.

To determine: The Results of parts (a), (c), (d) and (e).

f.

Explanation of Solution

- The correlation between's the profits on two securities is below 1, there is an advantage to diversification.

- A portfolio that comprise of negatively correlated portfolios can accomplish higher risk diminishment than a positively correlated portfolio and the expected return of the stock being even.

- Applying appropriate weights on perfectly negatively correlated securities can lessen portfolio change to 0.

Want to see more full solutions like this?

Chapter 11 Solutions

EBK CORPORATE FINANCE

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education