Intermediate Accounting

9th Edition

ISBN: 9781259722660

Author: J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher: McGraw-Hill Education

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 12, Problem 12.18E

Equity investments; fair value through net income

• LO12-4

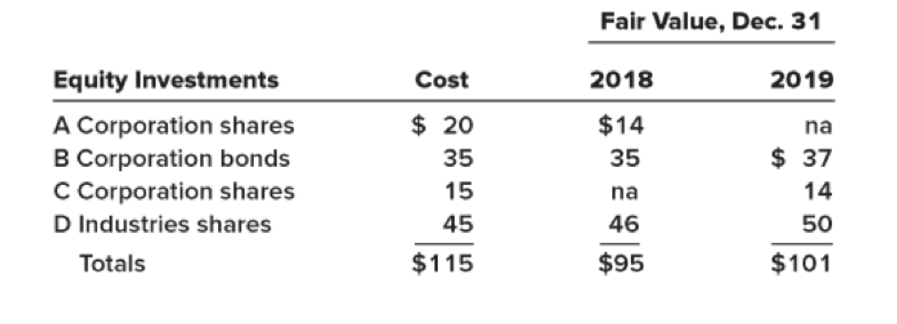

The investments of Harlon Enterprises included the following cost and fair value amounts ($ in millions):

Harlon accounts for its equity investment portfolio at fair value through net income. Harlon sold its holdings of A Corporation shares on June 1, 2019, for $15 million. On September 12, it purchased the C Corporation shares.

Required:

1. What is the effect of the sale of the A Corporation shares and the purchase of the C Corporation shares on Harlon’s 2019 pretax earnings?

2. At what amount should Harlon’s securities equity investment portfolio be reported in its 2019

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Problem 4. Mr. X is an investor in ABC Corporation. In 2020, he has 1,000 share holdings acquired at P120 per share classified as capital asset. Mr. X uses FIFO in costing his investment holdings.

b. How much is the nondeductible loss in May?

c. Supposing that all the remaining shares were liquidated in December 2021 at 130 per share, what would be the capital gain(loss) to be recognized.

nEED IN 10 MINUTES

9. On January 1, 20x1, an entity purchased marketable equity securities for P2,500,000. The entity paid commission and taxes of P190,000. The equity securities do not qualify as financial asset held for trading. The entity made irrevocable election to present unrealized gain and loss in other comprehensive income. The securities have a market value of P2,600,000, and P2,750,000 on December 31, 20x1 and December 31, 20x2.

On July 1, 2022, half of the securities are sold for P1,400,000. On July 1, 2022, the net increase/ decrease in retained earnings account is (sample answer: 10,500 increase or 10,500 decrease)

The investments of Harlon Enterprises included the following cost and fair value amounts ($ in millions):

Fair Value, Dec. 31

Equity Investments

Cost

2021

2022

A Corporation shares

$

50

$

29

N/A

B Corporation shares

65

65

$

67

C Corporation shares

30

N/A

29

D Industries shares

60

61

65

Totals

$

205

$

155

$

161

Harlon accounts for its equity investment portfolio at fair value through net income. Harlon sold its holdings of A Corporation shares on June 1, 2022, for $30 million. On September 12, it purchased the C Corporation shares. Required:1. What is the effect of the sale of the A Corporation shares and the purchase of the C Corporation shares on Harlon’s 2022 pretax earnings?2. At what amount should Harlon's securities equity investment portfolio be reported in its 2022 balance sheet? (For all requirements, enter your answers in millions, (i.e., 10,000,000 should be entered…

Chapter 12 Solutions

Intermediate Accounting

Ch. 12 - All investments in debt securities are classified...Ch. 12 - When market rates of interest rise after a...Ch. 12 - Does GAAP distinguish between fair values that are...Ch. 12 - When a debt investment is acquired to be held for...Ch. 12 - Prob. 12.5QCh. 12 - What is comprehensive income? Its composition...Ch. 12 - Why are holding gains and losses treated...Ch. 12 - Prob. 12.8QCh. 12 - Prob. 12.9QCh. 12 - Prob. 12.10Q

Ch. 12 - Under IFRS No. 9, which reporting categories are...Ch. 12 - Prob. 12.12QCh. 12 - Do U.S. GAAP and IFRS differ in the amount of...Ch. 12 - Under what circumstances is the equity method used...Ch. 12 - The equity method has been referred to as a...Ch. 12 - In the application of the equity method, how...Ch. 12 - Prob. 12.17QCh. 12 - Prob. 12.18QCh. 12 - Prob. 12.19QCh. 12 - How does IFRS differ from U.S. GAAP with respect...Ch. 12 - What is the effect of a company electing the fair...Ch. 12 - Define a financial instrument. Provide three...Ch. 12 - Some financial instruments are called derivatives....Ch. 12 - (Based on Appendix 12A) Northwest Carburetor...Ch. 12 - Prob. 12.25QCh. 12 - Prob. 12.26QCh. 12 - (Based on Appendix 12B) Reporting an investment at...Ch. 12 - Prob. 12.28QCh. 12 - Explain how the CECL model (introduced in ASU No....Ch. 12 - Prob. 12.30QCh. 12 - Prob. 12.1BECh. 12 - Prob. 12.2BECh. 12 - Trading securities LO12-3 For the Coca-Cola bonds...Ch. 12 - Available -for-sale securities LO12-4 SL...Ch. 12 - Available -for-sale securities LO12-4 For the...Ch. 12 - Prob. 12.6BECh. 12 - Prob. 12.7BECh. 12 - Prob. 12.8BECh. 12 - Prob. 12.9BECh. 12 - Prob. 12.10BECh. 12 - Equity investments and dividends LO12-5 Turner...Ch. 12 - Prob. 12.12BECh. 12 - Prob. 12.13BECh. 12 - Equity method investments LO12-6, LO12-9 Kim...Ch. 12 - Change in principle; change to the equity method ...Ch. 12 - Fair value option; equity method investments ...Ch. 12 - Prob. 12.17BECh. 12 - Impairments (AFS Credit Loss Model) (Appendix 12B)...Ch. 12 - Prob. 12.19BECh. 12 - Prob. 12.20BECh. 12 - Prob. 12.1ECh. 12 - Prob. 12.2ECh. 12 - Securities held-to-maturity LO12-1 FFT...Ch. 12 - Prob. 12.4ECh. 12 - Prob. 12.5ECh. 12 - Trading securities LO12-1 [This is a variation of...Ch. 12 - Various transactions relating to trading...Ch. 12 - Prob. 12.8ECh. 12 - Securities available-for-sale; adjusting entries ...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Classification of securities; adjusting entries ...Ch. 12 - Prob. 12.14ECh. 12 - Equity investments; fair value through net income ...Ch. 12 - Equity investments; fair value through net income ...Ch. 12 - Prob. 12.17ECh. 12 - Equity investments; fair value through net income ...Ch. 12 - Investment securities and equity method...Ch. 12 - Equity method; purchase; investee income;...Ch. 12 - Error corrections; equity method investment ...Ch. 12 - Prob. 12.22ECh. 12 - Prob. 12.23ECh. 12 - Prob. 12.24ECh. 12 - Prob. 12.25ECh. 12 - Prob. 12.26ECh. 12 - Prob. 12.27ECh. 12 - Prob. 12.28ECh. 12 - Prob. 12.29ECh. 12 - Prob. 12.30ECh. 12 - Prob. 12.31ECh. 12 - Prob. 12.32ECh. 12 - Accounting for impairments under IFRS (Appendix...Ch. 12 - Prob. 12.1PCh. 12 - Prob. 12.2PCh. 12 - Securities available-for-sale; bond investment;...Ch. 12 - Prob. 12.4PCh. 12 - Various transactions related to trading securities...Ch. 12 - Various transactions related to securities...Ch. 12 - Prob. 12.7PCh. 12 - Various transactions relating to trading...Ch. 12 - Securities held-to-maturity; securities available...Ch. 12 - Investment securities and equity method...Ch. 12 - Prob. 12.11PCh. 12 - Prob. 12.12PCh. 12 - Prob. 12.13PCh. 12 - Equity method LO12-6, LO12-7 On January 2, 2018,...Ch. 12 - Prob. 12.15PCh. 12 - Prob. 12.16PCh. 12 - Accounting for debt and equity investments ...Ch. 12 - Prob. 12.18PCh. 12 - Real World Case 121 Intels investments LO12-4 The...Ch. 12 - Prob. 12.2BYPCh. 12 - Prob. 12.4BYPCh. 12 - Prob. 12.6BYPCh. 12 - Real World Case 127 Comprehensive income Microsoft...Ch. 12 - Continuing Cases Target Case LO12-4, LO12-6...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Problem 4. Mr. X is an investor in ABC Corporation. In 2020, he has 1,000 share holdings acquired at P120 per share classified as capital asset. Mr. X uses FIFO in costing his investment holdings. Required: a.) What would be the net capital gain in March? b.) How much is the nondeductible loss in May? c.) Supposing that all the remaining shares were liquidated in December 2021 at 130 per share, what would be the capital gain(loss) to be recognized.arrow_forward1. How much is the realized gain or loss on the sale of Djursholm Corp. ordinary shares on April 1, 2022? 2. The 2,100 ordinary shares of Stockholm Corp. purchased on May 1, 2022, should be initially measured at how much? 3. Sweden’s December 31, 2022, statement of financial position should report financial assets at fair value through other comprehensive income at what amount?arrow_forward25 – 26:Judicious Company acquired an equity investment a number of years ago for P 3,000,000 and classified it as fair value through other comprehensive income. On December 31, 2020, the cumulative loss recognized in other comprehensive income was P 400,000 and the carrying amount of the investment was P 2,600,000. On December 31, 2021, the issuer of the equity instrument was in sever financial difficulty and the fair value of the equity investment had fallen to P 1,200,000. 25: What cumulative amount of unrealized loss should be reported as component of other comprehensive income in the statement of changes in equity for the year ended December 31, 2021? 26: prepare journal entry to recognize the decrease in value on December 31, 2021.arrow_forward

- Founded on January 1, 20X1, Gehl Company had the following passive investments in equity securities at the end of 20X1 and 20X2: Equity Security Cost 12/31/X2 Fair Value A $ 96,000 $ 94,000 B 184,000 162,000 C 126,000 136,000 Required: If the company recorded a $4,000 debit to its Fair value adjustment account as its 20X2 fair value adjustment, what must have been the unrealized gain or loss reported at the end of 20X1?arrow_forwardQuestion 10 On January 2, 2020, Tuao Company purchased 10% of Abulug Company’s outstanding ordinary shares for P20,000,000. Tuao is the largest single shareholder in Abulug and this gives Tuao the power to participate in the financial and operating policy decisions of the Abulug but is not control or joint control over those policies. Abulug reported profit of P10,000,000 and paid dividend of P4,000,000. What should be the balance in Tuao’s investment in Abulug Company at the end of 2020? Group of answer choices P20,600,000 P21,000,000 P20,000,000 P21,400,000arrow_forwardCase 2: the Investment Held for Trading Securities account in the book of Tatay (acquired in 2020) represents 30% ownership interest in Walanay, Inc. Walanay subsequently reacquires 50% of its outstanding shares from other investors. The previously held equity of Tatay have a fair value of three times its book value now. Tatay elected to measure NCI at ‘proportionate share’.With the stated facts, answer the following:1.How much is the Consideration Transferred?a. P 1,350,000.00b. P 1,900,000.00c. P 1,750,000.00d. P 1,800,000.002.How much is the Non-Controlling Interest in the acquiree?a. P 0.00b. P 150,000.00c. P 684,000.00d. P 1,200,000.003.How much is the Fair Value of the previously held equity interest in the acquiree?a. P 0.00b. P 540,000.00c. P 450,000.00d. P 500,000.00arrow_forward

- Question 7 During 2020, Crane Company purchased 91000 shares of Novak Corporation common stock for $1370000 as an equity investment. The fair value of these shares was $1299000 at December 31, 2020. Crane sold all of the Novak stock for $16 per share on December 3, 2021, incurring $67000 in brokerage commissions. Crane Company should report a realized gain on the sale of stock in 2021 of $86000. $19000. $157000. $90000.arrow_forward33. On December 31, 2018, Calm Company appropriately reported P80, 000 unrealized loss in OIC for equity securities measured irrevocably at FVOCI. Security Cost Fair value at 12/31/19 X 1, 250, 000 1, 600, 000 Y 1, 000, 000 950, 000 Z 1, 750, 000 1, 250, 000 What amount of unrealized loss is recognized in the 2019 statement of changes in equity? a.280,000 b.200,000 c.120,000 d.0arrow_forward29. the assets and liabilities of R were stated at their fair values when A acquired it's 80% interest and the fair value method was used to initially measure the NCI. A uses the cost method to account for its investment in R. Net income and dividends for 2021 for the affiliated companies were: A Corp. R Corp. Net Income P105,000 P31,500 Dividends paid 63,000 17,500 Dividends Payable, 1/1 20,000 9,250 Dividends Payable 12/31 31,500 8,750 Retained Earnings of A Corp. in the separate FS at the beginning of the year is P420,000. End of the year evaluation indicates P3,000 impairment in goodwill. The consolidated retained earnings at December 31, 2021 is:arrow_forward

- GL1501 - Based on Problem 15-4A LO P4 Twist Corp. had no short-term investments prior to year 2017. It had the following transactions involving short-term investments in available-for-sale securities during 2017. Apr. 16 Purchased 5,000 shares of Lafayette Co. stock at $26 per share. July 7 Purchased 3,500 shares of CVF Co. stock at $51 per share. 20 Purchased 1,600 shares of Green Co. stock at $18 per share. Aug. 15 Received an $1.20 per share cash dividend on the Lafayette Co. stock. 28 Sold 3,000 shares of Lafayette Co. stock at $29 per share. Oct. 1 Received a $3.30 per share cash dividend on the CVF Co. shares. Dec. 15 Received a $1.40 per share cash dividend on the remaining Lafayette Co. shares. 31 Received a $2.70 per share cash dividend on the CVF Co. shares.arrow_forward- What is the unrealized gain (loss) reported in profit or loss for the year 2021?A. P31,000B. (P31,000)C. P43,000D. (P43,000) - How much was the gain or loss on the sale of CD shares? A. P1,100 gain B. P2,000 gain C. P15,000 loss D. P15,900 lossarrow_forward12. The Polythene Pam Company purchases P2,000,000 of bonds. The asset has been designated as one at fair value through profit and loss. One year later, 10% of the bonds are sold for P400,000. Total cumulative gains previously recognized in Polythene Pam's financial statements in respect of the asset are P100,000. What is the amount of the gain on disposal to be recognized in profit or loss? Group of answer choices P90,000 P100,000 P190,000 P200,000arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Operating Loss Carryback and Carryforward; Author: SuperfastCPA;https://www.youtube.com/watch?v=XiYhgzSGDAk;License: Standard Youtube License