Videos

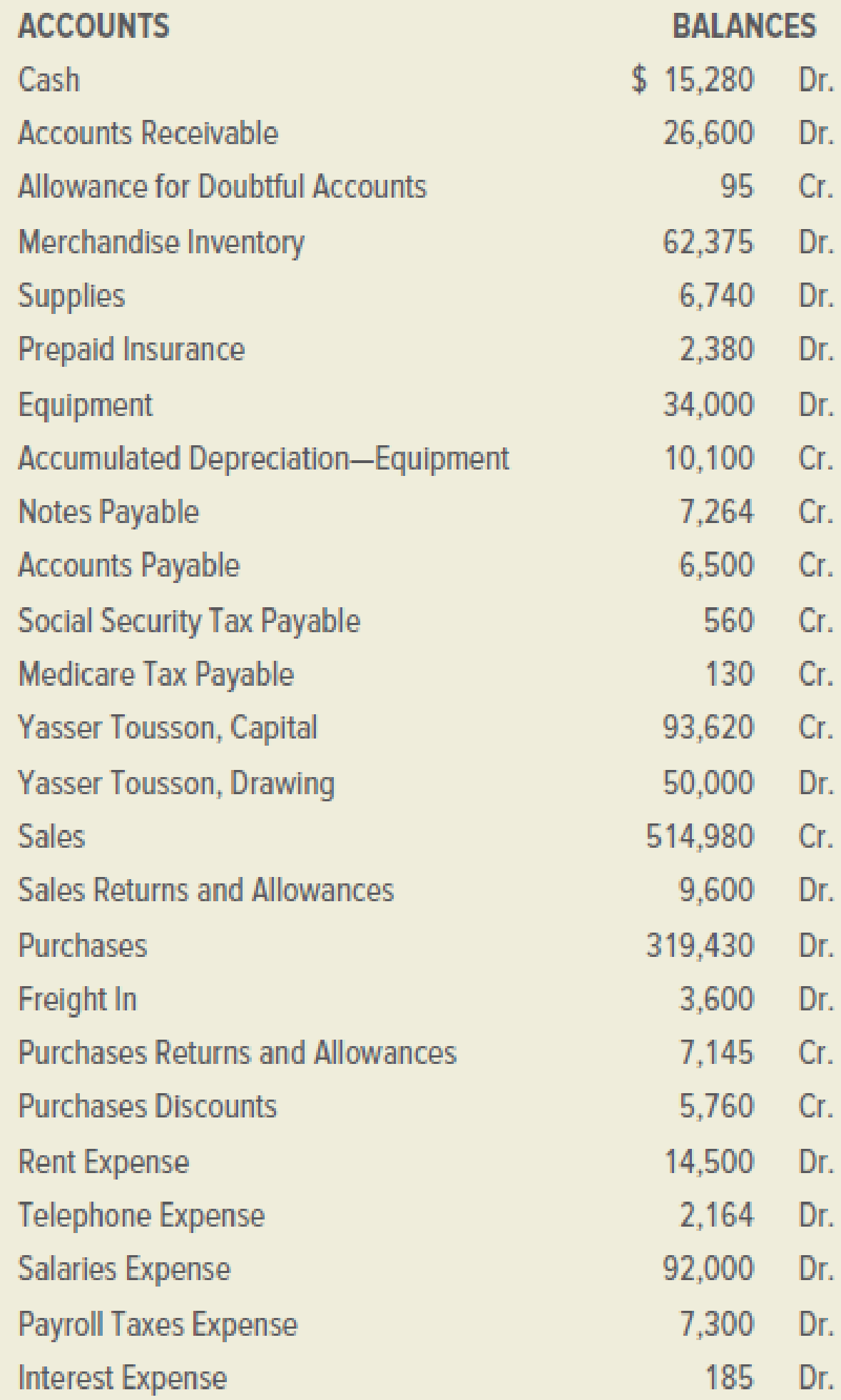

Programs Plus is a retail firm that sells computer programs for home and business use. On December 31, 2019, its general ledger contained the accounts and balances shown below:

The following accounts had zero balances:

The data needed for the adjustments on December 31 are as follows:

a.–b. Ending merchandise inventory, $67,850.

c. Uncollectible accounts, 0.5 percent of net credit sales of $245,000.

d. Supplies on hand December 31, $1,020.

e. Expired insurance, $1,190.

f.

g. Accrued interest expense on notes payable, $325.

h. Accrued salaries, $2,100.

i. Social Security Tax Payable (6.2 percent) and Medicare Tax Payable (1.45 percent) of accrued salaries.

INSTRUCTIONS

- 1. Prepare a worksheet for the year ended December 31, 2019.

- 2. Prepare a classified income statement. The firm does not divide its operating expenses into selling and administrative expenses.

- 3. Prepare a statement of owner’s equity. No additional investments were made during the period.

- 4. Prepare a classified

balance sheet . All notes payable are due within one year. - 5. Journalize the

adjusting entries . Use 25 as the first journal page number. - 6. Journalize the closing entries.

- 7. Journalize the reversing entries.

Analyze: By what percentage did the owner’s capital account change in the period from January 1, 2019, to December 31, 2019?

1.

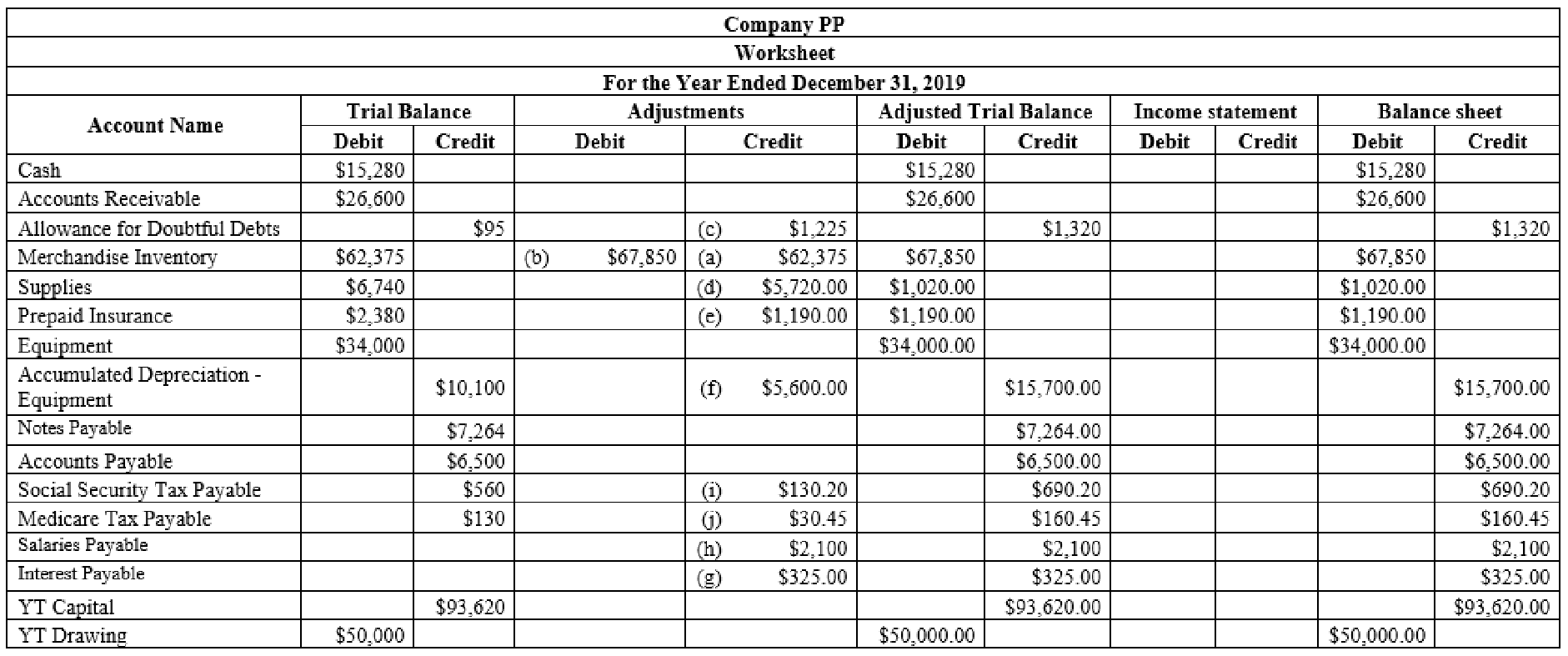

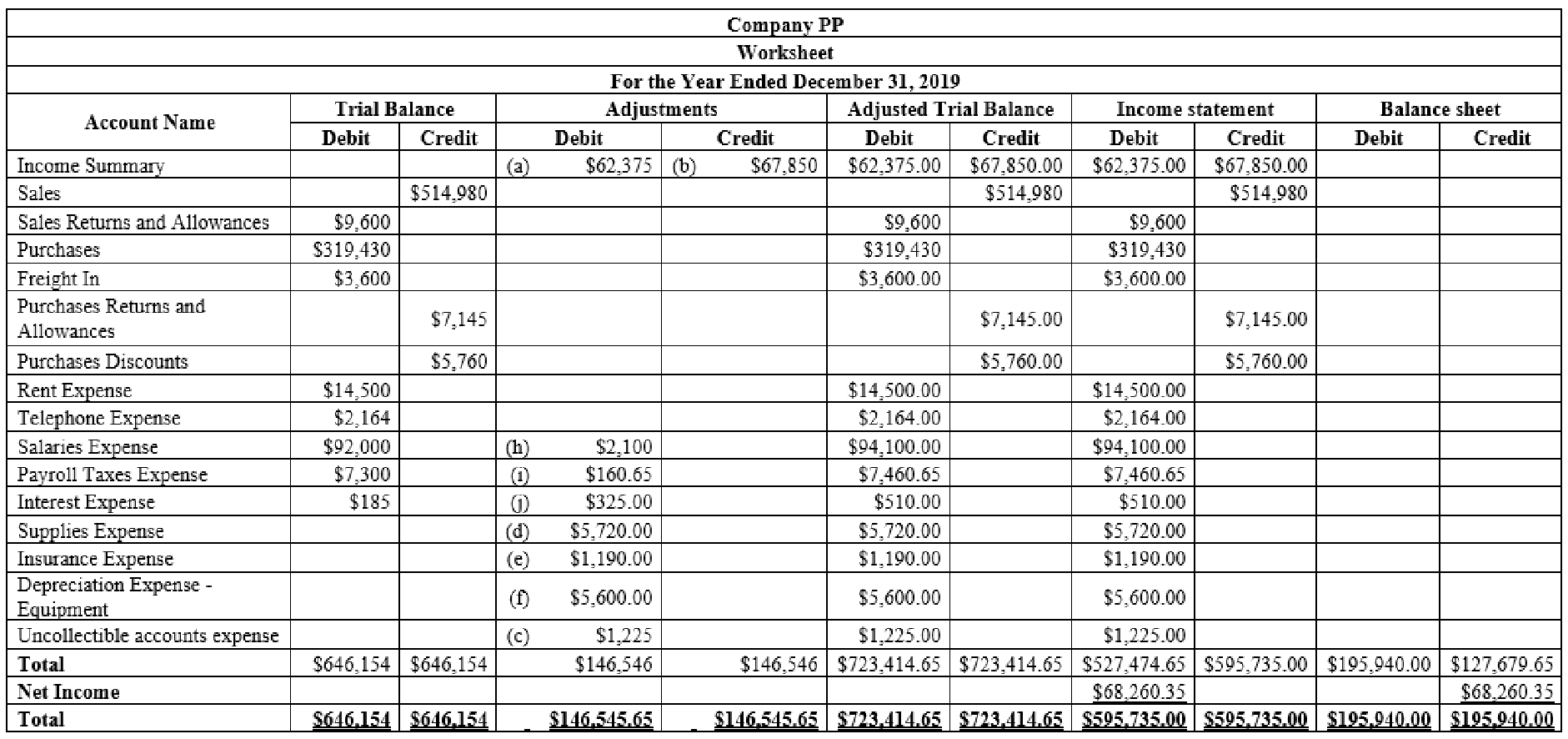

Prepare the worksheet and complete the sections of Trial balance, adjustments and compute the changes to the BW Capital that will be shown in the statement of owner's equity.

Explanation of Solution

Worksheet: A worksheet is the used in the preparation of the financial statement. It is a pre-defined form, having multiple columns, used in the adjustment process.

Prepare the worksheet for the year ended December 31, 2019.

Figure (1)

Figure (2)

2.

Show the Classified Income Statement.

Explanation of Solution

Classified Income statement: The classified income statement is a financial statement that shows the revenues, expenses with various classifications and sub-totals. The classified income statement is used for complex income statement as its more easily understandable.

Prepare the classified income statement:

| Company PP | ||||

| Income Statement | ||||

| Year Ended December 31, 2019 | ||||

| Particulars | Amount ($) | Amount ($) | Amount ($) | Amount ($) |

| Operating Revenue | ||||

| Sales | $514,980 | |||

| Less: Sales Returns and Allowances | $9,600 | |||

| Net Sales | $505,380 | |||

| Cost of Goods Sold | ||||

| Merchandise Inventory, January 1, 2019 | $62,375 | |||

| Purchases | $319,430 | |||

| Freight In | $3,600 | |||

| Delivered Cost of Purchases | $323,030 | |||

| Less: Sales Returns and Allowances | $7,145 | |||

| Purchases Discount | $5,760 | $12,905 | ||

| Net Delivered Cost of Purchases | $310,125 | |||

| Total Merchandise Available for sale | $372,500 | |||

| Less: Merchandise Inventory, closing | $67,850 | |||

| Cost of Goods Sold | $304,650 | |||

| Gross Profit on Sales | $200,730 | |||

| Operating Expenses | ||||

| Rent expense | $14,500 | |||

| Telephone Expense | $2,164 | |||

| Salaries Expense | $94,100 | |||

| Payroll Taxes Expense | $7,460.65 | |||

| Supplies Expense | $5,720 | |||

| Insurance Expense | $1,190 | |||

| Depreciation Expense - Equipment | $5,600 | |||

| Uncollectible Accounts Expense | $1,225 | |||

| Total Operating Expenses | $131,959.65 | |||

| Income from Operations | $68,770.35 | |||

| Other Expense | ||||

| Interest Expense | $510.00 | |||

| Net income for the year | $68,260.35 | |||

Table (1)

3.

Show the Statement of Owner's equity.

Explanation of Solution

Statement of owner's’ equity: This statement reports the beginning owner’s equity and all the changes which led to ending owner's’ equity.

Prepare the Statement of owner's’ equity:

| Company PP | ||

| Statement of Owner's Equity | ||

| Year Ended December 31, 2019 | ||

| Particulars | Amount ($) | Amount ($) |

| YT Capital, January 1, 2019 | $93,620 | |

| Net income for the year | $68,260.35 | |

| Deduct - Withdrawals | $50,000.00 | |

| Increase in Capital | $18,260.35 | |

| YT Capital, December 31, 2019 | $111,880.35 | |

Table (2)

4.

Show the Classified Balance Sheet and compute the percentage change in the owner’s capital in the accounting year 2019.

Explanation of Solution

Classified balance sheet: The main elements of balance sheet assets, liabilities, and stockholders’ equity are categorized or classified further into sections, and sub-sections in a classified balance sheet. Assets are further classified as current assets, long-term investments, property, plant, and equipment (PPE), and intangible assets. Liabilities are classified into two sections current and long-term. Stockholders’ equity comprises of common stock and retained earnings. Thus, the classified balance sheet includes all the elements under different sections.

Prepare the classified balance sheet:

| Company PP | |||

| Balance Sheet | |||

| December 31, 2019 | |||

| Particulars | Amount ($) | Amount ($) | Amount ($) |

| Assets | |||

| Current Assets | |||

| Cash | $15,280 | ||

| Accounts receivable | $26,600 | ||

| Less: Allowance for Doubtful Debts | $1,320 | $25,280 | |

| Merchandise Inventory | $67,850 | ||

| Prepaid expenses | |||

| Supplies | $1,020 | ||

| Prepaid insurance | $1,190 | $2,210 | |

| Total Current Assets | $110,620 | ||

| Plant and Equipment | |||

| Equipment | $34,000 | ||

| Less: Accumulated Depreciation | $15,700 | $18,300 | |

| Total Plant and Equipment | $18,300 | ||

| Total Assets | $128,920 | ||

| Liabilities and Owner's Equity | |||

| Current Liabilities | |||

| Notes Payable | $7,264 | ||

| Accounts payable | $6,500 | ||

| Interest Payable | $325 | ||

| Social Security Tax Payable | $690.20 | ||

| Medicare Tax Payable | $160.45 | ||

| Salaries Payable | $2,100 | ||

| Total Current Liabilities | $17,039.65 | ||

| Owner's Equity | |||

| YT Capital | $111,880.35 | ||

| Total Liabilities and Owner's Equity | $128,920 | ||

Table (3)

Compute the percentage increase in owner’s capital:

The percentage increase in the owner’s capital is 19.5%.

5.

Journalize the adjusting entries as on December 31, 2019.

Explanation of Solution

Adjusting entries: Adjusting entries are those entries which are recorded at the end of the year, to update the income statement accounts (revenue and expenses) and balance sheet accounts (assets, liabilities, and stockholders’ equity) to maintain the records according to accrual basis principle.

Pass the adjusting entry for the given transaction:

| General Journal | Page - 25 | |||

| Date | Description | Post Ref. | Debit | Credit |

| 2019 | ||||

| December 31 | Income Summary | $62,375 | ||

| Merchandise Inventory | $62,375 | |||

| (To record the beginning inventory) | ||||

| December 31 | Merchandise Inventory | $67,850 | ||

| Income Summary | $67,850 | |||

| (To record the closing inventory) | ||||

| December 31 | Uncollectible Accounts Expense | $1,225 | ||

| Allowance for Doubtful Accounts | $1,225 | |||

| (To record the estimated loss on the net credit sale) |

Table (4)

| General Journal | Page - 26 | |||

| Date | Description | Post Ref. | Debit | Credit |

| 2019 | ||||

| December 31 | Supplies Expense | $5,720 | ||

| Supplies | $5,720 | |||

| (To record the Supplies used) | ||||

| December 31 | Insurance expense | $1,190 | ||

| Prepaid Insurance | $1,190 | |||

| (To record the prepaid insurance) | ||||

| December 31 | Depreciation Expense - Equipment | $5,600 | ||

| Accumulated Depreciation - Equipment | $5,600 | |||

| (To record the depreciation on equipment) | ||||

| December 31 | Interest expense | $325 | ||

| Interest Payable | $325 | |||

| (To record the interest payable) | ||||

| December 31 | Salaries Expense | $2,100 | ||

| Salaries Payable | $2,100 | |||

| (To record the salaries payable) | ||||

| December 31 | Payroll Taxes Expense | $160.65 | ||

| Social Security Tax Payable | $130.20 | |||

| Medicare Tax Payable | $30.45 | |||

| (To record the taxes on accrued wages) |

Table (5)

6.

Journalize the closing entries as on December 31, 2019.

Explanation of Solution

Closing entries: The journal entries prepared to close the temporary accounts to Retained Earnings account are referred to as closing entries. The revenue, expense, and dividends accounts are referred to as temporary accounts because the information and figures in these accounts is held temporarily and consequently transferred to permanent account at the end of accounting year.

Pass the closing entries:

| General Journal | Page - 27 | |||

| Date | Description | Post Ref | Debit | Credit |

| 2019 | ||||

| December 31 | Sales | $514,980 | ||

| Purchases Returns and allowances | $7,145 | |||

| Purchases Discounts | $5,760 | |||

| Income Summary | $527,885 | |||

| (To record the closing entry for the income) | ||||

| December 31 | Income Summary | $465,099.65 | ||

| Sales Returns and Allowances | $9,600 | |||

| Purchases | $319,430 | |||

| Freight In | $3,600 | |||

| Rent Expense | $14,500 | |||

| Telephone Expense | $2,164 | |||

| Salaries Expense | $94,100.00 | |||

| Payroll Taxes Expense | $7,460.65 | |||

| Supplies Expense | $5,720 | |||

| Insurance expense | $1,190 | |||

| Depreciation Expense - Warehouse Equipment | $5,600 | |||

| Uncollectible Accounts Expense | $1,225 | |||

| Interest Expense | $510 | |||

| (To record the closing entry for the expenses) |

Table (6)

| General Journal | Page - 28 | |||

| Date | Description | Post Ref | Debit | Credit |

| 2019 | ||||

| December 31 | Income Summary | $68,260.35 | ||

| YT Capital | $68,260.35 | |||

| (To record the closing entry for the capital) | ||||

| December 31 | YT Capital | $50,000 | ||

| YT Drawings | $50,000 | |||

| (To record the closing entry for the capital) |

Table (7)

7.

Journalize the reversing entries as on January 1, 2020.

Explanation of Solution

Reversing entries: Reversing entries are those entries which are recorded at the beginning of the year, to reverse or set right the adjusting entries made in the end of the previous accounting year, in order to maintain the records according to accrual basis principle.

Pass the reversing entries:

| General Journal | Page - 29 | |||

| Date | Description | Post Ref | Debit | Credit |

| 2020 | ||||

| January 1 | Interest Payable | $325 | ||

| Interest Expense | $325 | |||

| (To record the reversing entry for interest payable) | ||||

| January 1 | Salaries Payable | $2,100 | ||

| Salaries Expense - Office | $2,100 | |||

| (To record the reversing entry for salaries payable) | ||||

| January 1 | Social Security Tax Payable | $130.20 | ||

| Medicare Tax Payable | $30.45 | |||

| Payroll Taxes Expense | $160.65 | |||

| (To record the reversing entry for payroll taxes payable) |

Table (8)

Want to see more full solutions like this?

Chapter 13 Solutions

COLLEGE ACCOUNTING ETEXT+CONNECT ACCESS

- Palisade Creek Co. is a merchandising business that uses the perpetual inventory system. The account balances for Palisade Creek Co. as of May 1, 2019 (unless otherwise indicated), are as follows: During May, the last month of the fiscal year, the following transactions were completed: Instructions 1. Enter the balances of each of the accounts in the appropriate balance column of a four-column account. Write Balance in the item section and place a check mark () in the Posting Reference column. Journalize the transactions for May, starting on Page 20 of the journal. 2. Post the journal to the general ledger, extending the month-end balances to the appropriate balance columns after all posting is completed. In this problem, you are not required to update or post to the accounts receivable and accounts payable subsidiary ledgers. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete (5) and (6). 5. (Optional) Enter the unadjusted trial balance on a 10-column end-of-period spreadsheet (work sheet), and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 22 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a statement of owners equity, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 23 of the journal. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. Insert the new balance in the owners capital account. 10. Prepare a post-closing trial balance.arrow_forwardSheridan Co. uses the gross method to record sales made on credit. On June 1, 2020, it made sales of $45,000 with terms 4/15, n/45. On June 12, 2020, Sheridan received full payment for the June 1 sale. Prepare the required journal entries for Sheridan Co. (If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.arrow_forwardOn March 2, Blossom Company sold $805,000 of merchandise on account to Ayayai Company, terms 2/10, n/30. The cost of the merchandise sold was $521,000. (List all debit entries before credit entries. Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts.) Account Titles and Explanation Debit Credit (To record credit sale) (To record cost of merchandise sold)arrow_forward

- Pina Company had the following adjusted account balances at year-end: Cost of Goods Sold $60,410, Inventory $15,010, Operating Expenses $29,380, Sales Revenue $126,580, Sales Discounts $1,340, and Sales Returns and Allowances $2,090.Prepare closing entries. (Credit account titles are automatically indented when amount is entered. Do not indent manually.) Account Titles and Explanation Debit Credit enter an account title to close accounts with credit balances enter a debit amount enter a credit amount enter an account title to close accounts with credit balances enter a debit amount enter a credit amount (To close accounts with credit balances) enter an account title to close accounts with debit balances enter a debit amount enter a credit amount enter an account title to close accounts with debit balances enter a debit amount enter a credit amount enter an account title to close accounts with debit balances enter a debit amount…arrow_forwardOn March 2, Sunland Company sold $995,000 of merchandise on account to Culver Company, terms 3/10, n/30. The cost of the merchandise sold was $583,000. (List all debit entries before credit entries. Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts.) Account Titles and Explanation (To record credit sale) (To record cost of merchandise sold) Debit Credit IMMarrow_forwardFlounder Company had the following adjusted account balances at year-end: Cost of Goods Sold $64,510, Inventory $14,660, Operating Expenses $29,240, Sales Revenue $126,730, Sales Discounts $1,140, and Sales Returns and Allowances $1,830.Prepare closing entries. (Credit account titles are automatically indented when amount is entered. Do not indent manually.) Account Titles and Explanation Debit Credit enter an account title to close accounts with credit balances enter a debit amount enter a credit amount enter an account title to close accounts with credit balances enter a debit amount enter a credit amount (To close accounts with credit balances) enter an account title to close accounts with debit balances enter a debit amount enter a credit amount enter an account title to close accounts with debit balances enter a debit amount enter a credit amount enter an account title to close accounts with debit balances enter a debit amount…arrow_forward

- On March 1, Pearl Industries sold merchandise on account to Amelia Company for $30,300, terms 2/10, net 45. On March 6, Amelia returns merchandise with a sales price of $1,200. On March 11, Pearl Industries receives payment from Amelia for the balance due. Prepare journal entries to record the March transactions on Pearl Industries's books. (You may ignore cost of goods sold entries and explanations.) (Credit account titles are automatically indented when amount is entered. Do not indent manually. Record journal entries in the order presented in the problem.) Date Account Titles and Explanation Debit Credit Mar. 11arrow_forwardOn December 31, Diane Photography Supplies estimated that $12,000 merchandise sold will be returned with a cost of $7,200. Journalize the adjusting entries needed to account for the estimated returns. (Assume the company uses a perpetual inventory system. Record debits first, then credits. Select the explanation on the last line of the journal entry table.) (1) Begin by preparing the entry for the estimated refunds. Do not prepare the entry to record the estimated return of merchandise with this entry. We will do that in the following step Date Accounts and Explanation Credit Dec. 31 (2) Prepare the entry for the estimated retum of merchandise Date Accounts and Explanation Dec 31 Debit Debit * Creditarrow_forwardRead through the information below for selected transactions during the month of December, 2021 and prepare the required jounal entry to record the transaction. Post each of the entries below to the general ledger T-accounts attached . Sold Merchandise for $5,000 to Lee Corp on account on December 9. Cost of the merchandise was $3,390 and the terms of the sale were 1/15, n/30.arrow_forward

- On March 2, Monty Corp. sold $932,000 of merchandise on account to Marigold Company, terms 4/10, n/30. The cost of the merchandise sold was $597,000. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts.) Account Titles and Explanation (To record credit sale) (To record cost of merchandise sold) Debit I Creditarrow_forwardOn 5 December 2020, Manal Trading company sold goods to a customer on account for 37800 OMR. Which of the following is the correct journal entry for the transaction? Select one: A. Date Accounts Debit (RO) Credit (RO) 05.12.2020 Receivable 37800 Sales (Revenue) 37800 B. Date Accounts Debit (RO) Credit (RO) 05.12.2020 Receivable 73800 Sales (Revenue) 73800 C. Date Accounts Debit (RO) Credit (RO) 05.12.2020 Sales (Revenue) 37800 Receivable 37800 D. Date Accounts Debit (RO) Credit (RO) 05.12.2020 Cash 37800 Sales (Revenue) 37800arrow_forwardOn March 2, Ivanhoe Company sold $890,000 of merchandise on account to Bridgeport Company, terms 2/10, n/30. The cost of the merchandise sold was $522,000. (List all debit entries before credit entries. Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Account Titles and Explanation (b) Inventory Accounts Payable Your Answer Correct Answer (Used) (c) Account Titles and Explanation Accounts Payable On March 6, Bridgeport Company returned $89,000 of the merchandise purchased on March 2. The cost of the returned merchandise was $54,800. (List all debit entries before credit entries. Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Inventory Debit count Titles and Explanation Debit 890,000 Debit Credit…arrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage