Concept explainers

Videos

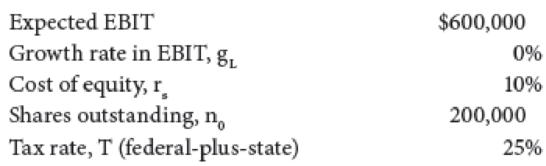

The Rivoli Company has no debt outstanding, and its financial position is given by the following data:

- a. What is Rivoli’s intrinsic value of operations (i.e., its unlevered value)? What is its intrinsic stock price? Its earnings per share?

- b. Rivoli is considering selling bonds and simultaneously repurchasing some of its stock. If it moves to a capital structure with 30% debt based on market values, its

cost of equity , rs, will increase to 12% to reflect the increased risk. Bonds can be sold at a cost, rd, of 7%. Based on the new capital structure, what is the new weighted average cost of capital? What is the levered value of the firm? What is the amount of debt? - c. Based on the new capital structure, what is the new stock price? What is the remaining number of shares? What is the new earnings per share?

a)

To determine: Company R’s intrinsic value of operations and intrinsic stock price and its earnings per share.

Explanation of Solution

Calculation of original value of operations:

Original free cash flow:

Hence, original cash flow is $450,000

Original cost of capital:

Hence, original cost of capital is 10%

Original value of operations:

Hence, original value of operations is $4,500,000

Calculation of intrinsic value of stock price:

Therefore, intrinsic stock price is $22.50

Calculation of original EPS:

Therefore, the original EPS is $2.25

b)

To determine: New WACC, levered value of the firm and the amount of debt.

Explanation of Solution

Calculation of WACC:

At 30% debt,

Hence, weighted average cost of capital of company R is 9.975%

Therefore, new beta is 11.0528%

Calculation of value of operations:

Leverage doesn’t change the cash flows, so the value of levered firm based on new WACC is as follows,

Hence, the value of operations is $4,511,278.195

Calculation of amount of debt:

Hence, the amount of debt is $1,353,383.459

c)

To determine: New stock price, remaining number of shares and new earnings per share based on new capital structure.

Explanation of Solution

Calculation of new stock price:

Therefore, the stock price after repurchase is equal to $22.5564

Calculation of total number of shares after repurchased:

Therefore, the number of remaining shares is 200,000-60,000 = 140,000

Calculation of earnings per share (EPS):

Therefore, the new earnings per share of company is $2.71

Want to see more full solutions like this?

Chapter 15 Solutions

Mindtap For Brigham/ehrhardt's Financial Management: Theory & Practice, 1 Term Printed Access Card (mindtap Course List)

- David Lyons, CEO of Lyons Solar Technologies, is concerned about his firms level of debt financing. The company uses short-term debt to finance its temporary working capital needs, but it does not use any permanent (long-term) debt. Other solar technology companies have debt, and Mr. Lyons wonders why they use debt and what its effects are on stock prices. To gain some insights into the matter, he poses the following questions to you, his recently hired assistant: d. Suppose that Firms U and L have the same input values as in Part c except for debt of 980,000. Also, both firms have total net operating capital of 2,000,000 and both firms are expected to grow at a constant rate of 7%. (Assume that the EBIT in part c is expected at t = 1.) Use the compressed adjusted present value (APV) model to estimate the value of U and L. Also estimate the levered cost of equity and the weighted average cost of capital.arrow_forwardDavid Lyons, CEO of Lyons Solar Technologies, is concerned about his firms level of debt financing. The company uses short-term debt to finance its temporary working capital needs, but it does not use any permanent (long-term) debt. Other solar technology companies have debt, and Mr. Lyons wonders why they use debt and what its effects are on stock prices. To gain some insights into the matter, he poses the following questions to you, his recently hired assistant: Now assume that Firms L and U are both subject to a 25% corporate tax rate. Using the data given in part b, repeat the analysis called for in parts b(1) and b(2) using assumptions from the MM model with taxes.arrow_forwardDavid Lyons, CEO of Lyons Solar Technologies, is concerned about his firm’s level of debt financing. The company uses short-term debt to finance its temporary working capital needs, but it does not use any permanent (long-term) debt. Other solar technology companies have debt, and Mr. Lyons wonders why they use debt and what its effects are on stock prices. To gain some insights into the matter, he poses the following questions to you, his recently hired assistant: Who were Modigliani and Miller (MM), and what assumptions are embedded in the MM and Miller models?arrow_forward

- Suppose IWT has decided to distribute $50 million, which it presently is holding in liquid short-term investments. IWT’s value of operations is estimated to be about $1,937.5 million; it has $387.5 million in debt and zero preferred stock. As mentioned previously, IWT has 100 million shares of stock outstanding. Assume that IWT has not yet made the distribution. What is IWT’s intrinsic value of equity? What is its intrinsic stock price per share? Now suppose that IWT has just made the $50 million distribution in the form of dividends. What is IWT’s intrinsic value of equity? What is its intrinsic stock price per share? Suppose instead that IWT has just made the $50 million distribution in the form of a stock repurchase. Now what is IWT’s intrinsic value of equity? How many shares did IWT repurchase? How many shares remained outstanding after the repurchase? What is its intrinsic stock price per share after the repurchase?arrow_forwardThe common stock and debt of XYZ Co. are valued $60 million and $40 million respectively. Currently cost of equity of the company is 18% and its cost of debt is 9%. If the company issues an additional $20 million of common stock and uses all of this cash to retire debt, what will be the new required rate of return on company’s equity? Assume change in leverage does not affect risk of debt and there are no taxes.arrow_forwardAppliances, Inc. has no debt outstanding, and its financial position is given by the following data: Assets (market value = book value) $5,000,000 EBIT $800,000 Cost of equity 12% Stock price $10 Shares outstanding 500,000 Tax rate 25% The firm is considering selling bonds and simultaneously repurchasing some of its stock. If it moves to a capital structure with 20% debt based on market values, its cost of equity will increase to 13% to reflect the increased risk. Bonds can be sold at a cost of 6%. Appliance, Inc. is a no-growth firm. Hence, all its earnings are paid out as dividends. Earnings are expected to be constant over time. As a creditor, you are concerned about the company’s ability to repay its debt and interest. What is the new times interest earned?arrow_forward

- Daichi Inc. is reassessing its debt position. Its current capital structure is composed of 80% debt and 20% common equity, its beta is 1.60, and its tax rate is 35%. However, the CFO believes the company has too much debt and is considering switching to a capital structure with 40% debt and 60% equity. The risk-free rate is 4.0 percent, with a 6.0 percent market risk premium. How much does a change in capital structure affect the firm's cost of equity?arrow_forwardLamont Corp. is debt-free and has a weighted average cost of capital of 12.7 percent. The current market value of the equity is $2.3 million and there are no taxes. According to M&M Proposition I, what will be the value of the company if it changes to a debt-equity ratio of .85?arrow_forwardDiol Athletics is trying to determine its optimal capital structure, which now consists of only debt and common equity. The firm does not currently use preferred stock in its capital structure, and it does not plan to do so in the future. To estimate how much its debt would cost at different debt levels, the company’s treasury staff has consulted with investment bankers and, on the basis of those discussions, has created the following table: Structure Market Debt-to-Value Ratio (Wd) Market Equity-to-Value Ratio (Ws) Bond Rating Pre-tax Cost of Debt (rd) A 0.0 1.0 AA 9.0% B 0.2 0.8 BBB 10.5% C 0.5 0.5 BB 11.6% D 0.6 0.4 C 12.7% E 0.75 0.25 D 14.0% Diol uses the CAPM to estimate its cost of common equity, rs. The company estimates that the risk-free rate is 7%; the market risk is 13%, and the company’s tax rate is 20%. Diol estimates that if it had no debt, its “unlevered” beta, bU, would be 1.3. What is the…arrow_forward

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning