Intermediate Accounting, 10 Ed

10th Edition

ISBN: 9781260310177

Author: Mark W. Nelson, Wayne B. Thomas J. David Spiceland

Publisher: McGraw-Hill Education

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 15, Problem 15.28E

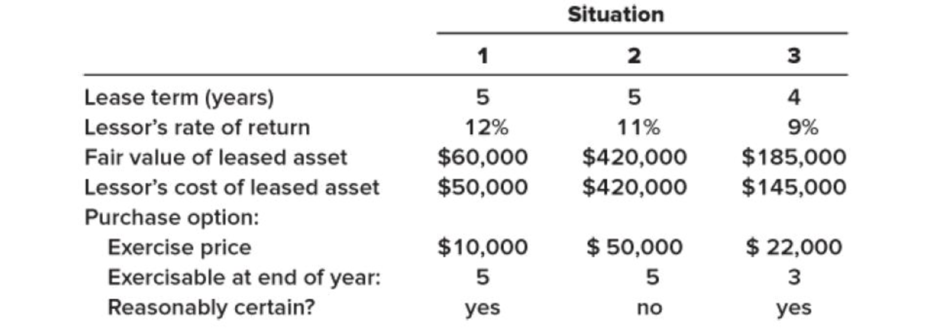

Calculation of annual lease payments; purchase option

• LO15–2, LO15–6

For each of the three independent situations below determine the amount of the annual lease payments. Each describes a finance lease in which annual lease payments are payable at the beginning of each year. Each lease agreement contains an option that permits the lessee to acquire the leased asset at an option price that is sufficiently lower than the expected fair value that the exercise of the option appears reasonably certain.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

WITH SOLUTION/COMPUTATION

53. Neal Corp. entered into a nine-year lease on a warehouse on December 31, 2019. Lease payments of P52,000, which includes payments for non-lease component of P2,000 (at stand-alone selling price), are due annually, beginning on December 31, 2019, and every December 31 thereafter. Neal does not know the interest rate implicit in the lease; Neal’s incremental borrowing rate is 9%. What amount should Neal report as lease liability at December 31, 2019?a. 280,000 b. 291,200 c. 450,000 d. 468,000

WITH SOLUTION/COMPUTATION.

51. On December 30, 2019, Haber Co. leased a new machine from Gregg Corp. The following data relate to the lease transaction at the inception of the lease:Lease term 10 yearsAnnual rental payable at end of each lease year P100,000Useful life of machine 12 yearsImplicit interest rate 10 %The lease has no renewal option, and the possession of the machine reverts to Gregg when the lease terminates. At the inception of the lease, Heber should record a lease liability of

a. 0 b. 615,000 c. 630,000 d. 676,000

EP#5

On January 1, 2021, Yancey, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Holt Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.(a) The agreement requires equal rental payments at the beginning each year.(b) The fair value of the building on January 1, 2021 is $6,000,000; however, the book value to Holt is $4,950,000.(c) The building has an estimated economic life of 10 years, with no residual value. Yancey depreciates similar buildings using the straight-line method.(d) At the termination of the lease, the title to the building will be transferred to the lessee.(e) Yancey’s incremental borrowing rate is 11% per year. Holt Warehouse Co. set the annual rental to insure a 10% rate of return. The implicit rate of the lessor is known by Yancey, Inc.(f) The yearly…

Chapter 15 Solutions

Intermediate Accounting, 10 Ed

Ch. 15 - Prob. 15.2QCh. 15 - Prob. 15.3QCh. 15 - Prob. 15.4QCh. 15 - A lessee should classify a lease transaction as a...Ch. 15 - Lukawitz Industries leased non-specialized...Ch. 15 - In accounting for a finance lease/sales-type...Ch. 15 - What is selling profit on a sales-type lease? How...Ch. 15 - At the beginning of an operating lease, the lessee...Ch. 15 - At the beginning of an operating lease, the lessor...Ch. 15 - In accounting for an operating lease, how are the...

Ch. 15 - Briefly describe the conceptual basis for asset...Ch. 15 - In a financing lease, front loading of lease...Ch. 15 - The discount rate influences virtually every...Ch. 15 - A lease that has a lease term (including any...Ch. 15 - A lease might specify that lease payments may be...Ch. 15 - What is a purchase option? How does it affect...Ch. 15 - A six-year lease can be renewed for two additional...Ch. 15 - Culinary Creations leased kitchen equipment under...Ch. 15 - What situations cause us to remeasure a lease...Ch. 15 - Prob. 15.21QCh. 15 - Compare the way a purchase option that is...Ch. 15 - What nonlease costs might be included as part of...Ch. 15 - The lessors initial direct costs often are...Ch. 15 - When are initial direct costs recognized in an...Ch. 15 - Prob. 15.26QCh. 15 - Prob. 15.27QCh. 15 - Prob. 15.28QCh. 15 - When a company sells an asset and simultaneously...Ch. 15 - Prob. 15.30QCh. 15 - Lease classification LO151 (Note: Brief Exercises...Ch. 15 - Lease classification LO151, LO152 Corinth Co....Ch. 15 - Lessee and lessor; calculate interest;...Ch. 15 - Finance lease; lessee; balance sheet effects ...Ch. 15 - Finance lease; lessee; income statement effects ...Ch. 15 - Sales-type lease; lessor; income statement effects...Ch. 15 - Prob. 15.7BECh. 15 - Operating lease LO154 (Note: Brief Exercises 8...Ch. 15 - Operating lease LO154 At the beginning of its...Ch. 15 - Short-term lease LO155 King Cones leased ice...Ch. 15 - Uncertain lease term LO156 Java Hut leased a...Ch. 15 - Uncertain lease payments LO156 On January 1,...Ch. 15 - Purchase option; lessor; sales-type lease LO152,...Ch. 15 - Residual value; sales-type lease LO152, LO153,...Ch. 15 - Guarantee d residual value LO156 On January 1,...Ch. 15 - Lessors initial direct costs; sales-type lease ...Ch. 15 - Lease classification LO151 Each of the four...Ch. 15 - Prob. 15.9ECh. 15 - Lessor calculation of annual lease payments;...Ch. 15 - Sales-type lease; lessor; income statement effects...Ch. 15 - Calculation of annual lease payments; residual...Ch. 15 - Lease concepts; finance/sales-type leases;...Ch. 15 - Calculation of annual lease payments; purchase...Ch. 15 - Prob. 15.37ECh. 15 - Prob. 15.38ECh. 15 - Prob. 15.39ECh. 15 - Lessors initial direct costs; operating and...Ch. 15 - Research Case 151 FASB codification; locate and...Ch. 15 - Ethics Case 153 Leasehold improvements LO153...Ch. 15 - Communication Case 155 Wheres the gain? Appendix...Ch. 15 - Prob. 15.6DMPCh. 15 - Prob. 1CCTCCh. 15 - Prob. 2CCTC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- WITH SOLUTION/COMPUTATION 57. On January 1, 2019, Blaugh Co. signed a long-term lease for an office building, the trems of the lease required Blaugh to pay P10,000 Annually, beginning December 30, 2019, and continuing each year for 30 years. On January 1, 2019, the present value of the lease payments is P112,500 at the 8% interest rate implicit in the lease. In Blaugh’s December 31, 2019, balance sheet, the lease liability should be 102,500 111,500 112,500 290,000arrow_forwardWITH SOLUTION/COMPUTATION 55. On January 1, 2019, Babson, Inc., leased two automobiles for executive use. The lease requires Babson to make five annual payments of P13,000 beginning January 1, 2019. At the end of the lease term, Babson guarantees the residual value of the automobiles will total P10,000. The interest rate implicit in the lease is 9%. Babson’s recorded lease liability on initial recognition isa. 48, 620 b. 44,070 ` c. 35,620 d. 31,070arrow_forwardMN.17. On 1 July 2020 Jane Ltd (lessor) leased equipment to Austin Ltd (Lessee). The equipment had a fair value of $369,824. This was also the present value of the lease payments .The lease agreement contained the following details: Lease term 5 years Economic life 6 years Annual rental payment in arrears commencing 30June 2021 $90,000 Residual Value at end of lease term $80,000 Residual Value guaranteed by lessee 80,ooo Interest rate implicit in lease 12% Lease is cancellable with permission of lessor, Jane Ltd .Lease is classified as a finance Lease by the Lessor . Required: (a)Prepare the Lease payment schedule for Austin Ltd, Lessee, for the first two years, for the year ended 30 June 2021 and for the year ended 30 June 2022.arrow_forward

- PROBLEM 10: LEASE MODIFICATION WITH EXTENSION of lease term Laze Company entered into a lease agreement for a stall space for its products on January 1, 2020. Some of the agreement in the lease contract are as follows: Annual rental payable at end of each year starting December 31, 2020 P350,000 Lease term 6 years Implicit interest rate in the lease 10% Laze Company proposed an amendment on the original lease contract on January 1, 2023, and was approved by the lessor. The amendment is to extend the lease term for another 2 years with the following additional features: Annual rental payable at end of each year starting December 31, 2023 P350,000 Implicit interest rate in the lease 11% REQUIRED:: Prepare table of amortization and journal entries for the entire lease term.arrow_forward16... Partially correct answer icon Your answer is partially correct. Grouper Corporation leases equipment from Falls Company on January 1, 2020. The lease agreement does not transfer ownership, contain a bargain purchase option, and is not a specialized asset. It covers 3 years of the equipment’s 8-year useful life, and the present value of the lease payments is less than 90% of the fair value of the asset leased.Prepare Grouper’s journal entries on January 1, 2020, and December 31, 2020. Assume the annual lease payment is $30,000 at the beginning of each year, and Grouper’s incremental borrowing rate is 8%, which is the same as the lessor’s implicit rate. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. For calculation purposes, use 5 decimal places as displayed in the factor table provided and round final answers to 0 decimal places, e.g. 5,265. Record journal entries in the order presented in the problem.)Click here to…arrow_forwardExercise 15-33 (Algo) Nonlease payments; lessor and lessee [LO15-2, 15-7] On January 1, 2024, NRC Credit Corporation leased equipment to Brand Services under a finance/sales-type lease designed to earn NRC a 11% rate of return for providing long-term financing. The lease agreement specified the following: Ten annual payments of $61,000 beginning January 1, 2024, the beginning of the lease and each December 31 thereafter through 2032. The estimated useful life of the leased equipment is 10 years with no residual value. Its cost to NRC was $346,464. The lease qualifies as a finance lease/sales-type lease. A 10-year service agreement with Quality Maintenance Company was negotiated to provide maintenance of the equipment as required. Payments of $8,000 per year are specified, beginning January 1, 2024. NRC was to pay this cost as incurred, but lease payments reflect this expenditure. A partial amortization schedule, appropriate for both the lessee and lessor, follows: Note: Use…arrow_forward

- P17–4 LEASE VERSUS PURCHASE JLB Corporation is attempting to determine whether to lease or purchase research equipment. The firm is in the 21% tax bracket, and its after-tax cost of debt is currently 8%. The terms of the lease and of the purchase are as follows: LEASE Annual end-of-year lease payments of $25,200 are required over the three-year life of the lease. All maintenance costs will be paid by the lessor; insurance and other costs will be borne by the lessee. The lessee will exercise its option to purchase the asset for $5,000 at termination of the lease. PURCHASE The equipment costs $60,000 and can be financed with a 14% loan requiring annual end-of-year payments of $25,844 for three years. JLB will depreciate the equipment under MACRS using a three-year recovery period. (See Table 4.2 for the applicable depreciation percentages.) JLB will pay $1,800 per year for a service contract that covers all maintenance costs; insurance and other costs will be borne by the JLB, who plans…arrow_forwardCH 21 POST-CLASS - SU21 Question 1 Ivanhoe Corporation enters into a 5-year lease of equipment on December 31, 2019, which requires 5 annual payments of $37,800 each, beginning December 31, 2019. In addition, Ivanhoe guarantees the lessor a residual value of $20,500 at the end of the lease. However, Ivanhoe believes it is probable that the expected residual value at the end of the lease term will be $10,250. The equipment has a useful life of 5 years.Prepare Ivanhoes' December 31, 2019, journal entries assuming the implicit rate of the lease is 10% and this is known to Ivanhoe. (Credit account titles are automatically indented when amount is entered. Do not indent manually. For calculation purposes, use 5 decimal places as displayed in the factor table provided and round final answers to 0 decimal places e.g. 5,275.)Click here to view factor tables. Date Account Titles and Explanation Debit Credit December 31, 2019 (To…arrow_forwardt34 Initial direct costs incurred by the lessor in an operating lease should beA. expensed in the year of incurrence by including them in the cost of goods sold or by treating them as a sellingexpense.B. deferred and recognized as reduction in the interest rate implicit in the lease.C. capitalized as part of asset cost and depreciated over the lease term.D. deferred and carried on the statement of financial position until the end of the lease term.arrow_forward

- 18. Which of the following lease conditions would result in a finance lease to the lessee? a.The fair market value of the property at the inception of the lease is $18,000; the present value of the minimum lease payments is $16,000. b.The lease term is 70% of the property's economic life. c.The lessee will return the property to the lessor at the end of the lease term. d.The lessee can purchase the property for $1 at the end of the lease term.arrow_forward23. One of the four general criteria for a capital lease is that the present value at the beginning of the lease term of the minimum lease payments equals or exceeds a. the property's fair market value. b. 90 percent of the property's fair market value. c. 75 percent of the property's fair market value. d. 50 percent of the property's fair market value.arrow_forwardWITH SOLUTION/COMPUTATION 52. On January 2, 2019, Ashe Company entered into a ten-year non-cancellable lease requiring year-end payments of P100,000. Ashe’s incremental borrowing rate is 12% while the lessor’s implicit interest rate, known to Ashe, is 10%. Ownership of the property remains with the lessor at expiration of the lease. There is no bargain purchase option. The leased property has an estimated economic life of 12 years. What amount should Ashe capitalize for this leased property on January 2, 2019? a. 1,000,000 b. 614,500 c. 565,000 d. 0arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education

Accounting for Finance and Operating Leases | U.S. GAAP CPA Exams; Author: Maxwell CPA Review;https://www.youtube.com/watch?v=iMSaxzIqH9s;License: Standard Youtube License