INTERMEDIATE ACCOUNTING (ACCT 3200A)

10th Edition

ISBN: 9781307660630

Author: SPICELAND

Publisher: MCG CUSTOM

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 15, Problem 15.28E

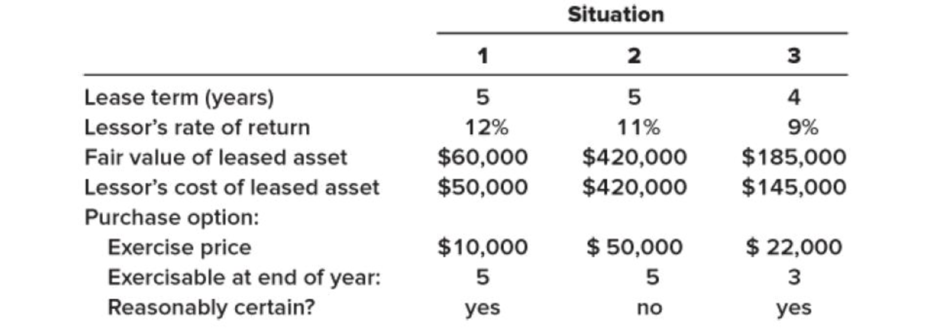

Calculation of annual lease payments; purchase option

• LO15–2, LO15–6

For each of the three independent situations below determine the amount of the annual lease payments. Each describes a finance lease in which annual lease payments are payable at the beginning of each year. Each lease agreement contains an option that permits the lessee to acquire the leased asset at an option price that is sufficiently lower than the expected fair value that the exercise of the option appears reasonably certain.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Part 1: New Lease Accounting – IFRS 16 Leases Effect Analysis.

What are the top three industries most affected by IFRS 16 as measured by the present value of future payments for off-balance-sheet leases to total assets? Which leased assets propel them to the top three? Also, discuss the extent that smaller firms would be affected by IFRS 16.

Which payments are to be included in the measurement of lease assets and lease liabilities? Also, discuss the pros and cons of excluding the following payments from the measurement.

Variable lease payments linked to future use or sales

Optional payments relating to lease-extension option when a lessee is not reasonably certain to exercise the option.

Discuss the effects of the new accounting on the following items and ratios of lessees. Provide reason(s) behind all effects.

EBITDA, operating profit, and profit before tax

Operating cash flow, financing cash flow, and total cash flow

Debt to equity, current ratio, and return on total assets

Question 5

The following facts pertain to a noncancelable lease agreement

between Mooney Leasing Company and Rode Company, a lessee.

Inception date: May 1, 2025

Annual lease payment due at the beginning of each year, beginning with May 1,

2025: $30,000

Bargain-purchase option price at end of lease term = $10,000

Lessor's implicit rate = 7%

The lease term ends in FIVE years on April 30, 2030.

What is the present value of the asset being leased?

Recommendation: draw a timeline of the cash flows from the lessee to the lessor.

Your Answer:

Answer

E 15-9 Lessor calculation of annual lease payments; lessee calculation of asset and liability LO15-2

Each of the three independent situations below describes a finance lease in which annual lease payments are payable at the beginning of

each year. The lessee is aware of the lessor's implicit rate of return.

Lease term (years)

Lessor's rate of return (known by lessee)

Lessee's incremental borrowing rate

Fair value of lease asset

1

10

11%

12%

$600,000

Required:

For each situation, determine:

a. The amount of the annual lease payments as calculated by the lessor.

b. The amount the lessee would record as a right-of-use asset and a lease liability.

Situation

2

20

9%

10%

$980,000

3

4

12%

10%

$185,000

Chapter 15 Solutions

INTERMEDIATE ACCOUNTING (ACCT 3200A)

Ch. 15 - Prob. 15.2QCh. 15 - Prob. 15.3QCh. 15 - Prob. 15.4QCh. 15 - A lessee should classify a lease transaction as a...Ch. 15 - Lukawitz Industries leased non-specialized...Ch. 15 - In accounting for a finance lease/sales-type...Ch. 15 - What is selling profit on a sales-type lease? How...Ch. 15 - At the beginning of an operating lease, the lessee...Ch. 15 - At the beginning of an operating lease, the lessor...Ch. 15 - In accounting for an operating lease, how are the...

Ch. 15 - Briefly describe the conceptual basis for asset...Ch. 15 - In a financing lease, front loading of lease...Ch. 15 - The discount rate influences virtually every...Ch. 15 - A lease that has a lease term (including any...Ch. 15 - A lease might specify that lease payments may be...Ch. 15 - What is a purchase option? How does it affect...Ch. 15 - A six-year lease can be renewed for two additional...Ch. 15 - Culinary Creations leased kitchen equipment under...Ch. 15 - What situations cause us to remeasure a lease...Ch. 15 - Prob. 15.21QCh. 15 - Compare the way a purchase option that is...Ch. 15 - What nonlease costs might be included as part of...Ch. 15 - The lessors initial direct costs often are...Ch. 15 - When are initial direct costs recognized in an...Ch. 15 - Prob. 15.26QCh. 15 - Prob. 15.27QCh. 15 - Prob. 15.28QCh. 15 - When a company sells an asset and simultaneously...Ch. 15 - Prob. 15.30QCh. 15 - Lease classification LO151 (Note: Brief Exercises...Ch. 15 - Lease classification LO151, LO152 Corinth Co....Ch. 15 - Lessee and lessor; calculate interest;...Ch. 15 - Finance lease; lessee; balance sheet effects ...Ch. 15 - Finance lease; lessee; income statement effects ...Ch. 15 - Sales-type lease; lessor; income statement effects...Ch. 15 - Prob. 15.7BECh. 15 - Operating lease LO154 (Note: Brief Exercises 8...Ch. 15 - Operating lease LO154 At the beginning of its...Ch. 15 - Short-term lease LO155 King Cones leased ice...Ch. 15 - Uncertain lease term LO156 Java Hut leased a...Ch. 15 - Uncertain lease payments LO156 On January 1,...Ch. 15 - Purchase option; lessor; sales-type lease LO152,...Ch. 15 - Residual value; sales-type lease LO152, LO153,...Ch. 15 - Guarantee d residual value LO156 On January 1,...Ch. 15 - Lessors initial direct costs; sales-type lease ...Ch. 15 - Lease classification LO151 Each of the four...Ch. 15 - Prob. 15.9ECh. 15 - Lessor calculation of annual lease payments;...Ch. 15 - Sales-type lease; lessor; income statement effects...Ch. 15 - Calculation of annual lease payments; residual...Ch. 15 - Lease concepts; finance/sales-type leases;...Ch. 15 - Calculation of annual lease payments; purchase...Ch. 15 - Prob. 15.37ECh. 15 - Prob. 15.38ECh. 15 - Prob. 15.39ECh. 15 - Lessors initial direct costs; operating and...Ch. 15 - Research Case 151 FASB codification; locate and...Ch. 15 - Ethics Case 153 Leasehold improvements LO153...Ch. 15 - Communication Case 155 Wheres the gain? Appendix...Ch. 15 - Prob. 15.6DMPCh. 15 - Prob. 1CCTCCh. 15 - Prob. 2CCTC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- For each of the three independent situations below determine the amount of the annual lease payments. Each describes a finance lease in which annual lease payments are payable at the beginning of each year. Each lease agreement contains an option that permits the lessee to acquire the leased asset at an option price that is sufficiently lower than the expected fair value that the exercise of the option appears reasonably certain. (EV of $1. PV of $1. EVA of $1, PVA of $1. EVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Situation Lease term (years) Lessor's rate of return Fair value of leased asset 6. 6 10% $ 193, 000 $ 153,000 12% 8% $ 76,000 $ 428,000 $ 58,000 $ 428,000 Lessor's cost of leased asset Purchase option: Exercise price Exercisable at end of year: $ 18,000 $ 58,000 $ 30,000 6. 6 4 Reasonably certain? yes no yes Determine the annual lease payments for each situation: (Round your intermediate and final answers to the nearest whole dollar…arrow_forwardA lessee has developed the following information regarding a lease contract, with payments due at the beginning of the period. Use this information to determine the amount at which the lease obligation will initially be recorded. Description Amount Present value Present value of total of annuity due amount Annual lease $4,500 S16.528 S14,258 payment Discount rate 6% Number of periods 4 Purchase option $300 S238 Group of answer choices: 18,000 14,495 16,528 14,258 18,300 16,766arrow_forwardExercise 15-1 (Static) Lease classification [LO15-1] Lease term (years) Asset's useful life (years) Asset's fair value Purchase option that is reasonably certain to be exercised? Annual lease payments. Lessor's implicit rate (known by lessee) Lessee's incremental borrowing rate Situation 1. 2 3 4 $44,000 Mo Beginning of year 5% 5x Lease Classification 4 Situation $45,000 Yes End of year 60% 5% 3 4 6 $41,000 Required: Each of the four independent situations above describes a lease requiring annual lease payments of $10,000 For each situation, determine the appropriate lease classification by the lessee. Note: Use tables, Excel, or a financial calculator. (EV of $1. PV of $1. EVA of $1. PVA of $1. EVAD of $1 and PVAD of $1) No Beginning of year 5% 5% $38,000 No End of year 6%arrow_forward

- Part 1: New Lease Accounting –IFRS 16 Leases Effect Analysis. Identify differences between IFRS 16 and U.S. GAAP new lease accounting (ASC Topic 842). Based on these differences, discuss which one (IFRS or U.S. GAAP) you favor and why? Discuss three main features of the two transition methods for lessees under ASC 842 and IFRS 16. Which transition method would investors likely prefer? Why? Which transition method may be preferred by companies? Why?arrow_forward3 By the lessee, a lessee-guaranteed residual value at the beginning of a finance lease should be: Multiple Choice O O O Excluded from lease payments. Included as part of lease payments at future value. Included as part of lease payments at present value. Jhy Included as part of lease payments only to the extent that guaranteed residual value is avnarted to avrear estimated residual valuearrow_forwardLease 1 does not contain a bargain purchase option, but the lease term is equal to 90 percent of the estimated economic life of the leased property. Lease 2 does not transfer ownership of the property to the lessee by the end of the lease term, but the lease term is equal to 75 percent of the estimated economic life of the leased property. How should the lessee classify these leases? Lease 1 1. Operating lease 2. Operating lease 3. Finance lease 4. Finance lease 03 02 01 04 Lease 2 Finance lease Operating lease Finance lease Operating leasearrow_forward

- 31 The interest rate implicit in the lease is the discount rate that causes the aggregate of the present value of the minimum lease payments and the unguaranteed residual value to be equal to theA. fair value of the leased asset.B. fair value of the leased asset and initial direct costs of the lessor.C. fair value of the leased asset and initial direct costs of the lessee.D. gross investment in the lease.arrow_forwardquestion 1: There are nine itsms list under "quantitive disclosure" for the lease. Why aren't short-term lease cost and variable lease cost shown? question 2 : What is the amount cintractual obligations and options that the lessee is reasonably certain to excercise for Operating lease? financing lease?arrow_forwardKnowleage Check UT f the option is reasonably certain to be exercised, how does the inclusion of a provision that gives the lessee the option to purchase the lease asset during the ease term at a specified exercise price impact that accounting for that lease? Note: Select all that apply. Check All That Apply The lessor must classify the lease as a sales-type lease. The lessee has the option of classifying the lease as an operating lease. The lease term is assumed to end on the date that the option is expected to be exercised. In the present value calculations, the lessor adds the present value of the exercise price to the present value of the periodic lease payments to determine the amount recorded as the lease receivable.arrow_forward

- PROBLEM NO. 3 Assume that DBP Leasing Corp. and Minasugbo Inc. sign a lease contract effective on January 1, 2019 where DBP Leasing leases to Minasugbo a bulldozer. The terms and provisions of the lease contract and other pertinent date are as follows: • The term of the lease is five years. The lease agreement is non-cancelable, requiring equal rental payments of P20,711.11 at the beginning of each year (annuity-due basis). The bulldozer has a fair value at the commencement of the lease of P100,000, an estimated economic life of five years, and a guaranteed residual value of P5,000. (Minasugbo expects that it is probable that the expected value of the residual value at the end of the lease will be greater than the guaranteed amount of P5,000.) The lease contains no renewal options. The bulldozer reverts to DBP Leasing at the termination of the lease. Minasugbo's incremental borrowing rate is 5 percent per year. • Minasugbo depreciates its equipment on a straight-line basis. DBP Leasing…arrow_forwardExercise 15-9 (Algo) Lessor calculation of annual lease payments; lessee calculation of asset and liability [LO15-2] Each of the three independent situations below describes a finance lease in which annual lease payments are payable at the beginning of each year. The lessee is aware of the lessor's implicit rate of return. Note: Use tables, Excel, or a financial calculator. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) Situation 1 2 3 Lease term (years) 11 21 4 Lessor's rate of return (known by lessee) 10% 8% 11% Lessee's incremental borrowing rate 11% 9% 10% Fair value of lease asset $800,000 $1,180,000 $385,000 Required: a. & b. Determine the amount of the annual lease payments as calculated by the lessor and the amount the lessee would record as a right-of-use asset and a lease liability, for each of the above situations. Note: Round your answers to the nearest whole dollar.arrow_forwardExercise 15-9 (Algo) Lessor calculation of annual lease payments; lessee calculation of asset and liability [LO15-2] Each of the three independent situations below describes a finance lease in which annual lease payments are payable at the beginning of each year. The lessee is aware of the lessor's implicit rate of return. Note: Use tables, Excel, or a financial calculator. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) Lease term (years) Lessor's rate of return (known by lessee) Lessee's incremental borrowing rate Fair value of lease asset Situation 1 Situation 2 Situation 3 Lease Payments Right-of-use Asset/Lease 1 Payable 10 10% 11% $790,000 Situation 2 20 8% 9% Required: a. & b. Determine the amount of the annual lease payments as calculated by the lessor and the amount the lessee would record as a right-of-use asset and a lease liability, for each of the above situations. Note: Round your answers to the nearest whole dollar. $1,170,000 5 11% 10% $375,000arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education

Accounting for Finance and Operating Leases | U.S. GAAP CPA Exams; Author: Maxwell CPA Review;https://www.youtube.com/watch?v=iMSaxzIqH9s;License: Standard Youtube License