Concept explainers

Videos

Devon Bishop, age 45, is single. He lives at 1507 Rose Lane, Albuquerque, NM 87131. His Social Security number is 111-11-1117. Devon does not want $3 to go to the Presidential Election Campaign Fund.

Devon’s wife, Ariane, passed away in 2014. Devon’s son, Tom, who is age 18, resides with Devon. Tom’s Social Security number is 123-45-6788.

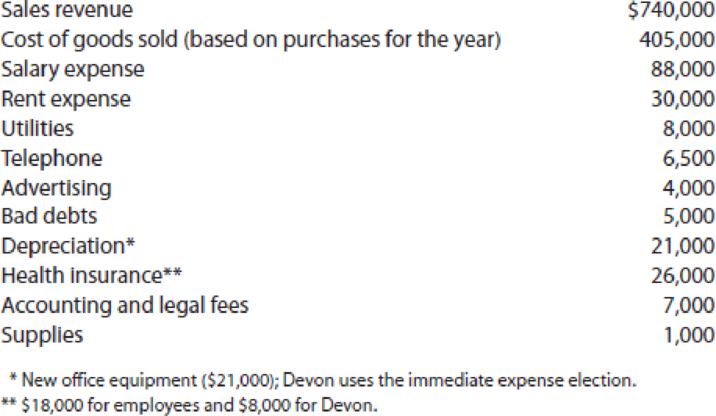

Devon owns a sole proprietorship for which he uses the accrual method of accounting and maintains no inventory; the business operates as Devon’s Copy Shop, 422 E. Main Street, Albuquerque, NM 87131, IRS business activity code: 453990. His revenues and expenses for 2018 are as follows.

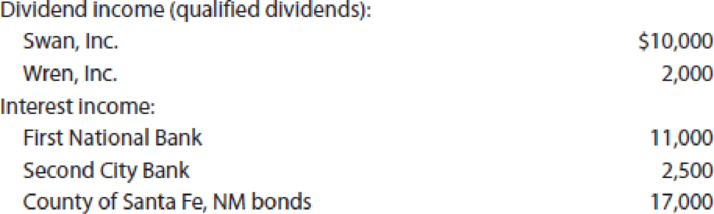

Other income received by Devon includes the following.

During the year, Devon and his sole proprietorship were involved in the following property transactions. Stock transactions were reported to Devon on Form 1099–B; basis was not reported to the IRS.

- a. Sold Blue, Inc. stock for $45,000 on March 12, 2018. He had purchased the stock on September 5, 2015, for $50,000.

- b. Received an inheritance of $300,000 from his uncle, Henry. Devon used $200,000 to purchase Green, Inc. stock on May 15, 2018, and invested $100,000 in Gold, Inc. stock on May 30, 2018.

- c. Received Orange, Inc. stock worth $9,500 as a gift from his aunt, Jane, on June 17, 2018. Her adjusted basis for the stock was $5,000. No gift taxes were paid on the transfer. Jane had purchased the stock on April 1, 2012. Devon sold the stock on July 1, 2018, for $22,000.

- d. On July 15, 2018, Devon sold one-half of the Green, Inc. stock for $40,000.

- e. Devon was notified on August 1, 2018, that Yellow, Inc. stock he purchased from a colleague on September 1, 2017, for $52,500 had become worthless. Although he understood that investing in Yellow was risky, Devon did not anticipate that the corporation would declare bankruptcy.

- f. On August 15, 2018, Devon received a parcel of land in Phoenix worth $220,000 in exchange for a parcel of land he owned in Tucson. Because the Tucson parcel was worth $245,000, he also received $25,000 cash. Devon’s adjusted basis for the Tucson parcel was $210,000. He originally purchased it on September 18, 2015.

- g. On December 1, 2018, Devon sold the condominium in which he had been living for the past 20 years (1844 Lighthouse Lane, Albuquerque, NM 87131) and moved into a rented townhouse. The sales price was $480,000, selling expenses were $28,500, and repair expenses related to the sale were $9,400. Devon purchased the condominium for $180,000.

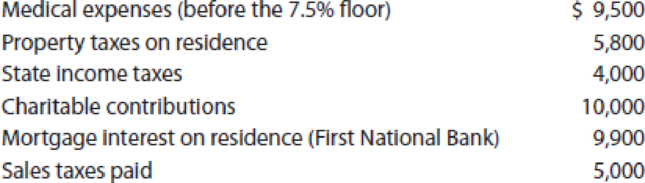

Devon’s potential itemized deductions, exclusive of the aforementioned information, are as follows.

During the year, Devon makes estimated Federal income tax payments of $35,000.

Compute Devon’s lowest net tax payable or refund due for 2018 assuming that he makes any available elections that will reduce the tax. If you use tax forms for your computations, you will need Form 1040 and its Schedules 1, 4, 5, A, B, C, D, and SE and Forms 4562, 8824, and 8949. Suggested software: ProConnect Tax Online.

Compute the lowest net tax payable or refund due for 2018.

Explanation of Solution

Compute the lowest net tax payable or refund due for 2018:

| Particulars | Amount ($) |

| Business income (Note 1) | $146,500 |

| Dividend Income | $12,000 |

| Interest income | $13,500 |

| Capital loss (Note 3) | ($3,000) |

| Self employment tax deduction (Note 4) | ($9,923) |

| Self employed health insurance (Note 4) | ($8,000) |

| Adjusted gross income | $151,077 |

| Less: Itemized deductions (Note 6) | ($29,900) |

| Deduction for qualifies business income (Note 7) | ($21,835) |

| Taxable income | $99,342 |

| Income tax computation: | |

| Tax on taxable income of $99,342 (Note 8) | $15,656 |

| Self employment tax (Note 4) | $19,845 |

| Tax liability before prepayments and credits | $35,501 |

| Less: Estimated tax payments | ($35,000) |

| Dependent tax credit (Note 9) | ($500) |

| Net tax payable (or refund) for 2018 | $1 |

Table (1)

Therefore, Net tax payable for the year 2018 is $1

Working note 1: Compute the business income:

| Particulars | Amount ($) | Amount ($) |

| Sales revenue | $740,000 | |

| Less: Cost of goods sold | ($405,000) | |

| Gross profit | $335,000 | |

| Less: Salary expense | $88,000 | |

| Rent expense | $30,000 | |

| Utilities | $8,000 | |

| Telephone | $6,500 | |

| Advertising | $4,000 | |

| Bad debts | $5,000 | |

| Depreciation | $21,000 | |

| Health insurance for employees | $18,000 | |

| Accounting and legal fees | $7,000 | |

| Supplies | $1,000 | ($188,500) |

| Net income | $146,500 |

Table (2)

Note: Out of the health insurance payments, only the $18,000 of health insurance paid for employees is allowed as a deduction while computing the net income of the sole proprietorship. The $8,000 paid for Person D eligible as a deduction for AGI.

Working Note 2: The amount of $17,000 interest on the County of SF, NM bonds is expelled from the gross income.

Working note 3: Compute the capital loss:

Compute the recognized gain or loss for each item:

Item a:

| Particulars | Amount ($) |

| Amount realized | $45,000 |

| Less: Adjusted basis | ($50,000) |

| Realized loss | ($5,000) |

| Recognized loss (long-term capital loss) | ($5,000) |

Table (3)

Item b: The $300,000 inheritance is barred from Person D’s gross income. His adjusted basis for Incorporation GR’s stock is the cost of $200,000, and his adjusted basis for Incorporation G’s, stock is $100,000.

Item c: Gifts are expelled from Person D’s gross income. His adjusted basis for the Incorporation O’s stock is a postpone basis of $5,000. His holding period also is a postpone holding period (i.e., it comprises Person J’s holding period, which began April 1, 2012).

| Item c. | |

| Amount realized | $22,000 |

| Less: Adjusted basis | ($5,000) |

| Realized gain | $17,000 |

| Recognized gain (long-term capital gain) | $17,000 |

Table (4)

Item d:

| Item d. | |

| Amount realized | $40,000 |

| Less: Adjusted basis | ($100,000) |

| Realized loss | ($60,000) |

| Recognized loss (short-term capital loss) | ($60,000) |

Table (5)

Item e:

| Item e. | |

| Amount realized | $0 |

| Less: Adjusted basis | ($52,500) |

| Realized loss | ($52,500) |

| Recognized loss (long-term capital loss) | ($52,500) |

Table (6)

Item f:

| Item f. | |

| Amount realized | $245,000 |

| Less: Adjusted basis | ($210,000) |

| Realized gain | $35,000 |

| Recognized gain (long-term capital gain) | $25,000 |

Table (7)

Item g:

| Item g. | |

| Amount realized | $451,500 |

| Less: Adjusted basis | ($180,000) |

| Realized gain | $271,500 |

| § 121 exclusion | ($250,000) |

| Recognized gain (long-term capital gain) | $21,500 |

Table (8)

Person D eligible’s for the § 121 exclusion since he has owned and occupied the residence as his principal residence throughout at least two of the five years prior to the date of sale. Therefore, his realized gain of $271,500 is decreased to $21,500.

Repair expenses of amount $9,400 are neither capitalizable nor allowed as deduction.

Person D’s capital gains and losses are abridged as follows:

| Long term capital gains: | ||

| Incorporation O’s stock | $17,000 | |

| Residence | 21,500 | |

| T land | 25,000 | $63,500 |

| Long-term capital losses: | ||

| Incorporation B’s stock | ($5,000) | |

| Incorporation Y stock | ($52,500) | ($57,500) |

| Net long-term capital gain | $6,000 | |

| Short-term capital loss: | ||

| Incorporation G’s stock | ($60,000) | |

| Net capital loss | ($54,000) |

Table (9)

Out of $54,000 capital loss, only $3,000 of the net capital loss can be allowed as a deduction in the year 2018. The balance amount of $51,000 is carried forwarded to the following year (2019).

Working note 4: Compute the self-employment tax:

| Particulars | Amount ($) |

| Step 1: Net profit from Schedule C (line 31 of Schedule C) | $146,500 |

| Step 2: Multiply step 1 amount by 92.35% | $135,293 |

| Step 3: If the amount in step 2 is $128,400 or less, multiply the step 2 amount by 15.3%. If the step 2 amount is more than $128,400, multiply the excess of the step 2 amount ($135,293) over $128,400 by 2.9% and add $19,645.20. This is the self-employment tax. | $19,845.10 |

Table (10)

The deduction for AGI for part of the self-employment tax is $9,923 (50% of $19,845.10).

Working note 5: Out of the amount $8,000 of health insurance premiums paid for Person D 100% is allowed as a deduction for AGI.

Working note 6: Compute the itemized deductions:

| Itemized deductions: | |

| Medical expenses | $0 |

| Property taxes and sales taxes (greater than $4,000 state income taxes); limited to $10,000 | $10,000 |

| Charitable contributions | $10,000 |

| Mortgage interest | $9,900 |

| Total itemized deductions | $29,900 |

Table (11)

Working note 7: Person D’s taxable income previous to the eligible business income deduction is $121,177

- (a) 20% of qualified business income $25,175

- (b) 20% of taxable income prior to the qualified business income deduction, decreased by any net capital gain (including any qualified dividends) is $21,835

Working note 8: Compute the taxable income:

All of Person D’s qualified dividends of $12,000 are taxed at 15% as his taxable income net of the qualified dividends goes above $51,700 and the head-of-household zero percent rate thresholds.

| Particulars | Amount ($) |

| Taxable income | $99,342 |

| Qualified dividends | ($12,000) |

| Portion of taxable income taxed at regular tax rates | $87,342 |

| Tax on qualified dividends | $1,800 |

| Tax on $87,342 from the 2018 Tax Tables (Head of Household) | 13,856 |

| Tax on taxable income | $15,656 |

Table (12)

Working note 9: Determine the dependent tax credit:

The child tax credit is not available (As Person T is 18, hence he is not eligible as child). But, Person T does qualify for a dependent tax credit of $500.

Want to see more full solutions like this?

Chapter 15 Solutions

Individual Income Taxes

- John Benson, age 40, is single. His Social Security number is 111-11-1111, and he resides at 150 Highway 51, Tangipahoa, LA 70465. John has a 5-year-old child, Kendra, who lives with her mother, Katy. As a result of his divorce in 2016, John pays alimony of 6,000 per year to Katy and child support of 12,000. The 12,000 of child support covers 65% of Katys costs of rearing Kendra. Kendras Social Security number is 123-45-6789, and Katys is 123-45-6788. Johns mother, Sally, lived with him until her death in early September 2019. He incurred and paid medical expenses for her of 15,588 and other support payments of 11,000. Sallys only sources of income were 5,500 of interest income on certificates of deposit and 5,600 of Social Security benefits, which she spent on her medical expenses and on maintenance of Johns household. Sallys Social Security number was 123-45-6787. John is employed by the Highway Department of the State of Louisiana in an executive position. His salary is 95,000. The appropriate amounts of Social Security tax and Medicare tax were withheld. In addition, 9,500 was withheld for Federal income taxes and 4,000 was withheld for state income taxes. In addition to his salary, Johns employer provides him with the following fringe benefits. Group term life insurance with a maturity value of 95,000; the cost of the premiums for the employer was 295. Group health insurance plan; Johns employer paid premiums of 5,800 for his coverage. The plan paid 2,600 for Johns medical expenses during the year. Upon the death of his aunt Josie in December 2018, John, her only recognized heir, inherited the following assets. Three months prior to her death, Josie gave John a mountain cabin. Her adjusted basis for the mountain cabin was 120,000, and the fair market value was 195,000. No gift taxes were paid. During the year, John reported the following transactions. On February 1, 2019, he sold for 45,000 Microsoft stock that he inherited from his father four years ago. His fathers adjusted basis was 49,000, and the fair market value at the date of the fathers death was 41,000. The car John inherited from Josie was destroyed in a wreck on October 1, 2019. He had loaned the car to Katy to use for a two-week period while the engine in her car was being replaced. Fortunately, neither Katy nor Kendra was injured. John received insurance proceeds of 16,000, the fair market value of the car on October 1, 2019. On December 28, 2019, John sold the 300 acres of land to his brother, James, for its fair market value of 160,000. James planned on using the land for his dairy farm. Other sources of income for John are: Potential itemized deductions for John, in addition to items already mentioned, are: Part 1Tax Computation Compute Johns net tax payable or refund due for 2019. Part 2Tax Planning Assume that rather than selling the land to James, John is considering leasing it to him for 12,000 annually with the lease beginning on October 1, 2019. James would prepay the lease payments through December 31, 2019. Thereafter, he would make monthly lease payments at the beginning of each month. What effect would this have on Johns 2019 tax liability? What potential problem might John encounter? Write a letter to John in which you advise him of the tax consequences of leasing versus selling. Also prepare a memo addressing these issues for the tax files.arrow_forwardRobert A. Kliesh, age 41, is single and has no dependents. Roberts Social Security number is 111-11-1115. His address is 201 Front Street, Missoula, MT 59812. He does not contribute to the Presidential Election Campaign fund through the Form 1040. Robert works as a financial analyst and is very well regarded in his field. This year his salary totaled 650,000. His professional success has allowed him to purchase investments in real estate and corporate stocks and bonds. He also spends time volunteering with various organizations that help people develop financial literacy skills. Examination of Roberts financial records provides the following information for 2018. a. On January 16, Robert sold 1,000 shares of stock for a loss of 12,000. The stock was acquired 14 months ago for 17,000 and sold for 5,000. On February 15, he sold 400 shares of stock for a gain of 13,100. That stock was acquired in 2010 for 6,000 and sold for 19,100. b. He received 30,000 of interest on private activity bonds that he purchased in 2015. He also received 40,000 of interest on tax-exempt bonds that are not private activity bonds. c. Robert received gross rent income of 190,000 from an apartment complex he owns. He qualifies as an active participant in the activity. The property is at 50 Big Sky Resort Road, Big Sky, Montana, 59716. d. Expenses related to the apartment complex, acquired in 2009, were 225,000. e. Roberts taxable interest income, all from corporate bonds, totaled 23,000. Because he invests only in growth stocks, he receives no dividend income. f. He won 60,000 in the Montana lottery. g. Robert was the beneficiary of an 800,000 life insurance policy on the life of his uncle Jake. He received the proceeds in October. h. In February, Robert exercised an incentive stock option that was granted by his employer in 2015. The strike price of the option was 10 per share. On the date of exercise, the fair market value of the stock was 25 per share. Robert purchased 400 shares with the option; as of the end of the year, he still owns the stock (current FMV 20 per share). i. Robert incurred the following potential itemized deductions. 5,200 fair market value of stock contributed to the Red Cross (3,000 stock basis). He had owned the stock for two years. Robert also made cash contributions of 8,000 to qualified organizations during the year. 4,200 interest on consumer purchases. 8,900 state and local income tax. 15,000 of medical expenses that he paid on behalf of his administrative assistant, who unexpectedly took ill. 8,000 paid for lottery tickets associated with playing the state lottery. 750 contribution to the campaign of the Democratic candidate for governor of Montana. Because Robert lived in Montana, he paid no state-income tax. Robert made estimated Federal tax payments of 210,000, and he was covered by health insurance for the entire tax year. Use Forms 1040 and 6251 and Schedules A, B, D, and E to compute the tax liability (including AMT) for Robert A. Kliesh for 2018. Omit Forms 8283, 8582, and 8949. Suggested software: ProConnect Tax Online.arrow_forwardAshley Panda lives at 1310 Meadow Lane, Wayne, OH 43466, and her Social Security number is 123-45-6777. Ashley is single and has a 20-year-old son, Bill. His Social Security number is 111-11-1112. Bill lives with Ashley, and she fully supports him. Bill spent 2018 traveling in Europe and was not a college student. He had gross income of 4,655 in 2018. Bill paid 4,000 of lodging expenses that Ashley reimbursed after they were fully documented. Ashley paid the 4,000 to Bill using a check from her sole proprietorship. That amount is not included in the items listed below. Ashley had substantial health problems during 2018, and many of her expenses were not reimbursed by her health insurance. Ashley owns Panda Enterprises, LLC (98-7654321), a data processing service that she operates as a sole proprietorship. Her business is located at 456 Hill Street, Wayne, OH 43466. The business activity code is 514210. Her 2018 Form 1040, Schedule C for Panda Enterprises shows revenues of 315,000, office expenses of 66,759, employee salary of 63,000, employee payroll taxes of 4,820, business meal expenses (before the 50% reduction) of 22,000, and rent expense of 34,000. The rent expense includes payments related to renting an office (30,000) and payments related to renting various equipment (4,000). There is no depreciation because all depreciable equipment owned has been fully depreciated in previous years. No fringe benefits are provided to the employee. Ashley personally purchases health insurance on herself and Bill. The premiums are 23,000 per year. Ashley has an extensive stock portfolio and has prepared the following analysis: Note: Ashley received a Form 1099B from her stockbroker that included the adjusted basis and sales proceeds for each of her stock transactions. The per-share cost includes commissions, and the per-share selling price is net of commissions. Also, the dividends are the actual dividends received in 2018, and these are both ordinary dividends and qualified dividends. Ashley had 800 of interest income from State of Ohio bonds and 600 of interest income on her Wayne Savings Bank account. She paid 25,000 of alimony to her former husband. His Social Security number is 123-45-6788. Ashley itemizes her deductions and provides the following information, which may be relevant to her return: Ashley made a 26,000 estimated Federal income tax payment, does not want any of her taxes to finance presidential elections, has no foreign bank accounts or trusts, and wants any refund to be applied against her 2019 taxes. Compute Ashleys net tax payable or refund due for 2018. If you use tax forms for your computations, you will need Form 1040 and its Schedules 1, 4, 5, A, C, D, and SE and Form 8949. Ashley qualifies for the 199A deduction for qualified business income. Be sure to include that in your calculations. Suggested software: ProConnect Tax Online.arrow_forward

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT