Videos

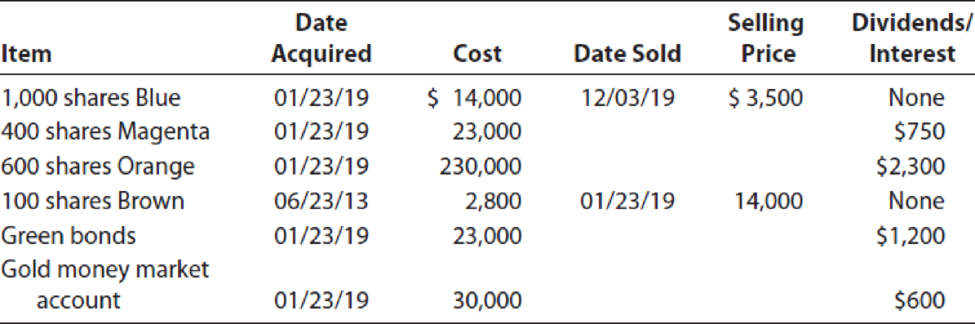

Paul Barrone is a graduate student at State University. His 10-year-old son, Jamie, lives with him, and Paul is Jamie’s sole support. Paul’s wife died in 2018, and Paul has not remarried. Paul received $320,000 of life insurance proceeds (related to his wife’s death) in early 2019 and immediately invested the entire amount as shown below.

Paul had $42,000 of taxable graduate assistant earnings from State University and received a $10,000 scholarship. He used $8,000 of the scholarship to pay his tuition and fees for the year and $2,000 for Jamie’s day care. Jamie attended Little Kids Daycare Center, a state-certified child care facility. Paul received a statement related to the Green bonds saying that there was $45 of original issue discount amortization during 2019. Paul maintains the receipts for the sales taxes he paid of $735.

Paul lives at 1610 Cherry Lane, Bradenton, FL 34212, and his Social Security number is 111-11-1111. Jamie’s Social Security number is 123-45-6789. The university withheld $2,000 of Federal income tax from Paul’s salary. Paul is not itemizing his deductions.

Part 1—Tax Computation

Compute Paul’s lowest tax liability for 2019.

Part 2—Tax Planning

Paul is concerned because the Green bonds were worth only $18,000 at the end of 2019, $5,000 less than he paid for them. He is an inexperienced investor and wants to know if this $5,000 is deductible. The bonds had original issue discount of $2,000 when he purchased them, and he is curious about how that affects his investment in the bonds. The bonds had 20 years left to maturity when he purchased them. Draft a brief letter to Paul explaining how to handle these items.

Also prepare a memo for Paul’s tax file.

Trending nowThis is a popular solution!

Chapter 16 Solutions

Individual Income Taxes

- Nadia died in 2018 and is survived by her husband, Jerold (age 44); her married son, Travis (age 22); and her daughter-in-law, Macy (age 18). Jerold is the executor of his wifes estate. He maintains the household where he, Travis, and Macy live and furnishes all of their support. During 2018 and 2019, Travis is a full-time student, and Macy earns 7,000 each year from a part-time job. Travis and Macy do not file jointly during either year. What is Jerolds filing status for 2018 and 2019 if all parties reside in: a. Idaho (a community property state)? b. Kansas (a common law state)?arrow_forwardGreg died on July 1,2019 , and left Lea, his wife, a $45,000 life insurance policy which she elects to receive at $9,000 per year plus interest for 5 years. In the current year, Lea receives $9,500. How much should Lea include in her gross income? $____________arrow_forwardJed, age 55, is married with no children. During 2019, Jed had the following income and expense items: a. Three years ago, Jed loaned a friend 10,000 to help him purchase a new car. In June of the current year, Jed learned that his friend had been declared bankrupt and had left the country. There is no possibility that Jed will ever collect any of the 10,000. b. In April of last year, Jed purchased some stock for 5,000. In March of the current year, the company was declared bankrupt, and Jed was notified that his shares of stock were worthless. c. Several years ago Jed purchased some 1244 stock for 120,000, This year he sold the stock for 30,000. d. In July of this year, Jed sold some land that he had held for two years for 60,000. He had originally paid 42,000 for the land. e. Jed received 40,000 of interest income from State of Minnesota bonds. f. In September, Jeds home was damaged by an earthquake; Jeds county was declared a Federal disaster area by the President. Jeds basis in his home was 430,000. The value of the home immediately before the quake was 610,000. After the quake, the home was worth 540,000. Because earthquake damage was an exclusion on Jeds homeowners insurance policy, he received no insurance recovery. g. Jed received a salary of 80,000. h. Jed paid home mortgage interest of 14,000. i. If Jed files a joint return for 2019, determine his NOL. for the year.arrow_forward

- In 2019, Lou has a salary of $53,300 from her job. She also has interest income of $1,600 and dividend income of $ 400. Lou is single and has no dependents. During the year, Lou sold silver coins held as an investment for a $7,000 loss. Calculate the following amounts for Lou: Adjusted gross income $ ____________________ Standard deduction $ ____________________ Taxable income $ ____________________arrow_forwardEllie purchases an insurance policy on her life and names her brother, Jason, as the beneficiary. Ellie pays 32,000 in premiums for the policy during her life. When she dies, Jason collects the insurance proceeds of 500,000. As a result, how much gross income does Jason report?arrow_forward

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT