Concept explainers

(1)

Pension expense: Pension expense is an expense to the employer paid as compensation after the completion of services performed by the employees.

Pension expense includes the following components:

- Service cost

- Interest cost

- Expected return on plan assets

- Amortization of prior service cost

- Amortization of net loss or net gain

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in

stockholders’ equity accounts. - Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

To determine: The pension expense for 2016 and record the respective pension related entries

(1)

Answer to Problem 17.16P

Compute the pension expense for 2016.

| Particulars | Amount ($) |

| Service cost | $48,000,000 |

| Interest cost | 24,000,000 |

| Expected return on the plan assets | (20,000,000) |

| Amortization of prior service cost | 4,000,000 |

| Amortization of net (gain) or loss–OCI | 1,000,000 |

| Pension expense | $57,000,000 |

Table (1)

Explanation of Solution

Working Note:

Compute expected return on plan assets.

Compute the amortization of Net Loss – AOCI.

| Particulars | Amount ($) |

| Net Loss – AOCI (Previous losses exceeded previous gains) | $40,000,000 |

| 10% of $300 ($300 is Greater than $200) | (30,000,000) |

| Amount to be Amortized | $10,000,000 |

| Divided by Number of Years | ÷ 10 years |

| Amortization of net loss | $1,000,000 |

Table (2)

Journalize pension expense for 2016 (Refer to Table (1) for all the values).

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | |

| ($ in Millions) | |||||

| Pension Expense | 57 | ||||

| Plan Assets | 20 | ||||

| Projected Benefit Obligation (PBO) | 72 | ||||

| Amortization of Prior Service Cost–OCI | 4 | ||||

| Amortization of Net Loss–OCI | 1 | ||||

| (To record pension expense) | |||||

Table (3)

- Pension Expense is an expense account. Expenses decrease Equity value, and a decrease in equity is debited.

- Plan Assets is an asset account. The return on assets increases plan assets, and an increase in assets is debited.

- PBO is a liability account. Service cost and interest cost increase PBO, and an increase in liability is credited.

- Amortization of Prior Service Cost–OCI is a contra to Prior Service Cost–OCI account. Since amortization reduces prior service cost balance, it is credited because Prior Service Cost–OCI account is debited.

- Amortization of Net Loss–OCI is a contra to Net Loss–OCI account. Since amortization reduces net loss balance, it is credited because Net Loss–OCI account is debited.

Journalize the amount funded to pension funds of plan assets.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | |

| Plan Assets | 45,000,000 | ||||

| Cash | 45,000,000 | ||||

| (To record plan assets being funded) | |||||

Table (4)

- Plan Assets is an asset account. Since cash is contributed to plan assets, assets are increased, and an increase in assets is debited.

- Cash is an asset account. Since cash is contributed by the company, asset amount is decreased and a decrease in asset is credited.

Journalize the amount of pension paid to retirees.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | |

| PBO | 20,000,000 | ||||

| Plan Assets | 20,000,000 | ||||

| (To record the pension being paid and liability reduced) | |||||

Table (5)

- PBO is a liability account. Since the pension benefits are paid to retirees, the liability to pay decreases, and a decrease in liability is debited.

- Plan Assets is an asset account. Since cash is paid to retirees, assets are decreased, and a decrease in assets is credited.

(2)

To journalize: Gains and losses of 2016.

(2)

Explanation of Solution

Journalize the gains and losses related to plan assets.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | |

| Loss–OCI | 5,000,000 | ||||

| Plan Assets | 5,000,000 | ||||

| (To record loss related to plan assets) | |||||

Table (6)

- Loss–OCI is a loss or expense account. Losses and expenses reduce shareholders’ equity, and a reduction in shareholders’ equity is debited.

- Plan Assets is an asset account. Since loss occurred due to excess of expected return ($20,000,000) over actual return ($15,000,000), assets are decreased by $5,000,000

Journalize the gain – other comprehensive income.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | |

| Projected Benefit Obligation | 2,000,000 | ||||

| Gain – OCI | 2,000,000 | ||||

| (To record gains related to PBO) | |||||

Table (7)

- PBO is a liability account. Since liability has decreased, and a decrease in liability is debited, so PBO is debited.

- Gain–OCI is a gain or revenue account. Gains and revenues increase shareholders’ equity, and an increase in shareholders’ equity is credited.

(3)

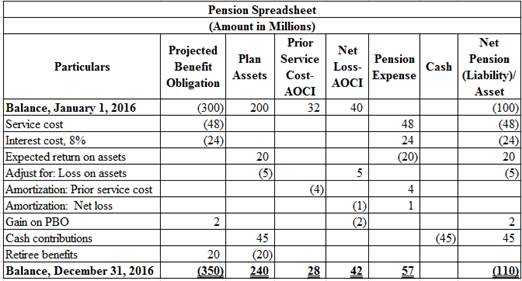

To prepare: Pension spreadsheet for L Cable for 2016.

(3)

Explanation of Solution

Prepare pension spreadsheet for L Cable for 2016.

Figure (1)

(4)

The pension expense for 2017 and record the respective pension related entries.

(4)

Answer to Problem 17.16P

Compute the pension expense for 2017.

| Particulars | Amount ($) |

| Service cost | $38,000,000 |

| Interest cost | 28,000,000 |

| Expected return on the plan assets | (24,000,000) |

| Amortization of prior service cost | 4,000,000 |

| Amortization of net (gain) or loss–OCI | 700,000 |

| Pension expense | $46,700,000 |

Table (8)

Explanation of Solution

Working Note:

Compute the expected return on plan assets.

Compute the amortization of Net Loss – AOCI.

| Particulars | Amount ($) |

| Net Loss – AOCI (Previous losses exceeded previous gains) | $42,000,000 |

| 10% of $350 ($350 is Greater than $240) | (35,000,000) |

| Amount to be Amortized | $7,000,000 |

| Divided by Number of Years | ÷ 10 years |

| Amortization | $700,000 |

Table (9)

Journalize pension expense for 2017 (Refer to Table (8) for all the values).

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | |

| ($ in Millions) | |||||

| Pension Expense | 46.7 | ||||

| Plan Assets | 24.0 | ||||

| Projected Benefit Obligation (PBO) | 66.0 | ||||

| Amortization of Prior Service Cost–OCI | 0.7 | ||||

| Amortization of Net Loss–OCI | 4.0 | ||||

| (To record pension expense) | |||||

Table (10)

- Pension Expense is an expense account. Expenses decrease Equity value, and a decrease in equity is debited.

- Plan Assets is an asset account. The return on assets increases plan assets, and an increase in assets is debited.

- PBO is a liability account. Service cost and interest cost increase PBO, and an increase in liability is credited.

- Amortization of Prior Service Cost–OCI is a contra to Prior Service Cost–OCI account. Since amortization reduces prior service cost balance, it is credited because Prior Service Cost–OCI account is debited.

- Amortization of Net Loss–OCI is a contra to Net Loss–OCI account. Since amortization reduces net loss balance, it is credited because Net Loss–OCI account is debited.

Journalize the amount funded to pension funds of plan assets.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | |

| Plan Assets | 30,000,000 | ||||

| Cash | 30,000,000 | ||||

| (To record plan assets being funded) | |||||

Table (11)

- Plan Assets is an asset account. Since cash is contributed to plan assets, assets are increased, and an increase in assets is debited.

- Cash is an asset account. Since cash is contributed by the company, asset amount is decreased and a decrease in asset is credited.

Journalize the amount of pension paid to retirees.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | |

| PBO | 16,000,000 | ||||

| Plan Assets | 16,000,000 | ||||

| (To record the pension being paid and liability reduced) | |||||

Table (12)

- PBO is a liability account. Since the pension benefits are paid to retirees, the liability to pay decreases, and a decrease in liability is debited.

- Plan Assets is an asset account. Since cash is paid to retirees, assets are decreased, and a decrease in assets is credited.

(5)

To journalize: Gains and losses of 2017.

(5)

Explanation of Solution

Journalize the gains and losses related to pension obligation.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | |

| Loss–OCI | 5,000,000 | ||||

| PBO | 5,000,000 | ||||

| (To record gains related to PBO) | |||||

Table (13)

- Loss–OCI is a loss or expense account. Losses and expenses reduce shareholders’ equity, and a reduction in shareholders’ equity is debited.

- PBO is a liability account. Since liability has increased, and an increase in liability is credited, so PBO is credited.

Journalize the gains and losses related to plan assets.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | |

| Plan Assets | 12,000,000 | ||||

| Gain–OCI | 12,000,000 | ||||

| (To record gain related to plan assets) | |||||

Table (14)

- Plan Assets is an asset account. Since gain occurred due to excess of actual return ($36,000,000) over expected return ($24,000,000), assets are increased by $12,000,000

- Gain–OCI is a gain or revenue account. Gains and revenues increase shareholders’ equity, and an increase in shareholders’ equity is credited.

(6)

To compute: The balances in net loss–AOCI, and prior service cost–AOCI accounts, as at December 31, 2017.

(6)

Explanation of Solution

Prepare T-account of net loss–AOCI to compute the balance as at December 31, 2017.

| Net Loss–AOCI | ||||||

| Date | Details | Debit | Date | Details | Credit | |

| (Dollars in Millions) | ||||||

| Balance, January 1 | $42.0 | New gain | $12.0 | |||

| New loss | 5.0 | Amortized loss in 2017 | 0.7 | |||

| Total | 47.0 | Total | 12.7 | |||

| Ending Balance | $34.3 | |||||

Table (15)

Thus, balance of net loss–AOCI as at December 31, 2017 is $34,300,000.

Prepare T-account of prior service cost–AOCI to compute the balance as at December 31, 2017.

| Prior Service Cost–AOCI | ||||||

| Date | Details | Debit | Date | Details | Credit | |

| (Dollars in Millions) | ||||||

| Balance, January 1 | $28 | Amortized prior service cost | $4 | |||

| Total | 28 | Total | 4 | |||

| Ending Balance | $24 | |||||

Table (16)

Thus, balance of prior service cost–AOCI as at December 31, 2017 is $24,000,000.

(7)

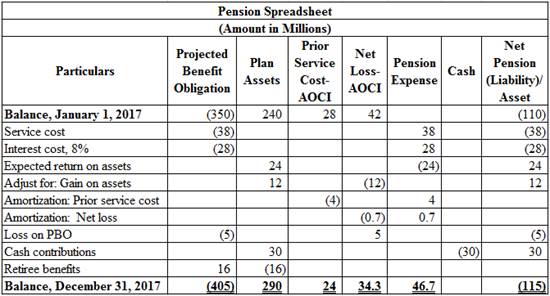

To prepare: Pension spreadsheet for L Cable for 2017.

(7)

Explanation of Solution

Prepare pension spreadsheet for L Cable for 2017.

Figure (2)

Want to see more full solutions like this?

Chapter 17 Solutions

INTER. ACC W/ ACCESS+AIRFRANCE >IC< (L

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education