Videos

Research Case 18–4

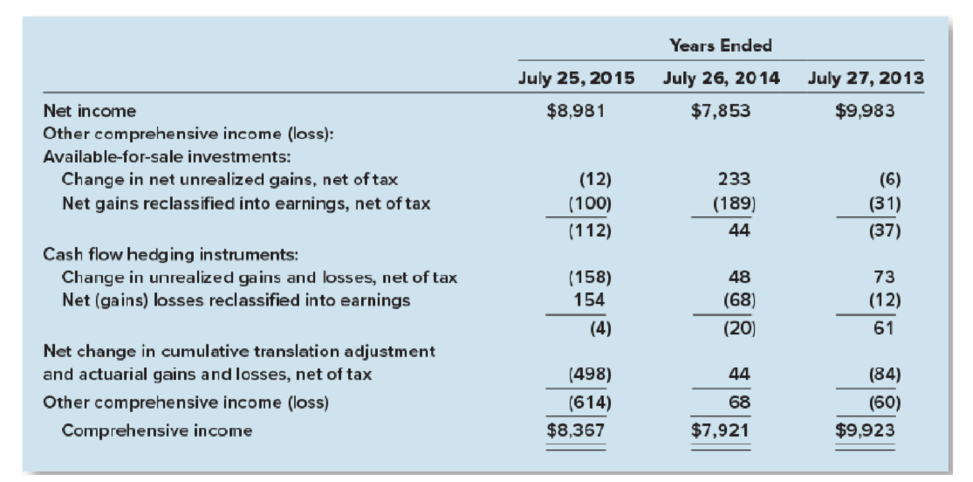

FASB codification; comprehensive income; locate and extract relevant information and authoritative support for a financial reporting issue; integrative; Cisco Systems

• LO18–2

Real World Financials

Required:

1. Locate the financial statements of Cisco at www.sec.gov or Cisco’s website. Search the 2015 annual report for information about how Cisco accounts for comprehensive income. What does Cisco report in its

2. Access the FASB Accounting Standards Codification at the FASB website (www.fasb.org). Identify the specific citation from the authoritative literature that describes the two alternative formats for reporting comprehensive income.

3. What is comprehensive income? How does it differ from net income? Where is it reported in a balance sheet?

4. One component of Other comprehensive income for Cisco is “net unrealized gains on investments.” What does this mean? From the information Cisco’s financial statements provide, determine how the company calculated the $61 million accumulated other comprehensive income at the end of fiscal 2015.

5. What might be possible causes for the “Other” component of Cisco’s Other comprehensive income? Alcoa is the world’s leading producer of primary aluminum, fabricated aluminum, and alumina. The following is a press release from the company:

Want to see the full answer?

Check out a sample textbook solution

Chapter 18 Solutions

INTERMEDIATE ACCOUNTING W/CONNECT

- Acc 202 Finance reporting Tutorial A conceptual framework can be defined as a system of ideas and objectives that lead to the creation of a consistent set of rules and standards. Specifically in accounting, the rule and standards set the nature, function and limits of financial accounting and financial statements. Question I. What is conceptual framework in accounting? II. Discuss whether a conceptual framework is necessary. III. Outline the advantages and disadvantages of a conceptual framework. IV. Summarize the finance reporting af the chapter 1 - chapter 8 of the conceptual framework.arrow_forwardQuestion 1 Segment disclosures are widely regarded as some of the most useful disclosures in financial reports because of the extent to which they disaggregate financial information into meaningful and often revealing groups. Discuss the objectives of segmental information and the requirements for the disclosure of segmental information in annual reports.arrow_forwardCase Study: Navigating the FASB Accounting Standards Codification (ASC)** *Introduction:* The FASB Accounting Standards Codification (ASC) serves as the authoritative source for U.S. generally accepted accounting principles (GAAP). It is a comprehensive system designed to organize and present accounting standards in a logical and accessible manner. In this case study, we explore the components included and excluded from the FASB ASC. *Components of FASB ASC:* 1. **AICPA Statements of Position (SOP):** - SOPs issued by the American Institute of Certified Public Accountants (AICPA) were included in the FASB ASC during its initial implementation. However, updates to the ASC may have modified this inclusion. 2. **FASB Statements:** - FASB Statements are a core part of the FASB ASC. These statements represent authoritative guidance on various accounting topics, ensuring consistency in financial reporting. 3. **Accounting Research Bulletins (ARB):** - ARBs were issued by…arrow_forward

- e 1:E1 OMANTEL Practice (page 5 . ... moodle.nct.edu.om P Flag question Timely payment of taxes comes under objective of financial managment a. Social Objectives b. Research Objectives c. None d. Basic objectives e. Operational Objectives العربية الإنجليزيةarrow_forwardMatch the correct term with its definition. A. Financial Accounting Standards Board FASB) i. used by the FASB, which is a set of concepts that guide financial reporting B. generally accepted accounting principles (GAAP) ii. independent, nonprofit organization that sets financial accounting and reporting standards for both public- and private-sector businesses that use generally accepted accounting principles (GAAP) here in the United States C. Securities and Exchange Commission SEC) iii. standards, procedures, and principles companies must follow when preparing their financial statements D. conceptual framework iv. assumes a business will continue to operate in the foreseeable future E. going concern assumption v. independent federal agency protecting the interests of investors, regulating stock markets, and ensuring companies adhere to GAAP requirements F. time period assumption vi. companies can present useful information in shorter time periods such as years, quarters, or monthsarrow_forwardChoose the best EBIT-EPS analysis helps organisation understand the effect of changes in resulting due to O EPS, EBIT under different financial combinations O EBIT, EPS O EPS, EBT O PAT, EPS Deepanshu | Support +1 650-924-9221 +91 80 4719 0917 metti P Type here to searcharrow_forward

- Knowledge Check 01 Which of the following statements about the equity method are true? Note: Select all that apply. Check All That Apply International accounting standards require the equity method for use with significant influence investees. U.S. GAAP require the equity method for use with significant influence investees. U.S. GAAP requires that the accounting policies of investees be adjusted to correspond to those of the investor when applying the equity method. Both IFRS and U.S. GAAP provide the fair value option for all investments that qualify for the equity method.arrow_forwardComprehension questions 11 and 12 page 58 11. How does accounting information reduce agency problems in relationships between management and debt holders?arrow_forwardQ39 Statement I: The objective of financial reporting is to provide insider information about the reporting entity. Statement II: The insider information provided about the reporting entity is useful only to international investors and lenders in making decisions about providing resources to the entity. a. Neither statement I is true nor statement II is true b. Only statement I is true c. Only statement II is true d. Statement I only false but statement II is truearrow_forward

- Q14 An audit of the financial statements of a company is referred to as a(n) a. Financial audit. b. Compliance audit. c. Operational audit. d. Integrated financial auditarrow_forwardQuestion 2 Make a critical assessment of the International Accounting Standard Board’s (ASB) Conceptual framework 2018. Discuss the key elements of the conceptual framework and their role in enhancing the relevance and reliability of financial reporting.arrow_forward4024 2023 2022 2021 2020 2019 2019 2017 Applications Rapidldentity X Principles of Accounting I- AC X O Question 1- Chapter 9 Quiz: A x ezto.mheducation.com/ext/map/index.html?_con=con&external_browser3D0&launchUrl=https%253A%252F%252 counting for Current Liabi... Saved Help Save & Exit Check Required information Liabilities are probable future payments of assets or services that past transactions or events obligate an entity to make. Current liabilities are due within one year or the operating cycle, whichever is longer. All other liabilities are long term. Balance Sheet January 31 508 II F3 F4 F5 F6 F8 F10 Finder F7 F11 F12 DDI 114 %24arrow_forward

Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning