Corporate Finance

12th Edition

ISBN: 9781259918940

Author: Ross, Stephen A.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 20, Problem 10CQ

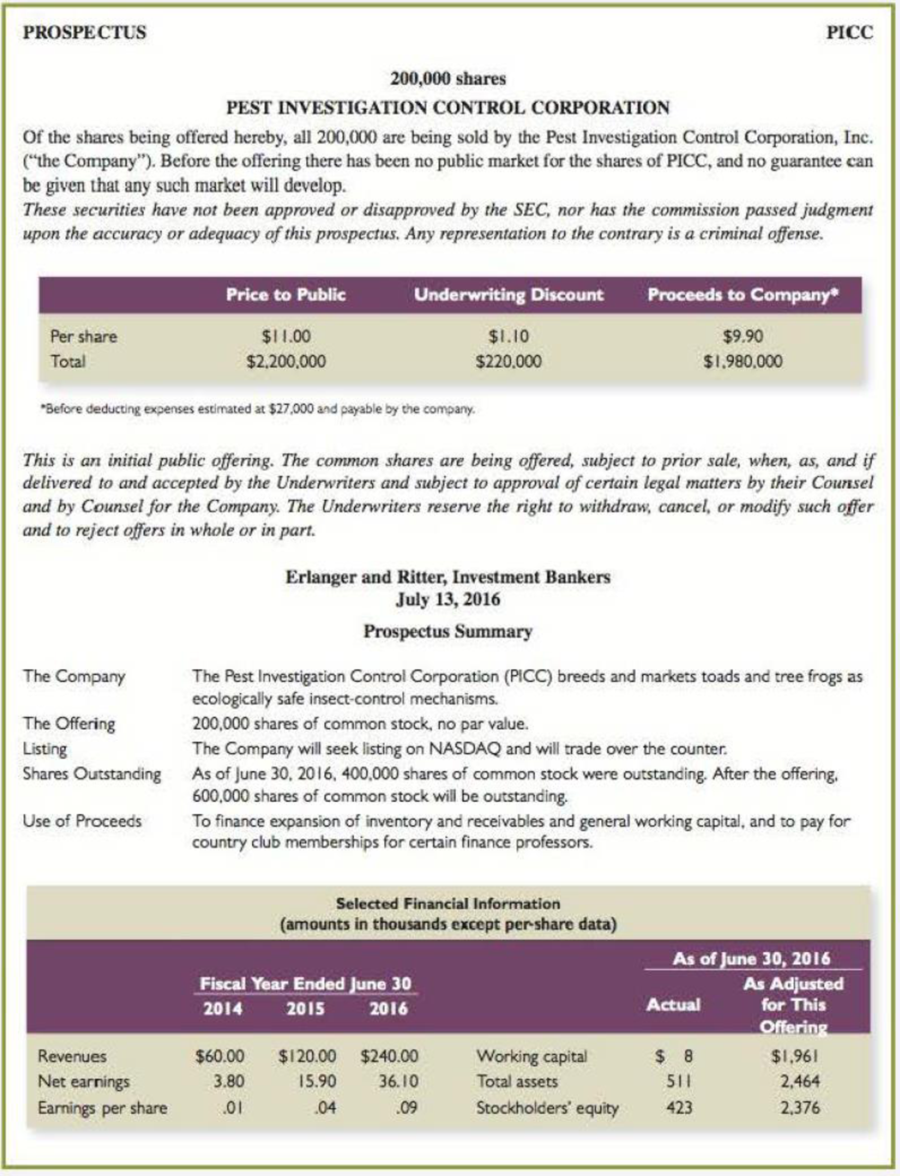

IPO Pricing The following material represents the cover page and summary of the prospectus for the initial public offering of the Pest Investigation Control Corporation (PICC), which is going public tomorrow with a firm commitment initial public offering managed by the investment banking firm of Erlanger and Ritter.

Answer the following questions:

- a. Assume that you know nothing about PICC other than the information contained in the prospectus. Based on your knowledge of finance, what is your prediction for the price of PICC tomorrow? Provide a short explanation of why you think this will occur.

- b. Assume that you have several thousand dollars to invest. When you get home from class tonight, you find that your stockbroker, whom you have not talked to for weeks, has called. She has left a message that PICC is going public tomorrow and that she can get you several hundred shares at the offering price if you call her back first thing in the morning. Discuss the merits of this opportunity.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Here is some price information on FinCorp stock. Suppose that FinCorp trades in a dealer market.Bid =55.25

Ask= 55.50a. Suppose you have submitted an order to your broker to buy at market. At what price will your trade be executed?b. Suppose you have submitted an order to sell at market. At what price will your trade be executed?c. Suppose you have submitted a limit order to sell at $55.62. What will happen?d. Suppose you have submitted a limit order to buy at $55.37. What will happen?

a) You observe the following quotes for the USD/AUD in the spot market from two banks:

Bank of Sydney

Bank of New York

Bid

Ask

Bid

Ask

0.71711

0.71715

0.71708

0.71715

Do these quotes imply the possibility of earning a profit by using locational arbitrage? If so, calculate the potential profit if you are able to use AUD 25,000. If not, explain why arbitrage is not possible?

(b) You observe the following quotes for the GBP /AUD in the spot market from two banks:

Bank of Melbourne

Bank of London

Bid

Ask

Bid

Ask

0.5458

0.5459

0.5514

0.5515

Do these quotes imply the possibility of earning a profit by using locational arbitrage? If so, calculate the potential profit if you are able to use GBP 50,000. If not, explain why arbitrage is not possible?

c) You observe the following quotes for the EUR / USD in the spot market from two banks:

Deutsche Bank

Bank of America

Bid

Ask

Bid

Ask

1.18102

1.18102

1.18094

1.18100

Do these quotes imply the…

Here is some price information on Fincorp stock. Suppose that Fincorp trades in a dealer market. Bid Ask 36.33 36.68 Required: Suppose you have submitted an order to your broker to buy at market. At what price will your trade be executed? Suppose you have submitted an order to sell at market. At what price will your trade be executed? Suppose you have submitted a limit order to sell at $36.76.What will happen? Suppose you have submitted a limit order to buy at $36.61. What will happen?

Chapter 20 Solutions

Corporate Finance

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Using Past Information to Estimate Required Returns Use online resources to work on this chapter's questions. Please note that website information changes over time, and these changes may limit your ability to answer some of these questions. Chapter 8 discussed the basic trade-off between risk and return. In the capital asset pricing model (CAPM) discussion, beta was identified as the correct measure of risk for diversified shareholders. Recall that beta measures the extent to which the returns of a given stock move with the stock market. When using the CAPM to estimate required returns, we would like to know how the stock will move with the market in the future, but because we dont have a crystal ball, we generally use historical data to estimate this relationship with beta. As mentioned in Web Appendix 8A, beta can be estimated by regressing the individual stock's returns against the returns of the overall market. As an alternative to running our own regressions, we can rely on reported betas from a variety of sources. These published sources make it easy for us to readily obtain beta estimates for most large publicly traded corporations. However, a word of caution is in order. Beta estimates can often be quite sensitive to the time period in which the data are estimated, the market index used, and the frequency of the data used. Therefore, it is not uncommon to find a wide range of beta estimates among the various Internet websites. 4. Select one of the four stocks listed in question 3 by entering the company's ticker symbol on the financial website you have chosen. On the screen you should see the interactive chart. Select the six-month time period and compare the stock's performance to the SP 500's performance on the graph by adding the SP 500 to the interactive chart. Has the stock outperformed or underperformed the overall market during this time period?arrow_forwardSuppose you are a seller . At time t = 0 you get £C from the buyer where C is the risk-neutral price of the option. You then have to design a hedging strategy which would allow you to meet your financial obligation in one year’s time. Your portfolio should consist of two investments: you are allowed to buy the underlying shares and to deposit money in the bank. The price of the share evolves according to a geometric Brownian motion. State the formulae you will need to compute the number of shares in the portfolio and the capital deposited in the bank at any time t, 0 ≤ t ≤ 1.arrow_forwarda) What is the similarity between the internal rate of return of a project and the yield-to-maturity of a bond? b) "If a stock had high returns so far, it will have low returns in the future". Discuss whether this statement is true or false, based on the knowledge of the different theories and models out there. c) A salt sprinkler manufacturer considers making an investment in a ball-point pen factory. Explain how you would evaluate this investment project and discuss the appropriate discount rate to use. d) Explain how you could earn a positive return by following a momentum strategy.arrow_forward

- You observe the following quotes for the USD/AUD in the spot market from two banks:Bank of Sydney /Bank of New YorkBid Ask/ Bid Ask0.71711 0.71715 /0.71708 0.71715Do these quotes imply the possibility of earning a profit by using locational arbitrage? If so, calculatethe potential profit if you are able to use AUD 25,000. If not, explain why arbitrage is not possible?(b) You observe the following quotes for the GBP /AUD in the spot market from two banks:Bank of Melbourne/ Bank of LondonBid Ask/ Bid Ask0.5458 0.5459 /0.5514 0.5515Do these quotes imply the possibility of earning a profit by using locational arbitrage? If so, calculatethe potential profit if you are able to use GBP 50,000. If not, explain why arbitrage is not possible?c) You observe the following quotes for the EUR / USD in the spot market from two banks:Deutsche Bank/ Bank of AmericaBid Ask /Bid Ask1.18102 1.18102 /1.18094 1.18100Do these quotes imply the possibility of earning a profit by using locational arbitrage? If…arrow_forward2. Based on your readings, summarize the key features of the markets with the guide questions below. Features Equity Market Fixed-Income Market Types of Securities Traded Accessibility of the Market Levels of Risk Expected Returns Goals of Investors Strategies Used by Market Participants Example marketsarrow_forwardAnswer the next 4 questions using the information in the following table. You are considering the purchase of a $1,000 par value Treasury Bill and observe the following quotes for T-Bills in the market: Ignore transaction costs. Time to Maturity (days) Bid Asked % % 60 1.64 1.55 88 1.63 1.54 116 1.62 1.53 144 1.61 1.52 4. The bid price of a T-bill in the secondary market is A. the price at which the dealer in T-bills is willing to sell the bill. B. the price at which the investor in T-bills is willing to sell the bill. C. larger than the ask price of the T-bill. D. The price at which the investor can buy the T-bill. 5. What is the purchase price of the 144-day bill that you face? А. $993.29 B. $993.56 С. $993.92 D. $994.05arrow_forward

- You have been asked to assess the impact of a proposed acquisition on the beta of a firm and have been provided the following information on the two firms involved in the deal: The risk-free rate is 4% and the equity risk premium is 6%. Now assume that Acquirer plans to retire all of Target’s debt and that it will be able to buy Target’s equity at the current market price. If Acquirer would like to have a levered beta of 1.35 for the combined firm after the transaction, estimate how much new debt it will need to raise to finish this acquisition.arrow_forwardNingbo Industrial Concepts Incorporated Initial stock price $115.00 Exercise price $115.00 Call price $4.75 Put Price $4.50 Required: Using the information in the table above, please calculate dollar value of the following option strategies. Use this calculated dollar value to determine the profit of each strategy at various stock prices. (Use cells A3 to B6 from the given information to complete this question. Negative answer should be input and displayed as a negative value. All other answers should be input and displayed as positive values.) Ningbo Industrial Concepts Incorporated Dollar Value of Strategy as a Function of Current Stock Price Strategy $95.00 $105.00 $115.00 $125.00 $135.00 Straddle Strip Strap Ningbo Industrial Concepts Incorporated Rate of Return…arrow_forward(a) Financial engineering deals with the design of new assets. Draw the payoff (at t=1) of the following bull butterfly spread: Purchase 1 call with exercise price a Sell 2 calls with exercise price (atb)/2 Purchase 1 call with exercise price b as a function of the underlying stock price S at t=1 where a=120and b=140. (b) An individual agent thinks that there is a high probability that the Dow Jones will have a payoff (or points) between a=32,000 and b=36,000 at t=1. Design a digital option (see Figure 1) as a sequence of calls on the Dow that converges to a pure bet on getting $1 on the interval [32,000, 36,000], i.e. if the Dow lies between Se[32,000, 36,000] at t=1, then the portfolio of calls pays off exactly $1. The payoff is O otherwise. Figure I (Digital option) payoff a-32,000 b-36,000 Hint: You have to modify the sell strategies of a bull butterfly spread to obtain a payoff as given in Figure 2 and then adjust n and õ appropriately. Figure 2 payoff of portfolio 1-nő a b-8arrow_forward

- You are going to a job interview for an entry-level financial analyst position at New Great City Financial Co. You are confident about your financial skills but want to prepare more for this important job interview. However, since the position involves a good understanding of bond valuation and yields, you have gathered the following possible questions to prepare for the interview: What is interest rate risk? What's the difference between bond's promised yield and its realized yield? Which one is more relevant? How do you value a bond? Explain in detail.arrow_forward4. Introduction to real options Consider the following statement about real options: Decision tree analysis is more commonly used in valuing securities than real assets. True or False: The preceding statement is correct. True False Which type of real option allows a project to be expanded if demand turns out to be greater than expected? Flexibility option Abandonment option Expansion option Timing option Consider the following example: Smoltz Motors has plants around the country that specialize in specific models of cars. Smoltz has determined that lower demand has led the firm’s inventory of SUVs to be too high. Smoltz wants to stop production for its SUVs and focus on its sedans. This example describes a real option to (expand/ abandon) . Please do not answer in excel, use math formulas Thank you!arrow_forwardOptions2. Construct profit diagrams at expiration time to show what position in META puts, calls and/or underlying stock best expresses the investor’s objectives described below. META currently sells for $210 so that profit diagrams between $150 and $250 in $10 increments are appropriate. Assume that at-the-money puts and calls currently cost$30 each. The call with strike $190 costs $40 and the call with strike $230 costs $20. (a) An investor wants to benefit from META price drops but does not want to lose more than $30 on the investment. (b) An investor wants to have a positive payoff if the upcoming META earnings announcement is close to market expectations—meaning that the price will not move by more than $20 dollars.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781285867977Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781285867977Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781285867977

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Financial instruments products; Author: fi-compass;https://www.youtube.com/watch?v=gvxozM3TUIg;License: Standard Youtube License