Concept explainers

Videos

Karen Johnson, CFO for Raucous Roasters (RR), a specialty coffee manufacturer, is rethinking her company’s working capital policy in light of a recent scare she faced when RR’s corporate banker, citing a nationwide credit crunch, balked at renewing RR’s line of credit. Had the line of credit not been renewed, RR would not have been able to make payroll, potentially forcing the company out of business. Although the line of credit was ultimately renewed, the scare has forced Johnson to examine carefully each component of RR’s working capital to make sure it is needed, with the goal of determining whether the line of credit can be eliminated entirely. In addition to (possibly) freeing RR from the need for a line of credit, Johnson is well aware that reducing working capital will improve

Historically, RR has done little to examine working capital, mainly because of poor communication among business functions. In the past, the production manager resisted Johnson’s efforts to question his holdings of raw materials, the marketing manager resisted questions about finished goods, the sales staff resisted questions about credit policy (which affects accounts receivable), and the treasurer did not want to talk about the cash and securities balances. However, with the recent credit scare, this resistance has become unacceptable and Johnson has undertaken a company-wide examination of cash, marketable securities, inventory, and accounts receivable levels.

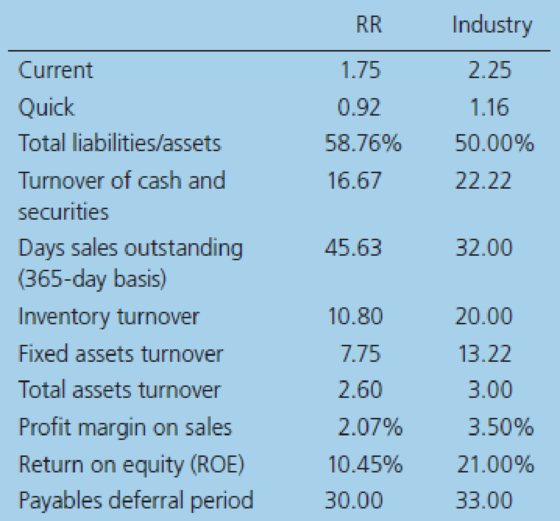

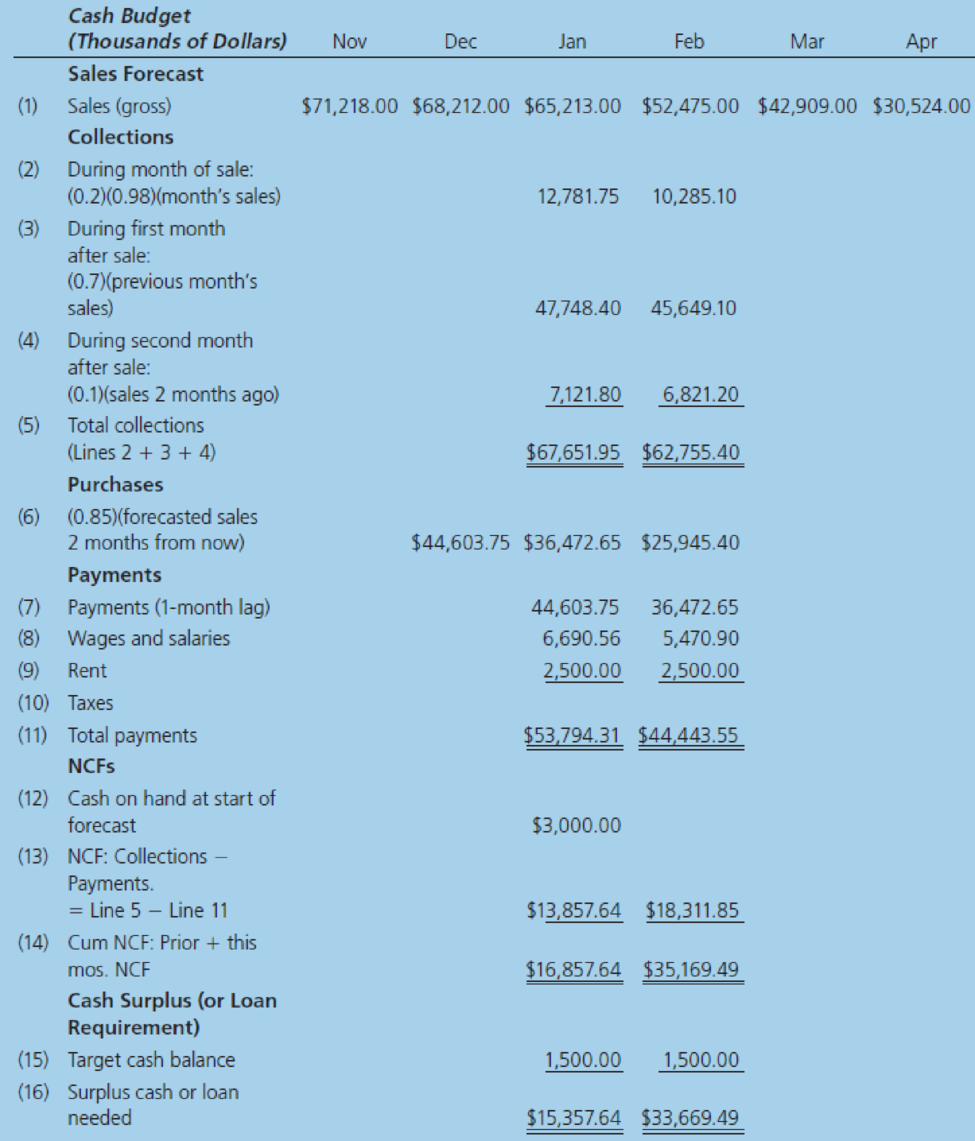

Johnson also knows that decisions about working capital cannot be made in a vacuum. For example, if inventories could be lowered without adversely affecting operations, then less capital would be required, and free cash flow would increase. However, lower raw materials inventories might lead to production slowdowns and higher costs, and lower finished goods inventories might lead to stockouts and loss of sales. So, before inventories are changed, it will be necessary to study operating as well as financial effects. The situation is the same with regard to cash and receivables. Johnson has begun her investigation by collecting the ratios shown here. (The partial cash budget shown after the ratios is used later in this mini case.)

Johnson plans to use the preceding ratios as the starting point for discussions with RR’s operating team. Based on the data, does RR seem to be following a relaxed, moderate, or restricted current asset usage policy?

Trending nowThis is a popular solution!

Chapter 21 Solutions

INTERMEDIATE FINAN...-MINDTAP(1 TERM)

- Karen Johnson, CFO for Raucous Roasters (RR), a specialty coffee manufacturer, is rethinking her company’s working capital policy considering a recent scare she faced when RR’s corporate banker, citing a nationwide credit crunch, balked at renewing RR’s line of credit. Had the line of credit not been renewed, RR would not have been able to make payroll, potentially forcing the company out of business. Although the line of credit was ultimately renewed, the scare has forced Johnson to examine carefully each component of RR’s working capital to make sure it is needed, with the goal of determining whether the line of credit can be eliminated entirely. In addition to (possibly) freeing RR from the need for a line of credit, Johnson is well aware that reducing working capital can also add value to a company by improving its EVA (Economic Value Added). In her corporate finance course Johnson learned that EVA is calculated by taking net operating profit after taxes (NOPAT) and then…arrow_forwardOtis is the CEO of Bay Corp. The company has been struggling for the last few years and is in danger of defaulting on several of its bank loan covenants. Otis is facing significant pressure from the board of directors to turn the company around. Unless he meets all of the financial goals for the year, he will be out the door without a golden parachute. To improve the financial appearance of the company, Otis undertakes a scheme to boost the balance sheet by faking inventory. The analysis of what financial ratio would most likely bring this scheme to light? Inventory turnover Quick ratio Collection ratio Profit marginarrow_forwardDavid Lyons, CEO of Lyons Solar Technologies, is concerned about his firms level of debt financing. The company uses short-term debt to finance its temporary working capital needs, but it does not use any permanent (long-term) debt. Other solar technology companies have debt, and Mr. Lyons wonders why they use debt and what its effects are on stock prices. To gain some insights into the matter, he poses the following questions to you, his recently hired assistant: Now assume that Firms L and U are both subject to a 25% corporate tax rate. Using the data given in part b, repeat the analysis called for in parts b(1) and b(2) using assumptions from the MM model with taxes.arrow_forward

- Penco Ltd’s board of directors are looking into expanding the company’s business operations. Before investing in a new product, the board conducted one focus group, and based on this one bit of feedback, invested $5m of company funds to develop the product. Within two years, the company had lost $8m due to poor sales. Shareholders are furious and wish to hold directors personally liable for this loss. Analyse the likely outcome for directors if shareholders were to accuse the board of breaching CA s 180.arrow_forwardReed Kohler is in his final year of employment as controller for Quality Sales Corporation: he hopes to retire next year. As a member of top management, Kohler participates in an attractive company bonus plan. The overall size of the bonus is a function of the firm's net income before bonus and income taxes - the larger the net income, the larger the bonus. Due to a slowdown in the economy due to Coronavirus, the company has encountered difficulty in managing its cash flow. The company auditors have recommended that the company change its inventory method from FIFO to LIFO . The change would cause a significant increase in the cost of goods sold for the year. Kohler thinks the company shouldn't switch to LIFO b/c its inventory quantities are too large. After expressing this opinion to the firm's treasurer, Kohler is stunned at the treasurer's reply "Reed, I can't believe that after all these years with the company, you put your personal interests ahead of the companies…arrow_forwardJerry Prior, Beeler Corporation’s controller, is concerned that net income may be lower this year. He is afraid upper-level management might recommend cost reductions by laying off accounting staff, including him. Prior knows that depreciation is a major expense for Beeler. The company currently uses the double-declining-balance method for both financial reporting and tax purposes, and he’s thinking of selling equipment that, given its age, is primarily used when there are periodic spikes in demand. The equipment has a carrying value of $2,000,000 and a fair value of $2,180,000. The gain on the sale would be reported in the income statement. He doesn’t want to highlight this method of increasing income. He thinks, “Why don’t I increase the estimated useful lives and the salvage values? That will decrease depreciation expense and require less extensive disclosure, since the changes are accounted for prospectively. I may be able to save my job and those of my staff.” Instructions Answer…arrow_forward

- "We must get it," Erickson Santos, president of Industrial Fasteners, roared. "Without it, we're in big trouble." The "it" Mr. Santos referred to is the renewal of a $20 million loan with Manila First Bank. The big trouble he fears is the lack of funds necessary to repay the existing debt and few, if any, prospects for raising the funds elsewhere. Mr. Santos had just hung up the phone after a conversation with a bank vice-president in which it was made clear that this year's statement of cash flows must look better than last year's. Mr. Santos knows that improvements are not on course to happen. In fact, cash flow projections were dismal. Later that day, Timothy Dela Cruz, assistant controller, was summoned to Mr. Santos's office. "Dela Cruz," Santos barked, "I've looked at our accounts receivable. I think we can generate quite a bit of cash by selling or factoring most of those receivables. I know it will cost us more than if we collect them ourselves, but it sure will make our cash…arrow_forwardDavid Lyons, CEO of Lyons Solar Technologies, is concerned about his firm’s level of debt financing. The company uses short-term debt to finance its temporary working capital needs, but it does not use any permanent (long-term) debt. Other solar technology companies have debt, and Mr. Lyons wonders why they use debt and what its effects are on stock prices. To gain some insights into the matter, he poses the following questions to you, his recently hired assistant: Who were Modigliani and Miller (MM), and what assumptions are embedded in the MM and Miller models?arrow_forwardJennifer Dawes is a young, vibrant entrepreneur whose business venture, Jennifer Limited, hasrapidly expanded as she developed new product lines and gained new customers. She has found,however, that even though her last financial statements have shown healthy profits, she sometimes has difficulty meeting in a timely manner, suppliers’ and utility bills and the payroll of employees. Miss Dawes has been further alarmed upon being informed that many businesses which appeared profitable have still gone into insolvency. A. Advise Jennifer on the role of working capital management in a business. B. Describe, for her, TWO (2) consequences of poor working capital management. Extracts from Annual Accounts of Jennifer Limited $Inventories: Raw materials 108 000Work in progress 75 600Finished goods 86 400Purchases of raw materials 518 400Cost of production 675 000Cost of goods sold 756 000Sales 864 000Accounts receivables 172 800Accounts payables 86 400C. Calculate the length of the working…arrow_forward

- II. Jerry Prior, Beeler Corporation’s controller, is concerned that net income may be lower this year. He is afraid upper-level management might recommend cost reductions by laying off accounting staff including him. Prior knows that depreciation is a major expense for Beeler. The company currently uses the double-declining-balance method for both financial reporting and tax purposes, and he’s thinking of selling equipment that, given its age, is primarily used when there are periodic spikes in demand. The equipment has a carrying value of $2,000,000 and a fair value of $2,180,000. The gain on the sale would be reported in the income statement. He doesn’t want to highlight this method of increasing income. He thinks, “Why don’t I increase the estimated useful lives and the salvage values? That will decrease depreciation expense and require less extensive disclosure, since the changes are accounted for prospectively. I may be able to save my job and those of my staff.” Instructions…arrow_forwardSal Shirey is an owner of a small business. His company has recently borrowed a large amount of funds to finance the construction of a large building addition, as well as, the purchase of equipment and machinery. Shirey's banker requires him to submit quarterly financial statements so that he can monitor the financial health of his business. The bank has warned that if profit margins decline, the interest rate on the loan may need to be increased in order to reflect additional risk. Shirey knows that profit may decline this year. As he is preparing the year-end adjusting entries, Sal decides, for depreciation purposes, to treat all long-term asset purchases as though they occurr on the first day of the month following the month of purchase. 1. Is there an ethical issue with the implementation of this rule? If so, what is it?2. When should depreciation first be recorded?3. What impact will Shirey's approach to recording depreciation have on the financial statements?arrow_forwardCaplan Pharma, Inc., recently was sued by a competitor for possible infringement of the competitor’s patent on a top-selling flu vaccine. The plaintiff is suing for damages of $15 million. Caplan's CFO has discussed the case with legal counsel, who believes it is possible that Caplan will not be able to successfully defend the lawsuit. The CFO knows that current U.S. accounting guidelines require that come gencies (such as lawsuits) must be disclosed in the annual report when a loss is possible. However, she is unsure whether this rule must be applied in the preparation of interim financial statements. She also knows that disclosure is necessary only if the amount is material, but she is unsure whether materiality should be assessed in relation to results for the interim period or for the entire year. Required Search current U.S. accounting standards to determine whether contingencies are required to be disclosed in interim reports, and, if so, how materiality is to be determined.…arrow_forward

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning