Videos

Binomial model* Over the coming year, Ragwort’s stock price will halve to $50 from its current level of $100 or it will rise to $200. The one-year interest rate is 10%.

- a. What is the delta of a one-year call option on Ragwort stock with an exercise price of $100?

- b. Use the replicating-portfolio method to value this call.

- c. In a risk-neutral world, what is the probability that Ragwort stock will rise in price?

- d. Use the risk-neutral method to check your valuation of the Ragwort option.

- e. If someone told you that in reality there is a 60% chance that Ragwort’s stock price will rise to $200, would you change your view about the value of the option? Explain.

a.

To compute: The delta of one year call option on R stock with a strike price of $100.

Explanation of Solution

The formula to calculate delta is:

The calculation of delta is as follows:

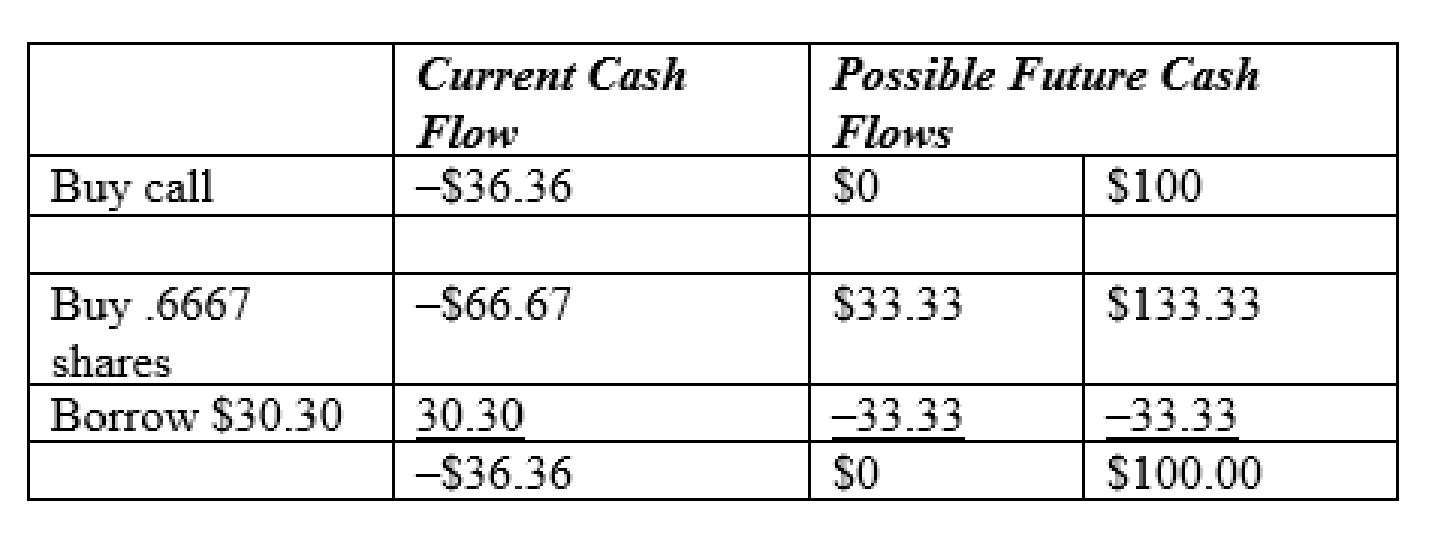

b.

To discuss: Apply the replicating portfolio technique to value this call.

Explanation of Solution

The replicating portfolio technique of valuing call is as follows.

c.

To discuss: The probability of increasing stock R price in a risk neutral world.

Explanation of Solution

The probability of increasing stock R calculated as follows:

The computation as follows:

Foot note: The probability is calculated on the basis of expected return.

d.

To compute: The value of stock R using the risk neutral method.

Explanation of Solution

The option value is calculated using the following formula:

Hence, the value of call is $36.36

e.

To discuss: Whether person X change his option regarding the value of option.

Explanation of Solution

Person X does not change his opinion regarding the value of option. The chance of price increase is most likely higher than the risk- neutral probability, but it does not aid to value the option.

Want to see more full solutions like this?

Chapter 21 Solutions

RU-N PRINCIPLE OF CORPORATE FINANCE & C

Additional Business Textbook Solutions

Corporate Finance (4th Edition) (Pearson Series in Finance) - Standalone book

Corporate Finance

Foundations Of Finance

Foundations of Finance (9th Edition) (Pearson Series in Finance)

Corporate Finance (The Mcgraw-hill/Irwin Series in Finance, Insurance, and Real Estate)

Gitman: Principl Manageri Finance_15 (15th Edition) (What's New in Finance)

- What makes for a good investment? Use the approximate yield formula or a financial calculator to rank the following investments according to their expected returns. Buy a stock for $30 a share, hold it for three years, and then sell it for $60 a share (the stock pays annual dividends of $2 a share). Buy a security for $40, hold it for two years, and then sell it for $100 (current income on this security is zero). Buy a one-year, 5 percent note for $1,000 (assume that the note has a $1,000 par value and that it will be held to maturity).arrow_forwardPut–Call Parity The current price of a stock is $33, and the annual risk-free rate is 6%. A call option with a strike price of $32 and with 1 year until expiration has a current value of $6.56. What is the value of a put option written on the stock with the same exercise price and expiration date as the call option?arrow_forwardConstant Growth Valuation Crisp Cookwares common stock is expected to pay a dividend of 3 a share at the end of this year (D1 = 3.00); its beta is 0.8. The risk-free rate is 5.2%, and the market risk premium is 6%. The dividend is expected to grow at some constant rate g, and the stock currently sells for 40 a share. Assuming the market is in equilibrium, what does the market believe will be the stocks price at the end of 3 years (i.e., what is P3)?arrow_forward

- Crisp Cookware’s common stock is expected to pay a dividend of $3 a share at the end of this year (D1 = $3.00); its beta is 0.8. The risk-free rate is 5.2%, and the market risk premium is 6%. The dividend is expected to grow at some constant rate g, and the stock currently sells for $40 a share. Assuming the market is in equilibrium, what does the market believe will be the stock’s price at the end of 3 years (i.e., what is )?arrow_forwardAssume that you’ve just inherited $500,000 and have decided to invest a big chunk of it ($350,000, to be exact) in common stocks. Your objective is to build up as much capital as you can over the next 15 to 20 years, and you’re willing to tolerate a “good deal’’ of risk. What types of stocks (blue chips, income stocks, and so on) do you think you’d be most interested in, and why? Select at least three types of stocks and briefly explain the rationale for selecting each. Would your selections change if you were dealing with a smaller amount of money—say, only $50,000? What if you were a more risk-averse investor?arrow_forwardCalculation of gL and EPS Spencer Suppliess stock is currently selling for 60 a share. The firm is expected to earn 5.40 per share this year and to pay a year-end dividend of 3.60. a. If investors require a 9% return, what rate of growth must be expected for Spencer? b. If Spencer reinvests earnings in projects with average returns equal to the stocks expected rate of return, then what will be next years EPS? [Hint: gL = ROE Retention ratio.)arrow_forward

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Pfin (with Mindtap, 1 Term Printed Access Card) (...FinanceISBN:9780357033609Author:Randall Billingsley, Lawrence J. Gitman, Michael D. JoehnkPublisher:Cengage Learning

Pfin (with Mindtap, 1 Term Printed Access Card) (...FinanceISBN:9780357033609Author:Randall Billingsley, Lawrence J. Gitman, Michael D. JoehnkPublisher:Cengage Learning Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781285065137Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781285065137Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning