Concept explainers

Videos

Equity as an Option and

- a. What is the current market value of the company’s equity?

- b. What is the current market value of the company’s debt?

- c. What is the company's continuously compounded cost of debt?

- d. The company has a new project available. The project has an NPV of $1,200,000. If the company undertakes the project, what will be the new market value of equity? Assume volatility is unchanged.

- e. Assuming the company undertakes the new project and does not borrow any additional funds, what is the new continuously compounded cost of debt? What is happening here?

a.

To compute: Current market value of the company’s equity.

Option Pricing:

Option pricing helps in determining the correct or fair price in the market. It is the value of one share on the basis of which option is traded. Black-Scholes is one of the pricing methods. Further, equity is also used as an option.

Explanation of Solution

Given,

Stock price is $9,050,000.

Exercise price is $10,000,000.

Risk free rate is 0.06.

Time to expire is 10.

Formula to calculate the value of equity by using Black Scholes model is,

Where,

- S is stock price.

- E is exercise price.

- R is risk free rate.

- T is time to expire.

Substitute $9,050,000 for S, $10,000,000 for E, 0.06for R, and 10for T.

Working Note:

Calculation of

Calculation of

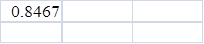

Hence, current market value of the company’s equity is $5,377,390.16.

b.

To compute: Current market value of the company’s debt.

Explanation of Solution

Given,

Value of company is $9,050,000.

Value of equity is $5,377,390.16.

Formula to calculate the value of debt is,

Substitute $9,050,000 as value of company and $5,377,390.16as value of equity.

Hence, current market value of company’s debt is $3,672,609.84.

c.

To compute: Company’s continuously compounded cost of debt.

Explanation of Solution

Given,

Value of debt is $3,672,609.84.

Face value is $10,000,000.

Time to expire is 10 years.

Formula to calculate the firm’s continuously cost of debt is,

Where,

- R is firm’s continuously cost of debt.

- t is maturity time.

Substitute $3,672,609.84as value of debt, $10,000,000 as face value and 10 for t.

Simplify the above equation.

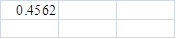

Hence, the company’s continuously cost of debt is 10.02%.

d.

To compute: New market value of equity.

Explanation of Solution

Given,

Exercise price is 10,000,000.

Risk free rate is 0.06.

Time to expire is 10 years.

Calculated stock price:

The stock price is $10,250,000.

Formula to calculate the value of equity by using Black Scholes model is,

Where,

- S is stock price.

- E is exercise price.

- R is risk free rate.

- T is time to expire.

Substitute $10,250,000for S, 10,000,000 for E, 0.06 for R, and 10 for T.

Working Note:

Calculation of

Calculation of

Calculate the revised stock price,

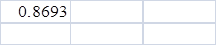

Hence, new market value of equity is $6,406,471.3.

e.

To compute: The new continuously compounded cost of debt.

Explanation of Solution

Given,

Value of company is $9,050,000.

Value of equity is $6,406,471.3.

Time to expire is 10 years.

Calculated value:

Value of equity is $6,406,471.3.

Value of the stock is $10,250,000.

Formula to calculate the value of debt is,

Substitute $10,250,000as value of company and $6,406,471.3 as value of equity.

Formula to calculate the new continuously cost of debt is,

Where,

- R is firm’s continuously cost of debt.

- t is maturity time.

Substitute $3,843,528.7 as value of debt, $10,000,000 as face value and 10 for t.

Simplify the above equation.

Hence, the company’s new continuously cost of debt is 9.56%.

Want to see more full solutions like this?

Chapter 22 Solutions

CONNECT 1 SEMESTER ACCESS CARD FOR CORPORATE FINANCE

- Crisp Cookware’s common stock is expected to pay a dividend of $3 a share at the end of this year (D1 = $3.00); its beta is 0.8. The risk-free rate is 5.2%, and the market risk premium is 6%. The dividend is expected to grow at some constant rate g, and the stock currently sells for $40 a share. Assuming the market is in equilibrium, what does the market believe will be the stock’s price at the end of 3 years (i.e., what is )?arrow_forwardWACC Estimation On January 1, the total market value of the Tysseland Company was $60 million. During the year, the company plans to raise and invest $30 million in new projects. The firm’s present market value capital structure, shown here, is considered to be optimal. There is no short-term debt. New bonds will have an 8% coupon rate, and they will be sold at par. Common stock is currently selling at $30 a share. The stockholders’ required rate of return is estimated to be 12%, consisting of a dividend yield of 4% and an expected constant growth rate of 8%. (The next expected dividend is $1.20, so the dividend yield is $1.20/$30 = 4%.) The marginal tax rate is 40%. In order to maintain the present capital structure, how much of the new investment must be financed by common equity? Assuming there is sufficient cash flow for Tysseland to maintain its target capital structure without issuing additional shares of equity, what is its WACC? Suppose now that there is not enough internal cash flow and the firm must issue new shares of stock. Qualitatively speaking, what will happen to the WACC? No numbers are required to answer this question.arrow_forwardCalculation of gL and EPS Spencer Suppliess stock is currently selling for 60 a share. The firm is expected to earn 5.40 per share this year and to pay a year-end dividend of 3.60. a. If investors require a 9% return, what rate of growth must be expected for Spencer? b. If Spencer reinvests earnings in projects with average returns equal to the stocks expected rate of return, then what will be next years EPS? [Hint: gL = ROE Retention ratio.)arrow_forward

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning