EBK CORPORATE FINANCE

11th Edition

ISBN: 8220102798878

Author: Ross

Publisher: YUZU

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 22, Problem 2QP

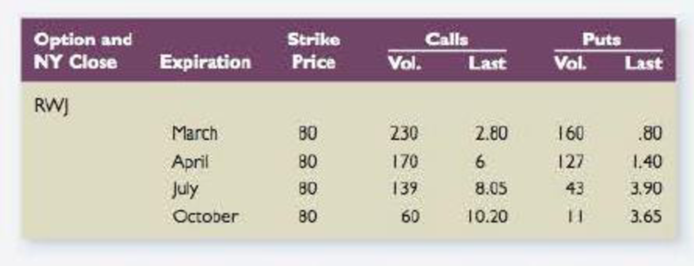

Understanding Option Quotes Use the option quote information shown here to answer the questions that follow. The stock is currently selling for $83.

- a. Are the call options in the money? What is the intrinsic value of an RWJ Corp. call option?

- b. Are the put options in the money? What is the intrinsic value of an RWJ Corp. put option?

- c. Two of the options are clearly mispriced. Which ones? At a minimum, what should the mispriced options sell for? Explain how you could profit from the mispricing in each case.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Both call and put options are affected by the following five factors: the exercise price, the underlying stock price, the time to expiration, the stock’s standard deviation, and the risk-free rate. However, the direction of the effects on call and put options could be different.

Use the following table to identify whether each statement describes put options or call options.

Statement

Put Option

Call Option

1. When the exercise price increases, option prices increase.

2. An option is more valuable the longer the maturity.

3. The effect of the time to maturity on the option prices is indeterminate.

4. As the risk-free rate increases, the value of the option increases.

Label the following for this diagram:

a. Name of options payoff

b. Identify whether positive or negative premium

c. Identify breakeven point

d. What is the profit or loss when stock price is S60 at maturity

e. Suppose you have this options position, should you exercise your right (if any) assuming that the stock price is $60 at maturity?

Option Payoffs and Profits Long put

$40

$20

$0

Option Payoff

Option Profit

Exerche Price

$20

S40

$20

$40

S60

$80.

Stock Price At Maturity

Payoff and Profit

Label the following for this diagram:

a. Name of options payoff

b. Identify whether positive or negative premium

c. Identify break-even point

d. What is the profit or loss when stock price is $60 at maturity

e. Suppose you have this options position, should you exercise your right (if any) assuming that the stock price is $60 at maturity?

Option Payoffs and Profits Long put

$40

$20

$0

Option Payoff

Option Profit

---- Exercise Price

-$20

-$40

$0

$20

$40

$60

$80

Stock Price At Maturity

Payoff and Profit

Chapter 22 Solutions

EBK CORPORATE FINANCE

Ch. 22 - Options What is a call option? A put option? Under...Ch. 22 - Options Complete the following sentence for each...Ch. 22 - American and European Options What is the...Ch. 22 - Intrinsic Value What is the intrinsic value of a...Ch. 22 - Option Pricing You notice that shares of stock in...Ch. 22 - Options and Stock Risk If the risk of a stock...Ch. 22 - Option Risk True or false: The unsystematic risk...Ch. 22 - Prob. 8CQCh. 22 - Option Price and Interest Rates Suppose the...Ch. 22 - Contingent Liabilities When you take out an...

Ch. 22 - Options and Expiration Dates What is the impact of...Ch. 22 - Options and Stock Price Volatility What is the...Ch. 22 - Insurance as an Option An insurance policy is...Ch. 22 - Equity as a Call Option It is said that the equity...Ch. 22 - Prob. 15CQCh. 22 - Put Call Parity You find a put and a call with the...Ch. 22 - Put- Call Parity A put and a call have the same...Ch. 22 - Put- Call Parity One thing put-call parity tells...Ch. 22 - Two-State Option Pricing Model T-bills currently...Ch. 22 - Understanding Option Quotes Use the option quote...Ch. 22 - Calculating Payoffs Use the option quote...Ch. 22 - Two-State Option Pricing Model The price of Ervin...Ch. 22 - Two-State Option Pricing Model The price of Tara,...Ch. 22 - Put-Call Parity A stock is currently selling for...Ch. 22 - Put-Call Parity A put option that expires in six...Ch. 22 - Put-Call Parity A put option and a call option...Ch. 22 - Pot-Call Parity A put option and a call option...Ch. 22 - Black-Scholes What are the prices of a call option...Ch. 22 - Black-Scholes What are the prices of a call option...Ch. 22 - Delta What are the deltas of a call option and a...Ch. 22 - Prob. 13QPCh. 22 - Prob. 14QPCh. 22 - Time Value of Options You are given the following...Ch. 22 - Prob. 16QPCh. 22 - Prob. 17QPCh. 22 - Prob. 18QPCh. 22 - Black-Scholes A call option has an exercise price...Ch. 22 - Black-Scholes A stock is currently priced at 35. A...Ch. 22 - Equity as an Option Sunburn Sunscreen has a zero...Ch. 22 - Equity as an Option and NPV Suppose the firm in...Ch. 22 - Equity as an Option Frostbite Thermalwear has a...Ch. 22 - Mergers and Equity as an Option Suppose Sunburn...Ch. 22 - Equity as an Option and NPV A company has a single...Ch. 22 - Two-State Option Pricing Model Ken is interested...Ch. 22 - Two-State Option Pricing Model Rob wishes to buy a...Ch. 22 - Two-State Option Pricing Model Maverick...Ch. 22 - Prob. 29QPCh. 22 - Prob. 30QPCh. 22 - Prob. 31QPCh. 22 - Two-State Option Pricing and Corporate Valuation...Ch. 22 - Black-Scholes and Dividends In addition to the...Ch. 22 - Prob. 34QPCh. 22 - Prob. 35QPCh. 22 - Prob. 36QPCh. 22 - Prob. 37QPCh. 22 - Prob. 38QPCh. 22 - Prob. 1MCCh. 22 - Prob. 2MCCh. 22 - Prob. 3MCCh. 22 - Prob. 4MCCh. 22 - Prob. 5MC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Assume that you have been given the following information on Purcell Corporations call options: According to the Black-Scholes option pricing model, what is the options value?arrow_forwardBlack-Scholes Model Assume that you have been given the following information on Purcell Industries call options: According to the Black-Scholes option pricing model, what is the option’s value?arrow_forwardLabel the following for this diagram: a. Name of options payoff b. Identify whether positive or negative premium c. Identify break-even point d. What is the profitt or loss when stock price is $60 at maturity e. If you have this option position, should you exercise your right (if any) assuming that the stock price is $60 at maturity? Option Payoffs and Profits $40 $20 $0 Option Payoff Option Profit --- Exercise Price -$20 -$40 $0 $20 $40 $60 $80 Stock Price At Maturity Payoff and Profitarrow_forward

- Label the following for this diagram: a. Name of options payoff b. Identify whether positive or negative premium c. Identify break-even point d. What is the profitt or loss when stock price is $60 at maturity e. Suppose you have this options position, should you exercise your right (if any) assuming that the stock price is $60 at maturity? Option Payoffs and Profits $40 Long call $20 $0 Option Payoff Option Profit ---- Exercise Price -$20 -$40 $0 $20 $40 $60 $80 Payoff and Profitarrow_forwardBoth call and put options are affected by the following five factors: the exercise price, the underlying stock price, the time to expiration, the stock’s standard deviation, and the risk-free rate. However, the direction of the effects on call and put options could be different. Use the following table to identify whether each statement describes put options or call options. Statement Put Option Call Option 1. An option is more valuable the longer the maturity. 2. A longer maturity in-the-money option on a risky stock is more valuable than the same shorter maturity option. 3. When the exercise price increases, option prices increase. 4. As the risk-free rate increases, the value of the option increases.arrow_forwardSuppose that call options on a stock with strike prices $100 and $106 cost $8 and $5, respectively. How can the options be (the profits from option positions and the total profit).arrow_forward

- You are given the following information on some company's stock, as well as the risk- free asset. Use it to calculate the price of the call option written on that stock, as well as the price of the put option. (HINT: You should use the Black-Scholes formula!) (Do not round intermediate calculations and round your final answers to 2 decimal places, e.g., 32.16.) Today's stock = $74 price Exercise price = $70 Risk-free rate = Option maturity = 4 months Standard deviation of annual stock returns 4.4% per year, compounded continuously Call price Put price = 62% per yeararrow_forwardDoes at the money ,in the money, out of the money is used to tell about position of strike price in the market when buy or sell the option only (judge by comparing srike price and the spot price in market at that moment,Is it used to tell status of the option on expiration date by comparing srike price and the market price at expiration date or not, if not please explain to me by using some example to explain it.arrow_forwardYou are given the following information on some company's stock, as well as the risk- free asset. Use it to calculate the price of the call option written on that stock, as well as the price of the put option. (HINT: You should use the Black-Scholes formula!) (Do not round intermediate calculations and round your final answers to 2 decimal places, e.g., 32.16.) Today's stock = $86 price Exercise price = $85 Risk-free rate = Option maturity = 4 months Standard deviation of 5% per year, compounded continuously annual stock returns = 62% per yeararrow_forward

- You are given the following information on some company's stock, as well as the risk- free asset. Use it to calculate the price of the call option written on that stock, as well as the price of the put option. (HINT: You should use the Black-Scholes formula!) (Do not round intermediate calculations and round your final answers to 2 decimal places, e.g., 32.16.) Today's stock $72 price Exercise price = $70 Risk-free rate = deviation of Option maturity = 4 months Standard annual stock returns = Call price Put price 4.3% per year, compounded continuously = 61% per yeararrow_forwardWhich of the following is not a determinant of the value of a call option in the Black-Scholes model? A. The interest rate. B. The exercise price of the stock. C. The price of the underlying stock. D. The beta of the underlying stock. Need typed answer only.Please give answer within 45 minutesarrow_forwardMichael Weber, CFA, is analyzing several aspects of option valuation, including the determinants of the value of an option, the characteristics of various models used to value options, and the potential for divergence of calculated option values from observed market prices.a. What is the expected effect on the value of a call option on common stock if the volatility of the underlying stock price decreases? If the time to expiration of the option increases?b. Using the Black-Scholes option-pricing model and an estimate of stock return volatility, Weber calculates the price of a 3-month call option and notices the option’s calculated value is different from its market price. With respect to Weber’s use of the Black-Scholes option-pricing model,i. Discuss why the calculated value of an out-of-the-money European option may differ from its market price.ii. Discuss why the calculated value of an American option may differ from its market price.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:9781337514835

Author:MOYER

Publisher:CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course...

Finance

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Cengage Learning

Accounting for Derivatives Comprehensive Guide; Author: WallStreetMojo;https://www.youtube.com/watch?v=9D-0LoM4dy4;License: Standard YouTube License, CC-BY

Option Trading Basics-Simplest Explanation; Author: Sky View Trading;https://www.youtube.com/watch?v=joJ8mbwuYW8;License: Standard YouTube License, CC-BY