UPENN: LOOSE LEAF CORP.FIN W/CONNECT

17th Edition

ISBN: 9781260361278

Author: Ross

Publisher: McGraw-Hill Publishing Co.

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 22, Problem 3QP

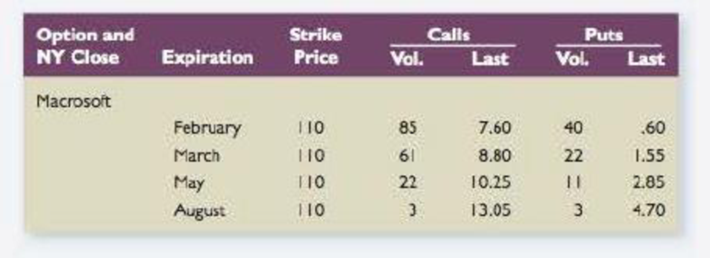

Calculating Payoffs Use the option quote information shown here to answer the questions that follow. The stock is currently selling for $114.

- a. Suppose you buy 10 contracts of the February 110 call option. How much will you pay, ignoring commissions?

- b. In part (a), suppose that Macrosoft stock is selling for $140 per share on the expiration date. How much is your options investment worth? What if the terminal stock price is $l25? Explain.

- c. Suppose you buy 10 contracts of the August 110 put option. What is your maximum gain? On the expiration date, Macrosoft is selling for $104 per share. How much is your options investment worth? What is your net gain?

- d. In part (c), suppose you sell 10 of the August 110put contracts. What is your net gain or loss if Macrosoft is selling for $103 at expiration? For $132? What is the breakeven price-that is, the terminal stock price that results in a zero profit?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Label the following for this diagram:

a. Name of options payoff

b. Identify whether positive or negative premium

c. Identify breakeven point

d. What is the profit or loss when stock price is S60 at maturity

e. Suppose you have this options position, should you exercise your right (if any) assuming that the stock price is $60 at maturity?

Option Payoffs and Profits Long put

$40

$20

$0

Option Payoff

Option Profit

Exerche Price

$20

S40

$20

$40

S60

$80.

Stock Price At Maturity

Payoff and Profit

You have written a call option on Walmart common stock. The option has an exercise price of $81, and Walmart’s stock currently trades at $79. The option premium is $1.60 per contract.

a. How much of the option premium is due to intrinsic value versus time value?

b. What is your net profit if Walmart’s stock price decreases to $77 and stays there until the option expires?

c. What is your net profit on the option if Walmart’s stock price increases to $87 at expiration of the option and the option holder exercises the option?

Label the following for this diagram:

a. Name of options payoff

b. Identify whether positive or negative premium

c. Identify break-even point

d. What is the profitt or loss when stock price is $60 at maturity

e. Suppose you have this options position, should you exercise your right (if any) assuming that the stock price is $60 at maturity?

Option Payoffs and Profits

$40

Long call

$20

$0

Option Payoff

Option Profit

---- Exercise Price

-$20

-$40

$0

$20

$40

$60

$80

Payoff and Profit

Chapter 22 Solutions

UPENN: LOOSE LEAF CORP.FIN W/CONNECT

Ch. 22 - Options What is a call option? A put option? Under...Ch. 22 - Options Complete the following sentence for each...Ch. 22 - American and European Options What is the...Ch. 22 - Intrinsic Value What is the intrinsic value of a...Ch. 22 - Option Pricing You notice that shares of stock in...Ch. 22 - Options and Stock Risk If the risk of a stock...Ch. 22 - Option Risk True or false: The unsystematic risk...Ch. 22 - Prob. 8CQCh. 22 - Option Price and Interest Rates Suppose the...Ch. 22 - Contingent Liabilities When you take out an...

Ch. 22 - Options and Expiration Dates What is the impact of...Ch. 22 - Options and Stock Price Volatility What is the...Ch. 22 - Insurance as an Option An insurance policy is...Ch. 22 - Equity as a Call Option It is said that the equity...Ch. 22 - Prob. 15CQCh. 22 - Put Call Parity You find a put and a call with the...Ch. 22 - Put- Call Parity A put and a call have the same...Ch. 22 - Put- Call Parity One thing put-call parity tells...Ch. 22 - Two-State Option Pricing Model T-bills currently...Ch. 22 - Understanding Option Quotes Use the option quote...Ch. 22 - Calculating Payoffs Use the option quote...Ch. 22 - Two-State Option Pricing Model The price of Ervin...Ch. 22 - Two-State Option Pricing Model The price of Tara,...Ch. 22 - Put-Call Parity A stock is currently selling for...Ch. 22 - Put-Call Parity A put option that expires in six...Ch. 22 - Put-Call Parity A put option and a call option...Ch. 22 - Pot-Call Parity A put option and a call option...Ch. 22 - Black-Scholes What are the prices of a call option...Ch. 22 - Black-Scholes What are the prices of a call option...Ch. 22 - Delta What are the deltas of a call option and a...Ch. 22 - Prob. 13QPCh. 22 - Prob. 14QPCh. 22 - Time Value of Options You are given the following...Ch. 22 - Prob. 16QPCh. 22 - Prob. 17QPCh. 22 - Prob. 18QPCh. 22 - Black-Scholes A call option has an exercise price...Ch. 22 - Black-Scholes A stock is currently priced at 35. A...Ch. 22 - Equity as an Option Sunburn Sunscreen has a zero...Ch. 22 - Equity as an Option and NPV Suppose the firm in...Ch. 22 - Equity as an Option Frostbite Thermalwear has a...Ch. 22 - Mergers and Equity as an Option Suppose Sunburn...Ch. 22 - Equity as an Option and NPV A company has a single...Ch. 22 - Two-State Option Pricing Model Ken is interested...Ch. 22 - Two-State Option Pricing Model Rob wishes to buy a...Ch. 22 - Two-State Option Pricing Model Maverick...Ch. 22 - Prob. 29QPCh. 22 - Prob. 30QPCh. 22 - Prob. 31QPCh. 22 - Two-State Option Pricing and Corporate Valuation...Ch. 22 - Black-Scholes and Dividends In addition to the...Ch. 22 - Prob. 34QPCh. 22 - Prob. 35QPCh. 22 - Prob. 36QPCh. 22 - Prob. 37QPCh. 22 - Prob. 38QPCh. 22 - Prob. 1MCCh. 22 - Prob. 2MCCh. 22 - Prob. 3MCCh. 22 - Prob. 4MCCh. 22 - Prob. 5MC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Suppose that a June call option to buy a share for $65 costs $3.5 and is held until June. Under what circumstances will the holder of the option make profit Under what circumstances will the option be exercised? Draw a diagram showing how the profit on a long position in the option depends on the stock price at the maturity of the option.arrow_forwardSuppose that a call option to buy a share for $200 costs $10. What is the delta of this option today if the current stock price is $180? (ignore time value of the option) A. around 2 B. None of these answers are correct. C. around 0.5 D. close to 0 E. close to 1arrow_forwardYou buy a put option on IBM common stock. The option has an exercise price of $136 and IBM’s stock currently trades at $140. The option premium is $5 per contract.a. What is your net profit on the option if IBM’s stock price increases to $150 at expiration of the option and you exercise the option? b. How much of the option premium is due to intrinsic value versus time value?c. What is your net profit if IBM’s stock price decreases to $130?d. Draw the payout diagram at maturity on a short put option position, option premium = $2, and the same exercise price... (Please give the full solution I will upvote)arrow_forward

- Give typing answer with explanation and conclusion You are considering purchasing a put on a stock with a current price of $33. The exercise price is $35, and the price of the corresponding call option is $3.25. According to the put-call parity theorem, if the risk-free rate of interest is 4% and there are 90 days until expiration, the value of the put should be:arrow_forwardSuppose you construct a strategy based on options on a stock that is currently selling for $100. The strategy is as follows: Buy one call option having an exercise price of $95. Sell two calls having an exercise price of $100. Buy one call option having an exercise price of $105. All of the options are written on the same stock and all have the same expiration date. Compute the payoff (the dollars you receive) from this strategy at the expiration date for each of the following alternative stocks prices: $90, $95, $98, $100, $102, $105, and $110. What additional information would be required to determine whether your strategy had been profitable? What is the name of this strategy?arrow_forward3. Suppose that a June put option to sell a share for $60 costs $4 and is held until June. (a) short position) make a profit? Under what circumstances will the seller of the option (i.e., the party with a (b) Under what circumstances will the option be exercised? (c) depends on the stock price at the maturity of the option. Draw a diagram showing how the profit from a short position in the optionarrow_forward

- A stock is currently trading for $25 per share and an investor is interested in the following two options with a one year expiration term. Options Call Put Strike Price $28 $24 Quoted Price $2 $4 a) Calculate the intrinsic values of the call and put. b) Draw the profit diagram for a short position in the put option described above. Label the diagram well. Show all the critical points on the diagram. For example, the intercepts on axes, maximum profit or maximum loss. What price movements are required for the investor to have a positive profit? c) Draw the profit diagram for a long position in the call option. And label the diagram well. d) Suppose one month later, the stock price moves up to $30 per share, how will the prices of the call and put change? Why? Briefly explain. e) Suppose an investor purchased 10 contracts of the 28 calls and sold 10 contracts of the 24 puts. If the stock price turns out to be $30 per share in one month, what is the total profit for this investor?arrow_forwardYou are pricing options with the following characteristics: •Current stock price (St): $35.60 •Exercise price (X): $50 •Time to expiration (T-t): 9 months •Risk-free rate (rf): 3.25% •Volatility (0): 45% (a): What is the Black-Scholes value of call option? In your hand-written solution, provide the calculations of d1,d2, and the final call price. Use Excel or another spreadsheet program to compute the values of N(d1) and N(d2). See the notes for details. (b): Using put-call parity, what is the value of a put option? For this case, assume continuous compounding, which implies that PVt(X)=e-r(T-t).X.arrow_forwardSuppose that a trader buys two call options and one put option. A one-year call| option on a stock with a strike price of $36 costs $1.90. A one-year put option on the stock with a strike price of $36 costs $1.68. What is the breakeven stock price rounded to the nearest cents , below which the trader makes a profit? Round your final result to the nearest cents and input one number only, without units or percentage sign [%], using the dot [.] to separate decimals. Your Answer: Answerarrow_forward

- Q1. You have purchased a call option on Johnson & Johnson common stock. The option has an exercise price of $57.50 and J & J’s stock currently trades at $58.93. The option premium is $2.17 per contract. Calculate your net profit on the option if J & J’s stock price rises to $62.50 and your exercise the option. Calculate your net profit on the option if J & J’s stock price falls to $58.00 and your exercise the option. If J & J’s stock price falls to $58.00 show that it is more profitable to exercise than not exercise the option you have purchased.arrow_forwardSuppose you purchase eight call contracts on Macron Technology stock. The strike price is $60 and the premium is $3. If, at expiration, the stock is selling for $64 per share, what are your call options worth? What is your net profit?arrow_forward2. Call Options A. How does the price of a call option respond to the following changes, other things equal? Does the price go up or down? Explain briefly the intuition for your answer. (). Stock price falls. (i). Volatility of stock price rises B. Suppose FlyByNight Corporation (FBN) is selling a one-year European call option that has an exercise price of $32. Assume that FBN's stock is currently selling for $20 and that over the coming year the price will either rise to $81 or fall to $11. Also assume that the one-year rate of interest is 10 percent. What would be the market price for this call option? Please explain carefully,arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...

Finance

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Cengage Learning

Accounting for Derivatives Comprehensive Guide; Author: WallStreetMojo;https://www.youtube.com/watch?v=9D-0LoM4dy4;License: Standard YouTube License, CC-BY

Option Trading Basics-Simplest Explanation; Author: Sky View Trading;https://www.youtube.com/watch?v=joJ8mbwuYW8;License: Standard YouTube License, CC-BY