Concept explainers

Videos

Recording and Posting Accrual Basis

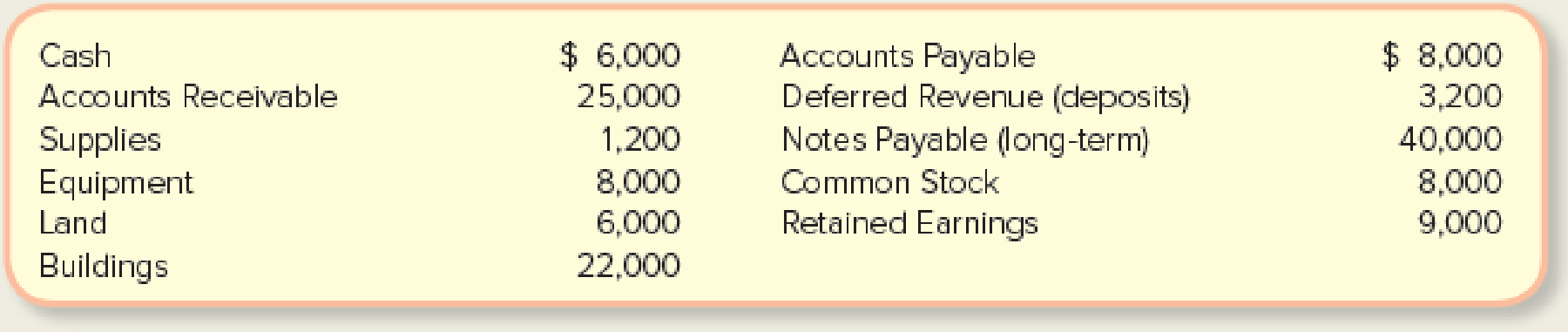

Ricky’s Piano Rebuilding Company has been operating for one year. On January 1, at the start of its second year, its income statement accounts had zero balances and its balance sheet account balances were as follows:

Required:

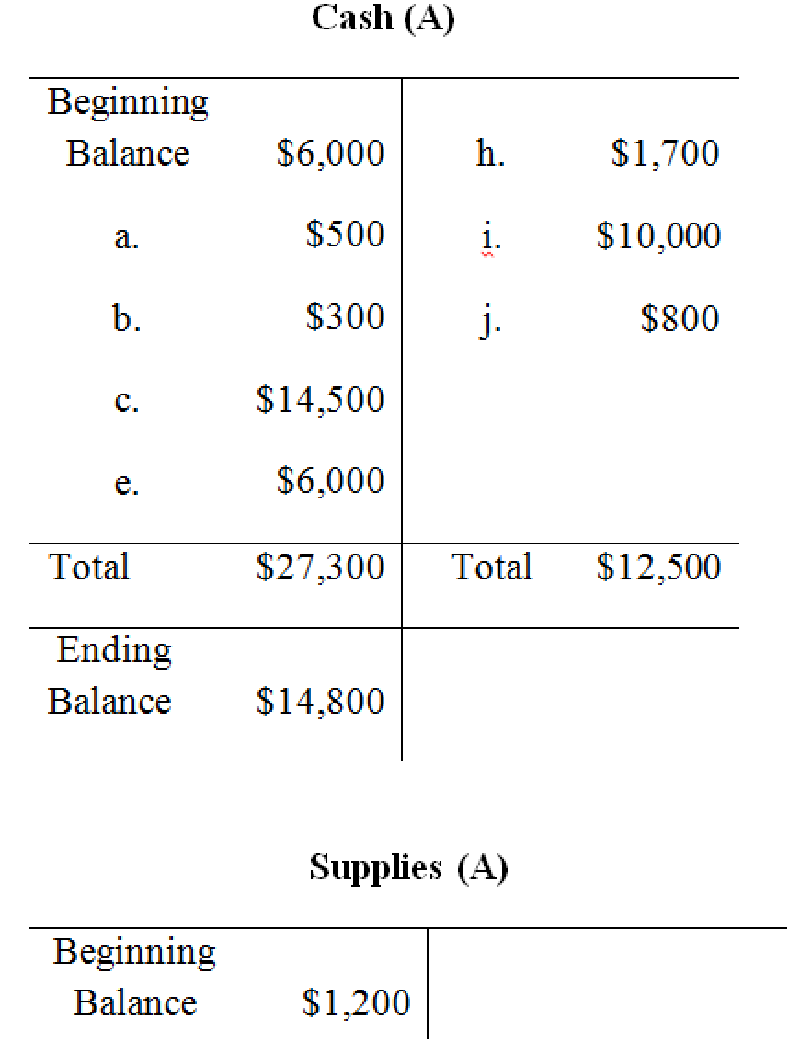

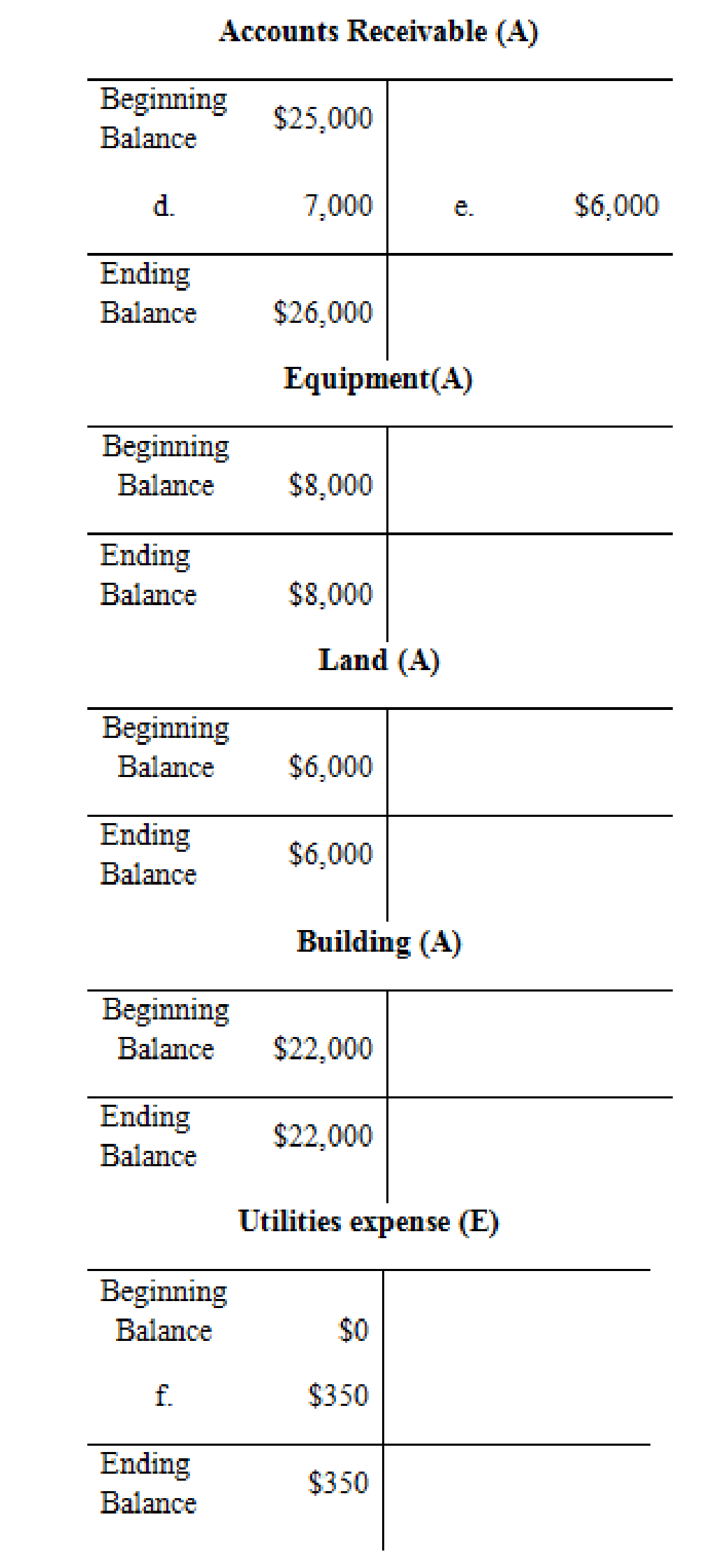

- 1. Create T-accounts for the balance sheet accounts and for these additional accounts: Service Revenue, Rent Revenue, Salaries and Wages Expense, and Utilities Expense. Enter the beginning balances. (If you are using the general ledger tool in Connect, this requirement will be completed for you.)

- 2. Prepare journal entries for the following January transactions, using the letter of each transaction as a reference:

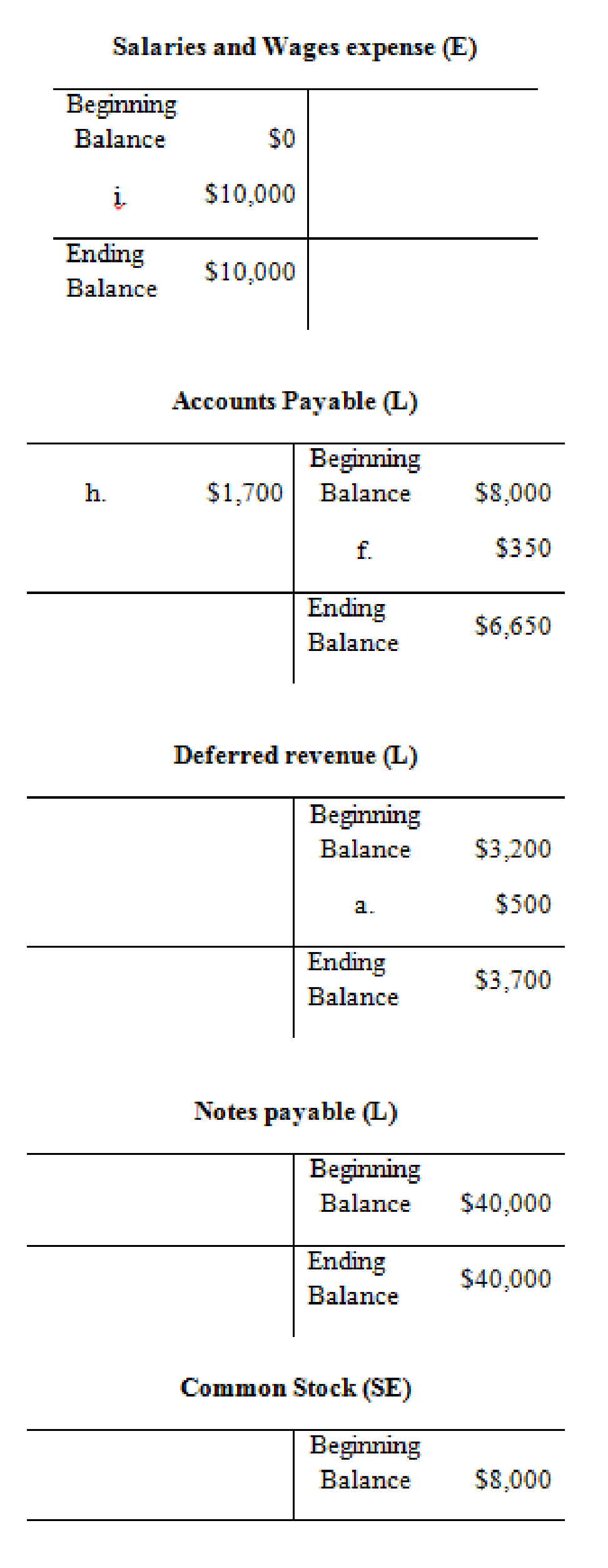

- a. Received a $500 deposit from a customer who wanted her piano rebuilt in February.

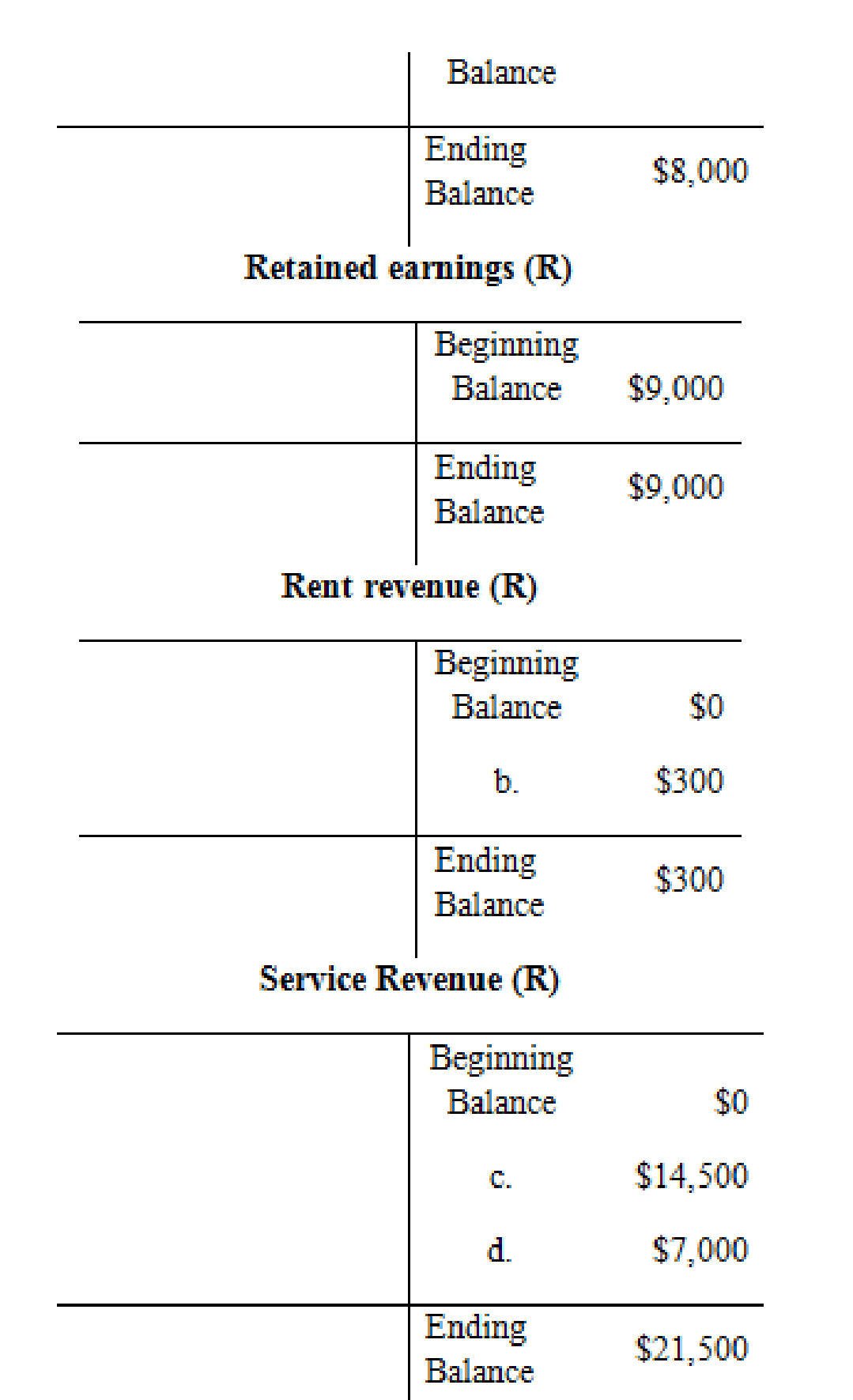

- b. Rented a part of the building to a bicycle repair shop; $300 rent received for January.

- c. Delivered five rebuilt pianos to customers who paid $14,500 in cash.

- d. Delivered two rebuilt pianos to customers for $7,000 charged on account.

- e. Received $6,000 from customers as payment on their accounts.

- f. Received an electric and gas utility bill for $350 for January services to be paid in February.

- g. Ordered $800 in supplies.

- h. Paid $1,700 on account in January.

- i. Paid $10,000 in wages to employees in January for work done this month.

- j. Received and paid cash for the supplies in (g).

- 3.

Post the journal entries to the T-accounts. Show the unadjusted ending balances in the T-accounts. (If you are using the general ledger tool, this requirement will be completed for you.) - 4. Use the balances in the completed T-accounts to prepare an unadjusted trial balance at January 31. (If you are using the general ledger tool, this requirement will be completed for you.)

- 5. Using the unadjusted balances, prepare a preliminary income statement and classified balance sheet for the month ended and at January 31

2.

Prepare journal entries for the given transaction.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Accrual basis of accounting:

In accrual Basis of accounting, the company records all the transaction that brings changes in the financial statement of the company. In accrual basis of accounting, the revenue is recognized for the accounting period, in which the goods are sold, or the service performed even if cash is not exchanged. Similarly the expenses are recognized for the accounting period, in which the business incurred expenses even if cash is not exchanged.

Prepare journal entries for the given transaction as follows:

|

Date | Account Title and Explanation | Debit ($) | Credit ($) | |

| a. | Cash (A+) | 500 | ||

| Deferred Revenue (L+) | 500 | |||

| (To record the cash receipt for the service yet to provide) | ||||

| b. | Cash (A+) | 300 | ||

| Rent Revenue (R+, SE+) | 300 | |||

| (To record the cash receipt from rental area) | ||||

| c. | Cash (A+) | 14,500 | ||

| Service Revenue (R+, SE+) | 14,500 | |||

| (To record the cash received for the service rendered) | ||||

| d. | Accounts Receivable (A+) | 7,000 | ||

| Service Revenue (R+, SE+) | 7,000 | |||

| (To record the service provided to customers on account) | ||||

| e. | Cash (A+) | 6,000 | ||

| Accounts Receivable (A–) | 6,000 | |||

| (To record the cash receipt from customer ) | ||||

| f. | Utilities expense (E+, SE–) | 350 | ||

| Accounts Payable (L+) | 350 | |||

| (To record the payment incurred for utilities expense which are to be paid later) | ||||

| g. | No transaction required | - | ||

| h. | Accounts Payable (L–) | 1,700 | ||

| Cash (A–) | 1,700 | |||

| (To record the payment of cash for the purchases made already) | ||||

| i. | Salaries and Wages Expense (E+, SE–) | 10,000 | ||

| Cash (A–) | 10,000 | |||

| (To record the payment of wages expenses to employees) | ||||

| j. | Supplies (A+) | 800 | ||

| Cash (A–) | 800 | |||

| (To record the purchase of supplies) | ||||

Table (1)

Note:

Item g is not a transaction because there is no cash exchange. Hence it is not recorded in the books of journal.

1. and 3.

Prepare the T accounts for the balance sheet accounts and post the journal entries to the T-account, also show the unadjusted ending balance in the T- accounts.

Explanation of Solution

T-account:

An account is referred to as a T-account, because the alignment of the components of the account resembles the capital letter ‘T’. An account consists of the three main components which are as follows:

- The title of the account.

- The left or debit side.

- The right or credit side.

The posting of the journal entries to the T accounts are as follows:

4.

Prepare an unadjusted trial balance at January 31 using the balances in the completed T-accounts.

Explanation of Solution

Unadjusted trial balance:

Unadjusted trial balance is that statement which contains complete list of accounts with their unadjusted balances. This statement is prepared at the end of every financial period.

Prepare an unadjusted trial balance at January 31 as follows:

| Company R | ||

| Unadjusted Trial Balance | ||

| At January 31 | ||

| Particulars | Debit | Credit |

| Cash | $14,800 | |

| Accounts Receivable | 26,000 | |

| Supplies | 2,000 | |

| Equipment | 8,000 | |

| Land | 6,000 | |

| Building | 22,000 | |

| Accounts Payable | $6,650 | |

| Deferred Revenue | 3,700 | |

| Notes Payable | 40,000 | |

| Common Stock | 8,000 | |

| Retained Earnings | 9,000 | |

| Service Revenue | 21,500 | |

| Rent Revenue | 300 | |

| Salaries and Wages Expense | 10,000 | |

| Utilities Expense | 350 | |

| Total | $89,150 | $89,150 |

Table (2)

5.

Prepare a preliminary income statement and classified balance sheet for the month ended January 31.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Classified balance sheet: The main elements of balance sheet assets, liabilities, and stockholders’ equity are categorized or classified further into sections, and sub-sections in a classified balance sheet. Assets are further classified as current assets, long-term investments, property, plant, and equipment (PPE), and intangible assets. Liabilities are classified into two sections current and long-term. Stockholders’ equity comprises of common stock and retained earnings. Thus, the classified balance sheet includes all the elements under different sections.

- Prepare a preliminary income statement for the month ended January 31 as follows:

| Company R | |

| Income Statement | |

| For the Month Ended January 31 | |

| Particulars | $ |

| Revenues: | |

| Service Revenue | $21,500 |

| Rent Revenue | 300 |

| Total Revenues (a) | 21,800 |

| Less: Expenses | |

| Salaries and Wages Expense | 10,000 |

| Utilities Expense | 350 |

| Total Expenses (b) | 10,350 |

| Net Income | $11,450 |

Table (3)

- Prepare the Statement of retained earnings for the month ended January 31 as follows:

| Company R | |

| Statement of Retained Earnings | |

| For the Month Ended January 31 | |

| Particulars | $ |

| Retained Earnings, January 1 | $9,000 |

| Add: Net Income | 11,450 |

| Less: Dividends | 0 |

| Retained Earnings, January 31 | $20,450 |

Table (4)

- Prepare the classified balance at January 31 as follows:

| Company R | |

| Statement of Retained Earnings | |

| For the Month Ended January 31 | |

| Particulars | $ |

| Assets: | |

| Current Assets: | |

| Cash | $14,800 |

| Accounts Receivable | 26,000 |

| Supplies | 2,000 |

| Total Current Assets | 42,800 |

| Equipment | 8,000 |

| Land | 6,000 |

| Building | 22,000 |

| Total Assets | $78,800 |

| Liabilities: | |

| Current Liabilities | |

| Accounts Payable | $6,650 |

| Deferred Revenue | 3,700 |

| Total Current Liabilities | 10,350 |

| Notes Payable (long-term) | 40,000 |

| Total Liabilities (a) | 50,350 |

| Stockholders’ Equity: | |

| Common Stock | 8,000 |

| Retained Earnings | 20,450 |

| Total Stockholders’ Equity (b) | 28,450 |

| Total Liabilities and Stockholders’ Equity | $78,800 |

Table (5)

Want to see more full solutions like this?

Chapter 3 Solutions

Connect Access Card for Fundamentals of Financial Accounting

- Journal entries and trial balance On August 1, 20Y7, Rafael Masey established Planet Realty, which completed the following transactions during the month: a. Rafael Masey transferred cash from a personal bank account to an account to be used for the business in exchange for common stock, 17,500. b. Purchased supplies on account, 2,300. c. Earned sales commissions, receiving cash, 13,300. d. Paid rent on office and equipment for the month, 3,000. e. Paid creditor on account, 1,150. f. Paid dividends, 1,800. g. Paid automobile expenses (including rental charge) for month, 1,500, and miscellaneous expenses, 400. h. Paid office salaries, 2,800. i. Determined that the cost of supplies used was 1,050. Instructions 1. Journalize entries for transactions (a) through (i), using the following account titles: Cash, Supplies, Accounts Payable, Common Stock, Dividends, Sales Commissions, Rent Expense, Office Salaries Expense, Automobile Expense, Supplies Expense, Miscellaneous Expense. Journal entry explanations may be omitted. 2. Prepare T accounts, using the account titles in (1). Post the journal entries to these accounts, placing the appropriate letter to the left of each amount to identify the transactions. Determine the account balances, after all posting is complete. Accounts containing only a single entry do not need a balance. 3. Prepare an unadjusted trial balance as of August 31, 20Y7. 4. Determine the following: a. Amount of total revenue recorded in the ledger. b. Amount of total expenses recorded in the ledger. c. Amount of net income for August. 5. Determine the increase or decrease in retained earnings for August.arrow_forwardJournal Entries, Trial Balance, and Financial Statements Neveranerror Inc. was organized on June 2 by a group of accountants to provide accounting and tax services to small businesses. The following transactions occurred during the first month of business: June 2: Received contributions of $10,000 from each of the three owners of the business in exchange for shares of stock. June 5: Purchased a computer system for $12,000. The agreement with the vendor requires a down payment of $2,500 with the balance due in 60 days. June 8: Signed a two-year promissory note at the bank and received cash of $20,000. June 15: Billed $12,350 to clients for the first half of June. Clients are billed twice a month for services performed during the month, and the bills are payable within ten days. June 17: Paid a $900 bill from the local newspaper for advertising for the month of June. June 23: Received the amounts billed to clients for services performed during the first half of the month. June 28: Received and paid gas, electric, and water bills. The total amount is $2,700. June 29: Received the landlords bill for $2,200 for rent on the office space that Neveranerror leases. The bill is payable by the 10th of the following month. June 30: Paid salaries and wages for June. The total amount is $5,670. June 30: Billed $18,400 to clients for the second half of June. June 30: Declared and paid dividends in the amount of $6,000. Required Prepare journal entries on the books of Neveranerror Inc. to record the transactions entered into during the month. Ignore depreciation expense and interest expense. Prepare a trial balance at June 30. Prepare the following financial statements: Income statement for the month of June Statement of retained earnings for the month of June Classified balance sheet at June 30 Assume that you have just graduated from college and have been approached to join this company as an accountant. From your reading of the financial statements for the first month, would you consider joining the company? Explain your answer. Limit your answer to financial considerations only.arrow_forwardOn July 1, a client paid an advance payment (retainer) of $5,000 to cover future legal services. During the period, the company completed $3,500 of the agreed-on services for the client. There was no beginning balance in the Unearned Revenue account for the period. Based on the information provided, A. Make the December 31 adjusting journal entry to bring the balances to correct. B. Show the impact that these transactions had.arrow_forward

- Williams Mechanic Services prepared the following work sheet for the year ended March 31,20--. Required 1. Complete the work sheet. (Skip this step if using CLGL.) 2. Prepare an income statement. 3. Prepare a statement of owners equity. Assume that there was an additional investment of 5,000 on March 13. 4. Prepare a balance sheet. 5. Journalize the closing entries using the four steps in the correct sequence. 6. Prepare a post-dosing trial balance. Check Figure Post-closing trial balance total, 31,765arrow_forwardAt the end of April, the first month of operations, the following selected data were taken from the financial statements of Shelby Crawford, an attorney: In preparing the financial statements, adjustments for the following data were overlooked: Supplies used during April, 2,750. Unbilled fees earned at April 30, 23,700. Depreciation of equipment for April, 1,800. Accrued wages at April 30, 1,400. Instructions 1. Journalize the entries to record the omitted adjustments. 2. Determine the correct amount of net income for April and the total assets, liabilities, and owners equity at April 30. In addition to indicating the corrected amounts, indicate the effect of each omitted adjustment by setting up and completing a columnar table similar to the following. The adjustment for supplies used is presented as an example.arrow_forwardAdjusting entries Trident Repairs Service, an electronics repair store, prepared the following unadjusted trial balance at the end of its first year of operations: For preparing the adjusting entries, the following data were assembled: Fees earned but unbilled on November 30 were 7,000. Supplies on hand on November 30 were 1,300. Depreciation of equipment was estimated to be 7,200 for the year. The balance in unearned fees represented the November 1 receipt in advance for services to be provided. During November, 13,500 of the services were provided. Unpaid wages accrued on November 30 were 4,800. Instructions 1. Journalize the adjusting entries necessary on November 30, 20Y3. 2. Determine the revenues, expenses, and net income of Trident Repairs Service before the adjusting entries. 3. Determine the revenues, expense, and net income of Trident Repairs Service after the adjusting entries. 4. Determine the effect of the adjusting entries on Retained Earnings.arrow_forward

- Complete accounting cycle For the past several years, Steffy Lopez has operated a part-time consulting business from his home. As of July 1, 20Y2, Steffy decided to move to rented quarters and to operate the business, which was to be known as Diamond Consulting, on a full-time basis. Diamond entered into the following transactions during July: Record the following transactions on Page 2 of the journal: Instructions 1. Journalize each transaction in a two-column journal starting on Page 1, referring to the following chart of accounts in selecting the accounts to be debited and credited. (Do not insert the account numbers in the journal at this time.) 2. Post the journal to a ledger of four-column accounts. 3. Prepare an unadjusted trial balance. 4. At the end of July, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6). (a) Insurance expired during July is 375. (b) Supplies on hand on July 31 are 1,525. (c) Depreciation of office equipment for July is 750. (d) Accrued receptionist salary on July 31 is 175. (e) Rent expired during July is 2,400. (f) Unearned fees on July 31 are 2,750. 5. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 3 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a statement of stockholders equity, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 4 of the journal. Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. 10. Prepare a post-closing trial balance.arrow_forwardDetermining an Ending Account Balance Jessies Accounting Services was organized on June 1. The company received a contribution of $1,000 from each of the two principal owners. During the month, Jessies Accounting Services provided services for cash of $1,400 and services on account for $450, received $250 from customers in payment of their accounts, purchased supplies on account for $600 and equipment on account for $1,350, received a utility bill for $250 that will not be paid until July, and paid the full amount due on the equipment. Use a T account to determine the companys Cash balance on June 30.arrow_forwardAt the end of August, the first month of operations, the following selected data were taken from the financial statements of Tucker Jacobs, an attorney: In preparing the financial statements, adjustments for the following data were overlooked: Unbilled fees earned at August 31, 31,900. Depreciation of equipment for August, 7,500. Accrued wages at August 31, 5,200. Supplies used during August, 3,000. Instructions 1. Journalize the entries to record the omitted adjustments. 2. Determine the correct amount of net income for August and the total assets, liabilities, and owners equity at August 31. In addition to indicating the corrected amounts, indicate the effect of each omitted adjustment by setting up and completing a columnar table similar to the following. The first adjustment is presented as an example.arrow_forward

- Considering the following events, determine which month the revenue or expenses would be recorded using the accounting method specified. a. Gerber Company uses the cash basis of accounting. Gerber prepays cash in May for insurance that only covers the following month, (June). b. Matthews and Dudley Attorneys uses the accrual basis of accounting. Matthews and Dudley Attorneys receives cash from customers in June for services to be performed in July. c. Eckstein Company uses the accrual basis of accounting. Eckstein prepays cash in October for rent that covers the following month, (October). d. Gerbino Company uses the cash basis of accounting. Gerbino makes a sale to a customer in February but does not expect payment until March.arrow_forwardThe Detection of Errors in a Trial Balance and Preparation of a Corrected Trial Balance Malcolm Inc. was incorporated on January 1 with the issuance of capital stock in return for $90,000 of cash contributed by the owners. The only other transaction entered into prior to beginning operations was the issuance of a $75,300 note payable in exchange for building and equipment. The following trial balance was prepared at the end of the first month by the bookkeeper for Malcolm Inc.: Required Identify the two errors in the trial balance. Ignore depreciation expense and interest expense. Prepare a corrected trial balance.arrow_forwardAdjusting entries and errors At the end of August, the first month of operations, the following selected data were taken from the financial statements of Tucker Jacobs, an attorney: In preparing the financial statements, adjustments for the following data were overlooked: Unbilled fees earned at August 31, 31,900. Depreciation of equipment for August, 7,500. Accrued wages at August 31, 5,200. Supplies used during August, 3,000. Instructions 1. Journalize the entries to record the omitted adjustments. 2. Determine the correct amount of net income for August and the total assets, liabilities, and stockholders equity at August 31. In addition to indicating the corrected amounts, indicate the effect of each omitted adjustment by setting up and completing a columnar table similar to the following. The first adjustment is presented as an example.arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

- Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub