Concept explainers

Videos

(a)

The Accounting Information System is a system that a business uses for collecting, storing, and processing the data of the accounting transactions and provides the financial information to the decision makers.

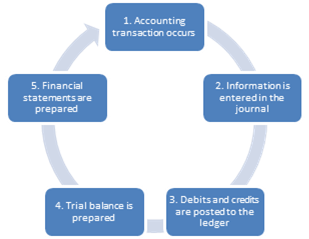

Accounting information cycle:

Figure (1)

To indicate: The proper flow of accounting information, as Person B is confused about the accounting information flows.

(b)

To indicate: The proper flow of accounting information, as Person B is confused about the accounting information flows.

(c)

To indicate: The proper flow of accounting information, as Person B is confused about the accounting information flows.

(d)

To indicate: The proper flow of accounting information, as Person B is confused about the accounting information flows.

(e)

To indicate: The proper flow of accounting information, as Person B is confused about the accounting information flows.

Want to see the full answer?

Check out a sample textbook solution

Chapter 3 Solutions

FINANCIAL ACCOUNTING:TOOLS FOR BUSINESS

- Which of the following accounting records is the main source of information used to prepare the financial statements? A. journal entries B. T-accounts C. trial balance D. chart of accountsarrow_forwardA __________ is a book in which business transactions are recorded. a. journal b. ledger c. trial balance d. balance sheetarrow_forwardWhich is the last step of accounting as a process of information? Select one: a. Recording the transaction b. Preparation of financial statement c. Communication of information d. Analysis and interpretation of information Which of the following is not a part of the functions of the accounting system? Select one: a. Reporting the results of operations during a reporting period b. Classifying and summarizing the effects of the transactions on the accounting elements c. Analyzing and recording the business transactions of the enterprise. d. Preparing financial statements that are favorable to the data-users. The chief accounting officer of a medium-sized or large business enterprise. Select one: a. Auditor b. Controller c. Bookkeeper d. Treasurerarrow_forward

- Posting is the process of a. Analyzing the impact of the transaction on the accounting equation. b. Obtaining information about external transactions from source documents. c. Transferring the debit and credit information from the journal to individual accounts in the general ledger. d. Listing all accounts and their balances at a particular date and showing the equality of total debits and total credits.arrow_forwardListed below are all the steps in the accounting cycle.(a) Record and post adjusting entries.(b) Post the transaction to the T-account in the general ledger.(c) Record the transaction.(d) Prepare financial statements (income statement, statement of stockholders’ equity, balance sheet, and statement of cash flows).(e) Record and post closing entries.(f) Prepare a trial balance.(g) Analyze the impact of the transaction on the accounting equation.(h) Assess whether the transaction results in a debit or a credit to the account balance.(i) Use source documents to identify accounts affected by external transactions.Required: List the steps in proper order.arrow_forwardJanis Engle has prepared the following list of statements about the accounting cycle. 1. “Journalize the transactions” is the first step in the accounting cycle. 2. Reversing entries are a required step in the accounting cycle. 3. Correcting entries do not have to be part of the accounting cycle. 4. If a worksheet is prepared, some steps of the accounting cycle are incorporated into the worksheet. 5. The accounting cycle begins with the analysis of business transactions and ends with the preparation of a post-closing trial balance. 6. All steps of the accounting cycle occur daily during the accounting period. 7. The step of “post to the ledger accounts” occurs before the step of “journalize the transactions.” 8. Closing entries must be prepared before financial statements can be prepared. Instructions Identify each statement as true or false. If false, indicate how to correct the statement. Please answer it with proper explanationarrow_forward

- Below are the steps in the measurement process of external transactions. Arrange them from first (1) to last (6).__________ a. Post the transaction to the T-accounts in the general ledger.__________ b. Assess whether the impact of the transaction results in a debit or credit to account balances.__________ c. Use source documents to identify accounts affected by an external transaction.__________ d. Analyze the impact of the transaction on the accounting equation.__________ e. Prepare a trial balance.__________ f. Record the transaction using debits and credits.arrow_forward(B) While processing the accounting Information Manually You would have to go through the Accounting Cycle. Discuss how you would decide regarding the debit and credit aspects of the transactionsarrow_forwardselect the item that best completes each of the description below A____ of accounts is a list of all accounts a company uses not including account balance a____ contains a record of decreases and increases in a spefic revenue, expenses, asset, liability, or equity a___ is a record containing all accounts used by a company including account balance a___ had a complete record of every transaction recored a___ such as a bank statement is objective evidence of transaction and their amountsarrow_forward

- Which of the following is true? a.The process of transferring information from the journal to the ledger is called journalizing. b.When recording business transactions, it is not important that one use the exact account titles as listed in the chart of accounts. c.The ledger account form maintains a running balance of the account. d.All of these listed answers are correct.arrow_forwardIn accounting it’s important to understand that there may be events that occur that are not business transactions that affects the accounting equation. Remember that the expand accounting equation is: Asset=Liabilities +owner’s Equity +Revenue-Expenses. Please be sure that you provide this transaction in general journal format. Additionally give us an example of an event that is not an accounting transaction .arrow_forwardb) What do you understand by the term booking, explain the process ofbookkeeping to be aopted by a petty trader and the likely summarizeddoucuments that can come out of the book keeping process? c) The process of preparing accounting records require care and good practice, explain to Maame Monkuah the characteristics of information needed to prepare a balance sheet or profit and loss acccount.arrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub