Concept explainers

Videos

You may refer to the opening story of Tony and Suzie and their decision to start Great Adventures in AP 1–1. More of their story and the first set of transactions for the company in July are presented in AP 2–1 and repeated here.

| July 1 | Sell $10,000 of common stock to Suzie. |

| 1 | Sell $10,000 of common stock to Tony. |

| 1 | Purchase a one-year insurance policy for $4,800 ($400 per month) to cover injuries to participants during outdoor clinics. |

| 2 | Pay legal fees of $1,500 associated with incorporation. |

| 4 | Purchase office supplies of $1,800 on account. |

| 7 | Pay for advertising of $300 to a local newspaper for an upcoming mountain biking clinic to be held on July 15. Attendees will be charged $50 the day of the clinic. |

| 8 | Purchase 10 mountain bikes, paying $12,000 cash. |

| 15 | On the day of the clinic, Great Adventures receives cash of $2,000 from 40 bikers. Tony conducts the mountain biking clinic. |

| 22 | Because of the success of the first mountain biking clinic, Tony holds another mountain biking clinic and the company receives $2,300. |

| 24 | Pay for advertising of $700 to a local radio station for a kayaking clinic to be held on August 10. Attendees can pay $100 in advance or $150 on the day of the clinic. |

| 30 | Great Adventures receives cash of $4,000 in advance from 40 kayakers for the upcoming kayak clinic. |

The following transactions occur over the remainder of the year.

| Aug. 1 | Great Adventures obtains a $30,000 low-interest loan for the company from the city council, which has recently passed an initiative encouraging business development related to outdoor activities. The loan is due in three years, and 6% annual interest is due each year on July 31. |

| Aug. 4 | The company purchases 14 kayaks, paying $28,000 cash. |

| Aug. 10 | Twenty additional kayakers pay $3,000 ($150 each), in addition to the $4,000 that was paid in advance on July 30, on the day of the clinic. Tony conducts the first kayak clinic. |

| Aug. 17 | Tony conducts a second kayak clinic, and the company receives $10,500 cash. |

| Aug. 24 | Office supplies of $1,800 purchased on July 4 are paid in full. |

| Sep. 1 | To provide better storage of mountain bikes and kayaks when not in use, the company rents a storage shed, purchasing a one-year rental policy for $2,400 ($200 per month). |

| Sep. 21 | Tony conducts a rock-climbing clinic. The company receives $13,200 cash. |

| Oct. 17 | Tony conducts an orienteering clinic. Participants practice how to understand a topographical map, read an altimeter, use a compass, and orient through heavily |

| Dec. 1 | Tony decides to hold the company’s first adventure race on December 15. Four-person teams will race from checkpoint to checkpoint using a combination of mountain biking, kayaking, orienteering, trail running, and rock-climbing skills. The first team in each category to complete all checkpoints in order wins. The entry fee for each team is $500. |

| Dec. 5 | To help organize and promote the race, Tony hires his college roommate, Victor. Victor will be paid $50 in salary for each team that competes in the race. His salary will be paid after the race. |

| Dec. 8 | The company pays $1,200 to purchase a permit from a state park where the race will be held. The amount is recorded as a miscellaneous expense. |

| Dec. 12 | The company purchases racing supplies for $2,800 on account due in 30 days. Supplies include trophies for the top-finishing teams in each category, promotional shirts, snack foods and drinks for participants, and field markers to prepare the racecourse. |

| Dec. 15 | The company receives $20,000 cash from a total of forty teams, and the race is held. |

| Dec. 16 | The company pays Victor’s salary of $2,000. |

| Dec. 31 | The company pays a dividend of $4,000 ($2,000 to Tony and $2,000 to Suzie). |

| Dec. 31 | Using his personal money, Tony purchases a diamond ring for $4,500. Tony surprises Suzie by proposing that they get married. Suzie accepts and they get married! |

The following information relates to year-end

a.

b. Six months’ worth of insurance has expired.

c. Four months’ worth of rent has expired.

d. Of the $1,800 of office supplies purchased on July 4, $300 remains.

e. Interest expense on the $30,000 loan obtained from the city council on August 1 should be recorded.

f. Of the $2,800 of racing supplies purchased on December 12, $200 remains.

g. Suzie calculates that the company owes $14,000 in income taxes.

Required:

1. Record transactions from July 1 through December 31.

2. Record adjusting entries as of December 31, 2018.

3. Post transactions from July 1 through December 31 and adjusting entries on December 31 to T-accounts.

4. Prepare an adjusted

5. For the period July 1 to December 31, 2018, prepare an income statement and statement of stockholders’ equity. Prepare a classified balance sheet as of December 31, 2018.

6. Record closing entries as of December 31, 2018.

7. Post closing entries to T-accounts.

8. Prepare a post-closing trial balance as of December 31, 2018.

Requirement – 1

To record: The journal entries for given transactions from July 1 to December 31.

Explanation of Solution

Journal:

Journal is the method of recording monetary business transactions in chronological order. It records the debit and credit aspects of each transaction to abide by the double-entry system.

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

The journal entries for given transactions of Company G are as follows:

| Date | Account Title and Explanation | PostRef. | Debit($) | Credit($) |

| 2018 | Cash | 10,000 | ||

| July 1 | Common stock | 10,000 | ||

| (To record the issuance of common stock in cash to Company S) | ||||

| 2018 | Cash | 10,000 | ||

| July, 2 | Common stock | 10,000 | ||

| (To record the issuance of common stock in cash to Company T) | ||||

| 2018 | Prepaid insurance | 4,800 | ||

| July 1 | Cash | 4,800 | ||

| (To record the purchase of one year insurance policy in cash) | ||||

| 2018 | Legal fees expense | 1,500 | ||

| July, 2 | Cash | 1,500 | ||

| (To record the payment of legal fees) | ||||

| 2018 | Supplies (office) | 1,800 | ||

| July, 4 | Accounts payable | 1,800 | ||

| (To record purchase of office supplies on account) | ||||

| 2018 | Advertising expense | 300 | ||

| July, 7 | Cash | 300 | ||

| (To record payment of advertising expense) | ||||

| 2018 | Equipment (Bikes) | 12,000 | ||

| July, 7 | Cash | 12,000 | ||

| (To record the purchase of mountain bike) | ||||

| 2018 | Cash | 2,000 | ||

| July, 15 | Service revenue (Clinic) | 2,000 | ||

| ( To record the cash received for service revenue) | ||||

| 2018 | Cash | 2,300 | ||

| July, 22 | Service revenue (Clinic) | 2,300 | ||

| ( To record the cash received for service revenue) | ||||

| 2018 | Advertising expense | 700 | ||

| July, 22 | Cash | 700 | ||

| (To record the payment of advertising expense in cash) | ||||

| 2018 | Cash | 4,000 | ||

| July, 30 | Deferred revenue | 4,000 | ||

| (To record advance cash received from customer) | ||||

| 2018 | Cash | 30,000 | ||

| August, 1 | Notes payable | 30,000 | ||

| (To record loan received from city council) | ||||

| 2018 | Equipment (Kayaks) | 28,000 | ||

| August, 4 | Cash | 28,000 | ||

| (To record the purchase of equipment in cash) | ||||

| 2018 | Cash | 3,000 | ||

| August, 10 | Deferred revenue | 4,000 | ||

| Service revenue | 7,000 | |||

| (To record the cash received from service revenue and recognized service revenue) | ||||

| 2018 | Cash | 10,500 | ||

| August, 17 | Service revenue | 10,500 | ||

| (To record cash received from service revenue) | ||||

| 2018 | Accounts payable | 1,800 | ||

| August, 24 | Cash | 1,800 | ||

| ( To record payment of cash to creditors) | ||||

| 2018 | Prepaid rent | 2,400 | ||

| September 1 | Cash | 2,400 | ||

| (To record the payment of one year advance rent) | ||||

| 2018 | Cash | 13,200 | ||

| September 21 | Service revenue (Clinic) | 13,200 | ||

| (To record the cash received from customer) | ||||

| 2018 | Cash | 17,900 | ||

| October 17 | Service revenue (Clinic) | 17,900 | ||

| (To record the cash received from customer) | ||||

| 2018 | Miscellaneous expense | 1,200 | ||

| December 8 | Cash | 1,200 | ||

| (To record the payment of miscellaneous expense) | ||||

| 2018 | Supplies (Racing) | 2,800 | ||

| December 12 | Accounts payable | 2,800 | ||

| (To record purchase of supplies on account) | ||||

| 2018 | Cash | 20,000 | ||

| December 15 | Service revenue (Racing) | 20,000 | ||

| (To record cash received from service revenue) | ||||

| 2018 | Salaries expense | 2,000 | ||

| December 16 | Cash | 2,000 | ||

| (To record the supplies expense incurred) | ||||

| 2018 | Dividend | 4,000 | ||

| December 31 | Cash | 4,000 | ||

| (To record the payment of cash dividends) |

Table (1)

Requirement – 2

To record: The adjusting journal entries on December 31.

Explanation of Solution

Adjusting entries:

Adjusting entries refers to the entries that are made at the end of an accounting period in accordance with revenue recognition principle, and expenses recognition principle. The purpose of adjusting entries is to adjust the revenue, and the expenses during the period in which they actually occurs.

The adjusting journal entries for given transactions of Company G are as follows:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| 2018 | Depreciation expense | 8,000 | ||

| December 31 | Accumulated depreciation | 8,000 | ||

| (To record depreciation expense incurred at the end of the accounting year) | ||||

| 2018 | Insurance expense | 2,400 | ||

| December 31 | Prepaid insurance | 2,400 | ||

| (To record the insurance expense incurred at the end of the accounting period) | ||||

| 2018 | Rent expense | 800 | ||

| December 31 | Prepaid rent | 800 | ||

| (To record the rent expense incurred at the end of the accounting year) | ||||

| 2018 | Supplies expense (Office) | 1,500 | ||

| December 31 | Supplies | 1,500 | ||

| (To record supplies expense incurred at the end of the accounting year) | ||||

| 2018 | Interest expense | 750 | ||

| December 31 | Interest payable | 750 | ||

| (To record interest expense incurred at the end of the accounting year) | ||||

| 2018 | Supplies expense (Racing) | 2,600 | ||

| December 31 | Supplies | 2,600 | ||

| (To record supplies expense incurred at the end of the accounting year) | ||||

| 2018 | Income tax expense | 14,000 | ||

| December 31 | Income tax payable | 14,000 | ||

| (To record the income tax expense incurred at the end of the accounting year) |

Table (2)

Requirement – 3

To post: The Transactions to T-accounts of Company G.

Explanation of Solution

T-account:

T-account refers to an individual account, where the increases or decreases in the value of specific asset, liability, stockholder’s equity, revenue, and expenditure items are recorded.

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

- (a) The title of the account

- (b) The left or debit side

- (c) The right or credit side

T-accounts for above transactions are as follows:

| Cash | |

| 10,000 | 4,800 |

| 10,000 | 1,500 |

| 2,000 | 300 |

| 2,300 | 12,000 |

| 4,000 | 700 |

| 30,000 | 28,000 |

| 3,000 | 1,800 |

| 10,500 | 2,400 |

| 13,200 | 1,200 |

| 17,900 | 2,000 |

| 20,000 | 4,000 |

| 64,200 | |

| Prepaid Insurance | |

| 4,800 | 2,400 |

| 2,400 | |

| Supplies (Racing) | |

| 2,800 | 2,600 |

| 200 | |

| Prepaid Rent | |

| 2,400 | 800 |

| 1,600 | |

| Supplies (Office) | |

| 1,800 | 1,500 |

| 300 | |

| Equipment (Bikes) | |

| 12,000 | |

| 12,000 | |

| Equipment (Kayaks) | |

| 28,000 | |

| 28,000 | |

| Accumulated Depreciation | |

| 8,000 | |

| 8,000 | |

| Accounts Payable | |

| 1800 | 1,800 |

| 2,800 | |

| 2,800 | |

| Deferred Revenue | |

| 4,000 | 4,000 |

| 0 | |

| Interest Payable | |

| 750 | |

| 750 | |

| Income Tax Payable | |

| 14,000 | |

| 14,000 | |

| Notes Payable | |

| 30,000 | |

| 30,000 | |

| Common Stock | |

| 10,000 | |

| 10,000 | |

| 20,000 | |

| Dividends | |

| 4,000 | |

| 4,000 | |

| Service Revenue (Clinic) | |

| 2,000 | |

| 2,300 | |

| 7,000 | |

| 10,500 | |

| 13,200 | |

| 17,900 | |

| 52,900 | |

| Service Revenue (Racing) | |

| 20,000 | |

| 20,000 | |

| Legal Fees Expense | |

| 1,500 | |

| 1,500 | |

| Advertising Expense | |

| 300 | |

| 700 | |

| 1,000 | |

| Rent Expense | |

| 800 | |

| 800 | |

| Salaries Expense | |

| 2,000 | |

| 2,000 | |

| Depreciation Expense | |

| 8,000 | |

| 8,000 | |

| Insurance Expense | |

| 2,400 | |

| 2,400 | |

| Supplies Expense (Office) | |

| 1,500 | |

| 1,500 | |

| Supplies Expense (Racing) | |

| 2,600 | |

| 2,600 | |

| Interest Expense | |

| 750 | |

| 750 | |

| Income Tax Expense | |

| 14,000 | |

| 14,000 | |

| Miscellaneous Expense | |

| 1,200 | |

| 1,200 | |

Requirement – 4

To prepare: The adjusted trial balance of Company G.

Explanation of Solution

Adjusted trial balance:

Adjusted trial balance is a summary of all the ledger accounts, and it contains the balances of all the accounts after the adjustment entries are journalized, and posted.

Adjusted trial balance of Company G is as follows:

| Company G | ||

| Adjusted Trial Balance | ||

| December 31, 2018 | ||

| Accounts | Debit ($) | Credit ($) |

| Cash | 64,200 | |

| Prepaid Insurance | 2,400 | |

| Prepaid Rent | 1,600 | |

| Supplies (Office) | 300 | |

| Supplies (Racing) | 200 | |

| Equipment (Bikes) | 12,000 | |

| Equipment (Kayaks) | 28,000 | |

| Accumulated Depreciation | $8,000 | |

| Accounts Payable | 2,800 | |

| Income Tax Payable | 14,000 | |

| Interest Payable | 750 | |

| Notes Payable | 30,000 | |

| Common Stock | 20,000 | |

| Dividends | 4,000 | |

| Service Revenue (Clinic) | 52,900 | |

| Service Revenue (Racing) | 20,000 | |

| Advertising Expense | 1,000 | |

| Depreciation Expense | 8,000 | |

| Income Tax Expense | 14,000 | |

| Insurance Expense | 2,400 | |

| Interest Expense | 750 | |

| Legal Fees Expense | 1,500 | |

| Miscellaneous Expense | 1,200 | |

| Rent Expense | 800 | |

| Salaries Expense | 2,000 | |

| Supplies Expense (Office) | 1,500 | |

| Supplies Expense (Racing) | 2,600 | |

| Totals | 148,450 | 148,450 |

Table (3)

Requirement –5

To prepare: The income statement and classified balance sheet of Company G.

Explanation of Solution

Income statement:

This is the financial statement of a company which shows all the revenues earned and expenses incurred by the company over a period of time.

Statement of stockholders’ equity:

This statement reports the beginning stockholder’s equity and all the changes, which led to ending stockholder’s’ equity. Additional capital, net income from income statement is added to and drawings are deducted from beginning stockholder’s equity to arrive at the result of closing balance of stockholders’ equity.

Classified balance sheet:

This is the financial statement of a company which shows the grouping of similar assets and liabilities under subheadings.

Income statement:

Income statement of Company G is as follows:

| Company G | ||

| Income Statement | ||

| For the year ended December 31, 2018 | ||

| ($) | ($) | |

| Revenues: | ||

| Service revenue (clinic) | 52,900 | |

| Service revenue (racing) | 20,000 | |

| Total revenues | 72,900 | |

| Expenses: | ||

| Advertising expense | 1,000 | |

| Depreciation expense | 8,000 | |

| Income tax expense | 14,000 | |

| Insurance expense | 2,400 | |

| Interest expense | 750 | |

| Legal fees expense | 1,500 | |

| Miscellaneous expense | 1,200 | |

| Rent expense | 800 | |

| Salaries expense | 2,000 | |

| Supplies expense (office) | 1,500 | |

| Supplies expense (racing) | 2,600 | |

| Total expenses | 35,750 | |

| Net income | 37,150 | |

Table (4)

Therefore, the net income of Company G is $37,150.

Statement of stockholder’s equity:

The statement of stockholder’s equity of Company G for the year ended December 31, 2018 is as follows:

| Company G | |||

| Statement of Stockholders’ Equity | |||

| For the period ended December 31, 2018 | |||

| Common stock ($) | Retained earnings ($) | Total stockholders' equity ($) | |

| Balance at July 1 | $0 | $0 | $0 |

| Issuance of common stock | 20,000 | 20,000 | |

| Add: Net income for 2018 | 37,150 | 37,150 | |

| Less: Dividends | -4,000 | -4,000 | |

| Balance at December 31 | $20,000 | $33,150 | $53,150 |

Table (5)

Therefore, the total stockholder’s equity of Company G for the year ended December 31, 2018 is $53,150.

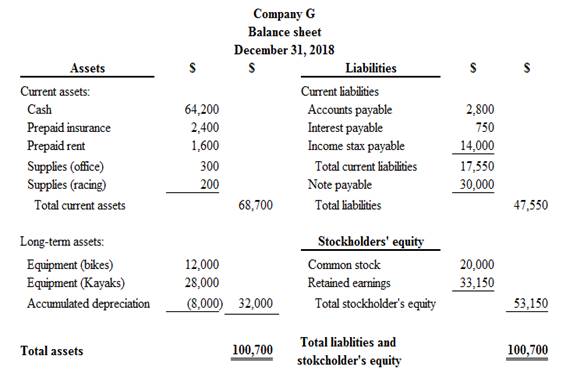

Classified balance sheet:

Classified balance sheet of Company G is as follows:

Figure (1)

Therefore, the total assets of Company G are $100,700, and the total liabilities and stockholders’ equity are $100,700.

Requirement – 6

To record: The necessary closing entries of Company G.

Explanation of Solution

Closing entries:

Closing entries are those journal entries, which are passed to transfer the final balances of temporary accounts, (all revenues account, all expenses account and dividend) to the retained earnings. Closing entries produce a zero balance in each temporary account.

Closing entries of Company G is as follows:

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| 2018 | Service revenue (Clinic) | 52,900 | ||

| December 31 | Service revenue (Racing) | 20,000 | ||

| Retained earnings | 72,900 | |||

| (To close all revenue account) | ||||

| 2018 | Retained earnings | 37,750 | ||

| December 31 | Advertising expense | 1,000 | ||

| Depreciation expense | 8,000 | |||

| Income tax expense | 14,000 | |||

| Insurance expense | 2,400 | |||

| Interest expense | 750 | |||

| Legal fees expense | 1,500 | |||

| Miscellaneous expense | 1,200 | |||

| Rent expense | 800 | |||

| Salaries expense | 2,000 | |||

| Supplies expense (office) | 1,500 | |||

| Supplies expense (Racing) | 2,600 | |||

| (To close all the expenses account) | ||||

| 2018 | Retained earnings | 4,000 | ||

| December 31 | Dividends | 4,000 | ||

| (To close the dividends account) | ||||

Table (6)

Requirement – 7

To post: The closing entries to the T-accounts.

Explanation of Solution

| Service Revenue (Clinic) | |

| 2,000 | |

| 2,300 | |

| 7,000 | |

| 10,500 | |

| 13,200 | |

| 52,900 | 17,900 |

| 0 | |

| Service Revenue (Racing) | |

| 20,000 | 20,000 |

| 0 | |

| Legal Fees Expense | |

| 1,500 | 1,500 |

| 0 | |

| Advertising Expense | |

| 300 | |

| 700 | 1,000 |

| 0 | |

| Rent Expense | |

| 800 | 800 |

| 0 | |

| Salaries Expense | |

| 2,000 | 2,000 |

| 0 | |

| Depreciation Expense | |

| 8,000 | 8,000 |

| 0 | |

| Insurance Expense | |

| 2,400 | 2,400 |

| 0 | |

| Supplies Expense (Office) | |

| 1,500 | 1,500 |

| 0 | |

| Supplies Expense (Racing) | |

| 2,600 | 2,600 |

| 0 | |

| Interest Expense | |

| 750 | 0 |

| 750 | |

| Income Tax Expense | |

| 14,000 | 14,000 |

| 0 | |

| Miscellaneous Expense | |

| 1,200 | 1,200 |

| 0 | |

| Dividends | |

| 4,000 | 4,000 |

| 0 | |

| Retained Earnings | |

| 35,750 | 72,900 |

| 4,000 | |

| 33,150 | |

Requirement – 8

To prepare: A post-closing trial balance of Company G.

Explanation of Solution

Post-closing trial balance:

The post-closing trial balance is a summary of all ledger accounts, and it shows the debit and the credit balances after the closing entries are journalized and posted. The post-closing trial balance contains only permanent (balance sheet) accounts, and the debit and the credit balances of permanent accounts should agree.

Post-closing trial balance of Company G is as follows:

| Company G | ||

| Post-closing Trial Balance | ||

| For the year ended December 31, 2018 | ||

| Accounts | Debit ($) | Credit ($) |

| Cash | $64,200 | |

| Prepaid Insurance | 2,400 | |

| Prepaid Rent | 1,600 | |

| Supplies (Office) | 300 | |

| Supplies (Racing) | 200 | |

| Equipment (Bikes) | 12,000 | |

| Equipment (Kayaks) | 28,000 | |

| Accumulated Depreciation | $8,000 | |

| Accounts Payable | 2,800 | |

| Income Tax Payable | 14,000 | |

| Interest Payable | 750 | |

| Notes Payable | 30,000 | |

| Common Stock | 20,000 | |

| Retained Earnings | 33,150 | |

| Total | $108,700 | $108,700 |

Table (7)

Therefore, the total of debit, and credit columns of post-closing trial balance is $108,700 and agree.

Want to see more full solutions like this?

Chapter 3 Solutions

FINANCIAL ACCOUNTING W/ACCESS >CI<

- On October 1, 2019, Jay Pryor established an interior decorating business, Pioneer Designs. During the month, Jay completed the following transactions related to the business: Oct. 1. Jay transferred cash from a personal bank account to an account to be used for the business, 18,000. 4.Paid rent for period of October 4 to end of month, 3,000. 10.Purchased a used truck for 23,750, paying 3,750 cash and giving a note payable for the remainder. 13.Purchased equipment on account, 10,500. 14.Purchased supplies for cash, 2,100. 15.Paid annual premiums on property and casualty insurance, 3,600. 15.Received cash for job completed, 8,950. Enter the following transactions on Page 2 of the two-column journal: 21.Paid creditor a portion of the amount owed for equipment purchased on October 13, 2,000. 24.Recorded jobs completed on account and sent invoices to customers, 14,150. 26.Received an invoice for truck expenses, to be paid in November, 700. 27.Paid utilities expense, 2,240. 27.Paid miscellaneous expenses, 1,100. Oct. 29. Received cash from customers on account, 7,600. 30.Paid wages of employees, 4,800. 31.Withdrew cash for personal use, 3,500. Instructions 1. Journalize each transaction in a two-column journal beginning on Page 1, referring to the following chart of accounts in selecting the accounts to be debited and credited. (Do not insert the account numbers in the journal at this time.) Journal entry explanations may be omitted. 2. Post the journal to a ledger of four-column accounts, inserting appropriate posting references as each item is posted. Extend the balances to the appropriate balance columns after each transaction is posted. 3. Prepare an unadjusted trial balance for Pioneer Designs as of October 31, 2019. 4. Determine the excess of revenues over expenses for October. 5. Can you think of any reason why the amount determined in (4) might not be the net income for October?arrow_forwardNicole has decided that she is going to start her business, Nicole’s Getaway Spa (NGS). A lot hasto be done when starting a new business. Here are some transactions that have occurred prior toApril 30.a. Received $80,000 cash when issuing 8,000 new common shares.b. Purchased land by paying $2,000 cash and signing a note payable for $7,000 due in threeyears.c. Hired a new aesthetician for a salary of $1,000 a month, starting next month.d. NGS purchased a company car for $18,000 cash (list price of $21,000) to assist in runningerrands for the business.e. Bought and received $1,000 in supplies for the spa on credit.f. Paid $350 of the amount owed in ( e ).g. Nicole sold 100 of her own personal shares to Raea Gooding for $300.Required:1. For each of the events, prepare journal entries if a transaction exists, checking that debitsequal credits. If a transaction does not exist, explain why there is no transaction.2. Assuming that the beginning balances in each of the accounts are zero,…arrow_forwardHye Jin started his accounting consultancy business on January 1, 2021. During the first month of the business, the following transactions occurred: Hye Jin purchased a laptop on January 1, 2021 for P50,000. 30% of the purchase price was paid in cash, the balance was subject to a 2-year note at 3% interest. Vera expects that the laptop will be used in the business for 3 years. On January 5, Vera received P12,000 for services to be rendered on the succeeding 4 months. On January 3, Vera purchased a 1-year insurance policy for P24,000. Office supplies purchased cost P15,000. A count of supplies at month-end indicates P12,000 supplies are on hand. On January 31, Hye Jin received a bill from the lessor for January rent amounting to P16,000, and utilities amounting to P4,000. Services performed to clients but were not yet billed amounted to P7,850. REQUIRED (show supporting calculations):1. Prepare the adjusting entries on January 31 if the company makes use of the…arrow_forward

- Alex and Hagi decided to open a home cleaning service company, H@L .,. The following information is a partial list of transactions from H@L Inc.January 1- Alex and Hagi each donated $ 25.000 in exchange for common stock to start the business.March 3- H@L Inc., paid $ 3.000 cash for a two-year insurance policy that was effective immediately.March 15-The Company purchased $8.000 of supplies on account.April 5- The Company purchased some cleaning equipment for $10.000 cash. The equipment should last for five years with no residual value. H@L company will take a full year of depreciation in 2020.May 1-H@L Inc., purchased a year’s worth of advertising in a local newspaper for $ 1.200 cash.September 1- The Company obtained a nine-month loan for $ 15.000 at 5% from Do Not Trust Bank, with interest and principal payable on June 2021.December 31- The Company paid $ 5.000 of accounts payable owed from transaction 3.December 31- The Company earned service revenues of $ 26.225, of which $23.225…arrow_forwardAlex and Hagi decided to open a home cleaning service company, H@L .,. The following information is a partial list of transactions from H@L Inc.January 1- Alex and Hagi each donated $ 25.000 in exchange for common stock to start the business.March 3- H@L Inc., paid $ 3.000 cash for a two-year insurance policy that was effective immediately.March 15-The Company purchased $8.000 of supplies on account.April 5- The Company purchased some cleaning equipment for $10.000 cash. The equipment should last for five years with no residual value. H@L company will take a full year of depreciation in 2020.May 1-H@L Inc., purchased a year’s worth of advertising in a local newspaper for $ 1.200 cash.September 1- The Company obtained a nine-month loan for $ 15.000 at 5% from Do Not Trust Bank, with interest and principal payable on June 2021.December 31- The Company paid $ 5.000 of accounts payable owed from transaction 3.December 31- The Company earned service revenues of $ 26.225, of which $23.225…arrow_forwardAlex and Hagi decided to open a home cleaning service company, H@L .,. The following information is a partial list of transactions from H@L Inc.January 1- Alex and Hagi each donated $ 25.000 in exchange for common stock to start the business.March 3- H@L Inc., paid $ 3.000 cash for a two-year insurance policy that was effective immediately.March 15-The Company purchased $8.000 of supplies on account.April 5- The Company purchased some cleaning equipment for $10.000 cash. The equipment should last for five years with no residual value. H@L company will take a full year of depreciation in 2020.May 1-H@L Inc., purchased a year’s worth of advertising in a local newspaper for $ 1.200 cash. September 1- The Company obtained a nine-month loan for $ 15.000 at 5% from Do Not Trust Bank, with interest and principal payable on June 2021.December 31- The Company paid $ 5.000 of accounts payable owed from transaction 3.December 31- The Company earned service revenues of $ 26.225, of which $23.225…arrow_forward

- Ms. Ang put up an accounting firm on Nov. 1, 2021. The registered name of the business is "Ang Accounting Firm." The following were the transactions during the months of November and December, 2021. 1. The owner provided ₱300,000 cash as initial investment to the business on December 1, 2021. 2. Obtained a 12%, one year, bank loan for ₱50,000 on November 1, 2021. Principal and interest are due at maturity date. 3. On December 1, 2021, She purchased office supplies worth ₱60,000 for cash during the period. (the firm uses asset method). 4. The business acquired computer equipment for ₱150,000 cash on November 1, 2021, which has a useful life of 5 years with a residual value of ₱30,000. 5. On December 1, 2021, the business took one year insurance for ₱42,000 covering the months of December, 2021 to February, 2022. The business uses expense method in recording this transaction. 6. As of December 31, 2021, rendered services billed to clients are worth ₱280,000 for cash and ₱200,000 on…arrow_forwardHow do you record these on a journal entry? -Purchases liability insurance for its business starting in February at $12,000 for the year. Note all $12,000 is paid immediately -Purchases a $30,000 equity stake (investment) in a start-up company -Orca Company prepares its January adjusting and closing entries (performed together in class on 2/7)arrow_forwardMary Maywood opened Maywood Cleaners on March 1, 2022. During March, the following transactions were completed.Mar.1 Shareholders invested €25,000 cash in the business in exchange for ordinary shares.Mar.1 Borrowed €7,000 cash by signing a 6-month, 8%, €7,000 note payable. Interest will be paid the first day of each subsequent month.Mar.1 Purchased used truck for €9,000 cash.Mar.2 Paid €2,500 cash to cover rent from March 1 through May 31.Mar.3 Paid €3,400 cash on a 6-month insurance policy effective March 1.Mar.6 Purchased cleaning supplies for €2,000 on account.Mar.14 Billed customers €4,700 for cleaning services performed.Mar.18 Paid €700 on amount owed on cleaning supplies.Mar.20 Paid €1,750 cash for employee salaries.Mar.21 Collected €1,800 cash from customers billed on March 14.Mar.28 Billed customers €4,500 for cleaning services performed.Mar.31 Paid €450 for gas and oil used in truck during month (use Maintenance and RepairsExpense).Mar.31 Declared and paid a €1000 cash…arrow_forward

- Mary Maywood opened Maywood Cleaners on March 1, 2022. During March, the following transactions were completed.Mar.1 Shareholders invested €25,000 cash in the business in exchange for ordinary shares.Mar.1 Borrowed €7,000 cash by signing a 6-month, 8%, €7,000 note payable. Interest will be paid the first day of each subsequent month.Mar.1 Purchased used truck for €9,000 cash.Mar.2 Paid €2,500 cash to cover rent from March 1 through May 31.Mar.3 Paid €3,400 cash on a 6-month insurance policy effective March 1.Mar.6 Purchased cleaning supplies for €2,000 on account.Mar.14 Billed customers €4,700 for cleaning services performed.Mar.18 Paid €700 on amount owed on cleaning supplies.Mar.20 Paid €1,750 cash for employee salaries.Mar.21 Collected €1,800 cash from customers billed on March 14.Mar.28 Billed customers €4,500 for cleaning services performed.Mar.31 Paid €450 for gas and oil used in truck during month (use Maintenance and RepairsExpense).Mar.31 Declared and paid a €1000 cash…arrow_forwardHyun Bin started his accounting consultancy business on January 1, 2021. During the first month of the business, the following transactions occurred: Hyun Bin purchased a laptop on January 1, 2021 for ₱50,000. 30% of the purchase price was paid in cash, the balance was subject to a 2-year note at 3% interest. Vera expects that the laptop will be used in the business for 3 years. On January 5, Vera received ₱12,000 for services to be rendered on the succeeding 4 months. On January 3, Vera purchased a 1-year insurance policy for ₱24,000. Office supplies purchased cost ₱15,000. A count of supplies at month-end indicates ₱12,000 supplies are on hand. On January 31, Hyun Bin received a bill from the lessor for January rent amounting to ₱16,000, and utilities amounting to ₱4,000. Services performed to clients but were not yet billed amounted to ₱7,850. REQUIRED (show supporting calculations):1. Prepare the adjusting entries on January 31 if the company makes use of the…arrow_forwardjohn began an Upholstery cleaning business on October 1,2020 and engaged in the following transactions during the month: Began business by depositing 12,000 in a Clean & Premium ltd bank oct 1 : account oct 2 :Ordered Cleaning supplies 3,000 oct 3: Purchased cleaning equipment for 2,800. oct 4 : Made two months' van lease payment in advance, 1,200 Received the cleaning supplies ordered on (Oct 2) oct 7: and agreed to pay half the amount in 10 days, and the rest in 30 days oct 9: Paid for repairs on the van with cash, 1,080 oct 12 : Received cash for cleaning upholstery, 960. oct 17: Paid half the amount owed on supplies purchased on Oct 7, 1,500. oct 21 : Billed customers for cleaning upholstery, 1,340 oct 24 :Paid cash for additional repairs on the van, RM80 oct 27 : Received 600 from the customers billed on October 21. oct 31 Made a cash withdrawal of 700. you are Required to A : Prepare the general journal based on the above transactions. B:…arrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning