Concept explainers

Videos

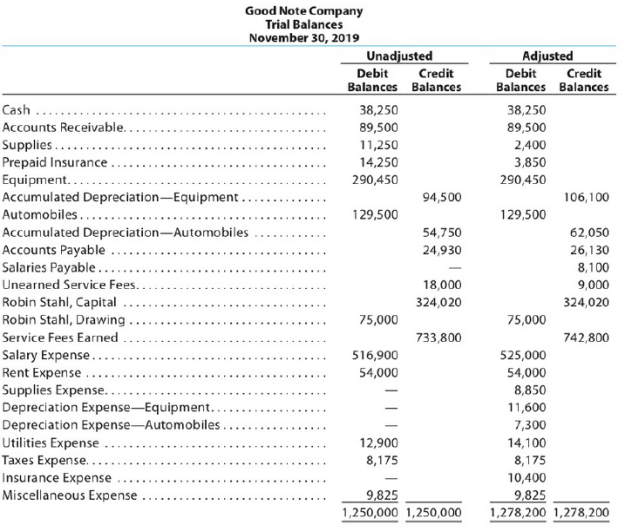

Good Note Company specializes in the repair of music equipment and is owned and operated by Robin Stahl. On November 30, 2019, the end of the current year, the accountant for Good Note prepared the following

Instructions

Journalize the seven entries that adjusted the accounts at November 30. None of the accounts were affected by more than one adjusting entry.

Adjusting entries:

Adjusting entries refers to the entries that are made at the end of an accounting period in accordance with revenue recognition principle, and expenses recognition principle. All adjusting entries affect at least one income statement account (revenue or expense), and one balance sheet account (asset or liability).

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

Ø Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

Ø Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

To prepare: The adjusting entries in the books of Company GN at the end of the year.

Answer to Problem 3.4APR

An adjusting entry for Supplies expenses:

In this case, Company GN recognized the supplies expenses at the end of the year. So, the necessary adjusting entry that the Company GN should record to recognize the supplies expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Supplies expenses (1) | 8,850 | |||

| November | 30 | Supplies | 8,850 | ||

| (To record the supplies expenses incurred at the end of the year) | |||||

Table (1)

Explanation of Solution

Working note:

Calculate the value of supplies expense

Explanation:

- Supplies expense decreases the value of owner’s equity by $8,850; hence debit the supplies expenses for $8,850.

- Supplies are an asset, and it decreases the value of asset by $8,850, hence credit the supplies for $8,850.

An adjusting entry for insurance expenses:

In this case, Company GN recognized the insurance expenses at the end of the year. So, the necessary adjusting entry that the Company GN should record to recognize the prepaid expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Insurance expenses (2) | 10,400 | |||

| November | 30 | Prepaid insurance | 10,400 | ||

| (To record the insurance expenses incurred at the end of the year) | |||||

Table (2)

Working note:

Calculate the value of insurance expense

Explanation:

- Insurance expense decreases the value of owner’s equity by $10,400; hence debit the insurance expenses for $10,400.

- Prepaid insurance is an asset, and it decreases the value of asset by $10,400, hence credit the prepaid insurance for $10,400.

An adjusting entry for depreciation expenses-Equipment:

In this case, Company GN recognized the depreciation expenses on equipment at the end of the year. So, the necessary adjusting entry that the Company GN should record to recognize the accrued expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Depreciation expenses –Equipment (3) | 11,600 | |||

| November | 30 | Accumulated depreciation-Equipment | 11,600 | ||

| (To record the depreciation expenses incurred at the end of the year) | |||||

Table (3)

Working note:

Calculate the value of depreciation expense-Equipment

Explanation:

- Depreciation expense decreases the value of owner’s equity by $11,600; hence debit the depreciation expenses for $11,600.

- Accumulated depreciation is a contra-asset account, and it decreases the value of asset by $11,600, hence credit the accumulated depreciation for $11,600.

An adjusting entry for depreciation expenses-Automobiles:

In this case, Company GN recognized the depreciation expenses on automobiles at the end of the year. So, the necessary adjusting entry that the Company GN should record to recognize the accrued expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Depreciation expenses –Automobiles (4) | 7,300 | |||

| November | 30 | Accumulated depreciation-Automobiles | 7,300 | ||

| (To record the depreciation expenses incurred at the end of the year) | |||||

Table (4)

Working note:

Calculate the value of depreciation expense-Automobiles

Explanation:

- Depreciation expense decreases the value of owner’s equity by $7,300; hence debit the depreciation expenses for $7,300.

- Accumulated depreciation is a contra-asset account, and it decreases the value of asset by $7,300, hence credit the accumulated depreciation for $7,300.

An adjusting entry for utilities expenses:

In this case, Company GN recognized the utilities expenses at the end of the year. So, the necessary adjusting entry that the Company GN should record to recognize the accrued expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Utilities expenses (5) | 1,200 | |||

| November | 30 | Accounts payable | 1,200 | ||

| (To record the utilities expenses incurred at the end of the year) | |||||

Table (5)

Working note:

Calculate the value of utilities expense

Explanation:

- Utilities expense decreases the value of owner’s equity by $1,200; hence debit the utilities expenses for $1,200.

- Accounts payable is a liability, and it increases the value of liability by $1,200, hence credit the accounts payable for $1,200.

An adjusting entry for salaries expenses:

In this case, Company GN recognized the salaries expenses at the end of the year. So, the necessary adjusting entry that the Company GN should record to recognize the accrued expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Salaries expenses (6) | 8,100 | |||

| November | 30 | Salaries payable | 8,100 | ||

| (To record the salaries expenses incurred at the end of the year) | |||||

Table (6)

Working note:

Calculate the value of salaries expense

Explanation:

- Salaries expense decreases the value of owner’s equity by $8,100; hence debit the salaries expenses for $8,100.

- Salaries payable is a liability, and it increases the value of liability by $8,100, hence credit the salaries payable for $8,100.

An adjusting entry for unearned service fees:

In this case, Company GN received cash in advance before the service provided to customer. So, the necessary adjusting entry that the Company GN should record for the unearned fees revenue at the end of the year is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2019 | Unearned service fees | 9,000 | |||

| November | 30 | Service fees earned (7) | 9,000 | ||

| (To record the unearned service fees at the end of the year) | |||||

Table (7)

Working note:

Calculate the value of service fees earned

Explanation:

- Unearned service fees are a liability, and it decreases the value of liability by $9,000, hence debit the unearned service fees for $9,000.

- Service fees earned increases owner’s equity by $9,000; hence credit the service fees earned for $9,000.

Want to see more full solutions like this?

Chapter 3 Solutions

CENGAGENOW 6 TERMS ACCESS CARD 27TH ED.

- Wig Creations Company supplies wigs and hair care products to beauty salons throughout Texas and the Southwest. The accounts receivable clerk for Wig Creations prepared the following partially completed aging of receivables schedule as of the end of business on December 31, 20Y1: The following accounts were unintentionally omitted from the aging schedule: Wig Creations has a past history of uncollectible accounts by age category, as follows: Instructions 1. Determine the number of days past due for each of the preceding accounts. 2. Complete the aging of receivables schedule by adding the omitted accounts to the bottom of the schedule and updating the totals. 3. Estimate the allowance for doubtful accounts, based on the aging of receivables schedule. 4. Assume that the allowance for doubtful accounts for Wig Creations has a credit balance of 7,375 before adjustment on December 31, 20Y1. Journalize the adjustment for uncollectible accounts. 5. Assuming that the adjusting entry in (4) was inadvertently omitted, how would the omission affect the balance sheet and income statement?arrow_forwardGood Note Company specializes in the repair of music equipment and is owned and operated by Robin Stahl. On November 30, 2019, the end of the current year, the accountant for Good Note prepared the following trial balances: Instructions Journalize the seven entries that adjusted the accounts at November 30. None of the accounts were affected by more than one adjusting entry.arrow_forwardMarcellus Purse conduct cleaning business on the credit basis. He provides the collects the sccount receivable in 60 days. The Allowance October 2019 is $3,993. The following information is available Douchd D 1. The business uses aging of account receivable method to count the bad de 2. The accountant is required to update the balance of allowance of dosud des OURE at the end of each month 3. On 5 October 2019 a total of $1.997 ewed by Lucy Frone has been deemed w uncollectable and therefore written off 4. The total sales recorded during 1 October 2019 to 31 October 2019 is $812577 The balance in the Account receivable on 31 October 2019 is $198.300 5. 6. On 31 October 2019 the accountant estimates that 3% of the account receivable is estimated as doubtful. Q3 Required (a) Prepare the Accounting Entries for the transactions or events relating to bad debt for the month ended 31 October 2019, ignore GST ( (b) Prepare and balance the T-account for Allowance for Doubtful Debts accounts as…arrow_forward

- At the end of the year, Dahir Incorporated’s balance of Allowance for Uncollectible Accounts is $1,500 (credit) before adjustment. The company estimates future uncollectible accounts to be $7,500. What adjusting entry would Dahir record for Allowance for Uncollectible Accounts? (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field.)arrow_forwardOn December 31, 2019, Mason Company made following proper year-end adjusting entries: 1. Prepare journal entries to record whatever reversing entries you think appropriate. 2. Explain your reasoning for each reversing entry.arrow_forwardAt the beginning of the year, the balance in Allowance for Doubtful Accounts is a credit of $766. During the year, previously written off accounts of $138 are reinstated and accounts totaling $741 are written off as uncollectible. The end-of-year balance (before adjustment) in Allowance for Doubtful Accounts should be a.$741 b.$766 c.$138 d.$163arrow_forward

- At the end of the year, Mercy Cosmetics’ balance of Allowance for Uncollectible Accounts is $420 (credit) before adjustment. The balance of Accounts Receivable is $16,000. The company estimates that 10% of accounts will not be collected over the next year. What adjusting entry would Mercy Cosmetics record for Allowance for Uncollectible Accounts? (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field.)arrow_forwardAt the beginning of the year, the balance in Allowance for Doubtful Accounts is a credit of $780. During the year, previously written off accounts of $119 are reinstated and accounts totaling $744 are written off as uncollectible. The end-of-year balance (before adjustment) in Allowance for Doubtful Accounts should be Oa. $780 © b. $744 O c. $119 Od. $155arrow_forwardRecord (write out in proper journal entry format) each of the adjusting entries. Post each of these adjusting entries to the correct T-accounts. Adjusting & other entries: A) December 31: The company has not recorded bad debt expense for 2025. Sinfully uses the Aging of Receivables approach and estimates that the ending balance in the Allowance for Bad Debts should be $9,300. B) December 31: The long term note payable was recorded on August 1, 2025. The interest and the note are due on July 31, 2030. Interest rate is 9.5%. Record 2025 interest expense.arrow_forward

- As of Sene 30 1994, the end of the current fiscal year, the accountant for Abay General Trading completed the worksheet before journalizing and posting the adjustments. Required: (a) Compare the adjusted and unadjusted trial balances and prepare the eight journal entries that were required to adjust the accounts. (b) Prepare the journal entries that were required to close temporary accounts. Abay General Trading Trial Balance Sene 30, 1994 Un adjusted Adjusted Cash 12,825.00 12,825.00 Supplies 8,950.00 3,635.00 Prepaid rent 19,500.00 1,500.00 Prepaid insurance 3,750.00 1,250.00 Equipment 92,150.00 92,150.00 Accumulated depreciation equipment 53,480.00 66,270.00 Automobile 56,500.00 56,500.00 Accumulated depreciation automobile 28,250.00 36,900.00 Accounts payable 8,310.00 8,730.00 Salary payable 3,400.00…arrow_forwardSunshine and Rainbows Resort had the following balances at December 31, 2025, before the year-end adjustments: View the balances. The aging of accounts receivable yields the following data: View the accounts receivable aging schedule. Requirements 1. Journalize Sunshine and Rainbows Resort's entry to record bad debts expense for 2025 using the aging-of-receivables method. 2. Prepare a T-account to compute the ending balance of Allowance for Bad Debts. Requirement 1. Journalize Sunshine and Rainbows Resort's entry to record bad debts expense for 2025 using the aging-of-receivables method. (Record debits first, then credits. Select the explanation on the last line of the journal entry table.) Dec. Date 31 Accounts and Explanation Debit Credit Balances - ☑ Accounts Receivable Aging Schedule Age of Accounts Receivable 0-60 Days Over 60 Days Total Receivables Accounts Receivable 75,000 $ 3,000 $ 78,000 Estimated percent uncollectible × 4% * 24% - ☑ Accounts Receivable Allowance for Bad…arrow_forwardAt the end of the year, Dahir Incorporated’s balance of Allowance for Uncollectible Accounts is $1,900 (credit) before adjustment. The company estimates future uncollectible accounts to be $9,500. What adjustment would Dahir record for Allowance for Uncollectible Accounts? (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field.)arrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning