Videos

Judgment Case 3–5

• LO3–2 through LO3–4

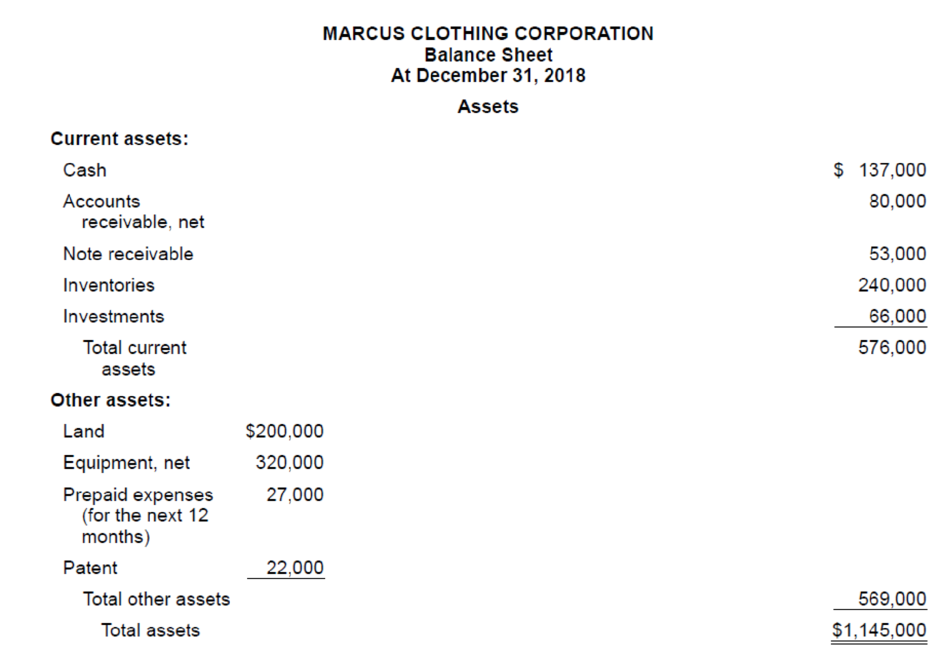

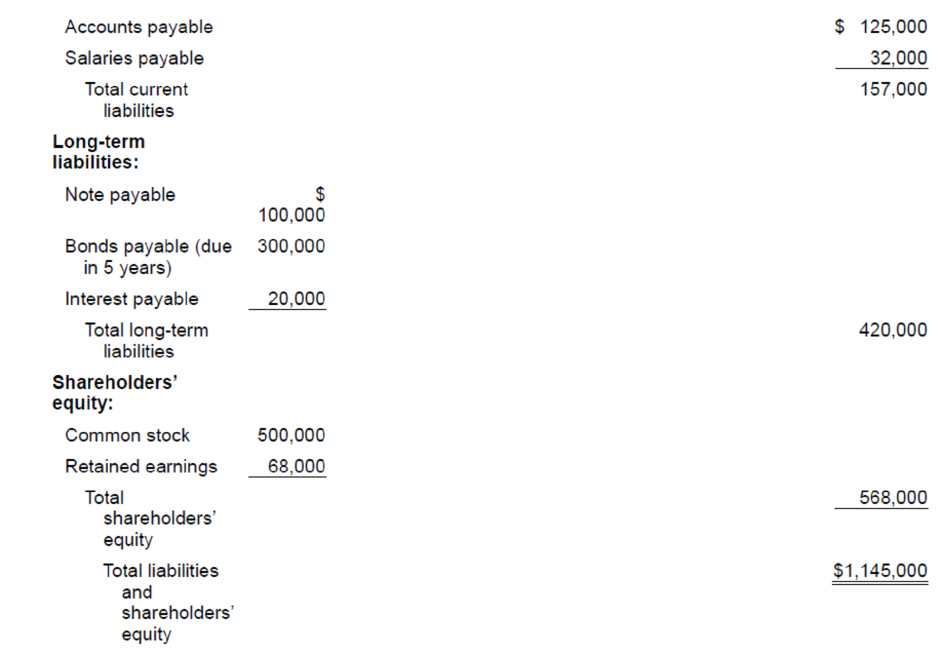

You recently joined the internal auditing department of Marcus Clothing Corporation. As one of your first assignments, you are examining a balance sheet prepared by a staff accountant.

In the course of your examination you uncover the following information pertaining to the balance sheet:

1. The company rents its facilities. The land that appears in the statement is being held for future sale.

2. The note receivable is due in 2020. The balance of $53,000 includes $3,000 of accrued interest. The next interest payment is due in July 2019.

3. The note payable is due in installments of $20,000 per year. Interest on both the notes and bonds is payable annually.

4. The company’s investments consist of marketable equity securities of other corporations. Management does not intend to liquidate any investments in the coming year.

Required:

Identify and explain the deficiencies in the statement prepared by the company’s accountant. Include in your answer items that require additional disclosure, either on the face of the statement or in a note.

Want to see the full answer?

Check out a sample textbook solution

Chapter 3 Solutions

INTERMEDIATE ACCOUNTING RMU 9TH EDITION

- PROBLEM 1 – Problem 2 Audit of CashYour examination of the financial statements of MAGDALO Group Co. for the year ended December 31, 2007 youobtained the following information on the checking account of the company:a. The bank statement on November 30, 2007 showed a balance of P15,300.b. Among the bank credits in November was a customer’s note for P5,000 collected for the account of thecompany which the company recognized in December among its receipts.c. Included in the bank debits in November was a cost of checkbooks amounting to P60.d. A check for P2,000 issued by MAGULO Group Co. in November was charged by the bank in error againstMAGDALO Group Co. account.e. You also ascertained that there were deposits in transit amounting to P4,000 and outstanding checkstotaling P8,500 as of November 30, 2007.f. The bank statement for the month of December showed total credits of P20,800 and total charges ofP10,200.g. Company books for December showed total receipts of P36,780 and disbursements…arrow_forwardH6. Question 15 During an audit, you are selecting a sample of transactions from the vouchers payable register at the end of the period and tracing them to underlying documents. By doing this, you are gathering evidence primarily to support that: Incurred obligations were recorded in the correct period Recorded obligations were paid Recorded obligations occurred prior to year-end 1 pts Cash disbursements were recorded as incurred obligation Please show all step by step calculationarrow_forwardquestion 40 A client has a separate sales group for its largest preferred customers, a select group of customers who normally make purchases in excess of $250,000 and often have balances of over $1,000,000. Whcih of the following audit procedures would the auditor most likely perform? Prepare a schedule of purchases and payments for these customers. Send out negative confirmations on a large sample of these customers. Inquire of the sales manager regarding accounts receivable items. Send out positive confirmations on a large sample of these customers.arrow_forward

- PART 2: Audit Practice Cases/Problems PROBLEM 1-A: CASH COUNT You were assigned to render a cash count of Tindig The count was rendered on the morning of January 4 instead of exactly at the Balance sheet date December 31. The custodian presented to you the following: Currencies and coins 1. A disbursement check payable to the custodian An officer's personal check accommodated by the fund Officer's check marked NSF Petty cash expense vouchers: 12/20 Transportation 12/24 Office repairs 12/27 Miscellaneous 1/3 Office supplies Corporation's petty cash fund with an imprest balance of P40,000. Unused postage stamps An enveloped marked "collections for charity" with list of names and corresponding amounts contributed. There is no money inside the envelope. What is the petty cash shortage, if there are any? a 3,860 b. 1,360 C. d. 3,360 2,860 10,940 15,600 4,000 2,000 1,500 900 2,100 1,600 500 2,500arrow_forwardISA 300 Planning an Audit of Financial Statements provides guidance to auditors. Planning an audit involves establishing the overall audit strategy for the engagement and developing an audit plan. Adequate planning benefits the audit of financial statements in several ways.Required:Identify and explain the five stages in audit process. Discuss three importance of audit planning. b) You are the audit senior in charge of the audit of Malaika Company and have been informed by your audit manager that during the year a fraud occurred at the client. A payroll clerk set up fictitious employees and the wages were paid into the clerk’s own bank account. This clerk has subsequently left the company, but the audit manager is concerned that additional frauds have taken place in the wages department.Required:i) Describe six procedures which should be undertaken during the audit of wages as a result of the manager’s assessment of the increased risk of fraud.arrow_forwardQues 18 In the course of your audit of Rollins and Gordon, Ltd., you discover that the company recorded its office building purchase in a land account and, therefore, does not depreciate it. The land account makes up about 10 percent of the total assets of the firm. Num Type of Audit Opinion Num Other Modifications to add to the Audit Opinion A Adverse 1 Emphasis of matter paragraph B Disclaimer 2 Other matter paragraph C Qualified 3 Basis for modification other than additional paragraph D Unmodified/Unqualified 4 Make modification other than additional paragraph 5 Make no modificationarrow_forward

- Question 8 Which 3 statements are correct regarding reconciling a bank account in QuickBooks Online? To begin the reconcile process, you need to enter the statement ending date and ending balance from the relevant bank statement Reconciliations must only be run at period end to estimate tax owed The primary admin can undo reconciliations Transactions added or matched in the Banking center are automatically marked tentatively cleared To view the reconciliation report, select History by account Bank accounts can be reconciled only if they are connected through bank feedsarrow_forwardBER 2021 CONFIDENTIALEAB31103_Audit 2 Page 9 of 10Question 5Nurin, Aliah & Co has audited Kinokuyi Publishing Sdn Bhd (KPSB) for several years. Auditdocumentation, including internal control flowcharts as well as sales and cash receipts system,purchasing and payables system and payroll system notes, are accessible from the previousyear's file. You are the audit supervisor of Nurin, Aliah & Co, and you are evaluating thepaperwork documenting KPSB’s purchasing and payables system in preparation for theinterim and final audits for the fiscal year ending 31 December 2021. The company is a bookretailer with twelve locations across the Klang Valley and a central warehouse located in ShahAlam which holds the majority of the company's inventory. Below is an excerpt from theexisting systems notes:Store managers are in charge of placing book orders for their store. Store managers arecurrently unable to request books from any of the other eleven locations. Customers who wantto order books…arrow_forwardQ1 The following are specific balance-related audit objectives applied to the audit of accounts receivable (a. through h.) and management assertions about account balances (1 through 4). The list referred to in the specific balance-related audit objectives is the list of the accounts receivable from each customer at the balance sheet date. Specific Balance-Related Audit Objective a . There are no unrecorded receivables. b . Receivables have not been sold or discounted. c . Uncollectible accounts have been provided for. d . Receivables that have become uncollectible have been written off. e . All accounts on the list are expected to be collected within 1 year. f . The total of the amounts on the accounts receivable listing agrees with the general ledger balance for accounts receivable. g . All accounts on the list arose from the normal course of business and are not due from related parties. h . Sales cutoff at year-end is proper. Management Assertion about Account Balances 1 .…arrow_forward

- Q1 The following are specific balance-related audit objectives applied to the audit of accounts receivable (a. through h.) and management assertions about account balances (1 through 4). The list referred to in the specific balance-related audit objectives is the list of the accounts receivable from each customer at the balance sheet date. Specific Balance-Related Audit Objective a . There are no unrecorded receivables. b . Receivables have not been sold or discounted. c . Uncollectible accounts have been provided for. d . Receivables that have become uncollectible have been written off. e . All accounts on the list are expected to be collected within 1 year. f . The total of the amounts on the accounts receivable listing agrees with the general ledger balance for accounts receivable. g . All accounts on the list arose from the normal course of business and are not due from related parties. h . Sales cutoff at year-end is proper. ----------------- Management Assertion about…arrow_forwardCornerstone Exercise 4-18 Adjusting Entry from Bank Reconciliation A customer of Mutare paid for merchandise originally purchased on account with a check that has been erroneously entered into Mutares cash account for $570 (it actually has been issued and paid for $750). Required: Record the appropriate journal entry to correct the error.arrow_forwardQuestion 4 of 20 Which type of source document is best for providing evidence of disbursements of funds from petty cash? A. A bank statement B. A lockbox check image C. A credit card receipt D. A supplier invoice SUBMIT E PREVIOUS % &arrow_forward

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning Corporate Financial AccountingAccountingISBN:9781337398169Author:Carl Warren, Jeff JonesPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781337398169Author:Carl Warren, Jeff JonesPublisher:Cengage Learning