Concept explainers

Videos

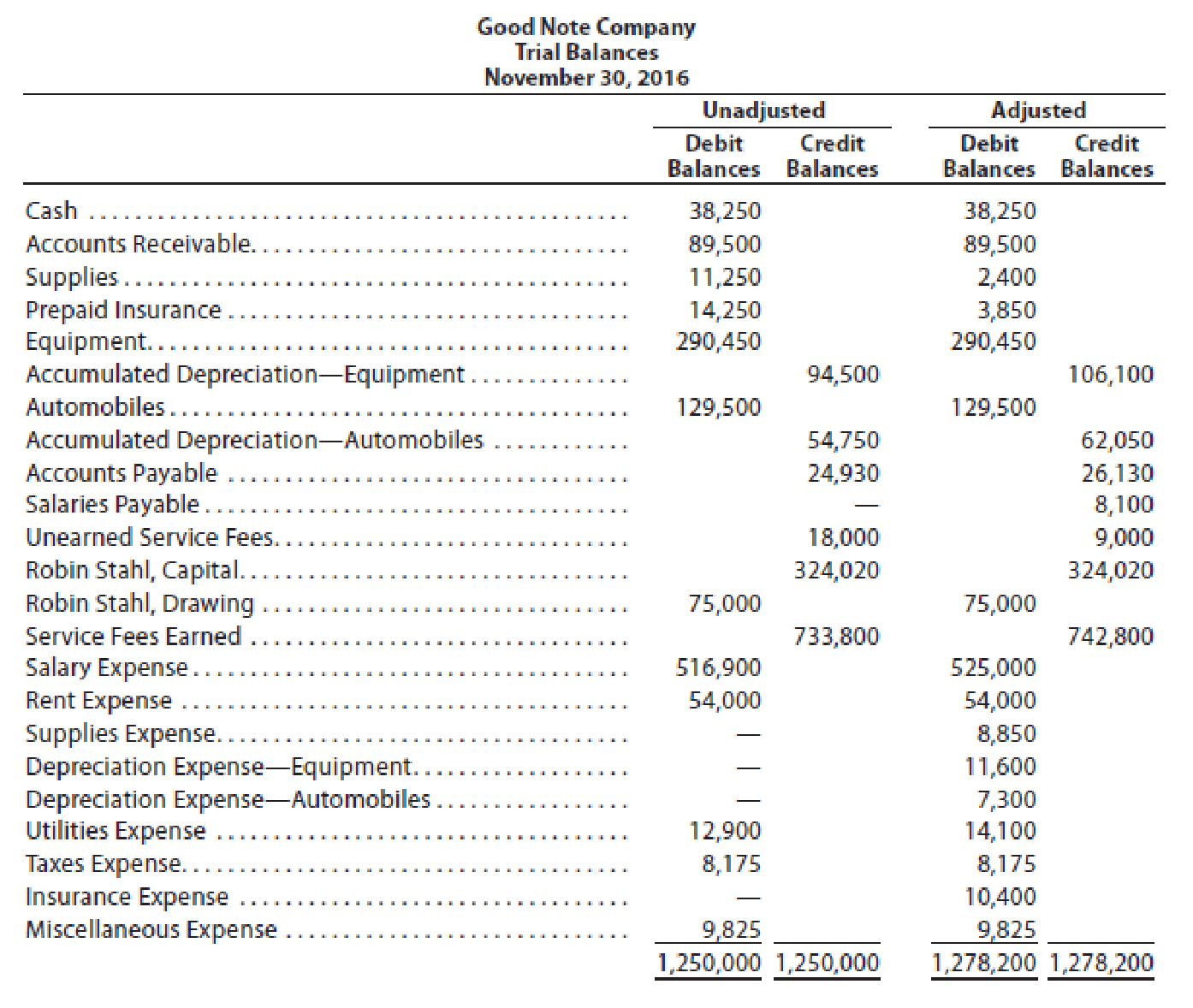

Good Note Company specializes in the repair of music equipment and is owned and operated by Robin Stahl. On November 30, 2016, the end of the current year, the accountant for Good Note Company prepared the following

Instructions

Journalize the seven entries that adjusted the accounts at November 30. None of the accounts were affected by more than one

Prepare the adjusting entries in the books of Company GN at the end of the year.

Explanation of Solution

Adjusting entries: Adjusting entries refers to the entries that are made at the end of an accounting period in accordance with revenue recognition principle, and expenses recognition principle. All adjusting entries affect at least one income statement account (revenue or expense), and one balance sheet account (asset or liability).

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

An adjusting entry for Supplies expenses:

In this case, Company GN recognized the supplies expenses at the end of the year. So, the necessary adjusting entry that the Company GN should record to recognize the supplies expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2016 | Supplies expenses (1) | 8,850 | |||

| November | 30 | Supplies | 8,850 | ||

| (To record the supplies expenses incurred at the end of the year) | |||||

Table (1)

- Supplies expense decreases the value of owner’s equity by $8,850; hence debit the supplies expenses for $8,850.

- Supplies are an asset, and it decreases the value of asset by $8,850, hence credit the supplies for $8,850.

Working note (1):

Calculate the value of supplies expense.

An adjusting entry for insurance expenses:

In this case, Company GN recognized the insurance expenses at the end of the year. So, the necessary adjusting entry that the Company GN should record to recognize the prepaid expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2016 | Insurance expenses (2) | 10,400 | |||

| November | 30 | Prepaid insurance | 10,400 | ||

| (To record the insurance expenses incurred at the end of the year) | |||||

Table (2)

- Insurance expense decreases the value of owner’s equity by $10,400; hence debit the insurance expenses for $10,400.

- Prepaid insurance is an asset, and it decreases the value of asset by $10,400, hence credit the prepaid insurance for $10,400.

Working note (2):

Calculate the value of insurance expense.

An adjusting entry for depreciation expenses-Equipment:

In this case, Company GN recognized the depreciation expenses on equipment at the end of the year. So, the necessary adjusting entry that the Company GN should record to recognize the accrued expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2016 | Depreciation expenses –Equipment (3) | 11,600 | |||

| November | 30 | Accumulated depreciation-Equipment | 11,600 | ||

| (To record the depreciation expenses incurred at the end of the year) | |||||

Table (3)

- Depreciation expense decreases the value of owner’s equity by $11,600; hence debit the depreciation expenses for $11,600.

- Accumulated depreciation is a contra-asset account, and it decreases the value of asset by $11,600, hence credit the accumulated depreciation for $11,600.

Working note (3):

Calculate the value of depreciation expense-Equipment.

An adjusting entry for depreciation expenses-Automobiles:

In this case, Company GN recognized the depreciation expenses on automobiles at the end of the year. So, the necessary adjusting entry that the Company GN should record to recognize the accrued expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2016 | Depreciation expenses –Automobiles (4) | 7,300 | |||

| November | 30 | Accumulated depreciation-Automobiles | 7,300 | ||

| (To record the depreciation expenses incurred at the end of the year) | |||||

Table (4)

- Depreciation expense decreases the value of owner’s equity by $7,300; hence debit the depreciation expenses for $7,300.

- Accumulated depreciation is a contra-asset account, and it decreases the value of asset by $7,300, hence credit the accumulated depreciation for $7,300.

Working note (4):

Calculate the value of depreciation expense-Automobiles.

An adjusting entry for utilities expenses:

In this case, Company GN recognized the utilities expenses at the end of the year. So, the necessary adjusting entry that the Company GN should record to recognize the accrued expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2016 | Utilities expenses (5) | 1,200 | |||

| November | 30 | Accounts payable | 1,200 | ||

| (To record the utilities expenses incurred at the end of the year) | |||||

Table (5)

- Utilities expense decreases the value of owner’s equity by $1,200; hence debit the utilities expenses for $1,200.

- Accounts payable is a liability, and it increases the value of liability by $1,200, hence credit the accounts payable for $1,200.

Working note (5):

Calculate the value of utilities expense.

An adjusting entry for salaries expenses:

In this case, Company GN recognized the salaries expenses at the end of the year. So, the necessary adjusting entry that the Company GN should record to recognize the accrued expense is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2016 | Salaries expenses (6) | 8,100 | |||

| November | 30 | Salaries payable | 8,100 | ||

| (To record the salaries expenses incurred at the end of the year) | |||||

Table (6)

- Salaries expense decreases the value of owner’s equity by $8,100; hence debit the salaries expenses for $8,100.

- Salaries payable is a liability, and it increases the value of liability by $8,100, hence credit the salaries payable for $8,100.

Working note (6):

Calculate the value of salaries expense.

An adjusting entry for unearned service fees:

In this case, Company GN received cash in advance before the service provided to customer. So, the necessary adjusting entry that the Company GN should record for the unearned fees revenue at the end of the year is as follows:

| Date | Description |

Post Ref. | Debit ($) | Credit ($) | |

| 2016 | Unearned service fees | 9,000 | |||

| November | 30 | Service fees earned (7) | 9,000 | ||

| (To record the unearned service fees at the end of the year) | |||||

Table (7)

- Unearned service fees are a liability, and it decreases the value of liability by $9,000, hence debit the unearned service fees for $9,000.

- Service fees earned increases owner’s equity by $9,000; hence credit the service fees earned for $9,000.

Working note (7):

Calculate the value of service fees earned.

Want to see more full solutions like this?

Chapter 3 Solutions

Bundle: Financial Accounting, Loose-Leaf Version, 14th + CengageNOWv2, 1 term Printed Access Card (2)

- Good Note Company specializes in the repair of music equipment and is owned and operated by Robin Stahl. On November 30, 2019, the end of the current year, the accountant for Good Note prepared the following trial balances: Instructions Journalize the seven entries that adjusted the accounts at November 30. None of the accounts were affected by more than one adjusting entry.arrow_forwardThe Signage Company specializes in the maintenance and repair of signs, such as billboards. On March 31, 2016, the accountant for The Signage Company prepared the following trial balances: Instructions Journalize the seven entries that adjusted the accounts at March 31. None of the accounts were affected by more than one adjusting entry.arrow_forwardThe trial balance of Wikki Cleaners at December 31, 2012, the end of the current fiscal year, is as follows: Information for the adjusting entries is as follows: a. Cleaning supplies on hand on December 31, 2012, 18,750. b. Insurance premiums expired during the year, 1,800. c. Depreciation on equipment during the year, 21,600. d. Wages accrued but not paid at December 31, 2012, 1,830. Suppose you discover that an assistant in your department had misunderstood your instructions and had provided you with the wrong information on two of the adjusting entries. Cleaning supplies consumed during the year should have been 18,750, and insurance premiums unexpired at year-end were 1,800. Make the corrections on your worksheet and save the corrected file as F1WORK4. Reprint the worksheet.arrow_forward

- Reece Financial Services Co., which specializes in appliance repair services, is owned and operated by Joni Reece. Reece Financial Services Co.s accounting clerk prepared the following unadjusted trial balance at July 31, 2016: The data needed to determine year-end adjustments are as follows: a. Depreciation of building for the year, 6,400. b. Depreciation of equipment for the year, 2,800. c. Accrued salaries and wages at July 31, 900. d. Unexpired insurance at July 31, 1,500. e. Fees earned but unbilled on July 31, 10,200. f. Supplies on hand at July 31, 615. g. Rent unearned at July 31, 300. Instructions 1. Journalize the adjusting entries using the following additional accounts: Salaries and Wages Payable; Rent Revenue; Insurance Expense; Depreciation ExpenseBuilding; Depreciation ExpenseEquipment; and Supplies Expense. 2. Determine the balances of the accounts affected by the adjusting entries and preparean adjusted trial balance.arrow_forwardThe trial balance of Wikki Cleaners at December 31, 2012, the end of the current fiscal year, is as follows: Information for the adjusting entries is as follows: a. Cleaning supplies on hand on December 31, 2012, 18,750. b. Insurance premiums expired during the year, 1,800. c. Depreciation on equipment during the year, 21,600. d. Wages accrued but not paid at December 31, 2012, 1,830. As the accountant for Wikki Cleaners, you have been asked to prepare financial statements for the year. A file called F1WORK has been provided to assist you in this assignment. As you review this file, it should be noted that columns H and I will automatically change when you enter values in columns E or G.arrow_forwardIn addition to those accounts listed on the trial balance, the chart of accounts for McGee Company also contains the following accounts and account numbers: No. 158 Accumulated Depreciation—Equipment, No. 212 Salaries and Wages Payable, No. 631 Supplies Expense, No. 711 Depreciation Expense, No. 722 Insurance Expense, and No. 732 Utilities Expense.Other data:1. Supplies on hand at June 30 are $750.2. A utility bill for $150 has not been recorded and will not be paid until next month.3. The insurance policy is for a year.4. $2,800 of unearned service revenue has been earned at the end of the month.5. Salaries of $1,900 are accrued at June 30.6. The equipment has a 5-year life with no salvage value. It is being depreciated at $250 per month for 60 months.7. Invoices representing $1,200 of services performed during the month have not been recorded as of June 30.Instructions(a) Prepare the adjusting entries for the month of June. Use J3 as the page number for your journal.(b) Post the…arrow_forward

- In August, JemCo, which has an October 31 year end, pays $1,200 for office supplies and records it in Supplies Expense. On October 31, a physical count reveals $440 of supplies unused. What adjusting entry must JemCo record on October 31? If this entry is not recorded, how will it affect JemCo’s financial statements?arrow_forwardCesar Mahusay operates an accounting firm. Shown below are selected accounts that appear in the Preliminary Trial Balance as of Dec. 31, 2018, and require adjustment. ACCOUNTS RECEIVABLE P 22,500 ALLOWANCE FOR DOUBTFUL ACCOUNTS 1,200 NOTES RECEIVABLE 20,000 OFFICE EQUIPMENT 92,000 ACCUMULATED DEPRECIATION 4,500 RENTAL INCOME 12,000 SERVICE INCOME 450,000 SUPPLIES EXPENSE 6,250 INSURANCE EXPENSE 7,200 SALARIES EXPENSE 120,000 The following adjustments are to be made: Unused office supplies at the end, P 320 One year insurance was paid on April 1 of the current year Office equipment has a useful life of 10 years with a salvage value of P 2,000. It was acquired in July 2018. Unearned rental income is 1/3 of the amount collected Service income not yet collected P 3,000 The 60 days 6% note was received on Dec.1 Estimated Bad Debts is 10 % of the Accounts…arrow_forwardarty Wagon, Inc., provides musical entertainment at weddings, dances, and various other functions. The company performs adjusting entries monthly, but prepares closing entries annually on December 31. The company recently hired Jack Armstrong as its new accountant. Jack’s first assignment was to prepare an income statement, a statement of retained earnings, and a balance sheet using an adjusted trial balance given to him by his predecessor, dated December 31, current year.From the adjusted trial balance, Jack prepared the following set of financial statements. Required: a. Prepare a corrected set of financial statements dated December 31, current year. (You may assume that all of the figures in the company’s adjusted trial balance were reported correctly except for Interest Payable of $240, which was mistakenly omitted in the financial statements prepared by Jack.) b. Prepare the necessary year-end closing entries. c. Using the financial statements prepared in part a, briefly…arrow_forward

- Olney Cleaning Company had the following items that require adjustment at year end. For one cleaning contract, $11,100 cash was received in advance. The cash was credited to Unearned Service Revenue upon receipt. At year end, $260 of the service revenue was still unearned. For another cleaning contract, $8,700 cash was received in advance and credited to Unearned Service Revenue upon receipt. At year end, $3,000 of the services had been provided. Required: 1. Prepare the adjusting journal entries needed at December 31. If an amount box does not require an entry, leave it blank. Dec. 31 Unearned Service Revenue fill in the blank 02e1a8f7d03afe9_2 fill in the blank 02e1a8f7d03afe9_3 Service Revenue fill in the blank 02e1a8f7d03afe9_5 fill in the blank 02e1a8f7d03afe9_6 Dec. 31 Unearned Service Revenue fill in the blank 02e1a8f7d03afe9_8 fill in the blank 02e1a8f7d03afe9_9 Service Revenue fill in the blank 02e1a8f7d03afe9_11 fill in the blank 02e1a8f7d03afe9_12…arrow_forwardIn November Craig received $225 from Kate Whelan as a customer prepayment for design work. Craig recorded the entire $225 as Design Income. At the end of the accounting period to Kate, so the $225 had not been earned as of year end. Since it had not been earned, the $225 is a liability because Craig has an obligation to provide the design service or return the $225 to the customer. So an adjusting entry is needed to bring accounts up to date at December 31.arrow_forwardTunstall, Inc., a small service company, keeps its records without the help of an accountant. After much effort, an outside accountant prepared the following unadjusted trial balance as of the end of the annual accounting period on December 31:arrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning