Managerial Accounting

16th Edition

ISBN: 9781259995484

Author: Ray Garrison

Publisher: MCGRAW-HILL HIGHER EDUCATION

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 3, Problem 6E

EXERCISE 3-6 Schedules of Cost of Goods Manufactured and Cost of Goods Sold; Income Statement LO3-3

The following data from the just completed year are taken from the accounting records of Mason Company:

Required;

- Prepare a schedule of cost of goods manufactured. Assume all raw materials used in production were direct materials.

- Prepare a schedule of cost of goods sold. Assume that the company's underapplied or overapplied

overhead is closed to Cost of Goods Sold. - Prepare an income statement.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

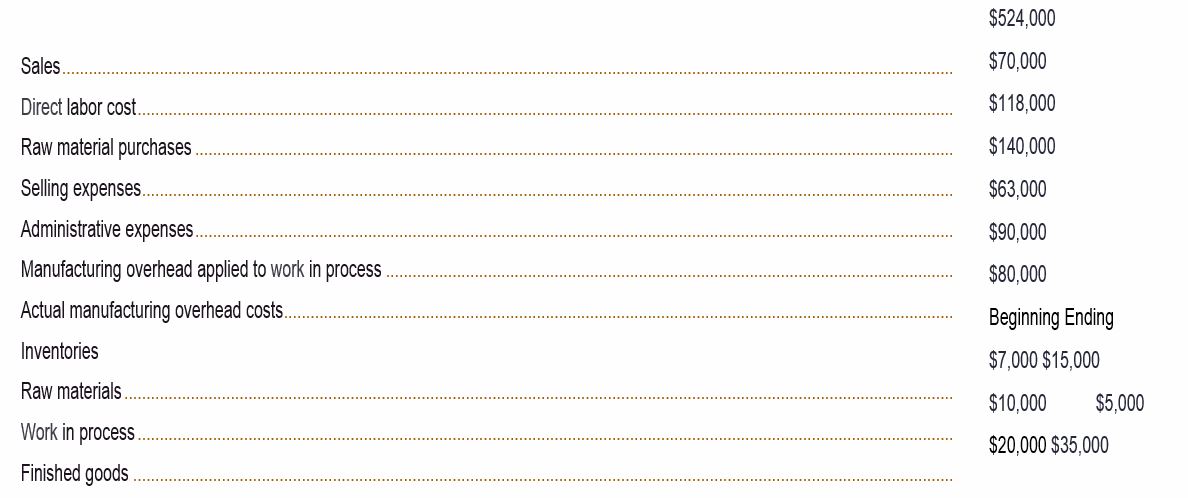

Exercise 3-6 (Static) Schedules of Cost of Goods Manufactured and Cost of Goods Sold; Income Statement [LO3-3]

The following data from the just completed year are taken from the accounting records of Mason Company:

Sales

$ 524,000

Direct labor cost

$ 70,000

Raw material purchases

$ 118,000

Selling expenses

$ 140,000

Administrative expenses

$ 63,000

Manufacturing overhead applied to work in process

$ 90,000

Actual manufacturing overhead costs

$ 80,000

Inventories

Beginning

Ending

Raw materials

$ 7,000

$ 15,000

Work in process

$ 10,000

$ 5,000

Finished goods

$ 20,000

$ 35,000

Required:

1. Prepare a schedule of cost of goods manufactured. Assume all raw materials used in production were direct materials.

2. Prepare a schedule of cost of goods sold. Assume that the company's underapplied or overapplied overhead is closed to Cost of Goods Sold.

3. Prepare an income statement.

Problem 3-13 (Algo) Schedules of Cost of Goods Manufactured and Cost of Goods Sold; Income Statement [LO3-3]

Superior Company provided the following data for the year ended December 31 (all raw materials are used in production as direct materials):

Selling expenses

$ 214,000

Purchases of raw materials

$ 268,000

Direct labor

?

Administrative expenses

$ 159,000

Manufacturing overhead applied to work in process

$ 373,000

Actual manufacturing overhead cost

$ 355,000

Inventory balances at the beginning and end of the year were as follows:

Beginning

Ending

Raw materials

$ 54,000

$ 40,000

Work in process

?

$ 24,000

Finished goods

$ 39,000

?

The total manufacturing costs added to production for the year were $670,000; the cost of goods available for sale totaled $730,000; the unadjusted cost of goods sold totaled $669,000; and the net operating income was $33,000. The company’s underapplied or overapplied overhead is closed to Cost of Goods Sold.…

PROBLEM 2-27 Schedule of Cost of Goods Manufactured; Income Statement; Cost Behavior[LO1, LO2, LO3, LO4, LO5]The following selected account balances for the year ended December 31 are provided for ValenkoCompany

Advertising expense . . . . . . . . . . . . . . . . . . $215,000Insurance, factory equipment. . . . . . . . . . . . $8,000Depreciation, sales equipment. . . . . . . . . . . $40,000Rent, factory building . . . . . . . . . . . . . . . . . . $90,000Utilities, factory. . . . . . . . . . . . . . . . . . . . . . . $52,000Sales commissions . . . . . . . . . . . . . . . . . . . $35,000Cleaning supplies, factory . . . . . . . . . . . . . . $6,000Depreciation, factory equipment . . . . . . . . . $110,000Selling and administrative salaries. . . . . . . . $85,000Maintenance, factory . . . . . . . . . . . . . . . . . . $74,000Direct labor. . . . . . . . . . . . . . . . . . . . . . . . . . ?Purchases of raw materials . . . . . . . . . . . . . $260,000

Inventory balances at the beginning and…

Chapter 3 Solutions

Managerial Accounting

Ch. 3.A - EXERCISE 3A-1 Transaction Analysis LO3-5 Carmen...Ch. 3.A - EXERCISE 3A-2 Transaction Analysis LO3-5 Adams...Ch. 3.A - EXERCISE 3A-3 Transaction Analysis LO3-5 Dixon...Ch. 3.A - PROBLEM 3A-4 Transaction Analysis LO3-5 Morrison...Ch. 3.A - PROBLEM 3A-5 Transaction Analysis LO3-5 Star...Ch. 3.A -

PROBLEM 3A-6 Transaction Analysis LO3-5

Brooks...Ch. 3 - Prob. 1QCh. 3 - Prob. 2QCh. 3 - What is underapplied overhead Overapplied...Ch. 3 - 3-4 Provide two reasons why overhead might be...

Ch. 3 - Prob. 5QCh. 3 - How do you compute the raw materials used in...Ch. 3 - Prob. 7QCh. 3 - How do you compute the cost of goods manufactured?Ch. 3 - Prob. 9QCh. 3 - Prob. 10QCh. 3 - Prob. 1AECh. 3 - Prob. 2AECh. 3 - Prob. 3AECh. 3 - Prob. 4AECh. 3 - Prob. 1F15Ch. 3 - Prob. 2F15Ch. 3 - Bunnell Corporation is a manufacturer that uses...Ch. 3 - Prob. 4F15Ch. 3 - Prob. 5F15Ch. 3 - Bunnell Corporation is a manufacturer that uses...Ch. 3 - Prob. 7F15Ch. 3 - Prob. 8F15Ch. 3 - Prob. 9F15Ch. 3 - Prob. 10F15Ch. 3 - Bunnell Corporation is a manufacturer that uses...Ch. 3 - Prob. 12F15Ch. 3 - Prob. 13F15Ch. 3 - Prob. 14F15Ch. 3 - Prob. 15F15Ch. 3 - EXERCISE 3-1 Prepare Journal Entries LO3-1 Lamed...Ch. 3 - Prob. 2ECh. 3 - EXERCISE 3-3 Schedules of Cost of Goods...Ch. 3 - EXERCISE 3-4 Underapplied and Overapplied Overhead...Ch. 3 - Prob. 5ECh. 3 - EXERCISE 3-6 Schedules of Cost of Goods...Ch. 3 - (

$

15,000...Ch. 3 - EXERCISE 3-8 Applying Overhead: Journal Entries;...Ch. 3 - Prob. 9ECh. 3 - Prob. 10ECh. 3 -

PROBLEM 3-11: T-Account Analysis of Cost Flows...Ch. 3 - Prob. 12PCh. 3 - PROBLEM 3-13 Schedules of Cost of Goods...Ch. 3 - Prob. 14PCh. 3 -

PROBLEM 3-15 Journal Entries; T-Accounts;...Ch. 3 - Prob. 16PCh. 3 - Prob. 17PCh. 3 - Prob. 18C

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Construct and interpret a product profitability report, allocating selling and administrative expenses Naper Inc. manufactures power equipment. Naper has two primary productsgenerators and air compressors. The following report was prepared by the controller for Napers senior marketing management for the year ended December 31: Generators Air Compressors Total Revenue 4,200,000 3,000,000 7,200,000 Cost of goods sold 2,940,000 2,100,000 5,040,000 Gross profit 1,260,000 900,000 2,160,000 Selling and administrative expenses 610,000 Income from operations 1,550,000 The marketing management team was concerned that the selling and administrative expenses were not traced to the products. Marketing management believed that some products consumed larger amounts of selling and administrative expense than did other products. To verify this, the controller was asked to prepare a complete product profitability report, using activity-based costing. The controller determined that selling and administrative expenses consisted of two activities: sales order processing and post-sale customer service. The controller was able to determine the activity base and activity rate for each activity, as follows: Activity Activity Base Activity Rate Sales order processing Sales orders 65 per sales order Post-sale customer service Service requests 200 per customer service request The controller determined the following activity-base usage information about each product: Generators Air Compressors Number of sales orders 3,000 4,000 Number of service requests 225 550 A. Determine the activity cost of each product for sales order processing and post-sale customer service activities. B. Use the information in (A) to prepare a complete product profitability report dated for the year ended December 31. Compute the gross profit to sales and the income from operations to sales percentages for each product. (Round to two decimal places.) C. Interpret the product profitability report. How should management respond to the report?arrow_forwardBrief Exercise 3-32 Absorption-Costing Income Statement Refer to the data for Beyta Company above. Required: 1. Calculate the cost of goods sold under absorption costing. 2. Prepare an income statement using absorption costing. Use the following information for Brief Exercises 3-32 and 3-33: During the most recent year, Beyta Company had the following data:arrow_forwardProblem 2. Statement of Costs of Goods Manufactured and Income statement. The following information are gathered from the accounting records of Genet Inc. for the current month: Inventory information Beginning balance $ Ending balance $ Raw materials inventory $46,800 $43,600 Work-in-Process inventory $33,400 $35,700 Finished goods inventory $42,500 $31,800 Other information $ Revenue $800,000 Purchase of raw materials $72,100 Indirect materials costs $5,600 Indirect labor costs $20,000 Office staff salaries $28,000 Office equipment depreciation $2,000 Factory machinery maintenance costs $5,000 Environmental compliance costs - factory $1,200 Direct labor - Wages of production line workers $32,000 Sales staff salaries $12,000 Advertising costs $8,000 Miscellaneous manufacturing overhead costs $11,000 Required: a.…arrow_forward

- Exercise 2: Flow of Cost - Cost System You are required to compute for the unknowns in the following accounts: Materials Inventory 7,950 Purchase Returns 750 Purchases 27,500 Direct Materials ? Indirect Materials (e) Inventory, end 5,100 Work in Process Inventory 13,650 Cost of Goods Sold Completed (c) Direct Materials Cost 23,500 Direct Labor Cost (a) Factory Overhead Applied (100% of direct labor cost) (b) Inventory 11,750 62,150 Finished Goods Inventory 12,500 Cost of Goods Sold (d) Cost of Goods Sold Completed ? Inventory, end 11,250arrow_forwardEXERCISE 3-12 Applying Overhead; Cost of Goods Manufactured [LO3-2, L03-6, LO3-7] The following cost data relate to the manufacturing activities of Chang Company during the just completed year: $ 15,000 130,000 8,000 70,000 240,000 10,000 $473,000 Manufacturing overhead costs incurred: Indirect materials ....... Indirect labor Property taxes, factory ...... Utilities, factory Depreciation, factory ....... Insurance, factory ......... ........... ......... Total actual manufacturing overhead costs incurred ........ Other costs incurred: Purchases of raw materials (both direct and indirect) Direct labor cost ... Inventories: Raw materials, beginning ....... Raw materials, ending ....... Work in process, beginning ...... Work in process, ending ...... $400,000 $60,000 $20,000 $30,000 $40,000 $70,000 The company uses a predetermined overhead rate to apply overhead cost to jobs. The rate for the year was $25 per machine-hour. A total of 19,400 machine-hours was recorded for the year.…arrow_forwardQuestion 1. Case 2. Book problem. Incomplete manufacturing costs, expenses and selling data for two different cases are shown below: Required: 1. Indicate the missing amount for each letter 2. Prepare a schedule of cost of goods manufactured 3. Prepare a schedule of cost of goods sold 4. Prepare an income statement (Optional) Case 1 Case 2 Raw materials used 9,600 g) Direct labor cost 5,000 8,000 Total Factory overhead 8,000 4,000 Total Manufacturing costs a) 16,000 Beginning work in process inventory 1,000 h) Ending work in process inventory b) 3,000 Sales revenue 24,500 i)…arrow_forward

- Exercise 2-27 Statement of comprehensive Income and schedule of cost of goods manufactured. The Howell Corporation has the following account balances (all in millions): For Specific Date Direct Materials, January 01, 2019 $18 Work in process, January 01, 2019 12 Finished Goods, January 01, 2019 84 Direct Materials, December 31, 2019 24 Work in Process, December 31, 2019 6 Finished Goods, December 31, 2019 66 For the Year 2019 Purchased of Direct Materials $390 Direct Manufacturing Labour 120 Depreciation, - Plant, Building, and Equipment 96 Plant Supervisory Salaries 6 Miscellaneous Plant Overhead 42 Revenues 1140 Marketing, Distribution and Customer Service Cost 288 Plant Supplies Used 12 Plant Utilities 36 Indirect Manufacturing Labour 72 Required: Prepare a statement of Comprehensive Income and a supporting schedule of goods manufactured for…arrow_forwardQuestion 3- Part 1 The following data is provided for Garcon Company and Pepper Company. Garcon Company Pepper Company Beginning finished goods inventory $ 12,000 $ 16,450 Beginning work in process inventory 14,500 19,950 Beginning raw materials inventory 7,250 9,000 Rental cost on factory equipment 27,000 22,750 Direct labor 19,000 35,000 Ending finished goods inventory 17,650 13,300 Ending work in process inventory 22,000 16,000 Ending raw materials inventory 5,300 7,200 Factory utilities 9,000 12,000 Factory supplies used 8,200 3,200 General and administrative expenses 21,000 43,000 Indirect labor 1,250 7,660 Repairs—Factory equipment 4,780 1,500 Raw materials purchases 33,000 52,000 Selling expenses 50,000 46,000 Sales 195,030 290,010 Cash 20,000…arrow_forwardQUESTION 1: Schedule of Cost of Goods Manufactured: Income Statement. Richmond Chocolates Limited, a manufacturing Company, produces a single product. The following information has been taken from the company’s production, sales and cost records for the year ended December 31, 2021. Sales $ 450,000 Indirect Labour 12,000 Utilities 15,000 Direct Labour 70,000 Depreciation, factory equipment 21,000 Raw materials purchased 165,000 Depreciation, sales equipment 18,000 Insurance expired during the year 4,000 Rent on facilities 50,000 Selling and administrative salaries 32,000 Advertising 75,000 Additional information about the company follows: Some 60 percent of the utilities costs and 75 percent of the expired insurance apply to factory operations. The remaining amounts apply to selling and administrative activities Only 80 percent of the rent on facilities apply to factory operations: the remainder applies to…arrow_forward

- QUESTION 1: Schedule of Cost of Goods Manufactured: Income Statement. Richmond Chocolates Limited, a manufacturing Company, produces a single product. The following information has been taken from the company’s production, sales and cost records for the year ended December 31, 2021. Sales $ 450,000 Indirect Labour 12,000 Utilities 15,000 Direct Labour 70,000 Depreciation, factory equipment 21,000 Raw materials purchased 165,000 Depreciation, sales equipment 18,000 Insurance expired during the year 4,000 Rent on facilities 50,000 Selling and administrative salaries 32,000 Advertising 75,000 Additional information about the company follows: Some 60 percent of the utilities costs and 75 percent of the expired insurance apply to factory operations. The remaining amounts apply to selling and administrative activities Only 80 percent of the rent on facilities apply to factory operations: the remainder applies to…arrow_forwardQUESTION 1: Schedule of Cost of Goods Manufactured: Income Statement. Richmond Chocolates Limited, a manufacturing Company, produces a single product. The following information has been taken from the company’s production, sales and cost records for the year ended December 31, 2021. Sales $ 450,000 Indirect Labour 12,000 Utilities 15,000 Direct Labour 70,000 Depreciation, factory equipment 21,000 Raw materials purchased 165,000 Depreciation, sales equipment 18,000 Insurance expired during the year 4,000 Rent on facilities 50,000 Selling and administrative salaries 32,000 Advertising 75,000 Additional information about the company follows: Some 60 percent of the utilities costs and 75 percent of the expired insurance apply to factory operations. The remaining amounts apply to selling and administrative activities Only 80 percent of the rent on facilities apply to factory operations: the remainder…arrow_forwardManufacturing income statement, statement of cost of goods Obj. 3 manufactured Several items are omitted from the income statement and cost of goods manufactured statement data for two different companies for the month of May: Instructions 1. For both companies, determine the amounts of the missing items (a) through (f), identifying them by letter. 2. Prepare Yakima Company’s statement of cost of goods manufactured for May. 3. Prepare Yakima Company’s income statement for May.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Individual Income Taxes

Accounting

ISBN:9780357109731

Author:Hoffman

Publisher:CENGAGE LEARNING - CONSIGNMENT

Financial & Managerial Accounting

Accounting

ISBN:9781285866307

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Financial & Managerial Accounting

Accounting

ISBN:9781337119207

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

The KEY to Understanding Financial Statements; Author: Accounting Stuff;https://www.youtube.com/watch?v=_F6a0ddbjtI;License: Standard Youtube License