Concept explainers

Videos

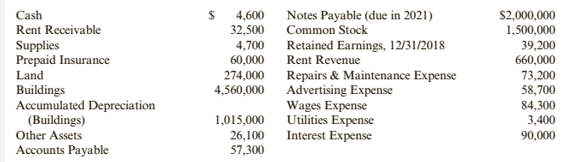

Problem 3-71 A Preparing a Worksheet (Appendix 3A)

Marsteller Properties Inc. owns apartments that it rents to university students. At December 31,

2019, the following unadjusted account balances were available:

The following information is available for

- An analysis of apartment rental contracts indicates that S3,800 of apartment rent is unbilled and unrecorded at year end.

- A physical count Of supplies reveals that $1,400 of supplies are on hand at December 31 , 2019.

- Annual

depreciation on the buildings is $204,250. - An examination of insurance policies indicates that $12,000 Of the prepaid insurance applies to coverage for 2019.

- Six months' interest at 9% is unrecorded and unpaid on the notes payable.

1.

To prepare: Worksheet of the company A.

Introduction:.Worksheet is a statement that represents the unadjusted balances of ledgers, adjustment entries and the balances after such adjustments. Adjusted balances are the final balances that are presented in the financial statements of a company.

Explanation of Solution

Preparation of worksheet for the period ending 31st December, 2019:

| Account Title | UnadjustedTrial balance | Adjustments | AdjustedTrial balance | |||||

| Dr. | Cr. | Dr. | Cr. | Dr. | Cr. | |||

| Cash | 4,600 | 4,600 | ||||||

| Rent receivable | 32,500 | 3,800 | 36,300 | |||||

| Supplies | 4,700 | 3,300 | 1,400 | |||||

| Prepaid insurance | 60,000 | 12,000 | 48,000 | |||||

| Land | 274,000 | 274,000 | ||||||

| Building | 4,560,000 | 4,560,000 | ||||||

| Accumulated depriciation-building | 1,015,000 | 204,250 | 1,219,250 | |||||

| Other assets | 26,100 | 26,100 | ||||||

| Accounts payable | 57,300 | 57,300 | ||||||

| Interest payable | 90,000 | 90,000 | ||||||

| Notes payable | 2,000,000 | 2,000,000 | ||||||

| Common stock | 1,500,000 | 1,500,000 | ||||||

| Retained earnings opening | 39,200 | 39,200 | ||||||

| Rent revenue | 660,000 | 3,800 | 663,800 | |||||

| Repair and maintenance expense | 73,200 | 73,200 | ||||||

| Advertising expense | 58,700 | 58,700 | ||||||

| Wages expense | 84,300 | 84,300 | ||||||

| Utilities expense | 3,400 | 3,400 | ||||||

| Interest expense | 90,000 | 90,000 | 180,000 | |||||

| Supplies expense | 3,300 | 3,300 | ||||||

| Depreciation expense | 204,250 | 204,250 | ||||||

| Insurance expense | 12,000 | 12,000 | ||||||

| Total | 5,271,500 | 5,271,500 | 313,350 | 313,350 | 5,569,550 | 5,569,550 | ||

Table (1)

2.

To prepare: Income statement, statement of retained earnings and balance sheet.

Introduction: Income statement, statement of retained earnings and balance sheet are financial statements. These statements are prepared for reporting purposes.

Explanation of Solution

Preparation of income statement for the Year ending 31st December, 2019:

| CompanyA | |||||

| Income Statement,For the Year ending on 31stDecember, 2019 | |||||

| Amount ($) | Amount ($) | ||||

| Revenues: | |||||

| Rent revenue | 663,800 | ||||

| Total Revenue | 663,800 | ||||

| Expenses: | |||||

| Repair and maintenance expense | 73,200 | ||||

| Advertising expense | 58,700 | ||||

| Wages Expense | 84,300 | ||||

| Utilities Expense | 3,400 | ||||

| Insurance Expense | 12,000 | ||||

| Interest Expense | 180,000 | ||||

| Supplies expense | 3,300 | ||||

| Depreciation expense | 204,250 | ||||

| Total Expenses | 619,150 | ||||

| Net Income | 44,650 | ||||

Table (2)

Preparation of balance sheet as on 31st December, 2019:

| Company A | ||

| Balance Sheet as on 31stDecember 2019 | ||

| Amount ($) | Amount($) | |

| Liabilities and Owners Equity | ||

| Current Liabilities | ||

| Accounts Payable | 57,300 | |

| Interest Payable | 90,000 | |

| Total Current Liabilities | 147,300 | |

| Non-Current Liabilities | ||

| Note Payable | 2,000,000 | |

| Total Non-Current Liabilities | 2,000,000 | |

| Total Liabilities | ||

| Common Stock | 1,500,000 | |

| Retained Earnings | 83,850 | 1,583,850 |

| Total Liabilities and Owner’s Equity | 3,731,150 | |

| Current Assets | ||

| Cash | 4,600 | |

| Rent Receivable | 36,300 | |

| Supplies | 1,400 | |

| Prepaid insurance | 48,000 | |

| Other Assets | 26,100 | |

| Total Current Assets | 116,400 | |

| Property, Plant and Equipment | ||

| Land | 274,000 | |

| Building | 4,560,000 | |

| Less: accumulated depreciation | ||

| Total Property, Plant and Equipment | 3,614,750 | |

| Total Assets | 3,731,150 | |

Table (3)

Preparation of statement of retained earnings as on 31st December, 2019:

| Company A | ||

| Statement of Retained Earning | ||

| Amount($) | Amount($) | |

| Owner’s Equity opening balance | 39,200 | |

| Add: Capital introduced by owner | ||

| Add: Net income | 44,650 | |

| Total: | 83,850 | |

| Less: Withdrawals | ||

| Closing Balance | 83,850 | |

Table (4)

6.

To record: closing journal entries.

Introduction: Closing entries are posted to close all the temporary accounts of the accounting books. Closing entries zeros the balances of income statement items, drawings, and dividends.

Explanation of Solution

Recording closing entry for expense accounts:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Income summary | 619,150 | |||

| Repair and maintenance expense | 73,200 | |||

| Advertising expense | 58,700 | |||

| Wages expense | 84,300 | |||

| Utilities expense | 3,400 | |||

| Insurance expense | 12,000 | |||

| Interest expense | 180,000 | |||

| Supplies expense | 3,300 | |||

| Depreciation expense | 204,250 | |||

| (to record closing of expense accounts) |

Table (5)

- Since income summary is a temporary income account, temporary income is decreased. Hence, income summary account is debited.

- Since repair and maintenance expense is an expense, expense is decreased. Hence, repair and maintenance expense account is credited.

- Since advertising expense is an expense, expense is decreased. Hence, advertising expense account is credited.

- Since wages expense is an expense, expense is decreased. Hence, wages expense account is credited.

- Since utilities expense is an expense, expense is decreased. Hence, utilities expense account is credited.

- Since insurance expense is an expense, expense is decreased. Hence, insurance expense account is credited.

- Since interest expense is an expense, expense is decreased. Hence, interest expense account is credited.

- Since supplies expense is an expense, expense is decreased. Hence, supplies expense account is credited.

- Since depreceiation expense is an expense, expense is decreased. Hence, depreceiation -building expense account is credited.

Recording closing entry for revenue accounts:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Rent revenue | 663,800 | |||

| Income summary | 663,800 | |||

| (to record closing of revenue account) |

Table (6)

- Since rent revenue is an income, income is decreased. Hence, rent revenue account is debited.

- Since income summary is a temporary income account, temporary income is increased. Hence, income summary account is credited.

Recording transfer of income summary account:

| Date | Account Title and Explanation | Post Ref. | Debit($) | Credit($) |

| Income summary | 44,650 | |||

| Retained earnings | 44,650 | |||

| (to record closing entry) |

Table (7)

- Since income summary is a temporary income account, temporary income is decreased. Hence, income summary account is debited.

- Since retained earnings is a reserve, reserve is increased. Hence, retained earnings account is credited.

Want to see more full solutions like this?

Chapter 3 Solutions

CORNERSTONES OF FINAN.ACCT.>CUSTOM<

- Problem 3-71B Preparing a Worksheet (Appendix 3A) Flint Inc. operates a cable television System. At December 31, 2019, the following unadjusted account balances were available: The following data are available for adjusting entries: At year end, $1,500 Of office supplies remain unused. Annual depreciation on the building is $20,000. Annual depreciation on the equipment is $150,000 The interest rate on the note is 8%. Four months' interest is unpaid and unrecorded at December 31, 2019. At December 31, 2019, services of $94,000 have performed but are unbilled and unrecorded. Utility bills of $2,800 are unpaid and unrecorded at December 31, 2019. Income taxes of $49,633 were unpaid and unrecorded at year end. Â Required: Prepare a worksheet for Flint. Prepare an income statement, a retained earnings statement, and a classified balance sheet for Flint. Prepare the closing entries.arrow_forwardCase 2-68 Accounting for Partially Completed Events: 3 Prelude to Chapter 3 Ehrlich Smith. the owner of The Shoe Bone has asked you to help him understand the proper way to account for certain accounting items as he prepares his 2019 financial statements. Smith has provided the following information and observations: (Continued) a. A 3-year fire insurance policy was purchased on 2019, for $2,400. Smith believes that a part of the cost of the insurance policy should be allocated to each period that benefits from its coverage. b. The store building was purchased for 580,000 in January 2011. Smith expected then (as he does now) that the building will be serviceable as a shoe store for 20 years from the date of purchase. In 2011, Smith estimated that he could sell the property for $6,000 at the end of its serviceable life. He feels that each period should bear some portion of the cost of this long-lived asset that is slowly being consumed. c. The Shoe Box borrowed 520300 on a 1-year, 8% note that is due on September 1 next year) Smith notes that $21,600 cash will be required to repay the note at maturity. The $1,600 difference is, he feels, a cost of using the loaned funds and should be spread over the periods that benefit from the use of' the loan funds; Required: Explain what Smith is trying to accomplish with the three items. Are his objectives supported by the concepts that underlie accounting?arrow_forwardCase 3-73 Recognition of Service Contract Revenue Zac Murphy is president of Blooming Colors Inc. which provides landscaping services in Tallahassee, Florida. On November 20, 2019, Mr. Murphy signed a service contract with Eastern State University. Under the contract, Blooming Colors will provide landscaping services for all Of Easterns buildings for a period of 2 years beginning on January l, 2020, and Eastern will pay Blooming Colors on a monthly basis beginning on January 31, 2020. Although the same amount of landscaping services will be rendered in every month, the contract provides for higher monthly payments in the first year. Initially, Mr. Murphy proposed that the revenue from the contract should be recognized when the contract is signed in 2019; however, his accountant, Sue Storm, convinced him that this would be inappropriate. Then Mr. Murphy proposed that the revenue should be recognized in an amount equal to the cash collected under the contract. Again, Ms. Storm argued against his proposal, indicating that generally accepted accounting principles (GAAP) required recognition of an equal amount of contract revenue each month. Required: Put yourself in the position of Sue Storm. How would you convince Mr. Murphy that his two proposals are unacceptable and that an equal amount of revenue should be recognized every month?arrow_forward

- Case 3-73 Recognition of Service Contract Revenue Zac Murphy is president of Blooming Colors Inc. which provides landscaping services in Tallahassee, Florida. On November 20, 2019, Mr. Murphy signed a service contract with Eastern State University. Under the contract, Blooming Colors will provide landscaping services for all Of Easterns buildings for a period of 2 years beginning on January l, 2020, and Eastern will pay Blooming Colors on a monthly basis beginning on January 31, 2020. Although the same amount of landscaping services will be rendered in every month, the contract provides for higher monthly payments in the first year. Initially, Mr. Murphy proposed that the revenue from the contract should be recognized when the contract is signed in 2019; however, his accountant, Sue Storm, convinced him that this would be inappropriate. Then Mr. Murphy proposed that the revenue should be recognized in an amount equal to the cash collected under the contract. Again, Ms. Storm argued against his proposal, indicating that generally accepted accounting principles (GAAP) required recognition of an equal amount of contract revenue each month. Required: 3. If Ms. Storms proposal is adopted. how would the contract be reflected in the balancesheets at the end of 2019 and at the end of 2020?arrow_forwardCase 3-73 Recognition of Service Contract Revenue Zac Murphy is president of Blooming Colors Inc. which provides landscaping services in Tallahassee, Florida. On November 20, 2019, Mr. Murphy signed a service contract with Eastern State University. Under the contract, Blooming Colors will provide landscaping services for all Of Easterns buildings for a period of 2 years beginning on January l, 2020, and Eastern will pay Blooming Colors on a monthly basis beginning on January 31, 2020. Although the same amount of landscaping services will be rendered in every month, the contract provides for higher monthly payments in the first year. Initially, Mr. Murphy proposed that the revenue from the contract should be recognized when the contract is signed in 2019; however, his accountant, Sue Storm, convinced him that this would be inappropriate. Then Mr. Murphy proposed that the revenue should be recognized in an amount equal to the cash collected under the contract. Again, Ms. Storm argued against his proposal, indicating that generally accepted accounting principles (GAAP) required recognition of an equal amount of contract revenue each month. Required: 1. Give a reason that might explain Mr. Murphys desire to recognize contract revenue earlier rather than later.arrow_forwardExercise 3-40 Revenue and Expense Recognition Electronic Repair Company repaired a high-definition television for Sarah Merrifield in December 2019. Sarah paid $80 at the time of the repair and agreed to pay Electronic Repair $80 each month for 5 months beginning on January 15, 2020. Electronic Repair used $120 of supplies, which were purchased in November 2020, to repair the television. Assume that Electronic Repair uses accrual-basis accounting. Required: In what month or months should revenue from this service be recorded by Electronic Repaid? In what month or months should the expense related to the repair of the television be recorded by Electronic Repair? CONCEPTUAL CONNECTION Describe the accounting principles used to answer the above questions.arrow_forward

- Exercise 3-46 Identification and Analysis of Adjusting Entries Medina Motor Service is preparing adjusting entries for the year ended December 31, 2019. The following items describe Medina s continuous transactions during 2019: Medinas salaried employees are paid on the last day of every month. Medinas hourly employees are paid every other Friday for the 2 weeks' work. The next payday falls on January 5, 2020. In November 2019, Medina borrowed $600,000 from Bank One, giving a 9% note payable with interest due in January 2020. The note was properly recorded. Medina rents a portion of its parking lot to the neighboring business under a long-term lease agreement that requires payment of rent 6 months in advance on April 1 and October 1 of each year. The October 1, 2019, payment was made and recorded as prepaid rent. Medinas department recognizes the entire revenue on every auto service job when the job is complete. At December 31, several service jobs are in process. Medina recognizes depreciation on shop equipment annually at the end of each year. Medina purchases all of its office supplies from Office Supplies Inc. All purchases are recorded in the supplies account. Supplies expense is calculated and recorded annually at the end of each year. Required: Indicate whether or not each item requires an adjusting entry at December 31, 2019. If an item requires an adjusting entry, indicate which accounts are increased by the adjustment and which are decreased.arrow_forwardProblem 3-69A Preparation of Closing Entries and an Income Statement Round Grove Alarm Company provides security services to homes in northwestern Indiana. At year end 2019, after adjusting entries have been made, the following list of account balances is prepared: Required: Prepare closing entries for Round Grove Alarm. Prepare an income statement for Round Grove Alarm.arrow_forwardExpense Adjustments Faraday Electronic Service repairs stereos and DVD players. During 2019, Faraday engaged in the following activities: On September 1, Faraday paid Wausau Insurance $4,860 for its liability insurance for the next 12 months. The full amount of the prepayment was debited to prepaid insurance. At December 31, Faraday estimates that $1,520 of utility costs are unrecorded and unpaid. Faraday rents its testing equipment from JVC. Equipment rent in the amount of $1,440 is unpaid and unrecorded at December 31. In late October, Faraday agreed to become the sponsor for the sports segment of the evening news program on a local television station. The station billed Faraday $4,350 for 3 months' sponsorship-November 2019, December 2019, and January 2020-in advance. When these payments were made, Faraday debited prepaid advertising. At December 31, 2 months' advertising has been and I month remains unused. Required: Prepare adjusting entries at December 31 for these four activities. CONCEPTUAL CONNECTION What would be the effect on expenses if the adjusting entries were not made?arrow_forward

- Problem 2-62B Comprehensive Problem Mulberry Services sells electronic data processing services to firms too Email to own their own computing equipment. Mulberry had the following amounts and amount balances as of January 1, 2019: During 2019, the following transactions occurred (the events described below are aggregations of many individual events): During 2019, Mulberry sold $690,000 of computing services, all on credit. Mulberry collected $570,000 from the credit sales in Transaction a and an additional $129,000 from the accounts receivable outstanding at the beginning of the year. Mulberry paid the interest payable of $8,000. A Wages of $379,000 were paid in cash. Repairs and maintenance of $9,000 were incurred and paid. The prepaid rent at the beginning of the year was used in 2019. In addition, $28,000 of computer rental costs were incurred and paid. There is no prepaid rent or rent payable at year-end. Mulberry purchased computer paper for $13,000 cash in late December. None of the paper was used by year-end. Advertising expense of $26,000 was incurred and paid. Income tax of $10,300 was incurred and paid in 2019. Interest of $5,000 was paid on the long-term loan. (Continued) Required: 1. Establish a ledger for the accounts listed above and enter the beginning balances. Use a chart of accounts to order the ledger accounts. 2. Analyze each transaction, Journalize as appropriate. (Note: Ignore the date because these events are aggregations of individual events.) 3. Post your journal entries to T-accounts, Add additional T-accounts when needed. 4. Use the ending balances in the T-accounts to prepare a trial balancearrow_forwardProblem 2-593 Journalizing Transactions Monilast Chemicals engaged in the following transactions during December 2019: Dec 2 Paid rent on office furniture, $1,200. 3 Borrowed $25,030 on a 9-month, 3% note. 7 Provided services on credit. $42,600. 10 Purchased supplies on credit, $2,850. 13 Collected accounts receivable, $20,150. 19 Issued common stock, $50000. 22 Paid employee wages for December. $13,825. 23 Paid accounts payable, $1,280. 25 Provided services for cash, $13,500. 30 Paid utility bills for December, $1,975. Required: Prepare a journal entry for each transaction.arrow_forwardCase 3-72 Cash- or Accrual-Basis Accounting Karen Ragsdale owns a business that rents parking spots to students at the local university. Karens typical rental contract requires the student to pay the years rent of $450 ($50 per month) on September 1. When Karen prepares financial statements at the end of December, her accountant requires that Karen spread the $450 over the 9 months that each parking Spot is rented. Therefore, Karen can recognize only $200 of revenue (4 months) from each parking spot rental contract in the year the cash is collected and must defer (delay) recognition of the remaining $250 (5 months) to the next year. Karen argues that getting students to agree to rent the parking Spot is the most difficult part of the activity so she Ought to be able to recognize all $450 as revenue when the cash is received from a student. Required: Why do generally accepted accounting principles require the use of accrual accounting rather than cash-basis accounting for transactions like the one described here?arrow_forward

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning