Intermediate Financial Management

14th Edition

ISBN: 9780357516782

Author: Brigham, Eugene F., Daves, Phillip R.

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 4, Problem 16P

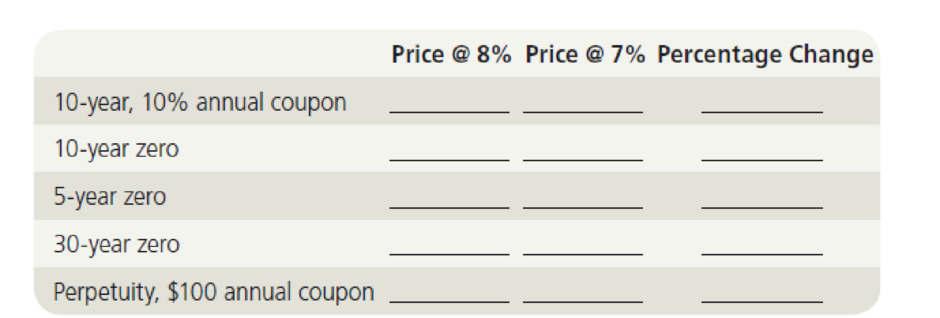

Interest Rate Sensitivity

A bond trader purchased each of the following bonds at a yield to maturity of 8%. Immediately after she purchased the bonds, interest rates fell to 7%. What is the percentage change in the price of each bond after the decline in interest rates? Assume annual coupons and annual compounding. Fill in the following table:

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Data table

不

The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of

face value):

a. Compute the yield to maturity for each bond.

b. Plot the zero-coupon yield curve (for the first five years).

c. Is the yield curve upward sloping, downward sloping, or flat?

a. Compute the yield to maturity for each bond.

The yield on the 1-year bond is ☐ %. (Round to two decimal places.)

(Click on the following icon in order to copy its contents into a spreadsheet.)

Maturity (years)

Price (per $100 face value)

1

$95.42

2

3

4

5

$90.99

$86.47

$81.58

$76.46

Print

Done

The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of the face value):

Maturity (years)

Price (per $100 face value)

1

$96.32

a. Compute the yield to maturity for each bond.

b. Plot the zero-coupon yield curve (for the first five years).

c. Is the yield curve upward sloping, downward sloping, or flat?

a. Compute the yield to maturity for each bond.

The yield on the 1-year bond is

%. (Round to two decimal places.)

2

$91.93

3

$87.36

4

5

$82.57

$77.42

Assume coupons are paid annually. Here are the prices of three bonds with 10 year maturities. Assume face value is $100. Bond Coupon a. What is the yield to maturity of each bond? b. What is the duration of each bond? Complete this question by entering your answers in the tabs below. Required A Required B What is the duration of each bond? Note: Do not round intermediate calculations. Round your answers to 2

decimal places.

Chapter 4 Solutions

Intermediate Financial Management

Ch. 4 - Short-term interest rates are more volatile than...Ch. 4 - The rate of return on a bond held to its maturity...Ch. 4 - If you buy a callable bond and interest rates...Ch. 4 - A sinking fund can be set up in one of two ways....Ch. 4 - Prob. 1PCh. 4 - Prob. 2PCh. 4 - Current Yield for Annual Payments Heath Food...Ch. 4 - Determinant of Interest Rates

The real risk-free...Ch. 4 - Default Risk Premium A Treasury bond that matures...Ch. 4 - Prob. 6P

Ch. 4 - Bond Valuation with Semiannual Payments

Renfro...Ch. 4 - Prob. 8PCh. 4 - Bond Valuation and Interest Rate Risk The Garraty...Ch. 4 - Prob. 10PCh. 4 - Prob. 11PCh. 4 - Bond Yields and Rates of Return A 10-year, 12%...Ch. 4 - Yield to Maturity and Current Yield You just...Ch. 4 - Current Yield with Semiannual Payments

A bond that...Ch. 4 - Prob. 15PCh. 4 - Interest Rate Sensitivity

A bond trader purchased...Ch. 4 - Bond Value as Maturity Approaches An investor has...Ch. 4 - Prob. 18PCh. 4 - Prob. 19PCh. 4 - Prob. 20PCh. 4 - Bond Valuation and Changes in Maturity and...Ch. 4 - Yield to Maturity and Yield to Call

Arnot...Ch. 4 - Prob. 23PCh. 4 - Prob. 1MCCh. 4 - Prob. 2MCCh. 4 - How does one determine the value of any asset...Ch. 4 - Prob. 4MCCh. 4 - What would be the value of the bond described in...Ch. 4 - Suppose a 10-year, 10% semiannual coupon bond with...Ch. 4 - Prob. 9MCCh. 4 - Prob. 10MCCh. 4 - Prob. 11MCCh. 4 - Prob. 12MCCh. 4 - Prob. 14MCCh. 4 - Prob. 15MCCh. 4 - Prob. 16MCCh. 4 - Prob. 17MC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- A plot of the yields on bonds with different terms to maturity but the same risk, liquidity, and tax considerations is known as O A. a yield curve. B. a risk-structure curve. OC. a term-structure curve. 5- O D. an interest-rate curve. Suppose people expect the interest rate on one-year bonds for each of the next four years to be 3%, 6%, 5%, and 6%. If the expectations theory of the term structure of interest rates is correct, then the implied interest rate on bonds with a maturity of four years is nearest whole number). %. (Round your response to the 2- Refer to the figure on your right. Suppose the expected interest rates on one-year bonds for each of the next four years are 4%, 5%, 6%, and 7%, respectively. 1. 1.) Use the line drawing tool (once) to plot the yield curve generated. 3 Term to Maturity in Years 2.) Use the point drawing tool to locate the interest rates on the next four years. 5. 3- Interest Rate .....arrow_forwardAssume that a bond will make payments every six months as shown on the following timeline (using six- month periods): Period Cash Flows a. What is the maturity of the bond (in years)? b. What is the coupon rate (as a percentage)? c. What is the face value? $19.36 2 $19.36 CHE a. What is the maturity of the bond (in years)? The maturity is years. (Round to the nearest integer.) 19 $19.36 20 $19.36+ $1,000arrow_forwardAssume that a bond will make payments every six months as shown on the following timeline (using six-month periods): Period 1 2 29 30 Cash Flows $20.37 $20.37 $20.37 $20.37 + $1,000 a. What is the maturity of the bond (in years)? b. What is the coupon rate (as a percentage)? c. What is the face value?arrow_forward

- K Assume that a bond will make payments every six months as shown on the following timeline (using six-month periods): 0 2 5 Period $19.53 a. What is the maturity of the bond (in years)? b. What is the coupon rate (as a percentage)? c. What is the face value? Cash Flows View an example Get more help. ★ a. What is the maturity of the bond (in years)? The maturity is years. (Round to the nearest integer.) A 6 1 MacBook Pro & 7 $19.53 * 8 9 C 59 $19.53 60 $19.53+$1,000 Clear all BUB 0 {arrow_forwardConsider the following bonds: . What is the percentage change in the price of each bond if its yield to maturity falls from 6.3% to 5.3%? The price of bond A at 6.3% YTM per $100 face value is $ (Round to the nearest cent.) - X Data table (Click on the following icon g in order to copy its contents into a spreadsheet.) Bond Coupon Rate (annual payments) Maturity (years) A 0.0% 15 В 0.0% 10 3.6% 15 8.4% 10 Print Donearrow_forwardnumerical answers should be calculated to at least two decimal places. Face value of bonds is taken as $100. assume coupon payments are paid once a year. Bond A: term to maturity=10 years, coupon rate = 9.75%, current price = $160.55. Find the current yield and yield to maturity of Bond A. Bond B: term to maturity-5 years, coupon rate = 11.25%, yield to maturity -2.35% p.a. Find the current price of Bond B. From your answer, what do say about this price when compared with the face value of the bond?arrow_forward

- Using the expectations hypothesis theory for the term structure of interest rates, determine the expected return for securities with maturities of two, three, and four years based on the following data. (Input your answers as a percent rounded to 2 decimal places.) Interest Rate 1-year T-bill at beginning of year 1 1-year T-bill at beginning of year 2 1-year T-bill at beginning of year 3 1-year T-bill at beginning of year 4 2% 5% 4% 7% Expected Return 0.00 % 2-year security 3-year security % 4-year 2 decimal places required.arrow_forwardAssume coupons are paid annually. Here are the prices of three bonds with 10-year maturities. Assume face value is $100. Bond Coupon (%) 2 Price (%) 48 80.57 97.19 134.92 a. What is the yield to maturity of each bond? b. What is the duration of each bond? Complete this question by entering your answers in the tabs below. Required A Required B What is the yield to maturity of each bond? Note: Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places. Bond Coupon YTM (%) 2 4 6.00 % 7.42% 8 7.01 %arrow_forwardAssume that a bond will make payments every six months as shown on the following timeline (using six-month periods): 0 2 Period Cash Flows 1 $20.73 a. What is the maturity of the bond (in years)? b. What is the coupon rate (as a percentage)? c. What is the face value? $20.73 a. What is the maturity of the bond (in years)? The maturity is years.. (Round to the nearest integer.) 19 $20.73 .... 20 $20.73 + $1,000arrow_forward

- Exploring Finance: Coupon Bonds. Coupon Bonds Conceptual Overview: Explore the value of fixed-interest coupon bonds of different terms. This graph shows the value of 10% coupon bonds of different terms across differing market interest rates. Each bond pays INT = $100 at the end of each year and returns M = $1,000 at maturity. For comparison, the blue line depicts the value of a one-year bond. The term of the other bond in years may be changed using the slider. Drag on the graph to change the current market interest rate (rd) at which the bond (orange curve) is evaluated. 4. For a 10% $1,000 coupon bond, when the market interest rate is greater than 10%, the value of the bond: Is unaffected and still equals its par value of $1,000. Is less than its par value of $1,000. Is greater than its par value of $1,000. Cannot determine because it depends on the term of the bond in years. 5. For a 10%, $1,000 coupon bond, a longer term bond (say, 15 years) is: less affected by…arrow_forwardUsing the expectations hypothesis theory for the term structure of interest rates, determine the expected return for securities with maturities of two, three, and four years based on the following data. Note: Input your answers as a percent rounded to 2 decimal places. Interest Rate 1-year T-bill at beginning of year 1 6% 1-year T-bill at beginning of year 2 9% 1-year T-bill at beginning of year 3 10% 1-year T-bill at beginning of year 4 12% Expected Return 2 year security % 3 year security % 4 year security %arrow_forwardExploring Finance: Coupon Bonds. Coupon Bonds Conceptual Overview: Explore the value of fixed-interest coupon bonds of different terms. This graph shows the value of 10% coupon bonds of different terms across differing market interest rates. Each bond pays INT = $100 at the end of each year and returns M = $1,000 at maturity. For comparison, the blue line depicts the value of a one-year bond. The term of the other bond in years may be changed using the slider. Drag on the graph to change the current market interest rate (rd) at which the bond (orange curve) is evaluated. 5. For a 10%, $1,000 coupon bond, a longer term bond (say, 15 years) is: less affected by changes in the market rate than a 1-year bond. affected the same by changes in the market rate than a 1-year bond. more affected by changes in the market rate than a 1-year bond. Cannot be determined.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...

Finance

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Cengage Learning

What happens to my bond when interest rates rise?; Author: The Financial Pipeline;https://www.youtube.com/watch?v=6uaXlI4CLOs;License: Standard Youtube License