Concept explainers

Videos

Recording Transactions (Including Adjusting Journal Entries), Preparing Financial Statements and Closing Journal Entries, and Computing Net Profit Margin and

Drs. Glenn Feltham and David Ambrose began operations of their physical therapy clinic, called Northland Physical Therapy, on January 1, 2017. The annual reporting period ends December 31. The

Transactions during 2018 (summarized in thousands of dollars) follow:

- a. Borrowed $22 cash on July 1, 2018, signing a six-month note payable.

- b. Purchased equipment for $25 cash on July 2, 2018.

- c. Issued additional shares of common stock for $5 on July 3.

- d. Purchased software on July 4, $3 cash.

- e. Purchased supplies on July 5 on account for future use, $7.

- f. Recorded revenues on December 6 of $55, including $8 on credit and $47 received in cash.

- g. Recognized salaries and wages expense on December 7 of $30; paid in cash.

- h. Collected accounts receivable on December 8, $9.

- i. Paid accounts payable on December 9, $10.

- j. Received a $3 cash deposit on December 10 from a hospital for a contract to start January 5, 2019.

Data for adjusting journal entries on December 31:

- k. Amortization for 2018, $1.

- l. Supplies of $3 were counted on December 31, 2018.

- m.

Depreciation for 2018, $4. - n. Accrued interest of $1 on notes payable.

- o. Salaries and wages incurred but not yet paid or recorded, $3.

- p. Income tax expense for 2018 was $4 and will be paid in 2019.

Required:

- 1. Set up T-accounts for the accounts on the trial balance and enter beginning balances. If you are completing this problem in Connect using the general ledger tool, this requirement will be completed for you.

- 2. Record journal entries for transactions (a) through (j).

- 3. Post the journal entries from requirement 2 to T-accounts and prepare an unadjusted trial balance. If you are completing this problem in Connect using the general ledger tool, this requirement will be completed for you using your answers to requirement 2.

- 4. Record the adjusting journal entries (k) through (p).

- 5. Post the

adjusting entries from requirement 4 and prepare an adjusted trial balance. If you are completing this problem in Connect using the general ledger tool, this requirement will be completed for you using your previous answers. - 6. Prepare an income statement, statement of

retained earnings , and balance sheet. - 7. Prepare the closing

journal entry . - 8.

Post the closing entry from requirement 7 and prepare a post-closing trial balance. If you are completing this problem in Connect using the general ledger tool, this requirement will be completed for you using your previous answers. - 9. How much net income did the physical therapy clinic generate during 2018? What was its net profit margin? Is the business financed primarily by liabilities or stockholders’ equity? What is its current ratio?

1, 3, 5 and 8

Prepare the necessary T-account for the given transactions.

Explanation of Solution

T-account:

T-account refers to an individual account, where the increases or decreases in the value of specific asset, liability, stockholder’s equity, revenue, and expenditure items are recorded.

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

(a)The title of the account

(b)The left or debit side

(c)The right or credit side

Prepare the T-account:

| Cash (A) account | |||

| Beginning Balance | $7 | ||

| a | 22 | ||

| c | 5 | b | $25 |

| f | 47 | d | 3 |

| h | 9 | g | 30 |

| j | 3 | j | 10 |

| Ending Balance | $25 | ||

| Accounts Receivable (A) account | |||||||

| Beginning Balance | 3 | ||||||

| f | 8 | h | 9 | ||||

| Ending Balance | 2 | ||||||

|

Supplies(A) account | |||||||

| Beginning Balance | 3 | ||||||

| e | 7 | ||||||

| 10 | |||||||

| l | 7 | ||||||

| Ending Balance | 3 | ||||||

|

Equipment (A) account | |||||||

| Beginning Balance | 8 | ||||||

| b | 25 | ||||||

| Ending Balance | 33 | ||||||

| Accumulated depreciation -Equipment (xA) account | |||

| Beginning Balance |

1 | ||

| k | 4 | ||

| Ending Balance | 5 | ||

| Software (A) account | |||

| Beginning Balance | 5 | ||

| d | 3 | ||

| Ending Balance | 8 | ||

|

Accumulated Amortization (xA) account | |||

| Beginning Balance | 1 | ||

| k | 1 | ||

| Ending Balance | 2 | ||

|

Accounts payable (L) account | |||

| Beginning Balance | 5 | ||

| i | 10 | e | 7 |

| Ending Balance | 2 | ||

|

Notes payable (L) account | |||

| Beginning Balance | 0 | ||

| a | 22 | ||

| Ending Balance | 22 | ||

| Salaries and wages payable (L) account | |||

| Beginning Balance | 0 | ||

| o | 3 | ||

| Ending Balance | 3 | ||

| Interest payable (L) | |||

| Beginning Balance | 0 | ||

| n | 1 | ||

| Ending Balance | 1 | ||

| Income tax payable (L) account | |||

| p | 4 | ||

| Ending Balance | 4 | ||

Deferred revenue (L) account

| j | 3 | ||

| Ending Balance | 3 | ||

|

Common Stock (SE) account | |||

| Beginning Balance |

15 | ||

| c | 5 | ||

| Ending Balance | 20 | ||

| Retained earnings (SE) account | |||

| Beginning Balance | 4 | ||

| CE1 | 5 | ||

| Ending Balance | 9 | ||

| Service Revenue (R) account | |||

| f | 55 | ||

| CE1 | 55 | ||

| Ending Balance | 0 | ||

| Depreciation expense (E) account | |||

| m | 4 | ||

| CE1 | 4 | ||

| Ending Balance | 0 | ||

| Amortization Expense ( E) account | |||

| Beginning Balance | 0 | ||

| k | 1 | ||

| CE1 | 1 | ||

| Ending Balance | 0 | ||

| Income Tax Expense ( E) account | |||

| p | 4 | ||

| CE1 | 4 | ||

| Ending Balance | 0 | ||

| Interest Expense ( E) account | |||

| n | 1 | ||

| CE1 | 1 | ||

| Ending Balance | 0 | ||

| Salaries and Wages Expense(E) account | |||

| g | 30 | ||

| o | 3 | CE1 | 33 |

| Ending Balance | 0 | ||

| Supplies Expense ( E) account | |||

| l | 7 | ||

| CE1 | 7 | ||

| Ending Balance | 0 | ||

2.

Record the necessary journal entries for transactions (a) to (j).

Explanation of Solution

Record the necessary journal entries for transactions (a) to (j) as follows:

| Date | Account Title and Explanation | Debit ($) | Credit ($) | ||

| a) | Cash (+A) | 22 | |||

| Notes payable (Short-term) (+L) | 22 | ||||

| (To record borrowed cash on note) | |||||

| b) | Equipment (+A) | 25 | |||

| Cash (-A) | 25 | ||||

| (To record purchase of equipment) | |||||

| c) | Cash (+A) | 5 | |||

| Common Stock (+SE) | 5 | ||||

| (To record issued common stock for cash) | |||||

| d) | Software (+A) | 3 | |||

| Cash (-A) | 3 | ||||

| (To record Purchase of additional software) | |||||

| e) | Supplies (+A) | 7 | |||

| Accounts payable (+L) | 7 | ||||

| (To record supplies purchased for future use) | |||||

| f) | Cash (+A) | 47 | |||

| Accounts Receivable (+A) | 8 | 55 | |||

| Service Revenue (+R, +SE) | |||||

| (To record service revenue earned during the year 2018) | |||||

| g) | Salaries and Wages Expense (+E, -SE) | 30 | |||

| Cash (-A) | 30 | ||||

| (To record salaries and wages expense incurred during 2018) | |||||

| h) | Cash (+A) | 9 | |||

| Accounts Receivable (-A) | 9 | ||||

| (To record cash collected on customer’s account) | |||||

| i) | Accounts payable (-L) | 10 | |||

| Cash (-A) | 10 | ||||

| (To record cash paid to creditors) | |||||

| j) | Cash (+A) | 3 | |||

| Deferred Revenue (+L) | 3 | ||||

| (To record receiving of customers deposit before doing work) | |||||

Table (1)

3.

Prepare an unadjusted trial balance based on requirement 2.

Explanation of Solution

Prepare an unadjusted trial balance based on requirement 2 as follows:

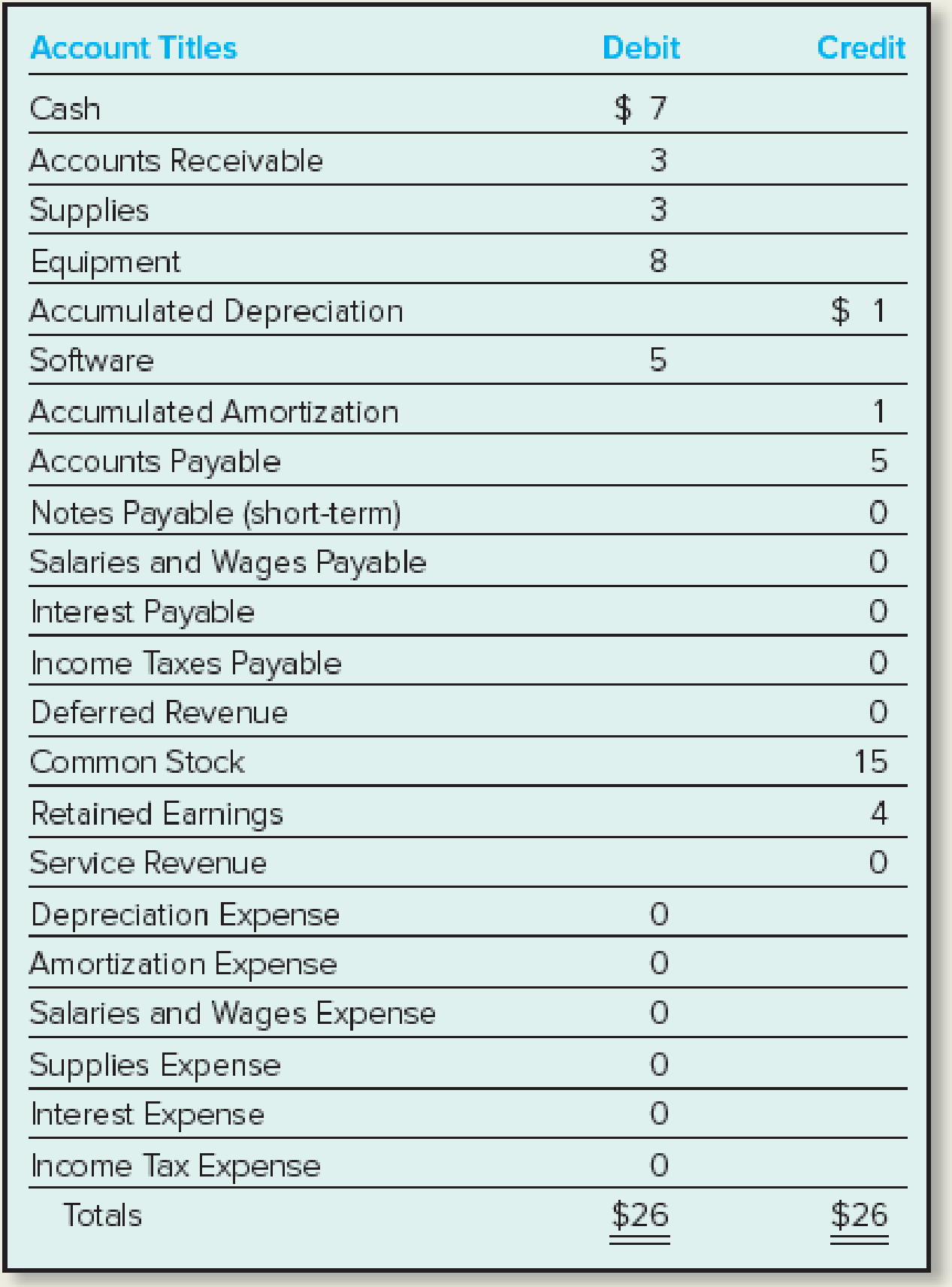

| Incorporation NPT | ||

| Unadjusted Trial Balance | ||

| At December 31, 2018 | ||

| (in thousands) | ||

| Account Titles | Debit ($) | Credit ($) |

| Cash | 25 | |

| Accounts Receivable | 2 | |

| Supplies | 10 | |

| Equipment | 33 | |

| Accumulated Depreciation–Equipment | 1 | |

| Software | 8 | |

| Accumulated Amortization | 1 | |

| Accounts Payable | 2 | |

| Notes Payable (short–term) | 22 | |

| Salaries and Wages Payable | ||

| Interest Payable | ||

| Income Tax Payable | ||

| Deferred revenue | 3 | |

| Common Stock | 20 | |

| Retained Earnings | 4 | |

| Service Revenue | 55 | |

| Salaries and Wages Expense | 30 | |

| Supplies Expense | ||

| Depreciation Expense | ||

| Amortization Expense | ||

| Interest Expense | ||

| Income Tax Expense | ||

| Total | 108 | 108 |

Table (2)

4.

Record the adjusting journal entries from transaction (k) to (p).

Explanation of Solution

Record the adjusting journal entries from transaction (k) to (p) as follows:

| Date | Account Title and Explanation | Debit ($) | Credit ($) | ||

| k. | Amortization Expense (+E, -SE) | 1 | |||

| Accumulated Amortization (+xA, -A) | 1 | ||||

| (To record adjusting entry for amortization expenses) | |||||

| l. | Supplies expense (+E, -SE) (refer working note 1) | 7 | |||

| Supplies(-A) | 7 | ||||

| (To record the use of supplies) | |||||

| m. | Depreciation expense (+E, -SE) | 4 | |||

| Accumulated depreciation –Equipment (+xA, -A) | 4 | ||||

| (To record adjusting entry for depreciation expense) | |||||

| n. | Interest expense (+E, -SE) | 1 | |||

| Interest payable(+L) | 1 | ||||

| (To record the adjusting entry for interest expense) | |||||

| o. | Salaries and wages expense (+E, -SE) | 3 | |||

| Salaries and wages payable (+L) | 3 | ||||

| (To record the adjusting entry for salaries and wages expenses) | |||||

| p. | Income tax expense(+E, -SE) | 4 | |||

| Income tax payable(+L) | 4 | ||||

| (To record the adjusting entry for income tax expense) | |||||

Table (3)

Working note 1:

Calculate the value of supplies expenses:

5.

Prepare an adjusted trial balance from requirement 4.

Explanation of Solution

Prepare an adjusted trial balance for Incorporation NPT for December 31, 2018 as follows:

| Incorporation NPT | ||

| Adjusted Trial Balance | ||

| At December 31, 2018 | ||

| (in thousands) | ||

| Account Titles | Debit ($) | Credit ($) |

| Cash | 25 | |

| Accounts Receivable | 2 | |

| Supplies | 3 | |

| Equipment | 33 | |

| Accumulated Depreciation–Equipment | 5 | |

| Software | 8 | |

| Accumulated Amortization | 2 | |

| Accounts Payable | 2 | |

| Notes Payable (short–term) | 22 | |

| Salaries and Wages Payable | 3 | |

| Interest Payable | 1 | |

| Income Tax Payable | 4 | |

| Deferred revenue | 3 | |

| Common Stock | 20 | |

| Retained Earnings | 4 | |

| Service Revenue | 55 | |

| Salaries and Wages Expense | 33 | |

| Supplies Expense | 7 | |

| Depreciation Expense | 4 | |

| Amortization Expense | 1 | |

| Interest Expense | 1 | |

| Income Tax Expense | 4 | |

| Total | 121 | 121 |

Table (4)

6.

Prepare an income statement, Statement of retained earnings and balance sheet.

Explanation of Solution

Prepare an income statement for the year ended December 31, 2018 as follows:

| Incorporation NPT | ||

| Income Statement | ||

| For the year ended December 31, 2018 | ||

| (in thousands) | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Service revenue | 55 | |

| Total revenues | 55 | |

| Less: Expenses | ||

| Salaries and wage expense | 33 | |

| Supplies expense | 7 | |

| Amortization expense | 1 | |

| Depreciation expense | 4 | |

| Interest expense | 1 | |

| Income tax expense | 4 | |

| Total expenses | 50 | |

| Net income | 5 | |

Table (5)

Prepare a statement of retained earnings as follows:

| Incorporation NPT | ||

| Statement of Retained Earnings | ||

| For the year ended December 31, 2018 | ||

| (in thousands) | ||

| Particulars | Amount ($) | Amount ($) |

| Balance, January 1, 2018 | 4 | |

| Add: Net income | 5 | |

| 9 | ||

| Less: Dividends | (0) | |

| Balance, December 31, 2018 | 9 | |

Table (6)

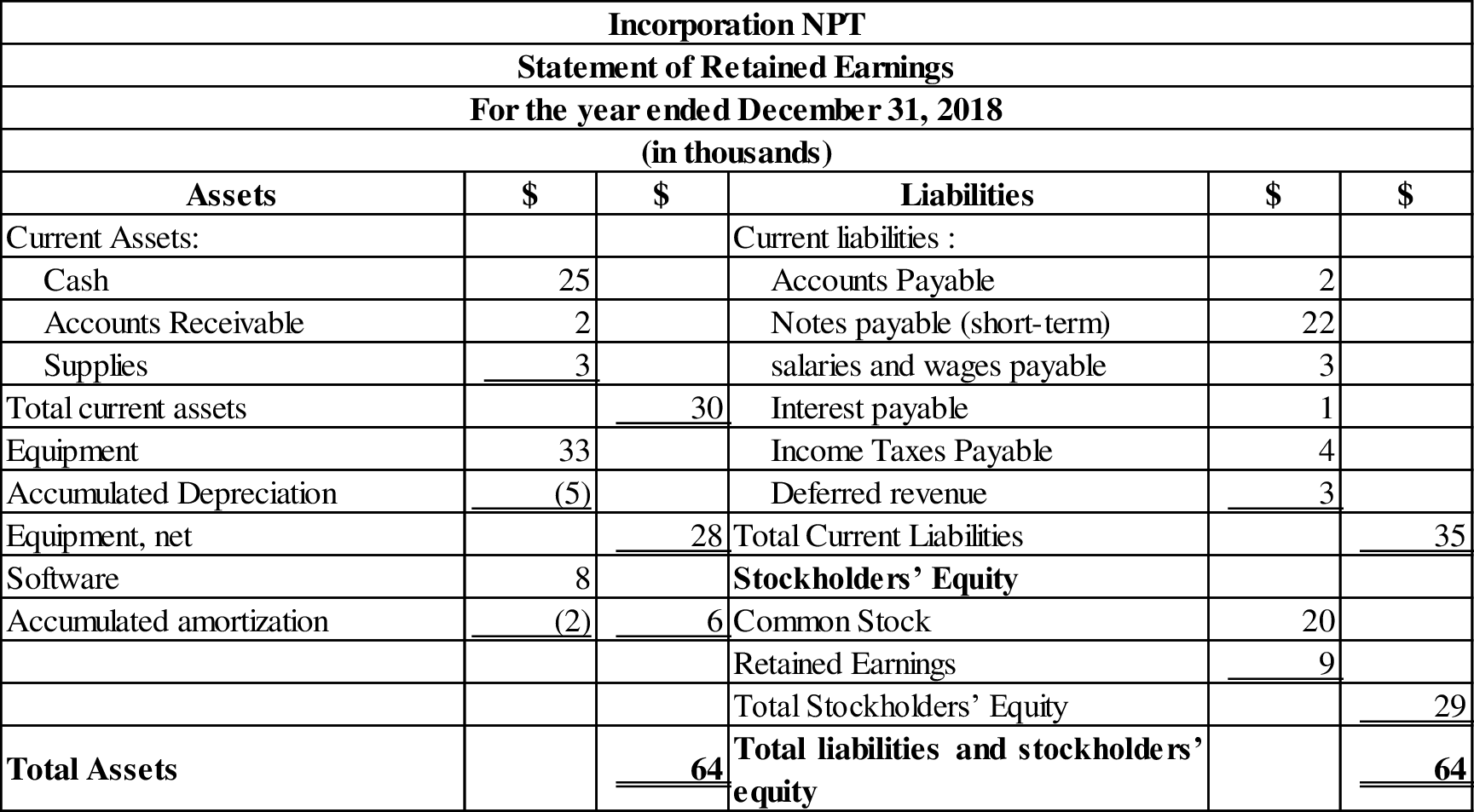

Prepare a balance sheet for the year December 31, 2018 as follows:

Table (7)

7.

Prepare the closing entry for Incorporation NPT on December 31, 2018.

Explanation of Solution

Prepare closing entries for Incorporation NPT on December 31, 2018 as follows:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| December 31, 2018 | Sales revenue(-R) | 55 | |

| Salaries and wages expense(-E) | 33 | ||

| Depreciation expense(-E) | 4 | ||

| Supplies expense(-E) | 7 | ||

| Amortization expense (-E) | 1 | ||

| Income tax expense(-E) | 4 | ||

| Interest expense (-E) | 1 | ||

|

Retained earnings(+SE) (refer table 5) | 5 | ||

| (To record the closing entries for Incorporation NPT) |

Table (8)

For closing of temporary accounts, the balances of revenues, expenses, and dividend accounts are transferred to retained earnings in order to bring zero balance for expenses and revenues accounts.

8.

Prepare a post-closing trial balance from the requirement 7.

Explanation of Solution

Prepare a Post-closing trial balance for Incorporation NPT for December 31, 2018 follows:

| Incorporation NPT | ||

| Post-closing Trial Balance | ||

| At December 31, 2018 | ||

| (in thousands) | ||

| Account Titles | Debit ($) | Credit ($) |

| Cash | 25 | |

| Accounts Receivable | 2 | |

| Supplies | 3 | |

| Equipment | 33 | |

| Accumulated Depreciation–Equipment | 5 | |

| Software | 8 | |

| Accumulated Amortization | 2 | |

| Accounts Payable | 2 | |

| Notes Payable (short–term) | 22 | |

| Salaries and Wages Payable | 3 | |

| Interest Payable | 1 | |

| Income Taxes Payable | 4 | |

| Deferred revenue | 3 | |

| Common Stock | 20 | |

| Retained Earnings | 9 | |

| Service Revenue | 0 | |

| Salaries and Wages Expense | 0 | |

| Supplies Expense | 0 | |

| Depreciation Expense | 0 | |

| Amortization expense | 0 | |

| Interest Expense | 0 | |

| Income Tax Expense | 0 | |

| Total | 71 | 71 |

Table (9)

9.

Ascertain the net income of Incorporation NPT that has been generated during 2018 and calculate the net profit margin. Explain whether the company has been financed primarily by liabilities or stockholders’ equity and to find the current ratio.

Explanation of Solution

The net income of Incorporation NPT for 2018:

Incorporation NPT generated net income of $5(thousand) in the year 2018.

Calculate the net profit margin:

The net profit margin of Incorporation NPT is 9.1%.

Whether the Incorporation NPT is financed primarily by liabilities or stockholders’ equity as follows:

The invested amount of assets primarily comes from liabilities of Incorporation NPT, because the liabilities have financed $35 thousand of the Incorporation NPT’s total assets, whereas stockholder’s equity has financed $29 thousand.

Calculate the current ratio:

The current ratio is 0.86:1.

Want to see more full solutions like this?

Chapter 4 Solutions

FUND. OF FINANCIAL ACCT. (LL) W/CONNECT

- Instruction: Use Journal Sheet (Yellow or White) for the Performance Tasks Performance Task No. 1- On Mar. 1, 2009, Samuel Barbo, a recent medical board topnotcher, started his medical practice. During the month of March, the following transactions were completed. Mar. 1 Barbo invested P42,500 personal funds in a new bank account in the name of Samuel Barbo, M.D. Acquired medical equipment costing P95,000 from Tambilo Medical Equipment Company, paying P15,000 cash, and financing the remainder issuing a P80,000 note payable. Paid rent for the month of March, P7,500. Acquired Medical Supplies from Suiza Medical Supply Company on account, P15,250. Received P18,450 in cash from patients for medical services rendered this week. 2 3 7 Paid Pablo Labs for preparing laboratory work on a patient, P1,800. Paid salaries of medical technician and receptionist, P9,600. 12 15 Billed patients P51,700 for services rendered. 17 Paid Suiza Medical Supply Company P3,750 on account. Paid telephone…arrow_forwardYou have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance. After showing your analysis to the controller, he tells you to change the aging category of a large account from over 120 days to current status and to prepare a new invoice to the customer with a revised date that agrees with the new category. This will change the required allowance for uncollectible accounts…arrow_forwardYou have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance. After showing your analysis to the controller, he tells you to change the aging category of a large account from over 120 days to current status and to prepare a new invoice to the customer with a revised date that agrees with the new category. This will change the required allowance for uncollectible accounts…arrow_forward

- You have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance.3.What is the ethical dilemma you face? What are the ethical considerations? Consider your options and responsibilities as assistant controller.4.Identify the key internal and external stakeholders. What are the negative impacts that can happen if you do not follow the instructions of your supervisor?5.What are the…arrow_forwardYou have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance. After showing your analysis to the controller, he tells you to change the aging category of a large account from over 120 days to current status and to prepare a new invoice to the customer with a revised date that agrees with the new category. This will change the required allowance for uncollectible accounts…arrow_forwardYou have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance. After showing your analysis to the controller, he tells you to change the aging category of a large account from over 120 days to current status and to prepare a new invoice to the customer with a revised date that agrees with the new category. This will change the required allowance for uncollectible accounts…arrow_forward

- 33 Calorie Catering completed the following selected transactions during May 2024: (Click the icon to view the transactions.) Read the requirements Requirement 1. Show whether each transaction would be handled as a revenue or an expense using both the cash basis and accrual basis accounting systems by completing the table provided. (Expenses should be shown in parentheses.) Also indicate the dollar amount of the revenue or expense. The May 1 transaction has been completed as an example. (Enter "0" for any transactions that do not affect revenues or expenses.) Date May 1 Help me solve Amount of Revenue (Expense) for May Cash Basis Amount of Revenue (Expense) $ (1,500) More info May 1 May 5 May 9 May 14 May 23 May 31 May 31 May 31 Accrual Basis Amount of Revenue (Expense) $ 0 Prepaid rent for three months, $1,500. Received and paid electricity bill, $400. Received cash for meals served to customers, $2,700. Paid cash for kitchen equipment, $3,120. Served a banquet on account, $2,900.…arrow_forwardin Requirements: s not been 1. Journalize every transaction in the General Journal 2. Post every general journal in the General Ledger 3. Prepare a trial balance he "out of f LAYTEY DRAGERN, a tax consultant, began his practice on December 2019. The transactions of the firm are as follows: n-balance December Mr. Dragern invested P150,000 in the firm. Paid rent for December to Marooney Devila's Realty P8,000. 3. Purchased supplies on account, P7,200. 1. 2. 4. Acquired P75,000 of office equipment from BibiKow Co, paying P37,000 down with the balance due in 20days. 5. Paid P7,200 on account for supplies purchased. 6. Paid the salaries for two weeks, P6,000 7. Performed consulting services to Dazzling Blowey for cash, P20,000. 8. Paid the salaries for two weeks, P6,000. CO 9. Performed consulting services to Gremma Repeh on account, P35,000. 10. Received and paid the telephone bills, P1,500. 11. Purchased supplies on account, P8,600. 12. Paid the accounts from BibiKow Co, P25,000. 13. Mr.…arrow_forwardOn 12/1/2021 White Clinic had the following balances: Equity of $350,000 Assets of $600,000 Liabilities of $$250,000 The following transactions occurred in December: 1. Paid $85,000 on a mortgage with $15,000 of this being interest. 2. Paid wages of $65,000. 3. Billed patients for services in the amount of $250,000. 4. Placed an order for a new MRI machine in the amount of $550,000. 5. Used supplies in the amount of $30,000 for patient services. 6. Purchased supplies on account in the amount of $60,000. 7. Received funds in the amount of $205,000 from BCBS for previously billed patients Would there be a Journal entry for #4? For #1 interest expense would be a debit or credit entry? Asset balance over the month increased or decreased? White clinic has an additional amount of how many $ in Assets over this period? White clinic made a profit or loss after all transactions? For #7 there would be a debit or credit to Accounts Receivable Liabilities increased by $10,000 over this reporting…arrow_forward

- List and record each transaction (in 000s) for the Claymont Outpatient Clinic, under the accrual basis of accounting, at December 31, 20X1. You are creating a General Ledger using exhibit 3-6 on page 112 as a guide. Zelman( Workbook) a. The clinic received a $10,000,000 unrestricted cash contribution from the community. b. The clinic purchased $4,500,000 of equipment using cash. c. The clinic borrowed $2,000,000 from the bank on a long-term basis. d. The clinic purchased $550,000 of supplies on credit. e. The clinic provided $8,400,000 of services on credit. f. In the provision of these services, the clinic used $420,000 of supplies. g. The clinic received $800,000 in advance to care for capitated patients. h. The clinic incurred $4,500,000 in labor expenses and paid cash for them. i. The clinic incurred $2,230,000 in general expenses and paid cash for them. j. The clinic received $6,000,000 from patients and their 3rd party payers in payment of outstanding accounts. k.…arrow_forwardProblem: The following account balances appeared in the general ledger of Dr. Robin Rubio at the end of December 2012, the second year of his private medical practice: Cash 350,403 Accounts Receivable 205, 000 Allowance for Bad Debts 7, 550 Prepaid Supplies Library 11,500 155,000 Accumulated Depreciation-Library Medical Equipment 15, 500 96,000 Accumulated depreciation-Medical Equipment 2, 000 Loans Payable 200, 000 Accounts Payable 18,000 SS and CC Premium Payable |200 HDMF Premium Payable 100 PhilHealth Premium Payable Withholding Taxes Payable 75 427 Rubio, Capital 180, 650 Rubio, Personal 42, 000 Medical Fees Earned 729, 000 HDMF Premium Expense 1,100 PhilHealth Premium Expense 825 Salaries Expense 72, 000 Rent Expense 110, 000 SS And EC Premium Expense 4,974 Taxes and Licenses 9, 000 Utilities Expense 75, 700 Interest Expense 20, 000 DATA FIR ADJUSTMENTS AS FOLLOWS 1. Rent expense represents payment for rent from January to November. 2. The estimated annual depreciation of the…arrow_forwardBefore you begin this assignment, review the Tying It All Together feature in the chapter. Part of Fry’s Electronics, Inc.'s experience involves providing technical support to its customers. This includes in-home installations of electronics and also computer support at their retail store locations. Requirements Suppose Fry’s Electronics, Inc. provides $10,500 of computer support at the Dallas-Fort Worth store during the month of November. How would Fry's Electronics record this transaction? Assume all customers paid in cash. What financial statement(s) would this transaction affect? Assume Fry’s Electronics, Inc.’s Modesto, California, location received $24,000 for an annual contract to provide computer support to the local city government. How would Fry’s Electronics record this transaction? What financial statement(s) would this transaction affect? What is the difference in how revenue is recorded in requirements 1 and 2? Clearly state when revenue is recorded in each requirement.arrow_forward

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning