Videos

Financial statements

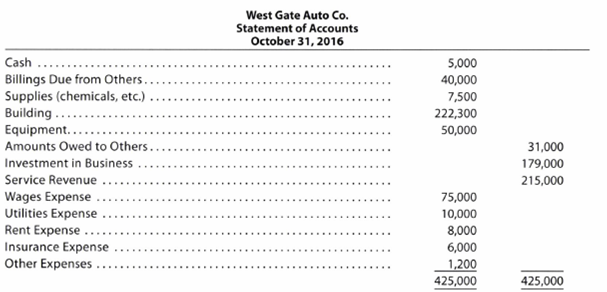

Assume that you recently accepted a position with Five Star National Bank & Trust as an assistant loan officer. As one of your first duties, you have been assigned the responsibility of evaluating a loan request for $300,000 from West Gate Auto Co., a small proprietorship. In support of the loan application, Joan Whalen, owner, submitted a “Statement of Accounts” (

1. Explain to Joan Whalen why a set of financial statements (income statement, statement of owner’s equity, and

2. In discussing the “Statement of Accounts” with Joan Whalen, you discovered that the accounts had not been adjusted at October 31. Analyze the “Statement of Accounts” and indicate possible

3. Assuming that an accurate set of financial statements will be submitted by Joan Whalen in a few days, what other considerations or information would you require before making a decision on the loan request?

Trending nowThis is a popular solution!

Chapter 4 Solutions

Working Papers, Chapters 1-17 for Warren/Reeve/Duchac's Accounting, 26th and Financial Accounting, 14th

- You have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance. After showing your analysis to the controller, he tells you to change the aging category of a large account from over 120 days to current status and to prepare a new invoice to the customer with a revised date that agrees with the new category. This will change the required allowance for uncollectible accounts…arrow_forwardYou have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance.3.What is the ethical dilemma you face? What are the ethical considerations? Consider your options and responsibilities as assistant controller.4.Identify the key internal and external stakeholders. What are the negative impacts that can happen if you do not follow the instructions of your supervisor?5.What are the…arrow_forwardYou have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance. After showing your analysis to the controller, he tells you to change the aging category of a large account from over 120 days to current status and to prepare a new invoice to the customer with a revised date that agrees with the new category. This will change the required allowance for uncollectible accounts…arrow_forward

- You have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance. After showing your analysis to the controller, he tells you to change the aging category of a large account from over 120 days to current status and to prepare a new invoice to the customer with a revised date that agrees with the new category. This will change the required allowance for uncollectible accounts…arrow_forwardJuice World Jamaica Limited, a leading juice manufacturing company has recently hired you as an Accounting Officer. As per job description, you are required to assist in the preparation of the financial statements. The Accounts Manager has extracted a list of balances as at December 2021 for you to review. Revenue 7 600 010 Administrative Expenses 2 300 000 Distribution Costs 980 231 Interest paid on loan Purchases 125 000 4 500 330 Inventories at 1 January 2021 Trade receivables 1 018 900 630 340 Provision for doubtful debts at Jan 2021 19 634 Bad debts 70 110 Non- current Investment 300 900 Additional notes i. Provide for Administrative Expenses of $500 000 paid in advance at 31 December 2021 and Distribution Costs of $50 528 owing at 31 December 2021 Provision for Doubtful Debts is to be maintained at 10% of receivables ii. iii. Inventories at 31 December 2021 were valued at $ı 000 000 iv. Provide for corporation tax of $80 000 which is payable on October 1, 2022 Loan interest…arrow_forwardPlease provide the following journal entries for these transactions, you can draw the T- Accounts or journal entries; A) Mortgage Company funded a loan for $100,000 and the company only advance 98% of the loan through financing (Warehouse Line). Remaining 2% is gathered from Companys funds. B) The same loan was sold to investor at 102 % 15 days later, please prepare the journal entries. C) The Company has expenses at the end of the month in the amount of $20,000 but has not paid until 30 days later. Please prepare journal entries at the end of the month and 30 days payment. D) The company received funds and has a trust liability account for borrowers in the amount of $10,000. 30 days later the trust liability is being transferred to the final investors. E) Company Prepaid Insurance for 12 months and paid in January for $1,200. You are now in the March 31 st of the year.arrow_forward

- You have recently been hired by First National Bank as the assistant loan officer. Part of your work involves assessing which companies should be allowed to borrow money from the bank. The bank wants to lend money to all companies that will likely have the resources available at the time the loan obligation becomes due. During the current week, three companies have approached you about obtaining a two-year loan. For each of these companies, you ask to see their balance sheets over the previous six years. Your analyses of the companies' assets and liabilities are provided in the graphs below. Examine those graphs and answer the following questions: $120,000 $100,000 $80,000 $60,000 $40,000 $20,000 $0 Year 1 2 Company A 3 4 5 $100,000 $75,000 6 Company B $75,000 RP -Liabilities -Assets $50,000 Click here to open the graph(s) in a new tab. Required: 1. The reported amount of assets for Company A over the six-year period is: 2. The reported amount of liabilities for Company B over the…arrow_forwardSantana Rey has consulted with her local banker and is considering financing an expansion of her business by obtaining a long-term bank loan. Selected account balances at March 31, 2020, for Business Solutions follow. Total assets . $120,268 Total liabilities . $875 Total equity $119,393 Required 1. The bank has offered a long-term secured note to Business Solutions. The bank’s loan procedures require that a client’s debt-to-equity ratio not exceed 0.8. As of March 31, 2020, what is the maximum amount that Business Solutions could borrow from this bank? 2. If Business Solutions borrows the maximum amount allowed from the bank, what percentage of assets would be financed (a) by debt and (b) by equity? 3. What are some factors Santana Rey should consider before borrowing the funds?arrow_forwardRecord the following transactions for the Scott Company: Transactions: Nov. 4 Received a $6,500, 90-day, 6% note from Tim’s Co. in payment of the account. Dec. 31 Accrued interest on the Tim’s Co. note. Feb. 2 Received the amount due from Tim’s Co. on the note. Required: Journalize the above transactions. Refer to the Chart of Accounts for exact wording of account titles. Round your answers to two decimal places. Assume a 360-day year when calculating interest. CHART OF ACCOUNTS Scott Company General Ledger ASSETS 110 Cash 111 Petty Cash 121 Accounts Receivable-Batson Co. 122 Accounts Receivable-Bynum Co. 123 Accounts Receivable-Calahan Inc. 124 Accounts Receivable-Dodger Co. 125 Accounts Receivable-Fronk Co. 126 Accounts Receivable-Miracle Chemical 127 Accounts Receivable-Solo Co. 128 Accounts Receivable-Tim’s Co. 129 Allowance for Doubtful Accounts 131 Interest Receivable 132 Notes Receivable-Tim’s Co. 141…arrow_forward

- Record the following transactions for the Scott Company: Transactions: Nov. 4 Received a $6,500, 90-day, 6% note from Tim’s Co. in payment of the account. Dec. 31 Accrued interest on the Tim’s Co. note. Feb. 2 Received the amount due from Tim’s Co. on the note. Required: Journalize the above transactions. Refer to the Chart of Accounts for exact wording of account titles. Round your answers to two decimal places. Assume a 360-day year when calculating interest. CHART OF ACCOUNTS Scott Company General Ledger ASSETS 110 Cash 111 Petty Cash 121 Accounts Receivable-Batson Co. 122 Accounts Receivable-Bynum Co. 123 Accounts Receivable-Calahan Inc. 124 Accounts Receivable-Dodger Co. 125 Accounts Receivable-Fronk Co. 126 Accounts Receivable-Miracle Chemical 127 Accounts Receivable-Solo Co. 128 Accounts Receivable-Tim’s Co. 129 Allowance for Doubtful Accounts 131 Interest Receivable 132 Notes Receivable-Tim’s Co. 141…arrow_forwardAssume you work as an assistant to the chief financial officer (CFO) of Fashions First, Inc. TheCFO reminds you that the fiscal year-end is only two weeks away and that he is looking to you toensure the company stays in compliance with its loan covenant to maintain a debt-to-assets ratio ofno more than 75 percent. A review of the general ledger indicates that assets total $690,000 and liabilities are $570,000. Your company has an excess of Cash ($300,000) and an equally large balancein Accounts Payable ($270,000), although none of its Accounts Payable are due until next month.Required:1. Determine whether the company is currently in compliance with its loan covenant.2. Assuming the level of assets and liabilities remains unchanged until the last day of the fiscalyear, evaluate whether Fashions First should pay down $210,000 of its Accounts Payable onthe last day of the year, before the Accounts Payable become duearrow_forwardAggressive Corporation approaches Matt Taylor, a loan officer for Oklahoma State Bank, seeking to increase the company's borrowings with the bank from $100,000 to $150,000. Matt has an uneasy feeling as he examines the loan application from Aggressive Corporation, which just completed its first year of operations. The application included the following financial statements. The income statement submitted with the application shows a net income of $30,000 in the first year of operations. Referring to the balance sheet, this net income represents a more-than-acceptable 15% rate of return on assets of $200,000. Matt's concern stems from his recollection that the $100,000 note payable reported on the balance sheet is a three-year loan from his bank, approved earlier this year. He recalls another promising new company that, just recently, defaulted on its loan due to its inability to generate sufficient cash flows to meet its loan obligations. Seeing Matt's hesitation, Larry Bling, the CEO…arrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage