Concept explainers

Videos

a. 1 and 4

Prepare

Prepare adjusting entry for the month of December.

a. 1 and 4

Explanation of Solution

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and equities.

- Credit, all increase in liabilities, revenues, and equities, all decrease in assets, and expenses.

Debit: The condensed form of a ledger is referred to as T-account. The left-hand side of this account is known as debit.

Credit: It refers to selling goods and services to the customers on account.

Adjusting entries are those entries which are recorded at the end of the year, to update the income statement accounts (revenue and expenses) and balance sheet accounts (assets, liabilities, and

Prepare journal entries for the December transactions as follows:

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) | |

| Year 1 | |||||

| December | 1 | Cash | 240,000 | ||

| Capital stock | 240,000 | ||||

| (To record the cash invested in the business) | |||||

| December | 1 | Rental Equipment | 288,000 | ||

| Cash | 168,000 | ||||

| Notes Payable | 120,000 | ||||

| (To record the Purchase of equipment from Rent-it and the Note payable is due for one year) | |||||

| December | 1 | Prepaid Rent | 14,400 | ||

| Cash | 14,400 | ||||

| (To record the payment of three months' rent in advance) | |||||

| December | 4 | Office Supplies | 1,200 | ||

| Accounts Payable | 1,200 | ||||

| (To record the purchase of supplies on account.) | |||||

| December | 8 | Cash | 9,600 | ||

| Unearned Rental Fees | 9,600 | ||||

| (To record the cash received in advance for equipment rental by the Construction Company) | |||||

| December | 12 | Salaries Expense | 6,240 | ||

| Cash | 6,240 | ||||

| (To record the Payment of salaries for first two weeks in December) | |||||

| December | 15 | Cash | 14,400 | ||

| 7,200 | |||||

| Rental Fees Earned | 21,600 | ||||

| (To record the rental fees earned in first 15 days of December) | |||||

| December | 17 | Maintenance Expense | 720 | ||

| Accounts Payable | 720 | ||||

| (To record the purchase of repair parts on account from Incorporation) | |||||

| December | 23 | Cash | 2,400 | ||

| Accounts Receivable | 2,400 | ||||

| (To record the collection of an accounts receivable) | |||||

| December | 26 | (No entry is required to record rental of backhoe.) | |||

| December | 26 | Salaries Expense | 6,240 | ||

| Cash | 6,240 | ||||

| (To record the Payment of biweekly payroll) | |||||

| December | 27 | Accounts Payable | 720 | ||

| Cash | 720 | ||||

| (To record the payment of account payable) | |||||

| 2,400 | |||||

| December | 28 | Dividends | 2,400 | ||

| Dividends Payable | |||||

| (To record the Declared dividend of 12% per share payable on January 15, Year 2) | |||||

| December | 29 | (No entry is required to record lawsuit.) | |||

| December | 29 | Unexpired Insurance | 11,520 | ||

| Cash | 11,520 | ||||

| (To record the Purchase of 12-month liability policy) | |||||

| December | 31 | Utilities Expense | 840 | ||

| Accounts Payable | 840 | ||||

| (To record the utilities incurred for December) | |||||

| December | 31 | Cash | 18,720 | ||

| Accounts Receivable | 5,280 | ||||

| Rental Fees Earned | 24,000 | ||||

| (To record the rental fees earned in the second half of December) | |||||

Table (1)

Prepare adjusting entry for the month of December as follows:

| General Journal (Adjusting) | |||||

| December, 31 Year 1 | |||||

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) | |

| Year 1, December | 31. | Rent Expense (1) | 4,800 | ||

| Prepaid Rent | 4,800 | ||||

| (To record the rent expense for December) | |||||

| December | 31. | Interest Expense (2) | 600 | ||

| Interest Payable | 600 | ||||

| (To record the interest expense accrued in December) | |||||

| December | 31. | 3,000 | |||

| Accumulated Depreciation of Rental Equipment | 3,000 | ||||

| (To record the depreciation expense incurred for December) | |||||

| December | 31. | Office Supplies Expense (4) | 480 | ||

| Office Supplies | 480 | ||||

| (To record the offices supplies used for December) | |||||

| December | 31. | Unearned Rental fees | 4,440 | ||

| Rental fees earned | 4,440 | ||||

| (To record the conversion of unearned revenue into earned revenue in December) | |||||

| December | 31. | Accounts Receivable | 1,800 | ||

| Rental fees earned | 1,800 | ||||

| (To record the revenue accrued at the end of December) | |||||

| December | 31. | Salaries Expense | 1,680 | ||

| Salaries Payable | 1,680 | ||||

| (To record the accrued but unpaid salaries in December) | |||||

| December | 31. | Income Taxes Expense (5) | 10,896 | ||

| Income Taxes Payable | 10,896 | ||||

| (To record the income taxes expense accrued in December) | |||||

Table (2)

Working notes:

Compute the amount of rent Expense:

Compute the amount of interest Expense:

Compute the amount of depreciation Expense:

Compute the amount of Office Supplies Expense:

Compute the amount of income taxes Expense:

a. 2 and 5

Post the December transactions to the suitable ledger accounts.

Post the adjusting entries to the suitable ledger accounts.

a. 2 and 5

Explanation of Solution

Posting transactions:

The process of transferring the journalized transactions into the accounts of the ledger is known as posting the transactions.

| Cash | |||||

| Date | Debit | Credit | Balance | ||

| December | 1 | 240,000 | 240,000 | ||

| 1 | 168,000 | 72,000 | |||

| 1 | 14,400 | 57,600 | |||

| 8 | 9,600 | 67,200 | |||

| 12 | 6,240 | 60,960 | |||

| 15 | 14,400 | 75,360 | |||

| 23 | 2,400 | 77,760 | |||

| 26 | 6,240 | 71,520 | |||

| 27 | 720 | 70,800 | |||

| 29 | 11,520 | 59,280 | |||

| 31 | 18,720 | 78,000 | |||

| Accounts Receivable | |||||

| Date | Debit | Credit | Balance | ||

| December | 15 | 7,200 | 7,200 | ||

| 23 | 2,400 | 4,800 | |||

| 31 | 5,280 | 10,080 | |||

| 31 | 1,800 | 11,880 | |||

| Prepaid Rent | |||||

| Date | Debit | Credit | Balance | ||

| December | 1 | 14,400 | 14,400 | ||

| 31 | 4,800 | 9,600 | |||

| Unexpired Insurance | |||||

| Date | Debit | Credit | Balance | ||

| December | 29 | 11,520 | 11,520 | ||

| Office Supplies | |||||

| Date | Debit | Credit | Balance | ||

| December | 4 | 1,200 | 1,200 | ||

| 31 | 480 | 720 | |||

| Rental Equipment | |||||

| Date | Debit | Credit | Balance | ||

| December | 1 | 288,000 | 288,000 | ||

| Accumulated Depreciation: Rental Equipment | |||||

| Date | Debit | Credit | Balance | ||

| December | 31 | 3,000 | 3,000 | ||

| Notes Payable | |||||

| Date | Debit | Credit | Balance | ||

| December | 1 | 120,000 | 120,000 | ||

| Accounts Payable | |||||

| Date | Debit | Credit | Balance | ||

| December | 4 | 1,200 | 1,200 | ||

| 17 | 720 | 1,920 | |||

| 27 | 720 | 1,200 | |||

| 31 | 840 | 2,040 | |||

| Interest Payable | |||||

| Date | Debit | Credit | Balance | ||

| December | 31 | 600 | 600 | ||

| Salaries Payable | |||||

| Date | Debit | Credit | Balance | ||

| December | 31 | 1,680 | 1,680 | ||

| Dividends Payable | |||||

| Date | Debit | Credit | Balance | ||

| December | 28 | 2,400 | 2,400 | ||

| Unearned Rental Fees | |||||

| Date | Debit | Credit | Balance | ||

| December | 8 | 9,600 | 9,600 | ||

| 31 | 4,440 | 5,160 | |||

| Income Taxes Payable | |||||

| Date | Debit | Credit | Balance | ||

| December | 31 | 10,896 | 10,896 | ||

| Income Taxes Payable | |||||

| Date | Debit | Credit | Balance | ||

| December | 1 | 240,000 | 240,000 | ||

| Date | Debit | Credit | Balance | ||

| December | 31 | Income, Year 1 | 16,344 | 16,344 | |

| 31 | Dividends | 2,400 | 13,944 | ||

Table (3)

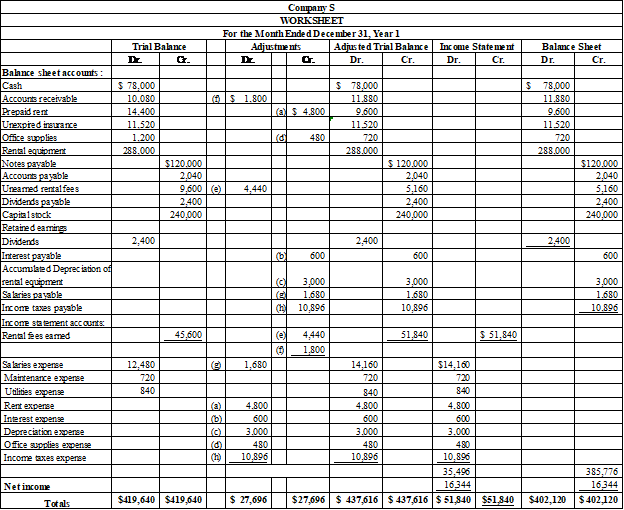

a. 3 and 6

Prepare the unadjusted

a. 3 and 6

Explanation of Solution

Worksheet:

A worksheet is the summarized form of accounting information which is made in order to ensure that the accounts are made properly.

Figure (1)

b.

Prepare an income statement and statement of retained earnings and a balance sheet for the year ended December 31.

b.

Answer to Problem 1CP

- Prepare the income statement of Company S as on December 31, Year 1 as follows:

| Company S | ||

| Income Statement | ||

| For the Year Ended December 31, Year 1 | ||

| Particulars | $ | $ |

| Revenues: | ||

| Rental fees earned | $51,840 | |

| Less: Expenses: | ||

| Salaries expense | $14,160 | |

| Maintenance expense | 720 | |

| Utilities expense | 840 | |

| Rent expense | 4,800 | |

| Office supplies expense | 480 | |

| Depreciation expense | 3,000 | |

| Interest expense | 600 | 24,600 |

| Income before income taxes expense | $27,240 | |

| Less: Income taxes expense | 10,896 | |

| Net income | $16,344 | |

Table (4)

- Prepare the statement of retained earnings of Company S as on December 31, Year 1 as follows:

| Company S | |

| Statement of retained earnings | |

| For the Year Ended December 31, Year 1 | |

| Particulars | $ |

| Retained earnings as on January 1, Year 1 | 0 |

| Add: Net Income | 16,344 |

| Less: Dividend | 2,400 |

| Retained earnings as on December 31, Year 1 | 13,944 |

Table (5)

- Prepare the Balance Sheet of Company S as on December 31, Year 1 as follows:

| Company S | ||

| Balance Sheet | ||

| December 31, Year 1 | ||

| Assets | $ | $ |

| Cash | $78,000 | |

| Accounts Receivable | 11,880 | |

| Prepaid rent | 9,600 | |

| Unexpired insurance | 11,520 | |

| Office supplies | 720 | |

| Rental equipment | 288,000 | |

| Less: Accumulated depreciation | 3,000 | 285,000 |

| Total Assets | $396,720 | |

| Liabilities | ||

| Notes payable | 120,000 | |

| Accounts payable | 2,040 | |

| Interest payable | 600 | |

| Salaries payable | 1,680 | |

| Dividends payable | 2,400 | |

| Unearned rental fees | 5,160 | |

| Income taxes payable | 10,896 | |

| Total Liabilities | $142,776 | |

| Stockholders' Equity | ||

| Capital stock | $240,000 | |

| Retained earnings | 13,944 | $253,944 |

| Total Stockholders' Equity | ||

| Total Liabilities and Stockholders' Equity | $396,720 | |

Table (6)

Explanation of Solution

Income statement:

The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Statement of retained earnings:

This statement reports the beginning retained earnings and all the changes which led to ending retained earnings. Net income from income statement is added to and dividends are deducted from beginning retained earnings to arrive at the end result, ending retained earnings.

Balance sheet:

This financial statement reports a company’s resources (assets) and claims of creditors (liabilities) and stockholders (stockholders’ equity) over those resources. The resources of the company are assets which include money contributed by stockholders and creditors. Hence, the main elements of the balance sheet are assets, liabilities, and stockholders’ equity.

c.

Prepare the disclosures that are required to accompany the December 31 financial statements.

c.

Answer to Problem 1CP

Note 1: Depreciation Policy

The Depreciation expense in the financial statements is calculated by using the straight-line method of depreciation. The estimated useful life of the rental equipment is 8 years.

Note 2: Maturity dates of liabilities

The notes payable of the company matures on November 30, Year 2 and it is the single obligation of the company. The maturity value of this note including interest, will amount to $127,200.

Note 3: Pending litigation

For $30,000 personal injury lawsuit the Company has been named as a co-defendant. The extent of legal and financial responsibility cannot be determined at this time.

Explanation of Solution

Straight-line depreciation method:

The depreciation method which assumes that the consumption of economic benefits of long-term asset could be distributed equally throughout the useful life of the asset, is referred to as straight-line method.

d.

Prepare the closing entries and

d.

Answer to Problem 1CP

Prepare the year-end closing entries of Company S as follows:

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| Year 1, December 31 | Rent fees earned | 51,840 | ||

| Income Summary | 51,840 | |||

| (To record the closure of revenues account ) | ||||

| December 31 | Income Summary | 35,496 | ||

| Salaries Expense | 14,160 | |||

| Maintenance Expense | 720 | |||

| Utilities Expense | 840 | |||

| Rent Expense | 4,800 | |||

| Office Supplies Expense | 480 | |||

| Depreciation Expense | 3,000 | |||

| Interest Expense | 600 | |||

| Income Taxes Expense | 10,896 | |||

| (To record the closure of expense account to income summary) | ||||

| December 31 | Income Summary | 16,344 | ||

| Retained earnings | 16,344 | |||

| (To record the closure of net income from income summary to retained earnings) | ||||

| December31 | Retained earnings | 2,400 | ||

| Dividends | 2,400 | |||

| (To record the closure of dividend to retained earnings) | ||||

Table (7)

Post the closing entries to ledger accounts:

| Retained Earnings | |||||

| Date | Explanation | Debit | Credit | Balance | |

| December | 31 | Income, Year 1 | 16,344 | 16,344 | |

| 31 | Dividends | 2,400 | 13,944 | ||

| Dividends | |||||

| Date | Explanation | Debit | Credit | Balance | |

| December | 28 | 2,400 | 2,400 | ||

| 31 | To close | 2,400 | 0 | ||

| Income Summary | |||||

| Date | Explanation | Debit | Credit | Balance | |

| December | 31 | To close revenue accounts | 51,840 | 51,840 | |

| 31 | To close expense accounts | 35,496 | 16,344 | ||

| 31 | To close | 16,344 | 0 | ||

| Rental Fees Earned | |||||

| Date | Explanation | Debit | Credit | Balance | |

| December | 15 | 21,600 | 21,600 | ||

| 31 | 24,000 | 45,600 | |||

| 31 | 4,440 | 50,040 | |||

| 31 | 1,800 | 51,840 | |||

| 31 | To close | 51,840 | 0 | ||

| Salaries Expense | |||||

| Date | Explanation | Debit | Credit | Balance | |

| December | 12 | 6,240 | 6,240 | ||

| 26 | 6,240 | 12,480 | |||

| 31 | 1,680 | 14,160 | |||

| 31 | To close | 14,160 | 0 | ||

| Maintenance Expense | |||||

| Date | Explanation | Debit | Credit | Balance | |

| December | 17 | 720 | 720 | ||

| 30 | To close | 720 | 0 | ||

| Utilities Expense | |||||

| Date | Explanation | Debit | Credit | Balance | |

| December | 31 | 840 | 840 | ||

| 31 | To close | 840 | 0 | ||

| Rent Expense | |||||

| Date | Explanation | Debit | Credit | Balance | |

| December | 31 | 4,800 | 4,800 | ||

| 31 | To close | 4,800 | 0 | ||

| Office Supplies Expense | |||||

| Date | Explanation | Debit | Credit | Balance | |

| December | 31 | 480 | 480 | ||

| 31 | To close | 480 | 0 | ||

| Depreciation Expense | |||||

| Date | Explanation | Debit | Credit | Balance | |

| December | 31 | 3,000 | 3,000 | ||

| 31 | To close | 3,000 | 0 | ||

| Interest Expense | |||||

| Date | Explanation | Debit | Credit | Balance | |

| December | 31 | 600 | 600 | ||

| 31 | To close | 600 | 0 | ||

| Income taxes Expense | |||||

| Date | Explanation | Debit | Credit | Balance | |

| December | 31 | 10,896 | 10,896 | ||

| 31 | To close | 10,896 | 0 | ||

Table (8)

Explanation of Solution

- Revenue Earned are the revenue account. Since the amount of revenue is closed, and transferred to retained earnings account, they are debited.

- Office supply Expense, Depreciation Expense, Rent expenses, Salaries Expense, Insurance Expense, Interest Expense, Income and Taxes Expense are the expense accounts. Since the amounts of expenses are closed to retained earnings account, they are credited.

- Income Summary is a clearing account or temporary account used to close revenues and expenses to Retained Earnings account. Since Income Summary account has a credit balance, it is transferred to Retained Earnings account by debiting it. Therefore, debit Income Summary account with $16,344.

- Since Retained Earnings account’s amount has increased due to closing of Income Summary account to Retained Earnings account, stockholders’ equity amount has increased. Therefore, credit Retained Earnings account with $16,344.

- Closing entries are also passed in order to close the excess of expenses over the revenues, and the dividend account.

e.

Prepare an after-closing trial balance of Company S.

e.

Answer to Problem 1CP

Prepare an after-closing trial balance of Company S as follows:

| Company S | ||

| After-Closing Trial Balance | ||

| December 31, Year 1 | ||

| Particulars | $ | $ |

| Cash | $78,000 | |

| Accounts receivable | 11,880 | |

| Prepaid rent | 9,600 | |

| Unexpired insurance | 11,520 | |

| Office supplies | 720 | |

| Rental equipment | 288,000 | |

| Accumulated depreciation: rental equipment | $3,000 | |

| Notes payable | 120,000 | |

| Accounts payable | 2,040 | |

| Interest payable | 600 | |

| Salaries payable | 1,680 | |

| Dividends payable | 2,400 | |

| Unearned rental fees | 5,160 | |

| Income taxes payable | 10,896 | |

| Capital stock | 240,000 | |

| Retained earnings | 13,944 | |

| Totals | 399,720 | 399,720 |

Table (9)

Explanation of Solution

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

f.

Describe whether the declined cash balance appears to be headed for insolvency in the near future.

f.

Explanation of Solution

- The company does not appear to face any instant solvency problems. This is because during the month of December the company commenced cash with $240,000 and out of which it spent $168,000 on equipment and left only $72,000 to begin its operation. However, on the end of the month the company had $78,000 cash. Hence, the company generated $6,000 of cash flow from operations during its first month of operations.

- The notes payable of $120,000 is due on November 30, Year 2 and it is the single obligation of the company and it does raise a potential concern about the solvency of the company. However, to satisfy this obligation, the business does not have sufficient liquid assets currently.

- On the other hand, the working capital of the company is negative by $31,056

g.

Describe whether it would be ethical for Person D to maintain the accounting records for the company or whether it must be maintained by someone who is independent of the organization.

g.

Explanation of Solution

Person D (the stockholder) can maintain the accounting records for the company and it is ethical. This is because, in most businesses, usually the accounting records are maintained either by owners or employees.

The concept of independence denotes auditing the financial statements, in which the auditor has to make an independent evaluation of the statements referred as fairness.” Independence does not apply to the routine maintenance of accounting records.

Want to see more full solutions like this?

Chapter 5 Solutions

Connect Access Card for Financial and Managerial Accounting

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education