1.

Provide a multi-step income statement for the year 2016.

1.

Explanation of Solution

Multi step income statement: A multiple step income statement refers to the income statement that shows the operating and non-operating activities of the business under separate head. In different steps of the multi-step income statement, principal operating activities are reported that starts from the record of sales revenue with all contra sales revenue account like sales returns, allowances and sales discounts.

Provide a multi-step income statement for the year 2016.

| Company R | ||

| Multi-Step Income Statement | ||

| For the Year Ended December 31, 2016 | ||

| Particulars | Amount | Amount |

| ($) | ($) | |

| Sales revenue | $200,000 | |

| Less: Cost of goods sold | ($121,120) | |

| Gross profit | $78,880 | |

| Less: Operating expenses | ||

| Selling expenses | ($26,000) | |

| Administrative expenses | ($16,000) | |

| ($7,000) | ||

| Operating expenses | ($49,000) | |

| Operating income | $29,880 | |

| Other revenues and expenses: | ||

| Interest revenue | $1,000 | |

| Interest expense | ($4,880) | |

| Loss due to flood | ($8,000) | ($11,880) |

| Income before taxes | $18,000 | |

| Less: Income taxes @30% | ($5,400) | |

| Net income | $12,600 | |

| Components of income | Earnings per common share | |

| Net income | $2.52 | |

Table (1)

2.

Provide a schedule that discloses the revenues, profits, and assets of divisions 1 and 2 and the remaining operating segments.

2.

Explanation of Solution

Provide a schedule that discloses the revenues, profits, and assets of divisions 1 and 2 and the remaining operating segments.

| Company R | ||||

| Industry Segment Financial Results | ||||

| For the Year Ended December 31, 2016 | ||||

| Particulars | Reportable Operating Segments | All Other Segments | Totals | |

| 1 | 2 | |||

| Total revenues (Sales) | 98,000 | 60,000 | 42,000 | 200,000 |

| Segment profit (Pretax) | 17,100 | 10,830 | 9,750 | 37,680 |

| General corporate expenses | -7,800 | |||

| Interest revenue | 1,000 | |||

| Interest expense | -4,880 | |||

| Loss due to flood | -8,000 | |||

| Income before taxes | 18,000 | |||

| Identifiable asset | 135,000 | 87,000 | 54,000 | 276,000 |

| General corporate assets | 24,000 | |||

Table (2)

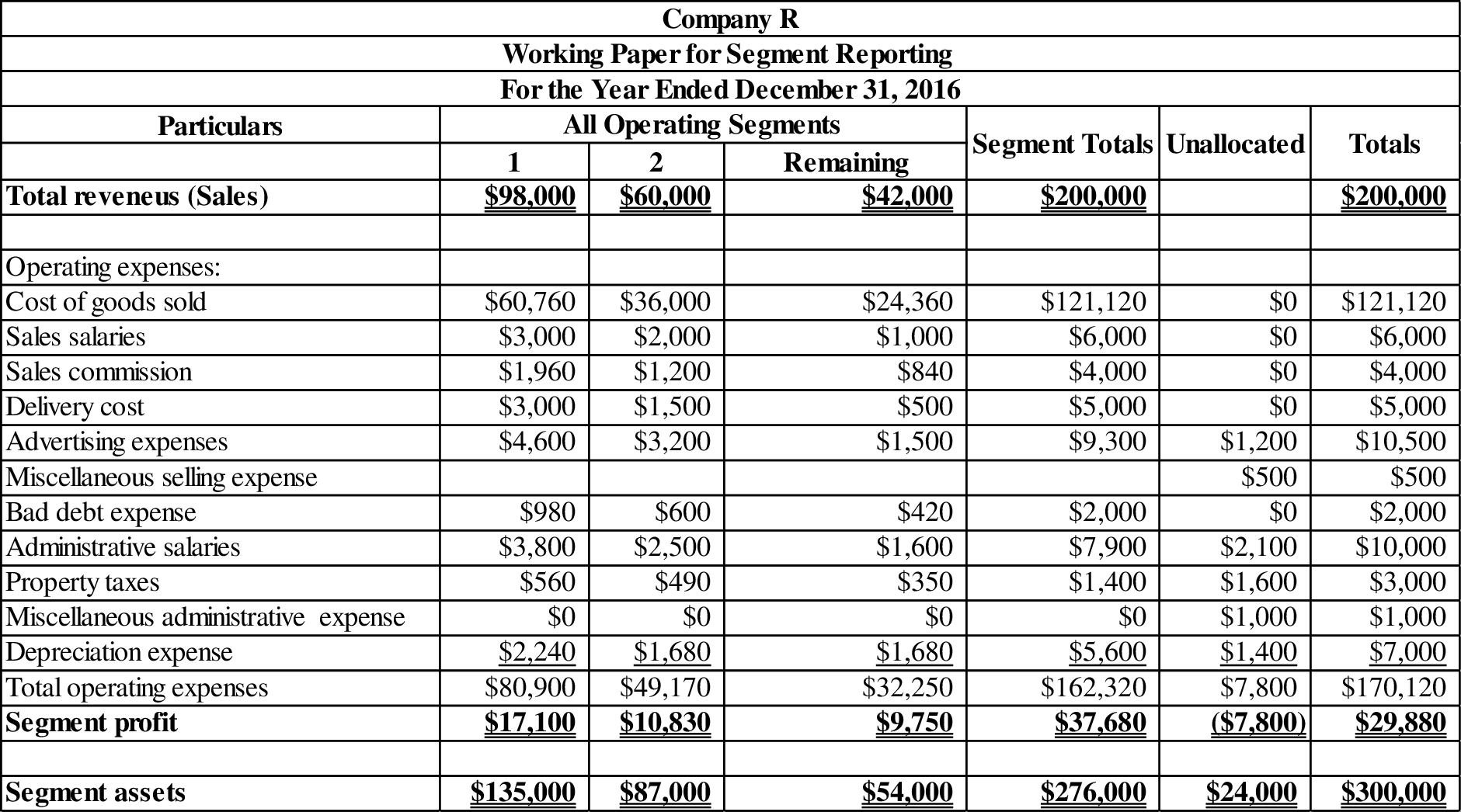

Working note (1):

Prepare a working paper for segment reporting:

Table (3)

3.

Provide a suitable segment notes related to depreciation, profit, and capital expenditures.

3.

Explanation of Solution

In the calculation of segment profit none on the following item has been added or subtracted. Formula for segment profit is as follows:

Depreciation expenses for Division 1 and 2 are $2,240 and $1,680 respectively.

In the year of 2016, capital expenditure amount of $25,000 placed in Division 1 and $6,000 placed in Division 2.

4.

Compute the profit margin before income taxes and pretax return on identifiable assets for Divisions 1 and 2 and for other divisions and evaluate the ratios.

4.

Explanation of Solution

Compute the profit margin before income taxes for Division 1:

Calculate profit margin before income taxes for Division 2:

Calculate profit margin before income taxes for other division:

Hence, the profit margin before income taxes for Division 1, 2 and other division is

Calculate pretax return on identifiable assets for Division 1:

Calculate pretax return on identifiable assets for Division 2:

Calculate pretax return on identifiable assets for other division:

Hence, the pretax return on identifiable assets Division 1, 2 and other division is

These ratios expose that the profit margin before income taxes for other division has higher margin of 23.21%.

This ratio expose that the other operating divisions have a higher pretax profit margin and pretax return on identifiable assets than the two reportable divisions. This reveals that the economic resources are used lesser in the reportable divisions.

Want to see more full solutions like this?

Chapter 5 Solutions

Bundle: Intermediate Accounting: Reporting And Analysis, 2017 Update, Loose-leaf Version, 2nd + Lms Integrated Cengagenowv2, 2 Terms Printed Access Card

- For the current year, Vidalia Company reported revenues of 250,000 and expenses of 225,000. At the beginning of the year, its retained earnings had a balance of 95,000. During the year, Vidalia paid 11,000 dividends to shareholders. Its contributed capital was 56,000 at the beginning of the year, and it did not issue any new stock during the year. Vidalias assets total 237,500 on December 31 of the current year. What are Vidalias total liabilities on December 31 of the current year?arrow_forwardJuroe Company provided the following income statement for last year: Juroes balance sheet as of December 31 last year showed total liabilities of 10,250,000, total equity of 6,150,000, and total assets of 16,400,000. Refer to the information for Juroe Company on the previous page. Also, assume that Juroes total assets at the beginning of last year equaled 17,350,000 and that the tax rate applicable to Juroe is 40%. Required: Note: Round answers to two decimal places. 1. Calculate the average total assets. 2. Calculate the return on assets.arrow_forwardPonce Towers, Inc., had 50,000 shares of common stock and 10,000 shares of 100 par value, 8% preferred stock outstanding on January 1, 2011. Each share of preferred stock is convertible into four shares of common stock. The stock has not been converted. During the year, Ponce Towers issued additional shares of common stock as follows: For 2011, Ponce Towers, Inc., had income from continuing operations of 545,000 and a 72,000 loss from discontinued operations (net of tax). As vice president of finance for the firm, you have been asked to calculate earnings per share for 2011. The worksheet EPS has been provided to assist you.arrow_forward

- Bloom Company had beginning unadjusted retained earnings of 400,000 in the current year. At the beginning of the current year, Bloom changed its inventory method from LIFO to FIFO, and the cumulative effect (net of taxes) of this change was 28,000. In addition, Bloom earned net income of 150,000 and paid dividends of 30,000 in the current year. Prepare Blooms retained earnings statement for the current year.arrow_forwardOn December 31, 2016, the end of the fiscal year, California Microtech Corporation completed the sale of its semiconductor business for $10 million. The business segment qualifies as a component of the entity according to GAAP. The book value of the assets of the segment was $8 million. The loss from operations of the segment during 2016 was $3.6 million. Pretax income from continuing operations for the year totaled $5.8 million. The income tax rate is 30%. Prepare the lower portion of the 2016 income statement beginning with pretax income from continuing operations. Ignore EPS disclosures.arrow_forwardFinley Corporation had income from continuing operations of $10,600,000 in 2017. During 2017, it disposed of its restaurant division at an after-tax loss of $189,000. Prior to disposal, the division operated at a loss of $315,000 (net of tax) in 2017 (assume that the disposal of the restaurant division meets the criteria for recognition as a discontinued operation). Finley had 10,000,000 shares of common stock outstanding during 2017. Prepare a partial income statement for Finley beginning with income from continuing operations.arrow_forward

- The following are partial income statement account balances taken from the December 31, 2016, year-end trial balance of White and Sons, Inc.: restructuring costs, $300,000; interest revenue, $40,000; before-tax loss on discontinued operations, $400,000; and loss on sale of investments, $50,000. Income tax expense has not yet been recorded. The income tax rate is 40%. Prepare the lower portion of the 2016 income statement beginning with $850,000 income from continuing operations before income taxes. Include appropriate EPS disclosures. The company had 100,000 shares of common stock outstanding throughout the year.arrow_forwardThe following Income Statement information has been obtained from the books of Unlimited Liquors Corporation for the year ended March 31, 2022. The Income tax rate is 40% and the company has 50,000 shares of common stock outstanding. Sales Revenue $890,000 Cost of Goods sold 300,000 Operating expenses 220,000 Income from discontinued operations 140,000 Loss on disposal of discontinued operations 60,000 Determine the net income or loss from the discontinued segment of the company as reported on the Income Statement:arrow_forwardThe following is a partial trial balance for General Lighting Corporation as of December 31, 2018 Account title Sales revenue 2,350,000 Interest revenue 80,000 Loss on sale of investments 22,500 Cost of goods sold 1,200,000 Loss from write-down of inventory due to obsolescence 200,000 Selling expenses 300,000 General and…arrow_forward

- Company S is 80% owned by Company P. Near the end of 2015, Company S sold merchandise with a cost of $6,000 to Company P for $7,000. Company P sold the merchandise to a nonaffiliated firm in 2016 for $10,000. How much total profit should be recorded on the consolidated income statements in 2015 and 2016? How much profit should be awarded to the controlling and noncontrolling interests in 2015 and 2016?arrow_forwardThe following Income Statement information has been obtained from the books of Unlimited Liquors Corporation for the year ended March 31, 2022. The Income tax rate is 40% and the company has 50,000 shares of common stock outstanding. Sales Revenue $890,000 Cost of Goods sold 300,000 Operating expenses 220,000 Income from discontinued operations 140,000 Loss on disposal of discontinued operations 60,000 Determine the income or loss from discontinued operations as reported on the Income Statement:arrow_forwardPresented below is information related to Ivanhoe Company as of and for the year ended December 31, 2017. This was Ivanhoe Company’s first year of operations. (Ignore income tax effects.) ● Sales revenue $1,310,000 ● Cost of goods sold 640,000 ● Selling and administrative expenses 310,000 ● Loss on sale of plant assets 64,000 ● Unrealized gain on available-for-sale investments 13,000 ● Interest expense 5,000 ● Interest revenue 4,100 ● Loss on discontinued operations 3,000 ● Allocation to noncontrolling interest 8,500 ● Dividends declared and paid 27,700 Compute the following: (a) Income from continuing operations $enter a dollar amount (b) Net income $enter a dollar amount (c) Net income attributable to Ivanhoe Company’s controlling shareholders $enter a dollar amount (d) Comprehensive income $enter a dollar amount (e) Retained earnings balance at December 31,…arrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT