Concept explainers

Videos

LO2 19 Interest Rate Risk. Both Bond Bill and Bond Ted have 6.2 percent coupons, make semiannual payments, and are priced at par value. Bond Bill has 5 years to maturity, whereas Bond Ted has 25 years to maturity. If interest rates suddenly rise by 2 percent, what is the percentage change in the price of Bond Bill? Of Bond Ted? Both bonds have a par value of $1,000. If rates were to suddenly fall by 2 percent instead, what would the percentage change in the price of Bond Bill be then? Of Bond Ted? Illustrate your answers by graphing

To determine: The percentage change in bond price.

Introduction:

A bond refers to the debt securities issued by the governments or corporations for raising capital. The borrower does not return the face value until maturity. However, the investor receives the coupons every year until the date of maturity.

Bond price or bond value refers to the present value of the future cash inflows of the bond after discounting at the required rate of return.

Answer to Problem 19QP

The percentage change in bond price is as follows:

| Yield to maturity | Bond B | Bond T |

| 4.2% | 8.94% | 30.77% |

| 8.2% | (8.071%) | (21.12%) |

The interest rate risk is high for a bond with longer maturity, and the interest rate risk is low for a bond with shorter maturity period. The maturity period of Bond B is 5 years, and the maturity period of Bond T is 25 years. Hence, the Bond T’s bond price fluctuates higher than the bond price of Bond B due to longer maturity.

Explanation of Solution

Given information:

There are two bonds namely Bond B and Bond T. The coupon rate of both the bonds is 6.2 percent. The bonds pay the coupons semiannually. The price of the bond is equal to its par value. Assume that the par value of both the bonds is $1,000. Bond B will mature in 5 years, and Bond T will mature in 25 years.

Formulae:

The formula to calculate the bond value:

Where,

“C” refers to the coupon paid per period

“F” refers to the face value paid at maturity

“r” refers to the yield to maturity

“t” refers to the periods to maturity

The formula to calculate the percentage change in price:

Determine the current price of Bond B:

Bond B is selling at par. It means that the bond value is equal to the face value. It also indicates that the coupon rate of the bond is equal to the yield to maturity of the bond. As the par value is $1,000, the bond value or bond price of Bond B will be $1,000.

Hence, the current price of Bond B is $1,000.

Determine the current yield to maturity on Bond B:

As the bond is selling at its face value, the coupon rate will be equal to the yield to maturity of the bond. The coupon rate of Bond B is 6.2 percent.

Hence, the yield to maturity of Bond B is 6.2 percent.

Determine the current price of Bond T:

Bond T is selling at par. It means that the bond value is equal to the face value. It also indicates that the coupon rate of the bond is equal to the yield to maturity of the bond. As the par value is $1,000, the bond value or bond price of Bond T will be $1,000.

Hence, the current price of Bond T is $1,000.

Determine the current yield to maturity on Bond T:

As the bond is selling at its face value, the coupon rate will be equal to the yield to maturity of the bond. The coupon rate of Bond T is 6.2 percent.

Hence, the yield to maturity of Bond T is 6.2 percent.

The percentage change in the bond value of Bond B and Bond T when the interest rates rise by 2 percent:

Compute the new interest rate (yield to maturity) when the interest rates rise:

The interest rate refers to the yield to maturity of the bond. The initial yield to maturity of the bonds is 6.2 percent. If the interest rates rise by 2 percent, then the new interest rate or yield to maturity will be 8.2 percent

Compute the bond value when the yield to maturity of Bond B rises to 8.2 percent:

The coupon rate of Bond B is 6.2 percent, and its face value is $1,000. Hence, the annual coupon payment is $62

The yield to maturity is 8.2 percent. As the calculations are semiannual, the yield to maturity should also be semiannual. Hence, the semiannual yield to maturity is 4.1 percent

The remaining time to maturity is 5 years. As the coupon payment is semiannual, the semiannual periods to maturity are 10

Hence, the bond price of Bond B will be $919.29 when the interest rises to 8.2 percent.

Compute the percentage change in the price of Bond B when the interest rates rise to 8.2 percent:

The new price after the increase in interest rate is $919.29. The initial price of the bond was $1,000.

Hence, the percentage decrease in the price of Bond B is (8.071 percent) when the interest rates rise to 8.2 percent.

Compute the bond value when the yield to maturity of Bond T rises to 8.2 percent:

The coupon rate of Bond T is 6.2 percent, and its face value is $1,000. Hence, the annual coupon payment is $62

The yield to maturity is 8.2 percent. As the calculations are semiannual, the yield to maturity should also be semiannual. Hence, the semiannual yield to maturity is 4.1 percent

The remaining time to maturity is 25 years. As the coupon payment is semiannual, the semiannual periods to maturity are 50

Hence, the bond price of Bond T will be $788.8075 when the interest rises to 8.2 percent.

Compute the percentage change in the price of Bond T when the interest rates rise to 8.2 percent:

The new price after the increase in interest rate is $788.8075. The initial price of the bond was $1,000.

Hence, the percentage decrease in the price of Bond T is (21.12 percent) when the interest rates rise to 8.2 percent.

The percentage change in the bond value of Bond B and Bond T when the interest rates decline by 2 percent:

Compute the new interest rate (yield to maturity) when the interest rates decline:

The interest rate refers to the yield to maturity of the bond. The initial yield to maturity of the bonds is 6.2 percent. If the interest rates decline by 2 percent, then the new interest rate or yield to maturity will be 4.2 percent

Compute the bond value when the yield to maturity of Bond B declines to 4.2 percent:

The coupon rate of Bond B is 6.2 percent, and its face value is $1,000. Hence, the annual coupon payment is $62

The yield to maturity is 4.2 percent. As the calculations are semiannual, the yield to maturity should also be semiannual. Hence, the semiannual yield to maturity is 2.1 percent

The remaining time to maturity is 5 years. As the coupon payment is semiannual, the semiannual periods to maturity are 10

Hence, the bond price of Bond B will be $1,089.36 when the interest declines to 4.2 percent.

Compute the percentage change in the price of Bond B when the interest rates decline to 4.2 percent:

The new price after the increase in interest rate is $1,089.36. The initial price of the bond was $1,000.

Hence, the percentage increase in the price of Bond B is 8.94 percent when the interest rates decline to 4.2 percent.

Compute the bond value when the yield to maturity of Bond T declines to 4.2 percent:

The coupon rate of Bond T is 6.2 percent, and its face value is $1,000. Hence, the annual coupon payment is $62

The yield to maturity is 4.2 percent. As the calculations are semiannual, the yield to maturity should also be semiannual. Hence, the semiannual yield to maturity is 2.1 percent

The remaining time to maturity is 25 years. As the coupon payment is semiannual, the semiannual periods to maturity are 50

Hence, the bond price of Bond T will be $1,307.73 when the interest declines to 4.2 percent.

Compute the percentage change in the price of Bond T when the interest rates decline to 4.2 percent:

The new price after the increase in interest rate is $1,307.73. The initial price of the bond was $1,000.

Hence, the percentage increase in the price of Bond T is 30.77 percent when the interest rates decline to 4.2 percent.

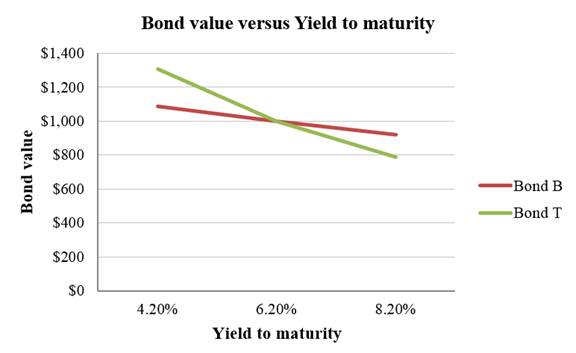

A summary of the bond prices and yield to maturity of Bond B and Bond T:

Table 1

|

Yield to maturity |

Bond B | Bond T |

| 4.2% | $1,089.36 | $1,307.73 |

| 6.2% | $1,000.00 | $1,000.00 |

| 8.2% | $919.29 | $788.81 |

A graph indicating the relationship between bond prices and yield to maturity based on Table 1:

Interpretation of the graph:

The above graph indicates that the price fluctuation is higher in a bond with higher maturity. Bond T has a maturity period of 25 years. As its maturity period is longer, its price sensitivity to the interest rates is higher. Bond B has a maturity period of 5 years. As its maturity period is shorter, its price sensitivity to the interest rates is lower. Hence, a bond with longer maturity is subject to higher interest rate risk.

Want to see more full solutions like this?

Chapter 6 Solutions

Loose Leaf for Essentials of Corporate Finance

- D6 Assume you own a 2-year US Treasury Note with a 5% coupon and a 7-year US Treasury Note with a 0% coupon. If market interest rates decrease by 100 basis points in the 2-year maturity and declined by only 75 basis points in the 7-year maturity, which bond would experience the smallest market value change? a. 5% US Treasury due in 2 years b. 0% US Treasury due in 7 years c. Both would change by the same amount d. Prices would not change since the coupons are fixedarrow_forwardD3) Finance Suppose that there is 30-year coupon bond with par value of $100 and Macaulay duration of 20.56. The coupon rate is unknown. Currently, the bond is traded at $90 and the yield is flat at 20% pa. Yield to maturity is an annualized simple interest rate compounded annually. If the bond yield increases by 50 basis points, what is the approximation of the percentage capital gain or loss? Please choose the correct range for the percentage capital gain/loss, i.e., if it is -3.5%, please select “A value between -3% and -4%” A value between -9% and -10% A value between -8% and -9% None of the other answers are correct. A value between -7% and -8% A value between -10% and -11%arrow_forward3. Bond Prices (LO2) Malahat Inc. has 7.5% coupon bonds on the market that have ten years left to maturity. the bond make annual payments. If the YTM on these bonds is 8.75%, what is the current bond price?arrow_forward

- 39. A government treasury bond with 5-year tenor carries a 4.5% coupon. Normally, government treasury bonds carry a 1.5% maturity risk premium. Assuming an inflation premium of 0.65%, how much is the real risk-free rate? Answer should be with 2 decimal points without the percentage sign (e.g., 3.00).arrow_forward6. Pure expectations theory The pure expectations theory, or the expectations hypothesis, asserts that long-term interest rates can be used to estimate future short-term interest rates. A. Based on the pure expectations theory, is the following statement true or false? The pure expectations theory assumes that a one-year bond purchased today will have the same return as a one-year bond purchased five years from now. False True B. The yield on a one-year Treasury security is 5.8400%, and the two-year Treasury security has a 8.7600% yield. Assuming that the pure expectations theory is correct, what is the market’s estimate of the one-year Treasury rate one year from now? (Note: Do not round your intermediate calculations.) 14.936% 13.4071% 11.7606% 9.9965% C. Recall that on a one-year Treasury security the yield is 5.8400% and 8.7600% on a two-year Treasury security. Suppose the one-year security does not have a…arrow_forwardHW#3 Consider a coupon bond that has a $1,000 par value and a coupon rate of 10%. The bond is currently selling for $1,150 and has 8 years to maturity. What is the bond’s yield to maturity? A 10-year, 7% coupon bond with a face value of $1,000 is currently selling for $871.65. Compute your rate of return if you sell the bond next year for $880.10. Consider the decision to purchase either a 5-year corporate bond or a 5-year municipal bond. The corporate bond is a 12% annual coupon bond with a par value of $1,000. It is currently yielding 5%. The municipal bond has an 8.5% annual coupon and a par value of $1,000. It is currently yielding 7%. Which of the two bonds would be more beneficial to you? Assume that your marginal tax rate is 35%. Calculate the duration of a $1,000 6% coupon bond with three years to maturity. Assume that all market interest rates are 7%. Consider the bond in the previous question. Calculate the expected price change if interest rates drop to 6.75% using the…arrow_forward

- Q1: A 20-year bond has a coupon rate of 8 percent, and another bond of the same maturity has a coupon rate of 15 percent. If the bonds are alike in all other respects, which will have the greater relative market price decline if interest rates increase sharply? Why?arrow_forward5. A coupon bond has a $1000 face value and a 12% coupon rate. It is currently sold at 5940 and is expe cted to be sold at 5960 next year. What is the yield to maturity and the expected rate of capital gain? lf the inflation rate is 4%, what is the real interest rate on this bond? 6. Suppose the Fed is about to have a new chair who thinks the current rate of money growth is too fast. Discuss all the possible scenarios for what will happen to interest ratesarrow_forward26. Assume that you wish to purchase a 30-year bond that has a maturity value of P1,000 and a coupon interest rate of 9.5%, paid semiannually. If you require a 6.75% rate of return on this investment, what is the maximum price that you should be willing to pay for this bond? a. P1,352 b. P1,450 c. P1,111 d. P675arrow_forward

- Q.2 A firm sells bonds with a par value of 1000 Rupees, carry a 8% coupon rate, with a maturity period of 9 years. The bond sells at a yield to maturity of 9%. a) What is the interest payment you should receive each year? b) What is the selling price of the bond?arrow_forwardA2 8e with inflation rates. may i please have your reply in formula version not excel. thanks:) You have just received an inheritance of $20,000. You wish to invest in fixed income securities such as bonds, which you think are less risky than stocks. After some research, you have narrowed down your choices to the following three fixed income securities: One-year Treasury Bill: Face value of $1000 Yield to maturity of 1.74% Coupon Bond A: Two years to maturityFace value of $1000Coupon rate of 3%, with semi-annual coupon paymentsPrice multiple of face value = 1.0189 Coupon Bond B: Five years to maturityFace value of $1000Coupon rate of 3.5%, with annual coupon paymentsYield to maturity of 2.51% All yields to maturity are compounded semi-annually. Adjusting real interest rate for inflation: (1 + real yield) = (1 + nominal yield) / (1 + inflation rate) One Year Treasury Bill: 1 + real yield = 1.0174 / 1.015 1 + real yield = 1.002365 Real yield = 1.002365 – 1 = .2365% Coupon…arrow_forwardD4) About rate of return For a consol that pays $100 annually, if the yield to maturity at the beginning of the year is 10%, and the yield to maturity at the end of the year is 5%, please calculate the return of the consol of this year. If a coupon bond that is going to mature in two years is selling at par. Suppose its coupon rate is 10%, the yield to maturity at the begging of the year is 10%, and the yield to maturity at the end of the year is 5%. Please calculate the return of the coupon bond of this year.arrow_forward