2.

Prepare

2.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in

stockholders’ equity accounts. - Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Prepare journal entry for the given transactions in a general journal.

| General Journal Page 3 | ||||||

| Date | Accounts Title and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| 2020 | ||||||

| January | 2 | Supplies | 121 | 7,000 | ||

| Cash | 101 | 7,000 | ||||

| (To record purchases of supplies for cash) | ||||||

| 2 | Prepaid Insurance | 134 | 8,400 | |||

| Cash | 101 | 8,400 | ||||

| (To record purchases of insurance for one year) | ||||||

| 7 | Cash | 101 | 20,000 | |||

| Accounts Receivable | 111 | 5,000 | ||||

| Fees Income | 401 | 25,000 | ||||

| (To record services performed for cash and account) | ||||||

| 12 | Cash | 101 | 4,000 | |||

| Accounts Receivable | 111 | 4,000 | ||||

| (To record receipts of cash on account) | ||||||

| 12 | Advertising Expense | 526 | 3,600 | |||

| Cash | 101 | 3,600 | ||||

| (To record payment of advertising on radio) | ||||||

| 13 | Cash | 101 | 4,500 | |||

| Accounts Receivable | 111 | 4,500 | ||||

| (To record receipts of cash on account) | ||||||

| 14 | Cash | 101 | 750 | |||

| Supplies | 121 | 750 | ||||

| (To record damage supplies return for cash) | ||||||

| 15 | Cash | 101 | 20,700 | |||

| Accounts Receivable | 111 | 2,300 | ||||

| Fees Income | 401 | 23,000 | ||||

| (To record services performed for cash and account) | ||||||

Table (1)

| General Journal Page 4 | ||||||

| Date | Account Title and Explanation | Post. Ref. | Debit ($) | Credit ($) | ||

| 2020 | ||||||

| January | 20 | Supplies | 121 | 5,000 | ||

| Accounts Payable | 202 | 5,000 | ||||

| (To record purchases of supplies on account) | ||||||

| 20 | Cash | 101 | 12,500 | |||

| Accounts Receivable | 111 | 3,500 | ||||

| Fees Income | 401 | 16,000 | ||||

| (To record services performed for cash and account) | ||||||

| 20 | Cash | 101 | 5,600 | |||

| Accounts Receivable | 111 | 5,600 | ||||

| (To record the collection on account) | ||||||

| 21 | Maintenance Expense | 529 | 7,065 | |||

| Cash | 101 | 7,065 | ||||

| (To record the payment for maintenance on equipment) | ||||||

| 22 | Advertising Expense | 526 | 3,600 | |||

| Cash | 101 | 3,600 | ||||

| (To record payment of cash for newspaper ads) | ||||||

| 23 | Telephone Expense | 532 | 1,025 | |||

| Cash | 101 | 1,025 | ||||

| (To Record the payment of telephone bill) | ||||||

| 26 | Cash | 101 | 1,600 | |||

| Accounts Receivable | 111 | 1,600 | ||||

| (To record the collection on account) | ||||||

| 27 | Accounts Payable | 202 | 3,000 | |||

| Cash | 101 | 3,000 | ||||

| (To record the payment to creditors) | ||||||

Table (2)

| General Journal Page 5 | ||||||

| Date | Accounts Title and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| 2020 | ||||||

| January | 28 | Utilities Expense | 514 | 2,675 | ||

| Cash | 101 | 2,675 | ||||

| (To record the payment of utility bill) | ||||||

| 29 | Cash | 101 | 19,000 | |||

| Accounts Receivable | 111 | 2,750 | ||||

| Fees Income | 401 | 21,750 | ||||

| (To record services performed for cash and account) | ||||||

| 31 | Salaries Expense | 511 | 32,800 | |||

| Cash | 101 | 32,800 | ||||

| (To record payment of monthly salaries) | ||||||

| 31 | TE, Drawing | 302 | 12,000 | |||

| Cash | 101 | 12,000 | ||||

| (To record withdrawal of cash for personal use) | ||||||

| 31 | Maintenance Expense | 529 | 4,150 | |||

| Cash | 101 | 4,150 | ||||

| (To record payment of monthly maintenance services) | ||||||

| 31 | Equipment | 141 | 15,000 | |||

| Cash | 101 | 10,000 | ||||

| Accounts Payable | 202 | 5,000 | ||||

| (To record the purchases of equipment for cash and on account) | ||||||

| 31 | Cash | 101 | 7,600 | |||

| Accounts Receivable | 111 | 1,620 | ||||

| Fees Income | 401 | 9,220 | ||||

| (To record services performed for cash and account) | ||||||

Table (3)

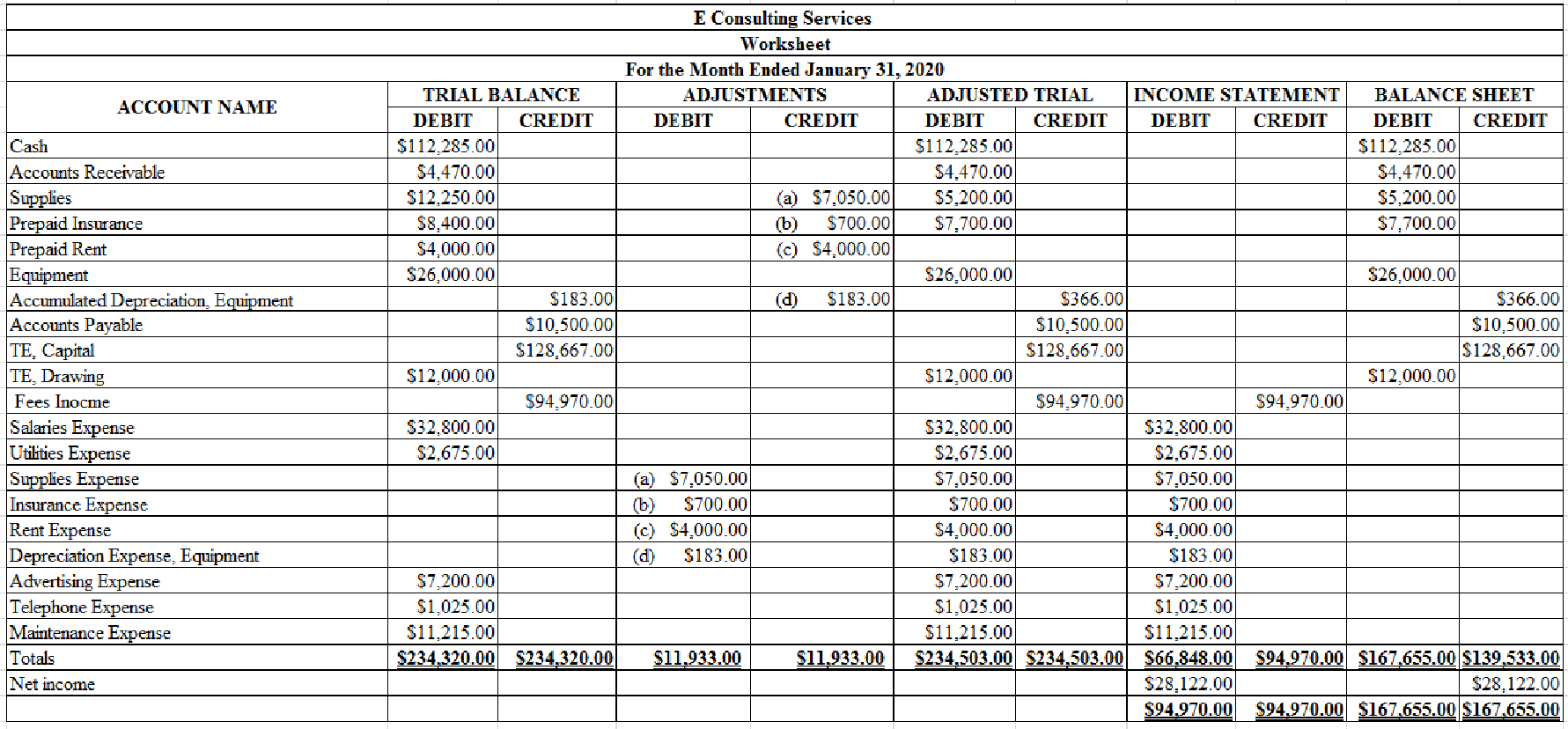

4, 5 and 6.

Prepare trail balance section, indicate the given adjustments, and complete the worksheet for E Consulting Services for the month ended January 31, 2020.

4, 5 and 6.

Explanation of Solution

Worksheet: Worksheet is an accounting tool that helps accountants to record adjustments and up-date balances required to prepare financial statements. Worksheet is a central place where

Prepare trail balance section, indicate the given adjustments, and complete the worksheet for E Consulting Services for the month ended January 31, 2020.

Table (4)

7.

Prepare income statement for E Consulting Services for the month ended January 31, 2020.

7.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operation and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare income statement for E Consulting Services for the month ended January 31, 2020.

| E Consulting Services | ||

| Income Statement | ||

| For the Month Ended January 31, 2020 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Fees Income | 94,970 | |

| Expenses: | ||

| Salaries Expense | 32,800 | |

| Utilities Expense | 2,675 | |

| Supplies Expense | 7,050 | |

| Rent Expense | 4,000 | |

| Insurance Expense | 700 | |

| | 183 | |

| Advertising Expense | 7,200 | |

| Telephone Expense | 1,025 | |

| Maintenance Expense | 11,215 | |

| Total expenses | 66,848 | |

| Net income | $28,122 | |

Table (5)

8.

Prepare statement of owners’ equity for E Consulting Services for the month ended January 31, 2020.

8.

Explanation of Solution

Statement of owners’ equity: This statement reports the beginning owner’s equity and all the changes which led to ending owners’ equity. Additional capital, net income from income statement is added to, and drawings are deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Prepare a statement of owners’ equity for E Consulting Services for the month ended January 31, 2020.

| E Consulting Services | ||

| Statement of Owners’ Equity | ||

| For the Month Ended January 31, 2020 | ||

| Particulars | Amount ($) | Amount ($) |

| TE, Capital, January 1, 2020 | $128,667 | |

| Net income for January | 28,122 | |

| Less: Withdrawals for January | 12,000 | |

| Increase in capital | 16,122 | |

| HK, Capital, January 31, 2020 | $144,789 | |

Table (6)

9.

Prepare balance sheet for E Consulting Services as at January 31, 2020.

9.

Explanation of Solution

Balance sheet: This financial statement reports a company’s resources (assets) and claims of creditors (liabilities) and owners (owners’ equity) over those resources. The resources of the company are assets which include money contributed by owners and creditors. Hence, the main elements of the balance sheet are assets, liabilities, and owners’ equity.

Prepare the balance sheet for E Consulting Services as at January 31, 2020.

| E Consulting Services | ||

| Balance Sheet | ||

| January 31, 2019 | ||

| Assets | ||

| Cash | $112,285 | |

| Accounts Receivable | 4,470 | |

| Supplies | 5,200 | |

| Prepaid Insurance | 7,700 | |

| Equipment | $26,000 | |

| Less: | 336 | 25,634 |

| Total Assets | $155,289 | |

| Liabilities and owner’s equity | ||

| Liabilities | ||

| Accounts Payable | 10,500 | |

| Owners’ Equity | ||

| TE, Capital | 144,789 | |

| Total Liabilities and Owners’ Equity | $155,289 | |

Table (7)

10.

Prepare adjusting entry for the given adjustments.

10.

Explanation of Solution

Prepare adjusting entry for supplies.

| GENERAL JOURNAL | Page 6 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 31, 2019 | Supplies expense | 517 | 7,050 | |

| Supplies | 121 | 7,050 | ||

| (to record supplies used) | ||||

Table (8)

Description:

- Supplies Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Supplies are an asset account. Since amount of supplies is used, asset account decreased, and a decrease in asset is credited.

Prepare adjusting entry for insurance expense:

| GENERAL JOURNAL | Page 6 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 31, 2019 | Insurance expense | 535 | 700 | |

| Prepaid insurance | 134 | 700 | ||

| (to record part of prepaid insurance expired) | ||||

Table (9)

Description:

- Insurance Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Prepaid Insurance is an asset account. Since amount of insurance is expired, asset account decreased, and a decrease in asset is credited.

Prepare adjusting entry for rent expense:

| GENERAL JOURNAL | Page 6 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 31, 2019 | Rent expense | 520 | 4,000 | |

| Prepaid rent | 137 | 4,000 | ||

| (to record part of prepaid rent expired) | ||||

Table (10)

Description:

- Rent Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Prepaid Rent is an asset account. Since amount of rent is expired, asset account decreased, and a decrease in asset is credited.

Prepare adjusting entry for depreciation expense-equipment:

| GENERAL JOURNAL | Page 6 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 31, 2019 | Depreciation expense-Equipment | 523 | 183 | |

| Accumulated depreciation-Equipment | 142 | 183 | ||

| (to record depreciation expense) | ||||

Table (11)

Description:

- Depreciation Expense, Equipment is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Accumulated Depreciation, Equipment is a contra-asset account, and contra-asset accounts would have a normal credit balance, hence, the account is credited.

11.

Prepare closing entries in general ledger.

11.

Explanation of Solution

Closing entries: The journal entries prepared to close the temporary accounts to capital account are referred to as closing entries. The revenue, expense, and drawing accounts are referred to as temporary accounts because the information and figures in these accounts is held temporarily and consequently transferred to permanent account at the end of accounting year.

Steps in closing procedure:

- 1. Close the revenue accounts to Income Summary account.

- 2. Close the expense accounts to Income Summary account.

- 3. Close the Income Summary account and transfer the net income or net loss balance to the Capital account.

- 4. Close the Drawing account to Capital account.

Close the revenue accounts to Income Summary account.

| GENERAL JOURNAL | Page 6 | |||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| 2019 | Fees Income | 401 | 94,970 | |||

| January | 31 | Income Summary | 309 | 94,970 | ||

| (Record closing of revenue to Income Summary account) | ||||||

Table (12)

Description:

- Fees income is a revenue account. Revenue account has a normal credit balance. Since revenue is closed to Income Summary account, the account is debited.

- Income Summary is a clearing account which closes revenue, expense, drawings, and net of revenues and expenses to capital accounts. The account is credited to hold the transferred balance from revenue account.

Close the expense accounts to Income Summary account.

| GENERAL JOURNAL | Page 6 | |||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| 2019 | Income Summary | 309 | 19,980 | |||

| January | 31 | Salaries Expense | 511 | 32,800 | ||

| Utilities Expense | 514 | 2,675 | ||||

| Supplies Expense | 517 | 7,050 | ||||

| Rent Expense | 520 | 4,000 | ||||

| Depreciation Expense, Equipment | 523 | 183 | ||||

| Advertising Expense | 526 | 7,200 | ||||

| Maintenance Expense | 529 | 11,215 | ||||

| Telephone Expense | 532 | 1,025 | ||||

| Insurance Expense | 535 | 700 | ||||

| (Record closing of expenses to Income Summary account) | ||||||

Table (13)

Description:

- Income Summary is a clearing account which closes revenue, expense, drawings, and net of revenues and expenses to capital accounts. The account is debited to hold the transferred balance from expense accounts.

- Salaries expense, Utilities expense, Supplies expense, Rent expense, Depreciation expense, Advertising expense, Maintenance expense, Telephone expense, and Insurance expense are expense accounts. Expense account has a normal debit balance. Since expenses are closed to Income Summary account, the accounts are credited.

Close the net income to Income Summary account.

| GENERAL JOURNAL | Page 6 | |||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| 2019 | Income Summary | 309 | 28,122 | |||

| January | 31 | TE, Capital | 301 | 28,122 | ||

| (Record closing of net income to capital account) | ||||||

Table (14)

Description:

- Income Summary is a clearing account which closes revenue, expense, drawings, and net of revenues and expenses to capital accounts. Since net income is closed, the account is reversed; hence, the Income Summary account is debited.

- TE, Capital is a capital account. Since net income is transferred to the account, the value increased, and an increase in capital is credited.

Working Note 1:

Compute net income.

Close the Drawing account to Capital account.

| GENERAL JOURNAL | Page 6 | |||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| 2019 | TE, Capital | 12,000 | ||||

| January | 31 | TE, Drawing | 12,000 | |||

| (Record closing of drawing to capital account) | ||||||

Table (15)

Description:

- TE, Capital is a capital account. Since drawings are transferred to the account, the value decreased, and a decrease in capital is debited.

- TE, Drawing is a capital account. Since drawings are transferred, the account is credited to reverse the previously debited effect.

1, 3, 10, and 11.

Open the general ledger account, enter the balance for January 1, 2020, and

1, 3, 10, and 11.

Explanation of Solution

Open the general ledger account, enter the balance for January 1, 2020, and post the journal entries, adjusting entries, and closing entries.

| ACCOUNT: Cash ACCOUNT NO. 101 | |||||||

| DATE | Item | Post Ref. | Debit ($) | Credit ($) | BALANCE | ||

| Debit ($) | Credit ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 111,350 | |||

| 2 | J3 | 7,000 | 104,350 | ||||

| 2 | J3 | 8,400 | 95,950 | ||||

| 7 | J3 | 20,000 | 115,950 | ||||

| 12 | J3 | 4,000 | 119,950 | ||||

| 12 | J3 | 3,600 | 116,350 | ||||

| 13 | J3 | 4,500 | 120,850 | ||||

| 14 | J3 | 750 | 121,600 | ||||

| 15 | J4 | 20,700 | 142,300 | ||||

| 20 | J4 | 12,500 | 154,800 | ||||

| 20 | J4 | 5,600 | 160,400 | ||||

| 21 | J4 | 7,065 | 153,335 | ||||

| 22 | J4 | 3,600 | 149,735 | ||||

| 23 | J4 | 1,025 | 148,710 | ||||

| 26 | J4 | 1,600 | 150,310 | ||||

| 27 | J5 | 3,000 | 147,310 | ||||

| 28 | J5 | 2,675 | 144,635 | ||||

| 29 | J5 | 19,000 | 163,635 | ||||

| 31 | J5 | 32,800 | 130,835 | ||||

| 31 | J5 | 12,000 | 118,835 | ||||

| 31 | J5 | 4,150 | 114,685 | ||||

| 31 | J5 | 10,000 | 104,685 | ||||

| 31 | J5 | 7,600 | 112,285 | ||||

Table (16)

| ACCOUNT: Accounts Receivable ACCOUNT NO. 111 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

|

DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 5,000 | |||

| 7 | J3 | 5,000 | 10,000 | ||||

| 12 | J3 | 4,000 | 6,000 | ||||

| 13 | J3 | 4,500 | 1,500 | ||||

| 15 | J4 | 2,300 | 3,800 | ||||

| 20 | J4 | 3,500 | 7,300 | ||||

| 20 | J4 | 5,600 | 1,700 | ||||

| 26 | J4 | 1,600 | 100 | ||||

| 29 | J5 | 2,750 | 2,850 | ||||

| 31 | J5 | 1,620 | 4,470 | ||||

Table (17)

| ACCOUNT: Supplies ACCOUNT NO. 121 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 1,000 | |||

| 2 | J3 | 7,000 | 8,000 | ||||

| 14 | J3 | 750 | 7250 | ||||

| 20 | J4 | 5,000 | 12,250 | ||||

| 31 | Adjusting | J6 | 7,050 | 5,200 | |||

Table (18)

| ACCOUNT: Accounts Payable ACCOUNT NO. 202 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 3,500 | |||

| 20 | J4 | 5,000 | 8,500 | ||||

| 27 | J5 | 3,000 | 5,500 | ||||

| 31 | J5 | 5,000 | 10,500 | ||||

Table (19)

| ACCOUNT: TE, Capital ACCOUNT NO. 301 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 128,667 | |||

| 31 | Closing | J6 | 34,597 | 163,264 | |||

| 31 | Closing | J6 | 15,000 | 148,264 | |||

Table (20)

| ACCOUNT: TE, Drawing ACCOUNT NO. 302 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | J5 | 12,000 | 12,000 | |||

| 31 | Closing | J6 | 12,000 | ||||

Table (21)

| ACCOUNT: Prepaid Insurance ACCOUNT NO. 134 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 2 | J3 | 8,400 | 8,400 | |||

| 31 | Adjusting | J6 | 700 | 7,700 | |||

Table (22)

| ACCOUNT: Prepaid Rent ACCOUNT NO. 137 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 4,000 | |||

| 31 | Adjusting | J6 | 4,000 | ||||

Table (23)

| ACCOUNT: Equipment ACCOUNT NO. 141 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 11,000 | |||

| 31 | J5 | 15,000 | 26,000 | ||||

Table (24)

| ACCOUNT: Accumulated Depreciation-Equipment ACCOUNT NO. 142 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 183 | |||

| 31 | Adjusting | J6 | 183 | 366 | |||

Table (25)

| ACCOUNT: Income Summary ACCOUNT NO. 309 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | Closing | J6 | 94,970 | 94,970 | ||

| 31 | Closing | J6 | 66,848 | 28,122 | |||

| 31 | Closing | J6 | 28,122 | ||||

Table (26)

| ACCOUNT: Fees Income ACCOUNT NO. 401 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 7 | J3 | 25,000 | 25,000 | |||

| 15 | J4 | 23,000 | 48,000 | ||||

| 20 | J4 | 16,000 | 64,000 | ||||

| 29 | J5 | 21,750 | 85,750 | ||||

| 31 | J5 | 9,220 | 94,970 | ||||

| 31 | Closing | J6 | 94,970 | ||||

Table (27)

| ACCOUNT: Salaries Expense ACCOUNT NO. 511 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | J5 | 32,800 | 32,800 | |||

| 31 | Closing | J6 | 32,800 | ||||

Table (28)

| ACCOUNT: Utilities Expense ACCOUNT NO. 514 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 28 | J5 | 2,675 | 2,675 | |||

| 31 | Closing | J6 | 2,675 | ||||

Table (29)

| ACCOUNT: Supplies Expense ACCOUNT NO. 517 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | Adjusting | J6 | 7,050 | 7,050 | ||

| 31 | Closing | J6 | 7,050 | ||||

Table (30)

| ACCOUNT: Rent Expense ACCOUNT NO. 520 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | Adjusting | J6 | 4,000 | 4,000 | ||

| 31 | Closing | J6 | 4,000 | ||||

Table (31)

| ACCOUNT: Depreciation Expense -Equipment ACCOUNT NO. 523 | |||||||

| DATE | ITEM | POST.REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | Adjusting | J6 | 183 | 183 | ||

| 31 | Closing | J6 | 183 | ||||

Table (32)

| ACCOUNT: Advertising Expense ACCOUNT NO. 526 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 12 | J3 | 3,600 | 3,600 | |||

| 22 | J4 | 3,600 | 7,200 | ||||

| 31 | Closing | J6 | 7200 | 0 | |||

Table (33)

| ACCOUNT: Maintenance Expense ACCOUNT NO. 529 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 21 | J4 | 7,065 | 7,065 | |||

| 31 | J5 | 4,150 | 11,215 | ||||

| 31 | Closing | J6 | 11,215 | 0 | |||

Table (34)

| ACCOUNT: Telephone Expense ACCOUNT NO. 532 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 23 | J4 | 1,025 | 1,025 | |||

| 31 | Closing | J6 | 1,025 | 0 | |||

Table (35)

| ACCOUNT: Insurance Expense ACCOUNT NO. 535 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | Adjusting | J6 | 700 | 700 | ||

| 31 | Closing | J6 | 700 | 0 | |||

Table (36)

12.

Prepare a post-closing trial balance for E Consulting Services as at January 31, 2020.

12.

Explanation of Solution

Post-closing trial balance: Post-closing trial balance is a summary of all the assets, liabilities, and capital accounts and their balances, after the closing entries are prepared. So, post-closing trial balance reports the balances of permanent accounts only.

Prepare a post-closing trial balance for E Consulting Services as at January 31, 2020.

|

E Consulting Services Post- closing Trial Balance January 31, 2020 | ||

| Account Title |

Debit ($) |

Credit ($) |

| Cash | 112,285 | |

| Accounts Receivable | 4,470 | |

| Supplies | 5,200 | |

| Prepaid Insurance | 7,700 | |

| Equipment | 26,000 | |

| Accumulated Depreciation | 366 | |

| Accounts Payable | 10,500 | |

| TE, Capital | 144,789 | |

| Total | 155,655 | 155,655 |

Table (37)

Analyze the changes of total assets, liabilities, and the ending balance of owner’s capital of by comparing the January 31, 2020 balance sheet and December 31, 2019 balance sheet.

Explanation of Solution

The total assets are increased by $23,122

The total liabilities are increased by $7,000

The Owner’s capital is increased by $16,122

Analyze the changes arisen in cash and accounts receivable accounts.

Explanation of Solution

The cash account is increased by $935

The accounts receivable account is decreased by $530

Analyze the improvement in the firm’s financial position.

Explanation of Solution

The firm’s capital is increased by $16,122

Want to see more full solutions like this?

Chapter 6 Solutions

COLLEGE ACCOUNTING ETEXT+CONNECT ACCESS

- As a bookkeeper of a new start-up company, you are responsible for keeping the chart of accounts up to date. At the end of each year, you analyze the accounts to verify that each account should be active for accumulation of costs, revenues and expenses. In July, the accounts payable clerk has asked you to open an account named “New Expenses”. You know that an account name should be specific and well defined. You feel that the A/P clerk might want to charge some expenses to that account that would not be appropriate. Why do you think the A/P clerk need this “New Expenses” account? Who needs to know this information and what action should you consider?arrow_forwardThis problem is designed to enable you to apply the knowledge you have acquired in the preceding chapters. In accounting, the ultimate test is being able to handle data in real-life situations. This problem will give you valuable experience. CHART OF ACCOUNTS You are to record transactions in a two-column general journal. Assume that the fiscal period is one month. You will then be able to complete all of the steps in the accounting cycle. When you are analyzing the transactions, think them through by visualizing the T accounts or by writing them down on scratch paper. For unfamiliar types of transactions, specific instructions for recording them are included. However, reason them out for yourself as well. Check off each transaction as it is recorded. Required 1. Journalize the transactions. (Start on page 1 of the general journal if using Excel or Working Papers.) 2. Post the transactions to the ledger accounts. (Skip this step if using CLGL.) 3. Prepare a trial balance. (If using a work sheet, use the first two columns.) 4. Data for the adjustments are as follows: a. Insurance expired during the month, 1,020. b. Depreciation of building for the month, 480. c. Depreciation of pool/slide facility for the month, 675. d. Depreciation of pool furniture for the month, 220. e. Wages accrued at July 31, 920. Your instructor may want you to use a work sheet for these adjustments. 5. Journalize adjusting entries. 6. Post adjusting entries to the ledger accounts. (Skip this step if using CLGL.) 7. Prepare an adjusted trial balance. 8. Prepare the income statement. 9. Prepare the statement of owners equity. 10. Prepare the balance sheet. 11. Journalize closing entries. 12. Post closing entries to the ledger accounts. (Skip this step if using CLGL.) 13. Prepare a post-closing trial balance. Check Figure Trial balance total, 601,941; net income, 16,293; post-closing trial balance total, 569,614arrow_forwardAssume you are a newly-hired accountant for a local manufacturing firm. You have enjoyed working for the company and are looking forward to your first experience participating in the preparation of the companys financial statements for the year-ending December 31, the end of the companys fiscal year. As you are preparing your assigned journal entries, your supervisor approaches you and asks to speak with you. Your supervisor is concerned because, based on her preliminary estimates, the company will fall just shy of its financial targets for the year. If the estimates are true, this means that all 176 employees of the company will not receive year-end bonuses, which represent a significant portion of their pay. One of the entries that you will prepare involves the upcoming bond interest payment that will be paid on January 15 of the next year. Your supervisor has calculated that, if the journal entry is dated on January 1 of the following year rather than on December 31 of the current year, the company will likely meet its financial goals thereby allowing all employees to receive year-end bonuses. Your supervisor asks you if you will consider dating the journal entry on January 1 instead of December 31 of the current year. Assess the implications of the various stake holders and explain what your answer will be.arrow_forward

- This problem is designed to enable you to apply the knowledge you have acquired in the preceding chapters. In accounting, the ultimate test is being able to handle data in real life situations. This problem will give you valuable experience. CHART OF ACCOUNTS You are to record transactions in a two-column general journal. Assume that the fiscal period is one month. You will then be able to complete all of the steps in the accounting cycle. When you are analyzing the transactions, think them through by visualizing the T accounts or by writing them down on scratch paper. For unfamiliar types of transactions, specific instructions for recording them are included. However, reason them out for yourself as well. Check off each transaction as it is recorded. Required 1. Journalize the transactions. (Start on page 1 of the general journal if using Excel or Working Papers.) 2. Post the transactions to the ledger accounts. (Skip this step if using CLGL.) 3. Prepare a trial balance. (If using a work sheet, use the first two columns.) 4. Data for the adjustments are as follows: a. Insurance expired during the month, 1,000. b. Depreciation of pool structure for the month, 715. c. Depreciation of fan system for the month, 260. d. Depreciation of sailboats for the month, 900. e. Wages accrued at June 30, 810. Your instructor may want you to use a work sheet for these adjustments. 5. Journalize adjusting entries. 6. Post adjusting entries to the ledger accounts. (Skip this step if using CLGL.) 7. Prepare an adjusted trial balance 8. Prepare the income statement 9. Prepare the statement of owners equity. 10. Prepare the balance sheet. 11. Journalize closing entries. 12. Post closing entries to the ledger accounts. (Skip this step if using CLGL.) 13. Prepare a post-dosing trial balance. Check Figure Trial balance total, 281,858; net income, 7,143; post-dosing trial balance total, 263,341arrow_forwardAssume you are a senior accountant and have been assigned the responsibility for making the entries to close the books for the year. You have prepared the following four entries and presented them to your boss, the chief financial officer of the company, along with the company CEO, in the weekly staff meeting: As the CEO was reviewing your work, he asked the question, What do these entries mean? Can we learn anything about the company from reviewing them? Provide an explanation to give to the CEO about what the entries reveal about the companys operations this year.arrow_forwardAfter completing your first degree in accounting you have been employed by XYZ Company as an account officer. The Management of the company has tasked you to implement a computerized accounting system.RequiredIn a paragraph each, address the following questions:a) Discuss five benefits associated with the implementation of the computerizedaccounting system within the company.b) Giventhattherearesomanyaccountingpackagesonthemarket,whatshouldyoube looking for when selecting a computerized accounting package for the company?Explain any five factors to considerc) Assuming you procure a Sales Ledger package, what kind of reports should weexpect? List five types of reports expected to be generated.d) Explainthedifferencebetweenastand-alonepackageandanintegratedpackage?Explain two advantaged and two disadvantages of an integrated packagee) Before a new accounting package can be deployed, it needs to be configured. What does it mean to configure an accounting package? Explain the processes…arrow_forward

- As the bookkeeper of a new start-up company, you are responsible for keeping the chart of accounts up to date. At the end of each year, you analyze the accounts to verify that each account should be active for accumulation of costs, revenues, and expenses. In July, the accounts payable clerk has asked you to open an account named New Expenses. You know that an account name should be specific and well defined. You feel that the A/P clerk might want to charge some expenses to that account that would not be appropriate. Why do you think the A/P clerk needs this New Expenses account? Who needs to know this information and what action should you consider?arrow_forwardRecord any five accounting transactions of your own choice for Ali furniture business (AFB) for the year 2019, Starting from the owner investment of $100,000. Post them in General journal, make ledger, and Trial balance for those entries. with explanation and to make it in best formate.arrow_forwardYou are a financial accountant for a small business and have been tasked with preparing a monograph for the company's financial statements. The monograph should include a list of economic events that have occurred over the course of one month, including: 1) receivables, 2)merchandising assets, 3)sales, 4)VAT, 5) prepaid expenses and revenues (these five categories have to be in your monograph as mandatory). Your list should include 15 economic events. For each economic event, you will need to create a general journal entry, post the entry to the general ledger, prepare a trial balance, and ultimately prepare the company's income statement and balance sheet. To complete this assignment, you will need to: 1. Create a list of at least 15 economic events that have occurred over the course of one month. Make sure to include the mandatory economic events mentioned above and any other important events that you can think of. 2. For each economic event, create a general journal entry and post…arrow_forward

- The first project for the semester will involve the following items to turn in: 1) Journal entries for financial transactions I will provide you. 2) An adjusted trial balance. 3) An Income statement. 1) On December 1 of 2019 Harold Hammer deposited $ 15,100 in a bank account in the name of Huaning Corporation in exchange for shares of common stock in the corporation. 2) On December 1 of 2019 Huaning Corporation purchased supplies on account for $ 226 . 3) On December 4 of 2019 Huaning Corporation received cash of $ 384 for product sold to the customer. 4) On December 5 of 2019 Huaning Corporation paid the vendor for the December 1st purchase of supplies. 5) On December 6 of 2019 Huaning Corporation purchases supplies on account for $ 469 .6) On December 8 of 2019 Huaning Corporation sells product for $ 445 on account to a customer.7) On December 9 of 2019 Huaning Corporation sells product for $ 462 on account to a customer. 8) On December 10 of 2019 Huaning Corporation paid, in…arrow_forwardRecord any five accounting transactions of your own choice for Ali furniture business (AFB) for the year 2019, Starting from the owner investment of $100,000. Post them in General journal, make ledger, and Trial balance for those entries. with explanation.arrow_forwardPrepare an explanatory memorandum about financial performance and record keeping requirements. The operations manager of Metharom Construction has asked you to prepare an explanatory memorandum for the accounting staff. They have requested that you include the following information: A) a description of a minimum of 5 financial records that the company must maintain B) any three factors while selecting software that could assist with finance management for small business C) list any 5 regulatory requirement for lodgement and payment of statutory obligations D) a set of policies to for Debt recovery procedures (minimum 3) E) explain how financial performance will be monitored (include a minimum of 2 key performance indicators) F) set of minimum 6 written financial procedures for Metharom which will help in financial health check for stakeholders G)This document must then be sent electronically to the Operations Manager (your assessor) as well as submitted in hard copy.arrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College