Videos

Refer to the data in Exercise 6-39. The president of Tiger Furnishings is confused about the differences in costs that result from using direct labor costs and machine-hours.

Required

- a. Explain why the two product costs are different.

- b. How would you respond to the president when asked to recommend one allocation base or the other?

- c. The president says to choose the allocation base that results in the highest income. Is this an appropriate basis for choosing an allocation base?

a.

Explain the difference between the two products costs.

Explanation of Solution

Product cost:

Product cost includes all the costs that are attributed to the production of the product. All the money that has spent on the process of production or purchase of the product is known as product cost.

Product cost per unit:

The product cost per unit is determined by dividing the total of variable and fixed cost with the total number of units.

Predetermined overhead rate:

The predetermined overhead rate is the rate computed for applying manufacturing overheads to the work-in-process inventory. This rate can be computed by dividing the total amount of manufacturing overheads by the base of allocation.

Difference between the two products costs:

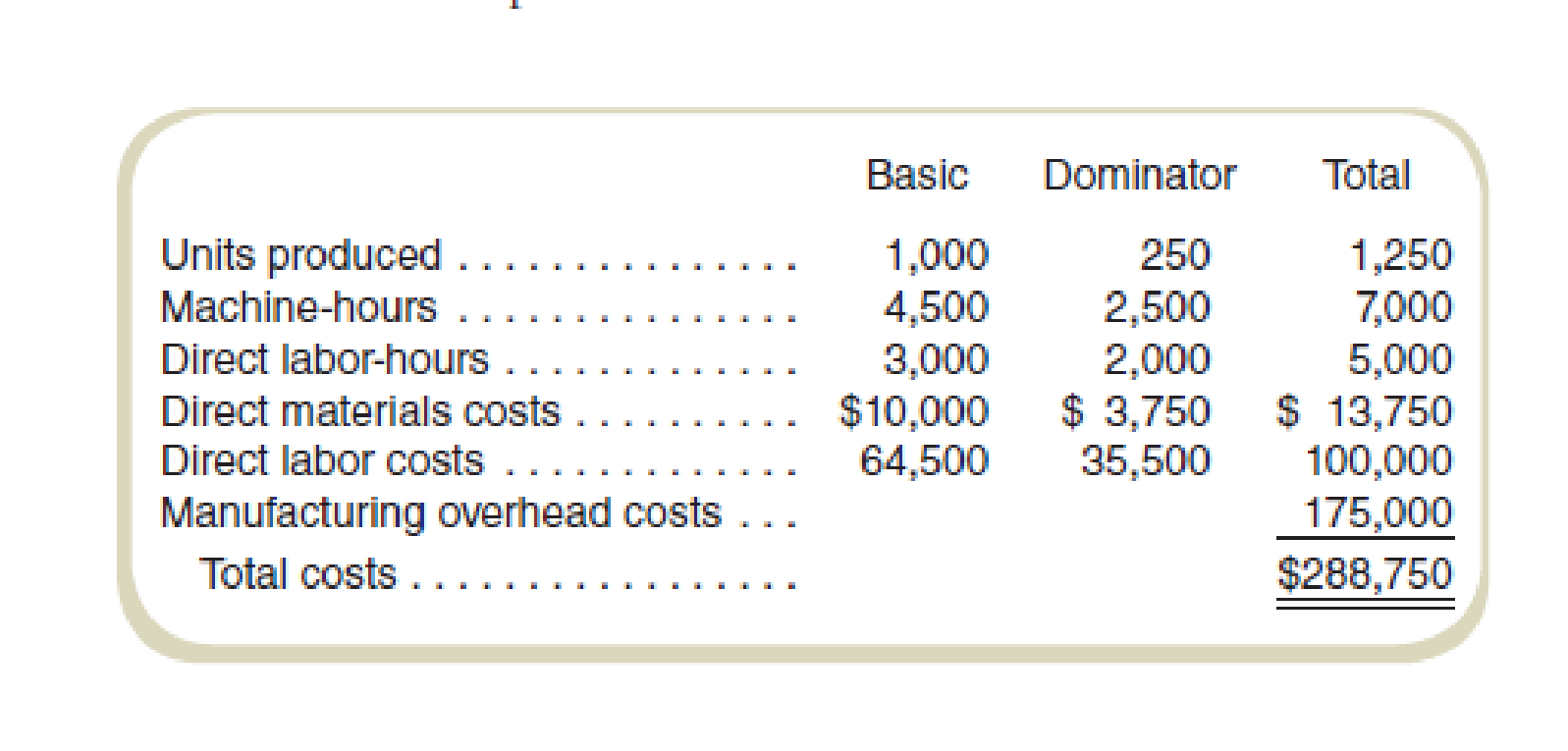

While using direct-labor costs the allocation of overheads is as follows:

For Product B: $112,875 (2)

For Product D: $62,125 (3)

And,

While using Machine-hours the allocation of overheads is as follows:

For Product B: $112,500 (5)

For Product D: $62,500 (6)

This shows the difference between the two methods of allocation is either increase or decrease of $375. This difference exists due to the different bases used for the calculation of predetermined rates. If the direct-labor costs are used then the resulting predetermined rate is $1.75 or 175% approximately. The process is oriented in terms of the base of direct-labor costs.

But, when machine-hours are used for the allocation of overheads with respect to the predetermined rate the resulting $25 will be giving a different result. The base for Compute both the predetermined rates is different.

The sum of allocation would be $175,000 for either method used for Compute cost allocation. But the allocations to both the products using the different methods would be different. The reason for this is that when direct-labor costs are used as a base the result is computed using direct-labor costs. But, when machine-hours are used as a base the computed result would be with respect to the machine-hours.

Thus, the allocation of overheads differs due to a different base of allocation used.

Working note 1:

Compute the predetermined overhead rate using direct labor costs as the base for allocation:

Working note 2:

Allocation of predetermined overhead costs using direct labor costs as the base for allocation:

For Basic:

For Dominator:

Working note 3:

The predetermined overhead rate while using machine-hours for cost allocation:

Working note 4:

Allocation of predetermined overhead costs using machine-hours as the base for allocation:

For Basic:

For Dominator:

b.

Describe the points to be taken into consideration when recommending one allocation base or the other.

Explanation of Solution

The points to be taken into consideration when recommending one allocation base or the other:

1) The method of production that is being used by the company in accordance with the operations and the availability of the resources.

2) The pooling of cost should be done but should correspond to the process of allocation that represents an accurate picture.

3) Either of the cost systems can be used as they both represent an accurate picture. But, if the product is labor intensive then the use of labor-hours cost is recommended. It would present facts clearly.

Hence, the recommendations to use any base for allocation should be in accordance with the production process. The company can use two-stage allocation for allocation of overheads.

c.

Comment on whether using the allocation base that results in the highest income is appropriate or not.

Explanation of Solution

It is not appropriate to choose the highest income generating base for the allocation of cost. The consideration should be to report the data accurately and consistently. While choosing the base to allocate the cost, the cost system should be in accordance with the base that is being used by the process and not the base which is generating more income.

Hence, the base that results in highest income should not be used as this is not an appropriate basis for choosing an allocation base.

Want to see more full solutions like this?

Chapter 6 Solutions

FUNDAMENTAL'S OF COST ACCOUNTING LL

- From the choices presented in parentheses, choose the appropriate term for completing each of the following sentences: a. A product, sales territory, department, or activity to which costs are traced is called a (direct cost, cost object). b. Advertising costs are usually viewed as (period, product) costs. c. Factory overhead costs combined with direct labor costs are called (prime, conversion) costs. d. Feedback is often used to (improve, direct) operations. e. A sacrifice made to obtain some benefit is a (cost, expense). f. The balance sheet of a manufacturer would include an account for (cost of goods sold, work in process inventory). g. The implementation of automatic, robotic factory equipment normally (increases, decreases) the direct labor component of product costs.arrow_forwardAs manager of department B in MarIeys Manufacturing, based on the costs you identified in the previous exercise for further research, how does this impact the financial performance of your department, and what might be some questions you want to ask or solutions you might propose to Marleys management?arrow_forwardWhich of the following statements is false? Multiple Choice Examples of selling costs include shipping, sales commissions, and costs of finished goods warehouses. Discretionary fixed costs may be altered in the short term by current managerial decisions. A particular cost may be direct or indirect depending on the cost object. All sunk costs should be ignored in making a decision. Some of the conversion costs are period costs.arrow_forward

- Consider the business application," filing excess capacity 'below cost'. As noted there, the determination of cost depends on the way in which cost of delivery services are allocated to different customers. Assume that USPS has to customers people who made first class letters and business that ship packages to customers. Management at USPS wants to understand how profitable each customer Group is. how would you recommend the costs of the USPS network (Trucks,buildings,carriers and so on)be allocated to these two customers to answer that question?arrow_forward1. In what way does a typical manufacturing business differ from a merchandising concern? In what ways are they similar? 2. What are the basic elements of production cost? 3. Define the following costs: a. Direct materials b. Indirect materials c. Direct labor d. Indirect labor e. Factory overhead 4. Give examples of variable overhead and fixed overhead costs. 5. Consider education as a product. What are the direct costs and the indirect costs to a university in educating a student?arrow_forwardPlease answer questions 1 and 2.arrow_forward

- 1.Choose all of the following statements that are true. a. Opportunity costs and sunk costs are not reflected on a firm's financial statements. b. Direct costs are manufacturing costs; indirect costs are non-manufacturing costs. c. Variable costs are always relevant to a decision. d. Under absorption costing, when a firm increases production, but has the same amount of sales, cost of goods sold decreases. e. Job order costing systems are used only in service industries; process costing systems are used only in manufacturing industries. 2.Which of the following are true about cost behavior within a particular relevant range? (Choose all that apply.) a. Variable costs per unit increase as a company produces more units of production. b. Total fixed cost is constant over all units of production. c. Fixed costs per unit decreases as a company produces less units of production. d. The slope of total variable costs is positive over increasing levels of production.arrow_forwardThe manager of the manufacturing unit of a company is responsible for the costs of the manufacturing unit. The president is in the process of deciding whether to evaluate the manager of the manufacturing unit by the average cost per unit or the variable cost per unit. Quality and timely delivery would be used in conjunction with the cost measure to reward the manager. Requlred: a. What problems are associated with using the average cost per unit as a performance measure? b. What problems are associated with using the variable cost per unit as a performance measure?arrow_forwardWhat from the upcoming options will be made when using the traditional costing method, relatively to using the ABC costing method? Pick only one answer – Underestimating the products cost with products that have low direct costs, and one-time products that are produced in small series. A tight costing connection between the cost and the factor causing it. All the answers are incorect. A higher cost for implementing and managing the accounts managing system, the general and the costing. Overestimating the products cost with products that have low direct costs, and one-time products that are produced in small series.arrow_forward

- “I’m going to focus on the customers of my business and leave cost-allocation issues to my accountant.” Do you agree with this comment by a division president? Explain.arrow_forwardI need help with this accounting problemarrow_forwardSelect a manufacturing organization for justifying“Companies with labor incentive manufacturing processes are most likely to benefit from sendingmanufacturing operations overseas because the bulk of potential cost savings relate to labor costs”.Q1. Identify relevant and irrelevant costs and benefits in a decision?Q2. Prepare an analysis showing whether a product line or other business segment should be addedor dropped?Q3. Determine the value of obtaining constrained resources?arrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning