Concept explainers

Videos

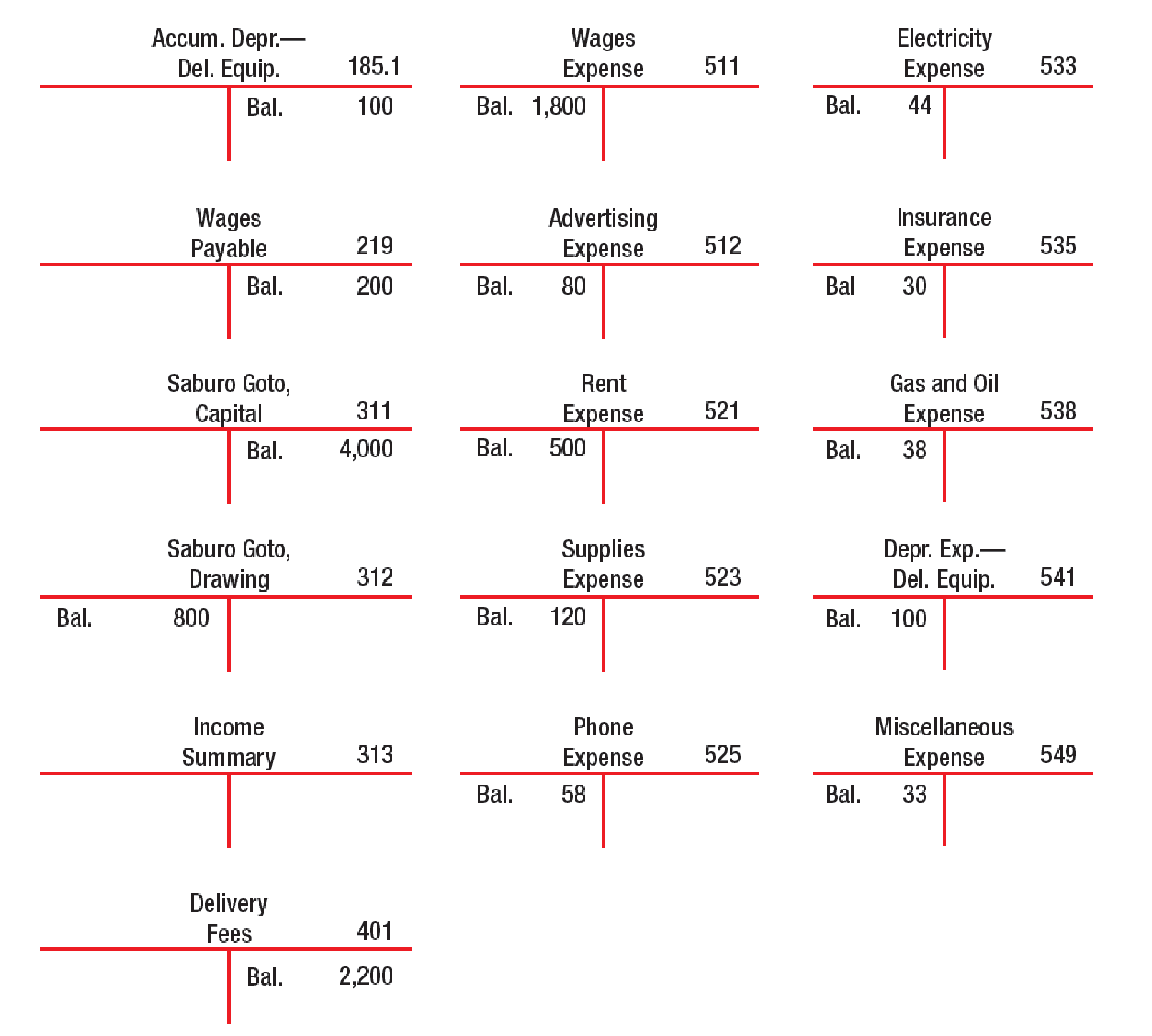

CLOSING ENTRIES (NET LOSS) Using the following partial listing of T accounts, prepare closing entries in general journal form dated January 31, 20--. Then

Prepare closing journal entries in general journal form and post those entries to the T accounts.

Explanation of Solution

Closing entries: The journal entries prepared to close the temporary accounts to permanent account are referred to as closing entries. The revenue, expense, and dividends accounts are referred to as temporary accounts because the information and figures in these accounts is held temporarily and consequently transferred to permanent account at the end of accounting year.

Prepare the closing entries.

| Date | Accounts and Explanation |

Account Number |

Debit ($) | Credit ($) |

| June 30 | Referral fees (SE–) | 401 | 2,813 | |

| Income Summary (SE+) | 313 | 2,813 | ||

| (To close the revenue account.) | ||||

| June 30 | Income summary (SE–) | 313 | 2,987 | |

| Wages expense (SE+) | 511 | 1,080 | ||

| Advertising expense (SE+) | 512 | 34 | ||

| Rent expense (SE+) | 521 | 900 | ||

| Supplies expense (SE+) | 523 | 322 | ||

| Phone expense (SE+) | 525 | 133 | ||

| Utilities expense (SE+) | 533 | 102 | ||

| Insurance expense (SE+) | 535 | 120 | ||

| Gas and oil expense (SE+) | 538 | 88 | ||

| Depreciation expense (SE+) | 541 | 110 | ||

| Miscellaneous expense (SE+) | 549 | 98 | ||

| (To close the expense accounts.) | ||||

| June 30 | RZ, Capital (SE+) | 313 | 174 | |

| Income Summary (SE–) | 313 | 174 | ||

| (To close the income summary accounts) | ||||

| June 30 | RZ, Capital (SE–) | 311 | 2,000 | |

| RZ, Drawings (SE+) | 312 | 2,000 | ||

| (To close withdrawals account.) |

Table (1)

Working Note:

Calculate the amount of RZ capital (transferred).

Revenue account: In this closing entry, the referral fees account is closed by transferring the amount of referral fees account to Income summary account in order to bring the revenue account balance to zero. Hence, debit referral fees account and credit Income summary account.

Expense account: In this closing entry, all expense accounts are closed by transferring the amount of total expense to the Income summary account in order to bring the expense account balance to zero. Hence, debit the Income summary account and credit all expenses account.

Income summary account: Income summary account is a temporary account. This account is debited to close the net income value to RZ capital account.

RZ capital is a component of stockholders’ equity account. The value of RZ capital increased because net income is transferred. Therefore, it is credited.

Withdrawals account: RZ capital is a component of owner’s equity. Thus, owners ‘equity is debited since the capital is decreased on owners’ drawings.

RZ withdrawals are a component of owner’s equity. It is credited because the balance of owners’ withdrawals account is transferred to owners ‘capital account.

T-account: The condensed form of a ledger is referred to as T-account. The left-hand side of this account is known as debit, and the right hand side is known as credit.

Posting the closing entries to the T- account:

| Accumulated Depreciation | Account No – 181.1 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Ending balance | 110 | Beginning balance | 110 | |||

| Beginning balance | 110 | |||||

Table (2)

| Wages Payable | Account No - 219 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Ending balance | 260 | Beginning balance | 260 | |||

| Beginning balance | 260 | |||||

Table (3)

| RZ Capital | Account No – 311 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Income summary | 174 | Beginning balance | 6,000 | |||

| RZ Drawings | 2,000 | |||||

| Ending balance | 3,826 | |||||

| Beginning balance | 3,826 | |||||

Table (4)

| SG Drawings | Account No - 312 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 2,000 | RZ Capital | 2,000 | |||

| Total | 2,000 | Total | 2,000 | |||

Table (5)

| Income Summary | Account No - 313 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Total expense | 2,987 | Referral fees | 2,813 | |||

| RZ Capital | 174 | |||||

| Total | 2,987 | Total | 2,987 | |||

Table (6)

| Referral Fees | Account No - 401 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Income summary | 2,813 | Beginning balance | 2,813 | |||

| Total | 2,813 | Total | 2,813 | |||

Table (7)

| Wages Expense | Account No - 511 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 1,080 | Income summary | 1,080 | |||

| Total | 1,080 | Total | 1,080 | |||

Table (8)

| Advertising Expense | Account No - 512 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 34 | Income summary | 34 | |||

| Total | 34 | Total | 34 | |||

Table (9)

| Rent Expense | Account No - 521 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 900 | Income summary | 900 | |||

| Total | 900 | Total | 900 | |||

Table (10)

| Supplies Expense | Account No - 524 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 322 | Income summary | 322 | |||

| Total | 322 | Total | 322 | |||

Table (11)

| Phone Expense | Account No - 525 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 133 | Income summary | 133 | |||

| Total | 133 | Total | 133 | |||

Table (12)

| Utilities Expense | Account No - 533 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 102 | Income summary | 102 | |||

| Total | 102 | Total | 102 | |||

Table (13)

| Insurance Expense | Account No - 535 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 120 | Income summary | 120 | |||

| Total | 120 | Total | 120 | |||

Table (14)

| Gas and Oil Expense | Account No - 538 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 88 | Income summary | 88 | |||

| Total | 88 | Total | 88 | |||

Table (15)

| Depreciation Expense | Account No - 541 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 110 | Income summary | 110 | |||

| Total | 110 | Total | 110 | |||

Table (16)

| Miscellaneous Expense | Account No - 549 | |||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Beginning balance | 98 | Income summary | 98 | |||

| Total | 98 | Total | 98 | |||

Table (17)

Want to see more full solutions like this?

Chapter 6 Solutions

Bundle: College Accounting, Chapters 1-27, Loose-leaf Version, 22nd + Cengagenowv2™, 2 Terms Printed Access Card For Heintz/parry's College ... Set For College Accounting, 22nd + Cenga

- Reconstruction of Closing Entries The following T accounts summarize entries made to selected general ledger accounts of Cooper $ Company. Certain entries, dated December 31, are closing entries. Prepare the closing entries that were made on December 31.arrow_forwardAfter the adjusting entries are recorded and posted and the financial statements have been prepared, you are ready to record the closing entries. Closing entries zero out the temporary owners equity accounts (revenue(s), expenses(s), and Drawing). This process transfers the net income or net loss and the withdrawals to the Capital account. In addition, the closing process prepares the records for the new fiscal period. Required 1. Journalize the dosing entries in the general journal. (If you are using Working Papers to prepare the closing entries, enter your transactions beginning on page 5.) 2. Post the closing entries to the general ledger accounts. (Skip this step if you are using CLGL.) 3. Prepare a post-dosing trial balance as of October 31, 20--. Check Figures 1. Debit to Income Summary second entry, 12,023.25 2. Post-closing trial balance total, 37,420.00arrow_forwardClosing Entries Lloyd Bookstore shows the following dividends, revenue, and expense account balances before closing: Required: Prepare closing entries.arrow_forward

- answer the followingarrow_forwardIf Income from Services had a 20,400 credit balance before closing entries, which of the following would be the appropriate closing entry to close revenues?arrow_forwardplease provide compulsory explanation , narration , computation clearly for each part and steps answer in text formarrow_forward

- Casilda Company uses the aging approach to estimate bad debt expense. The ending balance of each account receivable is aged on the basis of three time periods as follows: (1) not yet due, $50,100; (2) up to 180 days past due, $15,300; and (3) more than 180 days past due, $4,500. Experience has shown that for each age group, the average loss rate on the amount of the receivables at year-end due to uncollectibility is (1) 4 percent, (2) 12 percent, and (3) 30 percent, respectively. At December 31, the end of the current year, the Allowance for Doubtful Accounts balance is $400 (credit) before the end-of-period adjusting entry is made. Required: 1. Prepare the appropriate bad debt expense adjusting entry for the current year. 2. Show how the various accounts related to accounts receivable should be shown on the December 31, current year, balance sheet Complete this question by entering your answers in the tabs below.arrow_forwardOn January 1, 2021, the general ledger of TNT Fireworks includes the following account balances: Accounts Debit Credit Cash $ 59,000 Accounts Receivable 25,600 Allowance for Uncollectible Accounts $ 2,500 Inventory Notes Receivable (5%, due in 2 years) 36,600 15,600 Land 158,000 Accounts Payable 15,100 Common Stock 223,000 Retained Earnings 54,200 $294,800 Totals $294,800 During January 2021, the following transactions occur: January 1 Purchase equipment for $19,800. The company estimates a residual value of $1,800 and a six-year service life. January 4 Pay cash on accounts payable, $9,800. January 8 Purchase additional inventory on account, $85,900. January 15 Receive cash on accounts receivable, $22,30O. January 19 Pay cash for salaries, $30,100. January 28 Pay cash for January utilities, $16,800. January 30 Sales for January total $223,000. All of these sales are on account. The cost of the units sold is $116,500. Information for adjusting entries: a. Depreciation on the equipment…arrow_forwardClosing entries; net income Based on the data presented in Exercise 5-27, journalize the closing entries.arrow_forward

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage