a.

To identify:

Discount:

Discount refers to a situation where price issued for the bond is below the par value of the bond.

Premium:

Premium refers to a situation where price issued for the bond is above the par value of the bond.

Par value of bonds:

Par value of bond also mentioned as the face value of the bond is the original price printed on the bond certificate. A bond is considered to be issued at par when yield to maturity of a bond is equal to coupon rate of the bond.

a.

Explanation of Solution

Yield to maturity is 9%.

Bond A has 7% annual coupon rate.

Bond B has 9% annual coupon rate.

Bond C has 11% annual coupon rate.

Bond A has an annual coupon rate of 7% which is less than the required return of 9%, it means that the bond is being traded at below the par value or at discount.

Bond B has an annual coupon rate of 9% which is equal to the required return of 9%, it means that the bond is being traded at par value.

Bond C has an annual coupon rate of 11% which is more than the required return of 9%, it means that the bond is being traded at above the par value or at a premium.

b.

To compute: Price of bonds.

Bonds:

Bonds are a financial instrument, generally issued to raise debt generally for activities which require a significant amount of funds, with an undertaking to repay the amount with appropriate interest.

b.

Explanation of Solution

Bond A

Given,

The coupon rate is 7% or 0.07.

Par value is $1,000

Yield to maturity is 9%

Number of periods is 12

PVIF is 0.35553

PVIFA is 7.1607

The formula to compute the price of bonds:

Where,

i is the interest rate

n is number of time period

PVIFA is Present Value Interest Factor of

PVIF is Present Value Interest Factor

Substitute $1,000 for the par value of the bond, 0.35553 for PVIF (i,n), $70 for interest to be paid each year and 7.1607 for PVIFA (i,n)

Bond B

Given,

The coupon rate is 9% or 0.09.

Par value is $1,000

Yield to maturity is 9%

Number of periods is 12

PVIF is 0.35553

PVIFA is 7.1607

Since bond B is issued at par, the price of the bond will be its value $1,000.

Bond C

Given,

The coupon rate is 11% or 0.11.

Par value is $1,000

Yield to maturity is 9%

Number of periods is 12

PVIF is 0.35553

PVIFA is 7.1607

The formula to compute the price of bonds:

Where,

i is the interest rate

n is number of time period

PVIFA is Present Value Interest Factor of Annuity

PVIF is Present Value Interest Factor

Substitute $1,000 for the par value of the bond, 0.35553 for PVIF (i,n), $110 for interest to be paid each year and 7.1607 for PVIFA (i,n)

Working Note:

Bond A

Calculation of interest to be paid each year:

Bond B

Calculation of interest to be paid each year:

Bond C

Calculation of interest to be paid each year:

Hence, the price of the bond A, B and C are computed to be $856.78, $1,000 and $1,143.21.

c.

To compute: Current yield.

Current Yield:

Current yield is the anticipated

The formula for current yield:

c.

Explanation of Solution

Bond A

Given,

Annual coupon payment as computed is $70.

Current price as computed is $856.78.

The formula to calculate the current yield of Bond A:

Substitute $70 for annual coupon payment and $856.78 for the current price,

Bond B

Given,

Annual coupon payment as computed is $90.

Current price as computed is $1,000.

The formula to calculate the current yield of Bond B:

Substitute $90 for annual coupon payment and $1,000 for the current price,

Bond C

Given,

Annual coupon payment as computed is $110.

Current price as computed is $1,143.21.

The formula to calculate the current yield of Bond C:

Substitute $110 for annual coupon payment and $1,143.21 for the current price,

Hence, the current yield of Bond A, B and C are computed to be $8.17%, 9.00%, and 9.62%.

d.

To compute: Price of each bond 1 year from now. Expected

Bonds:

Bonds are a financial instrument, generally issued to raise debt generally for activities which require a significant amount of funds, with an undertaking to repay the amount with appropriate interest.

d.

Explanation of Solution

Price of each bond one year from now:

Bond A

Given,

The coupon rate is 7% or 0.07.

Par value is $1,000

Yield to maturity is 9%

Number of periods is 11

PVIF is 0.3875

PVIFA is 6.8052

The formula to compute the price of bonds:

Where,

i is the interest rate

n is number of time period

PVIFA is Present Value Interest Factor of

PVIF is Present Value Interest Factor

Substitute $1,000 for the par value of the bond, 0.3875 for PVIF (i,n), $70 for interest to be paid each year and 6.8052 for PVIFA (i,n)

Bond B

Given,

The coupon rate is 9% or 0.09.

Par value is $1,000

Yield to maturity is 9%

A number of periods is 11.

PVIF is 0.3875

PVIFA is 6.8052

Since bond B is issued at par, the price of the bond will be its value $1,000.

Bond C

Given,

The coupon rate is 11% or 0.11.

Par value is $1,000

Yield to maturity is 9%

Number of periods is 11.

PVIF is 0.3875

PVIFA is 6.8052

The formula to compute the price of bonds:

Where,

i is the interest rate

n is number of time period

PVIFA is Present Value Interest Factor of Annuity

PVIF is Present Value Interest Factor

Substitute $1,000 for the par value of the bond, 0.3875 for PVIF (i,n), $110 for interest to be paid each year and 6.8052 for PVIFA (i,n)

Expected total return for each bond:

Expected total return for each bond is equal to YTM which is 9%.

Expected capital gains yield for each bond:

Bond A

Given,

Expected total return for bond A, B and C is 9%.

The current yield of bond A as computed is 8.17%.

The formula to calculate capital gain yield for Bond A:

Substitute 9% for total return and 8.17% for current yield,

Bond B

Given,

Expected total return for bond A, B and C is 9%.

The current yield of bond A as computed is 9%.

The formula to calculate capital gain yield for Bond B:

Substitute 9% for total return and 9% for current yield,

Bond C

Given,

Expected total return for bond A, B and C is 9%.

The current yield of bond C as computed is 9.62%.

The formula to calculate capital gain yield for Bond A:

Substitute 9% for total return and 9.62% for current yield,

Working Note:

Bond A

Calculation of interest to be paid each year:

Bond B

Calculation of interest to be paid each year:

Bond C

Calculation of interest to be paid each year:

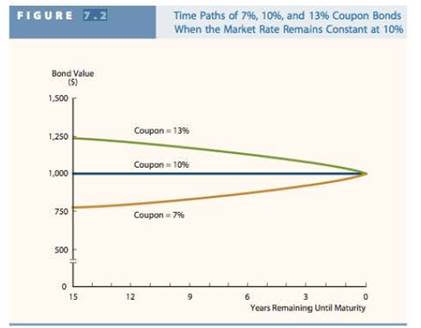

Hence, the price of the bond A, B and C are computed to be $863.86, $1,000 and $1,136.07 respectively. The capital gain yield of Bond A, B and C are computed to be 0.83%, 0% and -0.62% respectively. Expected total return for each bond is computed to be 9%.

e.1.

To compute: Bond’s normal yield to maturity.

e.1.

Explanation of Solution

Bond D

Given,

The semi-annual coupon rate is 8% or 0.08.

Par value is $1,000

Number of periods is 18

Bond price is $1,150.

The formula to compute bond’s nominal yield to maturity:

Where,

C is coupon value

FV is face value

P is the price of the bond

n is number of periods

Substituting $80 for C, $1,000 for FV, $1,150 for P and 18 months for n,

Working note:

Calculation of semiannual rate:

Interest is

Hence, yield to maturity is computed to be 5.88%

2.

To compute: Yield to call

2.

Explanation of Solution

Given,

Semi-annual coupon rate is 8% or 0.08.

Par value is $1,000

Number of periods is 10

The call price is $1,040

The formula to compute bond’s nominal yield to maturity:

Where,

C is coupon value

FV is face value

P is the price of the bond

n is number of periods

Substituting $80 for C, $1,150 for FV, $1,040 for P and 10 months for n,

Hence, yield to maturity is computed to be 5.29.

3.

To identify: Decision to choose between yield to maturity or yield to call.

3.

Answer to Problem 19SP

Mr. C will earn Yield to call in the given case.

Explanation of Solution

Since the bonds are trading at a premium, it indicates that interest rates have fallen.

In case interest rates remain to be constant at present level, Mr. C should anticipate the bond to be called.

As a result, he will earn Yield to call.

Hence, Mr. C will earn Yield to call in the given case.

f.

To identify: Difference between price risk and reinvestment risk. Bonds which have highest reinvestment risk.

f.

Explanation of Solution

Price risk

Price risk is the possibility of the fall in the price of bonds due to rising in the interest rates.

Price risk is higher on bonds having longer maturity period as it gives sufficient time to bondholder to replace the bond.

Reinvestment risk

Reinvestment risk is the possibility of fall in the interest rates which will subsequently result in fall in income from the bond portfolio.

Reinvestment risk is higher on short-term bonds as less high old coupon bonds will be replaced with a new low-coupon bond.

Bonds have been ranked in order from the most interest rate risk to the least interest rate risk:

18 year bond with a 9% annual coupon

A 10-year bond with a zero coupon

A 10-year bond with a 9% annual coupon

A 5-year bond with a zero coupon

A 5-year bond with a 9% annual coupon

Hence, bonds have been ranked above from the most interest rate risk to the least interest rate risk.

g.1.

To compute: Expected interest rate for each bond in each year.

g.1.

Explanation of Solution

Expected interest yield or current yield for each bond in each year:

| N | Bond A | Bond B | Bond C |

| 12 | 8.17% | 9.00% | 9.62% |

| 11 | 8.10% | 9.00% | 9.68% |

| 10 | 8.03% | 9.00% | 9.75% |

| 9 | 7.95% | 9.00% | 9.82% |

| 8 | 7.87% | 9.00% | 9.90% |

| 7 | 7.78% | 9.00% | 9.99% |

| 6 | 7.69% | 9.00% | 10.09% |

| 5 | 7.59% | 9.00% | 10.21% |

| 4 | 7.48% | 9.00% | 10.33% |

| 3 | 7.37% | 9.00% | 10.47% |

| 2 | 7.26% | 9.00% | 10.63% |

| 1 | 7.13% | 9.00% | 10.80% |

Hence, above table shows the expected interest yield or current yield for each bond in each year.

2.

To compute: Expected capital gains yield for each bond in each year.

2.

Explanation of Solution

Expected capital gains yield for each bond in each year:

| N | Bond A | Bond B | Bond C |

| 12 | 0.83% | 0.00% | -0.62% |

| 11 | 0.90% | 0.00% | -0.68% |

| 10 | 0.97% | 0.00% | -0.75% |

| 9 | 1.05% | 0.00% | -0.82% |

| 8 | 1.13% | 0.00% | -0.90% |

| 7 | 1.22% | 0.00% | -0.99% |

| 6 | 1.31% | 0.00% | -1.09% |

| 5 | 1.41% | 0.00% | -1.21% |

| 4 | 1.52% | 0.00% | -1.33% |

| 3 | 1.63% | 0.00% | -1.47% |

| 2 | 1.74% | 0.00% | -1.63% |

| 1 | 1.87% | 0.00% | -1.80% |

Hence, above table shows the expected capital gains yield for each bond in each year.

3.

To compute: Total return for each bond in each year.

3.

Explanation of Solution

Given,

Expected total return for bond A, B and C is 9%.

Total return for each bond in each year:

| N | Bond A | Bond B | Bond C |

| 12 | 9.00% | 9.00% | 9.00% |

| 11 | 9.00% | 9.00% | 9.00% |

| 10 | 9.00% | 9.00% | 9.00% |

| 9 | 9.00% | 9.00% | 9.00% |

| 8 | 9.00% | 9.00% | 9.00% |

| 7 | 9.00% | 9.00% | 9.00% |

| 6 | 9.00% | 9.00% | 9.00% |

| 5 | 9.00% | 9.00% | 9.00% |

| 4 | 9.00% | 9.00% | 9.00% |

| 3 | 9.00% | 9.00% | 9.00% |

| 2 | 9.00% | 9.00% | 9.00% |

| 1 | 9.00% | 9.00% | 9.00% |

Hence, above table shows the total return for each bond in each year.

Want to see more full solutions like this?

Chapter 7 Solutions

Bundle: Fundamentals Of Financial Management, Concise Edition + Mindtap, 1 Term Printed Access Card

- Yield to Maturity and Yield to Call Arnot International’s bonds have a current market price of $1,200. The bonds have an 11% annual coupon payment, a $1,000 face value, and 10 years left until maturity. The bonds may be called in 5 years at 109% of face value (call price = $1,090). What is the yield to maturity? What is the yield to call if they are called in 5 years? Which yield might investors expect to earn on these bonds, and why? The bond’s indenture indicates that the call provision gives the firm the right to call them at the end of each year beginning in Year 5. In Year 5, they may be called at 109% of face value, but in each of the next 4 years the call percentage will decline by 1 percentage point. Thus, in Year 6 they may be called at 108% of face value, in Year 7 they may be called at 107% of face value, and so on. If the yield curve is horizontal and interest rates remain at their current level, when is the latest that investors might expect the firm to call the bonds?arrow_forwardBond Valuation and Changes in Maturity and Required Returns Suppose Hillard Manufacturing sold an issue of bonds with a 10-year maturity, a 1,000 par value, a 10% coupon rate, and semiannual interest payments. a. Two years after the bonds were issued, the going rate of interest on bonds such as these fell to 6%. At what price would the bonds sell? b. Suppose that 2 years after the initial offering, the going interest rate had risen to 12%. At what price would the bonds sell? c. Suppose that 2 years after the issue date (as in Part a) interest rates fell to 6%. Suppose further that the interest rate remained at 6% for the next 8 years. What would happen to the price of the bonds over time?arrow_forwardBond Value as Maturity Approaches An investor has two bonds in his portfolio. Each bond matures in 4 years, has a face value of 1,000, and has a yield to maturity equal to 9.6%. One bond, Bond C, pays an annual coupon of 10%; the other bond, Bond Z, is a zero coupon bond. Assuming that the yield to maturity of each bond remains at 9.6% over the next 4 years, what will be the price of each of the bonds at the following time periods? Fill in the following table:arrow_forward

- Bond Valuation with Semiannual Payments Renfro Rentals has issued bonds that have a 10% coupon rate, payable semiannually. The bonds mature in 8 years, have a face value of $1,000, and a yield to maturity of 8.5%. What is the price of the bonds?arrow_forwardHello! Im stuck at this homework. Clifford Clark is a recent retiree who is interested in investing some ofhis savings in corporate bonds. His financial planner has suggested the following bonds:● Bond A has a 6% annual coupon, matures in 15years, and has a $1,000 face value.● Bond B has a 8% annual coupon, matures in 15years, and has a $1,000 face value.● Bond C has an 10% annual coupon, matures in 15years, and has a $1,000 face value.Each bond has a yield to maturity of 8%.d. If the yield to maturity for each bond remains at 8%, what will be the price of each bond 1 year from now? e. Mr. Clark is considering another bond, Bond D. It has an 7% semiannual coupon and a $1,000 face value. Interest is paid at the enf of each 6months. Bond is schedule to mature in 9 years and has a price of $1,200. It is also callable in 5 years at a call price of $1,050.1. What is the bond’s nominal yield to maturity?2. What is the bond’s nominal yield to call?3. If Mr. Clark were to purchase this bond,…arrow_forwardHello! Im stuck at this homework. Clifford Clark is a recent retiree who is interested in investing some ofhis savings in corporate bonds. His financial planner has suggested the following bonds:● Bond A has a 6% annual coupon, matures in 15years, and has a $1,000 face value.● Bond B has a 8% annual coupon, matures in 15years, and has a $1,000 face value.● Bond C has an 10% annual coupon, matures in 15years, and has a $1,000 face value.Each bond has a yield to maturity of 8%.d. If the yield to maturity for each bond remains at 8%, what will be the price of each bond 1 year from now? e. Mr. Clark is considering another bond, Bond D. It has an 7% semiannual coupon anda $1,000 face value. Interest is paid at the enf of each 6months. Bond is schedule tomature in 9 years and has a price of $1,200. It is also callable in 5 years at a call priceof $1,050.1. What is the bond’s nominal yield to maturity?2. What is the bond’s nominal yield to call?3. If Mr. Clark were to purchase this bond,…arrow_forward

- Bond Valuation. Thatcher Corporation’s bonds will mature in 20 years. The bonds have a face value of $1,000 and an 8 percent coupon rate, paid semiannually. The bonds have a yield to maturity of 10 percent. The bonds are callable in 12 years at a 9 percent call premium. What is the current bond price? What is the investor’s yield to call? Show your workarrow_forwardEconomics Corus Berhad is interested to invest in bonds. Currently, the financial manager is evaluating both Bond A and Bond B. Bond A pays 8 percent coupon semi-annually and matures in 12 years. Bond B pays 7 percent coupon annually having a maturity period of 13 years. Determine the value of each bond if the current market yield for both bonds is 8 percent.arrow_forward(Bond valuation) At the beginning of the year, you bought a $1,000 par value corporate bond with an annual coupon rate of 16 percent and a maturity date of 14 years. When you bought the bond, it had an expected yield to maturity of 15 percent. Today the bond sells for $1,190. a. What did you pay for the bond? b. If you sold the bond at the end of the year, what would be your one-period return on the investment? Assume that you did not receive any interest payment during the holding period.arrow_forward

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT