Concept explainers

Videos

Analyzing and Interpreting the Effects of the LIFO/FIFO Choice on Inventory Turnover Ratio

Simple Plan Enterprises uses a periodic inventory system. Its records showed the following:

Inventory, December 31, using FIFO → 38 Units @$14 = $532

Inventory, December 31, using UFO → 38 Units @ $10 = $380

Required:

- 1. Compute the number and cost of goods available for sale, the cost of ending inventory, and the cost of goods sold under FIFO and LIFO.

- 2. Compute the inventory turnover ratio under the FIFO and LIFO inventory costing methods (show computations).

- 3. Based on your answer to requirement 2, explain whether analysts should consider the inventory costing method when comparing companies’ inventory turnover ratios.

Requirement 1:

To Compute: The number of units and cost of goods available for sale and cost of ending inventory and the cost of goods sold under FIFO and LIFO.

Explanation of Solution

Determine cost of goods available for sale _FIFO.

| Date | Particulars | Units ($) | Unit cost ($) | Total cost ($) |

| (a) | (b) | (c = a × b) | ||

| December 31 | Beginning inventory | 38 | 14 | 532 |

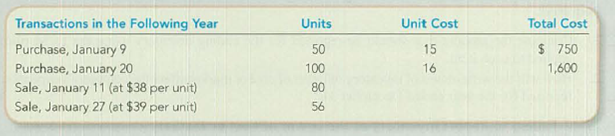

| January 9 | Purchased | 50 | 15 | 750 |

| January 20 | Purchased | 100 | 16 | 1,600 |

| Total | 188 | $2,882 |

Table (1)

Therefore, the cost of goods sold available for sale under FIFO for 188 units of inventory is $2,882.

Determine cost of goods available for sale _LIFO.

| Date | Particulars | Units ($) | Unit cost ($) | Total cost ($) |

| (a) | (b) | (c = a × b) | ||

| December 31 | Beginning inventory | 38 | 10 | 380 |

| January 9 | Purchased | 50 | 15 | 750 |

| January 20 | Purchased | 100 | 16 | 1,600 |

| Total | 188 | $2,730 |

Table (2)

Therefore, the cost of goods sold available for sale under LIFO for 188 units of inventory is $2,882.

Calculate the number of units in ending inventory:

Therefore, the number of units in ending inventory is 52 units.

In First-in-First-Out method, the cost of initial purchased items is sold first. The value of the ending inventory consists the recent purchased items.

Determine the amount of cost of goods sold.

| Date | Particulars | Units | Unit cost ($) | Total cost ($) |

| (a) | (b) | (c = a × b) | ||

| December 31 | Beginning inventory | 38 | 14 | 532 |

| January 9 | Purchased | 50 | 15 | 750 |

| January 20 | Purchased | 48 | 16 | 768 |

| Cost of goods sold | 136 | $2,050 |

Table (3)

Determine ending inventory under FIFO method.

| Date | Particulars | Units | Unit cost ($) | Total cost ($) |

| (a) | (b) | (c = a × b) | ||

| Ending inventory | 52 | 16 | 832 | |

| Ending inventory | $832 |

Table (4)

Hence, the cost of goods sold under FIFO is $2,050 and the value of ending inventory is $832.

In Last-in-First-Out method, the cost of last purchased items is sold first. The value of the closing stock consists the initial purchased items.

Determine the amount of cost of goods sold.

| Date | Particulars | Units | Unit cost ($) | Total cost ($) |

| (a) | (b) | (c = a × b) | ||

| January 20 | Purchased | 100 | 16 | 1,600 |

| January 9 | Purchased | 36 | 15 | 540 |

| Cost of goods sold | 136 | $2,140 |

Table (5)

Determine ending inventory under LIFO method.

| Date | Particulars | Units | Unit cost ($) | Total cost ($) |

| (a) | (b) | (c = a × b) | ||

| December 31 | Beginning inventory | 38 | 10 | 380 |

| January 9 | Purchased | 14 | 15 | 210 |

| Ending inventory | $590 |

Table (6)

Hence, the cost of goods sold under LIFO is $2,140 and the value of ending inventory is $590.

Requirement 2:

To Compute: The inventory turnover ratio under FIFO and LIFO inventory costing method.

Answer to Problem 7.14E

| Inventory Costing Method | Inventory Turnover Ratio |

| FIFO | 3.01 |

| LIFO | 4.41 |

Explanation of Solution

Inventory Turnover: The comparison between the average number of time of sales and the average level of inventory during a period is called as Inventory Turnover. In other words, it is the ratio between the Cost of Goods Sold and Average Inventory.

Calculate the inventory turnover ratio under FIFO:

Step 1: Calculate the average inventory.

Step 2: Calculate the inventory turnover ratio.

Calculate the inventory turnover ratio under LIFO:

Step 1: Calculate the average inventory.

Step 2: Calculate the inventory turnover ratio.

Requirement 3:

To Explain: Whether analysts consider the inventory costing method when comparing companies inventory turnover ratios.

Explanation of Solution

- The inventory costing method present a major difference in the inventory turnover ratio.

- If analysts compare the inventory turnover ratio across companies, they must take this into account before deciding whether one company has better inventory management than another.

- If they are comparing the same company over time, it is not as important provided the company is consistent in the method it uses.

Want to see more full solutions like this?

Chapter 7 Solutions

FUND.OF.FIN.ACCT.-CONNECT >CUSTOM<

- Calculate the cost of goods sold dollar value for B74 Company for the sale on November 20, considering the following transactions under three different cost allocation methods and using perpetual inventory updating. Provide calculations for (a) first-in, first-out (FIFO); (b) last-in, first-out (LIFO); and (c) weighted average (AVG).arrow_forwardCalculate the cost of goods sold dollar value for A74 Company for the sale on March 11, considering the following transactions under three different cost allocation methods and using perpetual inventory updating. Provide calculations for (a) first-in, first-out (FIFO); (b) last-in, first-out (LIFO); and (c) weighted average (AVG).arrow_forwardCalculate the cost of goods sold dollar value for A66 Company for the month, considering the following transactions under three different cost allocation methods and using perpetual inventory updating. Provide calculations for last-in, first-out (LIFO).arrow_forward

- Inventory Costing Methods Andersons Department Store has the following data for inventory, purchases, and sales of merchandise for December. Andersons uses a perpetual inventory system. All purchases and sales were for cash. Required: 1. Compute cost of goods sold and the cost of ending inventory using FIFO. 2. Compute cost of goods sold and the cost of ending inventory using LIFO. 3. Compute cost of goods sold and the cost of ending inventory using the average cost method. ( Note: Use four decimal places for per-unit calculations.) 4. Prepare the journal entries to record these transactions assuming Anderson chooses to use the FIFO method. 5. CONCEPTUAL CONNECTION Which method would result in the lowest amount paid for taxes?arrow_forwardAlternative Inventory Methods Park Companys perpetual inventory records indicate the following transactions in the month of June: Required: 1. Compute the cost of goods sold for June and the inventory at the end of June using each of the following cost flow assumptions: a. FIFO b. LIFO c. Average cost (Round unit costs to 3 decimal places and other amounts to the nearest dollar.) 2. Next Level Why are the cost of goods sold and ending inventory amounts different for each of the three methods? What do these amounts tell us about the purchase price of inventory during the year? 3. Next Level Which method produces the most realistic amount for net income? For inventory? Explain your answer. 4. Next Level If Park uses IFRS, which of the previous alternatives would be acceptable and why?arrow_forwardCalculate the cost of goods sold dollar value for B67 Company for the month, considering the following transactions under three different cost allocation methods and using perpetual inventory updating. Provide calculations for weighted average (AVG).arrow_forward

- Data on the physical inventory of Katus Products Co. as of December 31 follow: Quantity and cost data from the last purchases invoice of the year and the next-to-the-last purchases invoice are summarized as follows: Instructions Determine the inventory at cost as well as at the lower of cost or market, using the first-in, first-out method. Record the appropriate unit costs on the inventory sheet and complete the pricing of the inventory. When there are two different unit costs applicable to an item: 1. Draw a line through the quantity and insert the quantity and unit cost of the last purchase. 2. On the following line, insert the quantity and unit cost of the next-to-the-last purchase. 3. Total the cost and market columns and insert the lower of the two totals in the LCM column. The first item on the inventory sheet has been completed as an example.arrow_forwardInventory Write-Down Stiles Corporation uses the FIFO cost flow assumption and is in the process of applying the LCNRV rule for each of two products in its ending inventory. A profit margin of 30% on the selling price is considered normal for each product. Specific data for each product are as follows: Inventory Write-Down Use the information in E8-1. Assume that Stiles uses the LIFO cost flow assumption and is applying the LCM rule. Required: 1. What is the correct inventory value for each product? 2. Next Level With regard to requirement 1, what effect does the imposition of the constraints on market value have on the inventory valuations?arrow_forwardInventory Write-Down Stiles Corporation uses the FIFO cost flow assumption and is in the process of applying the LCNRV rule for each of two products in its ending inventory. A profit margin of 30% on the selling price is considered normal for each product. Specific data for each product are as follows:arrow_forward

- Alternative Inventory Methods Nevens Company uses a periodic inventory system. During November, the following transactions occurred: Required: 1. Compute the cost of goods sold for November and the inventory at the end of November for each of the following cost flow assumptions: a. FIFO b. LIFO c. Average cost 2. Next Level What can you conclude about the effects of the inventory cost flow assumptions on the financial statements?arrow_forwardLower-of-cost-or-market inventory Data on the physical inventory of Katus Products Co. as of December 31 follows: Quantity and cost data from the last purchases invoice of the year and the next-to-the-last purchases invoice are summarized as follows: Instructions Determine the inventory at cost and also at the lower of cost or market applied on an item-by-item basis, using the first-in, first-out method. Record the appropriate unit costs on the inventory sheet, and complete the pricing of the inventory. When there are two different unit costs applicable to an item, proceed as follows: 1. Draw a line through the quantity, and insert the quantity and unit cost of the last purchase. 2. On the following line, insert the quantity and unit cost of the next-to-the-last purchase. 3. Total the cost and market columns and insert the lower of the two totals in the LCM column. The first item on the inventory sheet has been completed as an example.arrow_forwardData on the physical inventory of Ashwood Products Company as of December 31 follow: Quantity and cost data from the last purchases invoice of the year and the next-to-the-last purchases invoice are summarized as follows: Instructions Determine the inventory at cost as well as at the lower of cost or market, using the first-in, first-out method. Record the appropriate unit costs on the inventory sheet and complete the pricing of the inventory. When there are two different unit costs applicable to an item, proceed as follows: 1. Draw a line through the quantity and insert the quantity and unit cost of the last purchase. 2. On the following line, insert the quantity and unit cost of the next-to-the-last purchase. 3. Total the cost and market columns and insert the lower of the two totals in the Lower of C or M column. The first item on the inventory sheet has been completed as an example.arrow_forward

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning