Videos

Evaluating the Income Statement and Income Tax Effects of Lower of Cost or Market

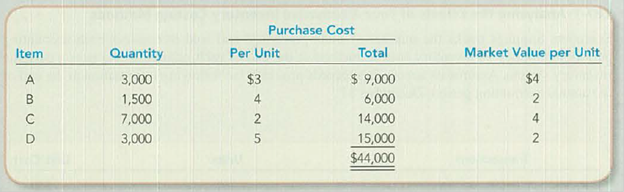

Smart Company prepared its annual financial statements dated December 31. The company used the FIFO inventory costing method, but it failed to apply LCM to the ending inventory. The preliminary income statement follows:

| Sales Revenue | $280,000 | |

| Cost of Goods Sold | ||

| Beginning Inventory | $30,000 | |

| Purchases | 182,000 | |

| Goods Available for Sale | 212,000 | |

| Ending Inventory (FIFO cost) | 44,000 | |

| Cost of Goods Sold | 168,000 | |

| Gross Profit | 112,000 | |

| Operating Expenses | 61,000 | |

| Income from Operations | 51,000 | |

| Income Tax Expense (30%) | 15,300 | |

| Net Income | $35,700 |

Assume that you have been asked to restate the financial statements to incorporate LCM. You have developed the following data relating to the ending inventory:

TIP: Inventory write-downs do not affect the cost of goods available for sale. Instead, the effect of the write-down is to reduce ending inventory, which increases Cost of Goods Sold and then affects other amounts reported lower in the income statement.

Required:

- 1. Restate the income statement to reflect LCM valuation of the ending inventory. Apply LCM on an item-by-item basis and show computations.

- 2. Compare and explain the LCM effect on each amount that was changed in requirement 1.

Want to see the full answer?

Check out a sample textbook solution

Chapter 7 Solutions

FUND OF FIN ACCT W/CONNECT (LL)>CUSTOM

- Lower of Cost or Market Garcia Company uses FIFO, and its inventory at the end of the year was recorded in the accounting records at $17,800. Due to technological changes in the market, Garcia would be able to replace its inventory for $16,500. Required: 1. Using the lower of cost or market method, what amount should Garcia report for inventory on its balance sheet at the end of the year? 2. Prepare the journal entry required to value the inventory at the lower of cost or market.arrow_forwardLower-of-cost-or-market inventory Data on the physical inventory of Ashwood Products Company as of December 31 follow: Quantity and cost data from the last purchases invoice of the year and the next-to-the-last purchases invoice are summarized as follows: Instructions Determine the inventory at cost and also at the lower of cost or market applied on an item-by-item basis, using the first-in, first-out method. Record the appropriate unit costs on the inventory sheet, and complete the pricing of the inventory. When there are two different unit costs applicable to an item, proceed as follows: 1. Draw a line through the quantity, and insert the quantity and unit cost of the last purchase. 2. On the following line, insert the quantity and unit cost of the next-to-the-last purchase. 3. Total the cost and market columns and insert the lower of the two totals in the LCM column. The first item on the inventory sheet has been completed as an example.arrow_forwardLower-of-cost-or-market inventory Data on the physical inventory of Katus Products Co. as of December 31 follows: Quantity and cost data from the last purchases invoice of the year and the next-to-the-last purchases invoice are summarized as follows: Instructions Determine the inventory at cost and also at the lower of cost or market applied on an item-by-item basis, using the first-in, first-out method. Record the appropriate unit costs on the inventory sheet, and complete the pricing of the inventory. When there are two different unit costs applicable to an item, proceed as follows: 1. Draw a line through the quantity, and insert the quantity and unit cost of the last purchase. 2. On the following line, insert the quantity and unit cost of the next-to-the-last purchase. 3. Total the cost and market columns and insert the lower of the two totals in the LCM column. The first item on the inventory sheet has been completed as an example.arrow_forward

- COST ALLOCATION AND LOWER-OF-COST-OR-MARKET Hall Companys beginning inventory and purchases during the fiscal year ended December 31, 20--, were as follows: There are 1,100 units of inventory on hand on December 31. REQUIRED 1. Calculate the total amount to be assigned to the ending inventory and cost of goods sold on December 31 under each of the following methods: (a) FIFO (b) LIFO (c) Weighted-average (round calculations to two decimal places) 2. Assume that the market price per unit (cost to replace) of Halls inventory on December 31 was 16. Calculate the total amount to be assigned to the ending inventory on December 31 under each of the following methods: (a) FIFO lower-of-cost-or-market (b) Weighted-average lower-of-cost-or-market 3. Prepare required entries to apply: (a) FIFO lower-of-cost-or-market (b) Weighted-average lower-of-cost-or-marketarrow_forwardLower-of-cost-or market inventory Data on the physical inventory of Moyer Company as of December 31, 20Y9, are presented below. Quantity and cost data from the last purchases invoice of the year and the next-to-the-last purchases invoice are summarized as follows: Instructions Determine the inventory at cost and at the lower of cost or market, using the first-in, first-out method. Record the appropriate unit costs on an inventory sheet and complete the pricing of the inventory. When there are two different unit costs applicable to an item, proceed as follows: 1. Draw a line through the quantity, and insert the quantity and unit cost of the last purchase. 2. On the following line, insert the quantity and unit cost of the next-to-the-last purchase. 3. Total the cost and market columns and insert the lower of the two totals in the LCM column. The first item on the inventory sheet has been completed below as an example.arrow_forwardSelected data on merchandise inventory, purchases, and sales for Jaffe Co. and Coronado Co. are as follows: Instructions 1. Determine the estimated cost of the merchandise inventory of Jaffe Co. on February 28 by the retail method, presenting details of the computations. 2. a. Estimate the cost of the merchandise inventory of Coronado Co. on October 31 by the gross profit method, presenting details of the computations. b. Assume that Coronado Co. took a physical inventory on October 31 and discovered that 366,500 of merchandise was on hand. What was the estimated loss of inventory due to theft or damage during May through October?arrow_forward

- Calculate the cost of goods sold dollar value for A66 Company for the month, considering the following transactions under three different cost allocation methods and using perpetual inventory updating. Provide calculations for last-in, first-out (LIFO).arrow_forwardSelected data on merchandise inventory, purchases, and sales for Celebrity Tan Co. and Ranchworks Co. are as follows: Instructions 1. Determine the estimated cost of the merchandise inventory of Celebrity Tan Co. on August 31 by the retail method, presenting details of the computations. 2. a. Estimate the cost of the merchandise inventory of Ranchworks Co. on November 30 by the gross profit method, presenting details of the computations. b. Assume that Ranchworks Co. took a physical inventory on November 30 and discovered that 369,750 of merchandise was on hand. What was the estimated loss of inventory due to theft or damage during March through November?arrow_forwardData on the physical inventory of Katus Products Co. as of December 31 follow: Quantity and cost data from the last purchases invoice of the year and the next-to-the-last purchases invoice are summarized as follows: Instructions Determine the inventory at cost as well as at the lower of cost or market, using the first-in, first-out method. Record the appropriate unit costs on the inventory sheet and complete the pricing of the inventory. When there are two different unit costs applicable to an item: 1. Draw a line through the quantity and insert the quantity and unit cost of the last purchase. 2. On the following line, insert the quantity and unit cost of the next-to-the-last purchase. 3. Total the cost and market columns and insert the lower of the two totals in the LCM column. The first item on the inventory sheet has been completed as an example.arrow_forward

- Data on the physical inventory of Ashwood Products Company as of December 31 follow: Quantity and cost data from the last purchases invoice of the year and the next-to-the-last purchases invoice are summarized as follows: Instructions Determine the inventory at cost as well as at the lower of cost or market, using the first-in, first-out method. Record the appropriate unit costs on the inventory sheet and complete the pricing of the inventory. When there are two different unit costs applicable to an item, proceed as follows: 1. Draw a line through the quantity and insert the quantity and unit cost of the last purchase. 2. On the following line, insert the quantity and unit cost of the next-to-the-last purchase. 3. Total the cost and market columns and insert the lower of the two totals in the Lower of C or M column. The first item on the inventory sheet has been completed as an example.arrow_forwardComparison of Inventory Costing Methods—Periodic System Bitten Companys inventory records show 600 units on hand on October 1 with a unit cost of $5 each. The following transactions occurred during the month of October: All expenses other than cost of goods sold amount to $3,000 for the month. The company uses an estimated tax rate of 30% to accrue monthly income taxes. Required Prepare a chart comparing cost of goods sold and ending inventory using the periodic system and the following costing methods: What does the Total column represent? Prepare income statements for each of the three methods. Will the company pay more or less tax if it uses FIFO rather than LIFO? How much more or less?arrow_forwardInventory Costing Methods VanderMeer Inc. reported the following information for the month of February: During February, VanderMeer sold 140 units. The company uses a periodic inventory system. Required What is the value of ending inventory and cost of goods sold for February under the following assumptions: Of the 140 units sold, 55 cost $20, 35 cost $22, 45 cost $23, and 5 cost $24. FIFO LIFO Weighted averagearrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT