Concept explainers

Videos

CASE 8-33

You have just been hired as a new management trainee by Earrings Unlimited, a distributor of earrings to various retail outlets located in shopping malls across the country. In the past, the company has done very little in the way of budgeting and at certain times of the year has experienced a shortage of cash. Since you are well trained in budgeting, you have decided to prepare a master budget for the upcoming second quarter. To this end, you have worked with accounting and other areas to gather the information assembled below.

The company sells many styles of earrings, but all are sold for the same price—$10 per pair. Actual sales of earrings for the last three months and budgeted sales for the next six months follow (in pairs of earrings):

The concentration of sales before and during May is due to Mother's Day. Sufficient inventory should be on hand at the end of each month to supply 40% of the earrings sold in the following month. Suppliers are paid $4 for a pair of earrings. One-half of a month's purchases ispaid for in the month of purchase: the other half is paid for in the following month. .All sales are on credit. Only 20% of a month's sales are collected in the month of sale. .An additional 70% is collected in the following month, and the remaining 10% is collected in the second month following sale.

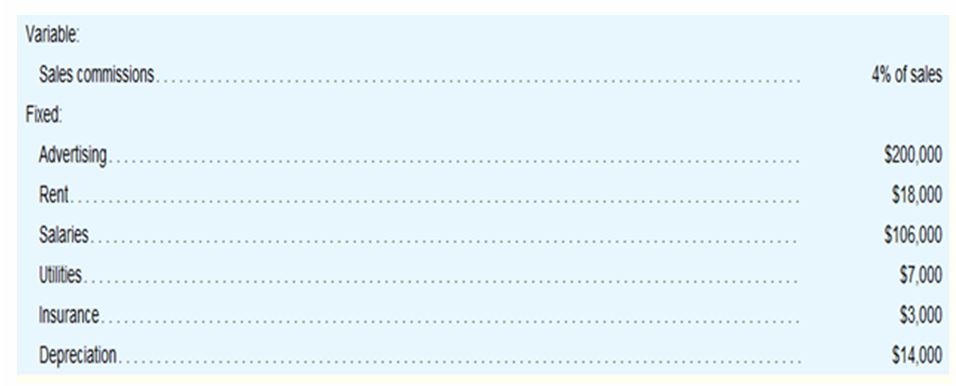

Monthly7operating expenses for the company are given below:

Insurance is paid on an annual basis, in November of each year.

The company plans to purchase $16,000 in new equipment during May and $40,000 in new equipment during June: both purchases will be for cash. The company declares dividends of $ 15,000 each quarter, payable in the first month of the following quarter.

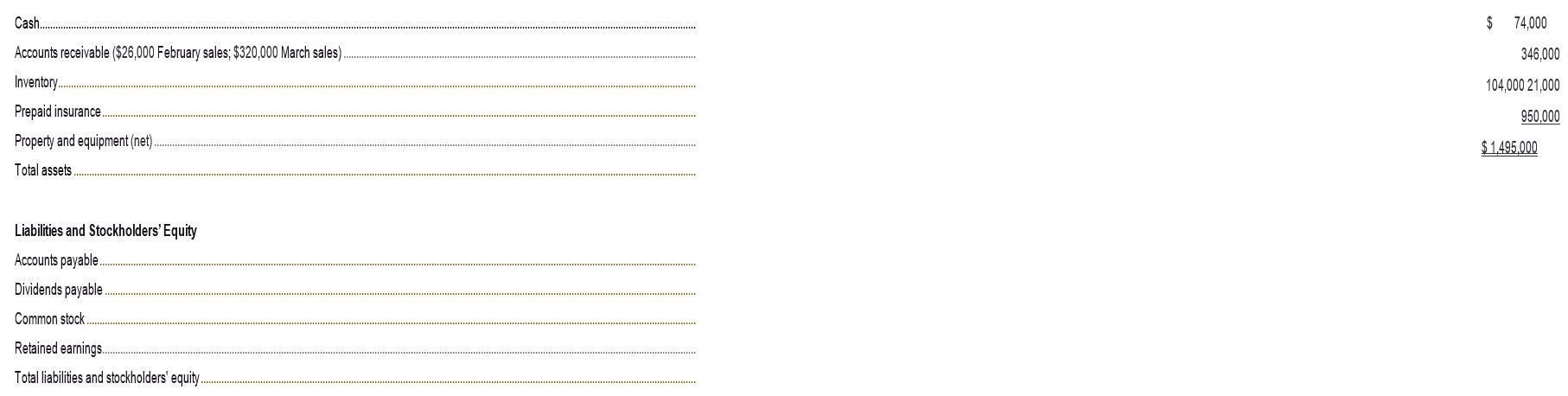

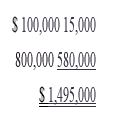

The company's balance sheet as of March 31 is given below:

Assets

The company has an agreement with a bank that allows the company to borrow in increments of $1,000 at the beginning of each month. The interest rate on these loans

is1% per month and for simplicity we will assume that interest is not compounded. At the end of the quarter, the company would pay the bank all of the accumulated interest on the loan and as much of the loan as possible (in increments of $1,000), while still retaining at least $50,000 in cash.

Required:

Prepare a master budget for the three-month period ending June 30. Include the following detailed schedules:

- A sales budget, by month and in total.

- A schedule of expected cash collections, by month and in total.

- A merchandise purchases budget in units and in dollars. Show' the budget by month and in total.

- A schedule of expected cash disbursements for merchandise purchases, by month and in total.

- A

cash budget . Show the budget by month and in total. Determine any borrowing that would be needed to maintain the minimum cash balance of $50,000. - A

budgeted income statement for the three-month period ending June 30. Use the contribution approach.

- A budgeted balance sheet as of June 30. 1.While popsicle manufacturing is likely to involve other raw materials, such as popsicle sticks and packaging materials, for simplicitv, we have limited our scope to high fructose sugar.

- For simplicity, we assume that

depreciation on these newly acquired assets is included in the quarterly depreciation estimates included in the Budgeting Assumptions tab.

3.For simplicity, the beginning balance sheet and the ending finished goods inventory budget both report a unit product cost of $13. For purposes of answering “what-if’ questions, this schedule would assume a FIFO inventory7 flow. In other words, the ending inventory would consist solely of units that are produced during the budget year.

4.Other adjustments might need to be made for differences between

6.The format for the statement of cash flows, which is discussed in a later chapter, may also be used for the cash budget.

7. Cost of goods sold can also be computed using equations introduced in earlier chapters. Manufacturing companies can use the equation: Cost of goods sold = Beginning finished goods inventory + Cost of goods manufactured - Ending finished goods inventory. Merchandising companies can use the equation: Cost of goods sold = Beginning merchandise inventory - Purchases - Ending merchandise inventory.

Want to see the full answer?

Check out a sample textbook solution

Chapter 8 Solutions

MANAGERIAL ACCOUNTING

- 8) Problem 8-31 (Algo) Completing a Master Budget [LO8-2, LO8-4, LO8-7, LO8-8, LO8-9, LO8-10] Hillyard Company, an office supplies specialty store, prepares its master budget on a quarterly basis. The following data have been assembled to assist in preparing the master budget for the first quarter: As of December 31 (the end of the prior quarter), the company’s general ledger showed the following account balances: Cash $ 41,000 Accounts receivable 200,800 Inventory 57,900 Buildings and equipment (net) 351,000 Accounts payable $ 85,425 Common stock 500,000 Retained earnings 65,275 $ 650,700 $ 650,700 Actual sales for December and budgeted sales for the next four months are as follows: December(actual) $ 251,000 January $ 386,000 February $ 583,000 March $ 297,000 April $ 194,000 Sales are 20% for cash and 80% on credit. All payments on…arrow_forward8 Problem 8-31 (Algo) Completing a Master Budget [LO8-2, LO8-4, LO8-7, LO8-8, LO8-9, LO8-10] Hillyard Company, an office supplies specialty store, prepares its master budget on a quarterly basis. The following data have been assembled to assist in preparing the master budget for the first quarter: As of December 31 (the end of the prior quarter), the company’s general ledger showed the following account balances: Cash $ 41,000 Accounts receivable 200,800 Inventory 57,900 Buildings and equipment (net) 351,000 Accounts payable $ 85,425 Common stock 500,000 Retained earnings 65,275 $ 650,700 $ 650,700 Actual sales for December and budgeted sales for the next four months are as follows: December(actual) $ 251,000 January $ 386,000 February $ 583,000 March $ 297,000 April $ 194,000 Sales are 20% for cash and 80% on credit. All payments on…arrow_forward8 Problem 8-31 (Algo) Completing a Master Budget [LO8-2, LO8-4, LO8-7, LO8-8, LO8-9, LO8-10] Hillyard Company, an office supplies specialty store, prepares its master budget on a quarterly basis. The following data have been assembled to assist in preparing the master budget for the first quarter: As of December 31 (the end of the prior quarter), the company’s general ledger showed the following account balances: Cash $ 41,000 Accounts receivable 200,800 Inventory 57,900 Buildings and equipment (net) 351,000 Accounts payable $ 85,425 Common stock 500,000 Retained earnings 65,275 $ 650,700 $ 650,700 Actual sales for December and budgeted sales for the next four months are as follows: December(actual) $ 251,000 January $ 386,000 February $ 583,000 March $ 297,000 April $ 194,000 Sales are 20% for cash and 80% on credit. All payments on…arrow_forward

- 9 Problem 8-29 (Algo) Completing a Master Budget [LO8-2, LO8-4, LO8-7, LO8-8, LO8-9, LO8-10] The following data relate to the operations of Shilow Company, a wholesale distributor of consumer goods: Current assets as of March 31: Cash $ 7,600 Accounts receivable $ 20,400 Inventory $ 40,200 Building and equipment, net $ 128,400 Accounts payable $ 23,925 Common stock $ 150,000 Retained earnings $ 22,675 The gross margin is 25% of sales. Actual and budgeted sales data: March (actual) $ 51,000 April $ 67,000 May $ 72,000 June $ 97,000 July $ 48,000 Sales are 60% for cash and 40% on credit. Credit sales are collected in the month following sale. The accounts receivable at March 31 are a result of March credit sales. Each month’s ending inventory should equal 80% of the following month’s budgeted cost of goods sold. One-half of a month’s inventory purchases is paid for in the month of purchase; the…arrow_forwardProblem 8-23 Schedule of Expected Cash Collections; Cash Budget [LO8-2, LO8-8] The president of the retailer Prime Products has just approached the company’s bank with a request for a $51,000, 90-day loan. The purpose of the loan is to assist the company in acquiring inventories. Because the company has had some difficulty in paying off its loans in the past, the loan officer has asked for a cash budget to help determine whether the loan should be made. The following data are available for the months April through June, during which the loan will be used: On April 1, the start of the loan period, the cash balance will be $24,400. Accounts receivable on April 1 will total $151,200, of which $129,600 will be collected during April and $17,280 will be collected during May. The remainder will be uncollectible. Past experience shows that 30% of a month’s sales are collected in the month of sale, 60% in the month following sale, and 8% in the second month following sale. The other 2%…arrow_forwardProblem 8-31 (Algo) Completing a Master Budget [LO8-2, LO8-4, LO8-7, LO8-8, LO8-9, LO8-10] Hillyard Company, an office supplies specialty store, prepares its master budget on a quarterly basis. The following data have been assembled to assist in preparing the master budget for the first quarter: As of December 31 (the end of the prior quarter), the company’s general ledger showed the following account balances: Cash $ 41,000 Accounts receivable 200,800 Inventory 57,900 Buildings and equipment (net) 351,000 Accounts payable $ 85,425 Common stock 500,000 Retained earnings 65,275 $ 650,700 $ 650,700 Actual sales for December and budgeted sales for the next four months are as follows: December(actual) $ 251,000 January $ 386,000 February $ 583,000 March $ 297,000 April $ 194,000 Sales are 20% for cash and 80% on credit. All payments on…arrow_forward

- Problem 8-29 (Algo) Completing a Master Budget [LO8-2, LO8-4, LO8-7, LO8-8, LO8-9, LO8-10] The following data relate to the operations of Shilow Company, a wholesale distributor of consumer goods: Current assets as of March 31: Cash $ 7,600 Accounts receivable $ 20,400 Inventory $ 40,200 Building and equipment, net $ 128,400 Accounts payable $ 23,925 Common stock $ 150,000 Retained earnings $ 22,675 The gross margin is 25% of sales. Actual and budgeted sales data: March (actual) $ 51,000 April $ 67,000 May $ 72,000 June $ 97,000 July $ 48,000 Sales are 60% for cash and 40% on credit. Credit sales are collected in the month following sale. The accounts receivable at March 31 are a result of March credit sales. Each month’s ending inventory should equal 80% of the following month’s budgeted cost of goods sold. One-half of a month’s inventory purchases is paid for in the month of purchase; the…arrow_forwardProblem 8-31 (Algo) Completing a Master Budget [LO8-2, LO8-4, LO8-7, LO8-8, LO8-9, LO8-10] Hillyard Company, an office supplies specialty store, prepares its master budget on a quarterly basis. The following data have been assembled to assist in preparing the master budget for the first quarter: As of December 31 (the end of the prior quarter), the company’s general ledger showed the following account balances: Debits Credits Cash $ 60,000 Accounts receivable 216,000 Inventory 60,750 Buildings and equipment (net) 370,000 Accounts payable $ 91,125 Common stock 500,000 Retained earnings 115,625 $ 706,750 $ 706,750 Actual sales for December and budgeted sales for the next four months are as follows: December(actual) $ 270,000 January $ 405,000 February $ 602,000 March $ 317,000 April $ 213,000 Sales are 20% for cash and 80% on credit. All payments on credit sales are collected in the month following sale. The…arrow_forward12.1 Problem 8-25 (Algo) Cash Budget with Supporting Schedules; Changing Assumptions [LO8-2, LO8-4, LO8-8] Garden Sales, Inc., sells garden supplies. Management is planning its cash needs for the second quarter. The company usually has to borrow money during this quarter to support peak sales of lawn care equipment, which occur during May. The following information has been assembled to assist in preparing a cash budget for the quarter: Budgeted monthly absorption costing income statements for April–July are: April May June July Sales $ 460,000 $ 990,000 $ 440,000 $ 340,000 Cost of goods sold 322,000 693,000 308,000 238,000 Gross margin 138,000 297,000 132,000 102,000 Selling and administrative expenses: Selling expense 89,000 94,000 55,000 34,000 Administrative expense* 42,000 56,000 34,400 32,000 Total selling and administrative expenses 131,000 150,000 89,400 66,000 Net operating income $ 7,000 $…arrow_forward

- Problem 8-24 Cash Budget with Supporting Schedules [LO8-2, LO8-4, LO8-8] Garden Sales, Inc., sells garden supplies. Management is planning its cash needs for the second quarter. The company usually has to borrow money during this quarter to support peak sales of lawn care equipment, which occur during May. The following information has been assembled to assist in preparing a cash budget for the quarter: Budgeted monthly absorption costing income statements for April–July are: April May June July Sales $ 510,000 $ 710,000 $ 410,000 $ 310,000 Cost of goods sold 357,000 497,000 287,000 217,000 Gross margin 153,000 213,000 123,000 93,000 Selling and administrative expenses: Selling expense 71,000 91,000 52,000 31,000 Administrative expense* 40,500 53,600 32,600 29,000 Total selling and administrative expenses 111,500 144,600 84,600 60,000 Net operating income $ 41,500 $ 68,400 $ 38,400 $ 33,000…arrow_forwardProblem 8-29 (Algo) Completing a Master Budget [LO8-2, LO8-4, LO8-7, LO8-8, LO8-9, LO8-10]The following data relate to the operations of Shilow Company, a wholesale distributor of consumer goods: Current assets as of March 31: Cash $ 9,200Accounts receivable $ 26,800Inventory $ 49,800Building and equipment, net $ 104,400Accounts payable $ 29,925Common stock $ 150,000Retained earnings $ 10,275The gross margin is 25% of sales.Actual and budgeted sales data:March (actual) $ 67,000April $ 83,000May $ 88,000June $ 113,000July $ 64,000Sales are 60% for cash and 40% on credit. Credit sales are collected in the month following sale. The accounts receivable at March 31 are a result of March credit sales.Each month’s ending inventory should equal 80% of the following month’s budgeted cost of goods sold.One-half of a month’s inventory purchases is paid for in the month of purchase; the other half is paid for in the following month. The accounts payable at…arrow_forwardroblem 8-24 Cash Budget with Supporting Schedules [LO8-2, LO8-4, LO8-8] Garden Sales, Inc., sells garden supplies. Management is planning its cash needs for the second quarter. The company usually has to borrow money during this quarter to support peak sales of lawn care equipment, which occur during May. The following information has been assembled to assist in preparing a cash budget for the quarter: Budgeted monthly absorption costing income statements for April–July are: April May June July Sales $ 510,000 $ 710,000 $ 410,000 $ 310,000 Cost of goods sold 357,000 497,000 287,000 217,000 Gross margin 153,000 213,000 123,000 93,000 Selling and administrative expenses: Selling expense 71,000 91,000 52,000 31,000 Administrative expense* 40,500 53,600 32,600 29,000 Total selling and administrative expenses 111,500 144,600 84,600 60,000 Net operating income $ 41,500 $ 68,400 $ 38,400 $ 33,000…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education