MyFinanceLab With eText - Access (Custom Package)

15th Edition

ISBN: 9781269945684

Author: Pearson

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 8, Problem 8.17P

Learning Goal 5

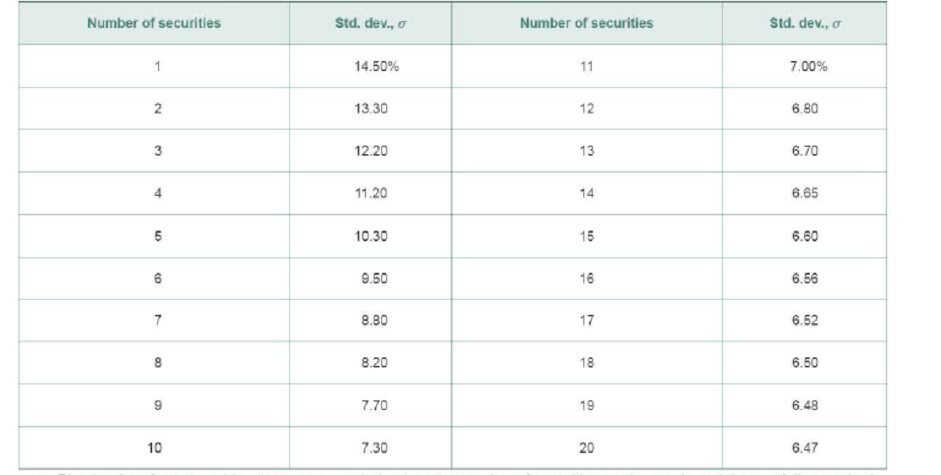

P8- 17 Total, nondiversifiable, and diversifiable risk David Talbot randomly selected securities from all those listed on the New York Stock Exchange for his portfolio. He began with a single security and added securities one by one until a total of 20 securities were held in the portfolio. After each security was added, David calculated the portfolio standard deviation, σ. The calculated values are shown in the following table

- a. Plot the data from the table above on a graph that has the number of sec unites on the x-axis and the portfolio standard deviation on the y-axis.

- b. Divide the total portfolio risk in the graph into its nondiversifiable and diversifiable risk components, and label each of these on the graph.

- c. Describe which of the two risk components is the relevant risk, and explain why it is relevant. How much of this risk exists in David Talbot’s portfolio?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Q2: A private investment club has $200,000 earmarked for investment in stocks. To arrive at an acceptable overall level of risk, the stocks that management is considering have been classified into three categories: high risk, medium risk, and low risk. Management estimates that high-risk stocks will have a rate of return of 15%/year; medium-risk stocks, 10%/year; and low-risk stocks, 6%/year. The members have decided that the investment in low-risk stocks should be equal to the sum of the investments in the stocks of the other two categories. Determine how much the club should invest in each type of stock if the investment goal is to have a return of $20,000/year on the total investment. (Assume that all the money available for investment is invested

9. Portfolio beta and weights

Brandon is an analyst at a wealth management firm. One of his clients holds a $5,000 portfolio that consists of four stocks. The investment allocation in the portfolio along with the contribution of risk from each stock is given in the following table:

Stock

Investment Allocation

Beta

Standard Deviation

Atteric Inc. (AI)

35%

0.750

38.00%

Arthur Trust Inc. (AT)

20%

1.400

42.00%

Li Corp. (LC)

15%

1.300

45.00%

Transfer Fuels Co. (TF)

30%

0.500

49.00%

Brandon calculated the portfolio’s beta as 0.888 and the portfolio’s required return as 12.6600%.

Brandon thinks it will be a good idea to reallocate the funds in his client’s portfolio. He recommends replacing Atteric Inc.’s shares with the same amount in additional shares of Transfer Fuels Co. The risk-free rate is 6%, and the market risk premium is 7.50%.

A. According to Brandon’s recommendation, assuming that the market is in equilibrium, how much will the portfolio’s…

onsider 123 Fund (which is invested in 35% High risk stock and 65% normal bonds).

Assume you have the following historical data of annual returns:

Return S.D.

Normal Stock 8% 20%

Risky Bonds 10% 35%

High Risk Stock 14% 40%

Normal Bonds 6% 10%

Assume High Risk Stocks and Normal Bonds have correlation coefficient of 0.24

Find the standard deviation of 123.

Please use 5 decimal places in your response.

Note: The right answer is 0.1679 Please explain step by step

Chapter 8 Solutions

MyFinanceLab With eText - Access (Custom Package)

Ch. 8.1 - Prob. 1FOECh. 8.1 - What is risk in the context of financial decision...Ch. 8.1 - Prob. 8.2RQCh. 8.1 - Prob. 8.3RQCh. 8.2 - Explain how the range is used in scenario...Ch. 8.2 - Prob. 8.5RQCh. 8.2 - Prob. 8.6RQCh. 8.2 - What does the coefficient of variation reveal...Ch. 8.3 - What is an efficient portfolio? How can the return...Ch. 8.3 - Prob. 8.9RQ

Ch. 8.3 - How does international diversification enhance...Ch. 8.4 - Prob. 8.11RQCh. 8.4 - Prob. 8.12RQCh. 8.4 - Prob. 8.13RQCh. 8.4 - What impact would the following changes have on...Ch. 8 - Prob. 1ORCh. 8 - Prob. 8.1STPCh. 8 - Prob. 8.2STPCh. 8 - Prob. 8.1WUECh. 8 - Prob. 8.2WUECh. 8 - Prob. 8.3WUECh. 8 - Prob. 8.4WUECh. 8 - Prob. 8.5WUECh. 8 - Prob. 8.6WUECh. 8 - Prob. 8.1PCh. 8 - Prob. 8.2PCh. 8 - Prob. 8.3PCh. 8 - Prob. 8.4PCh. 8 - Prob. 8.5PCh. 8 - Learning Goal 2 P8-6 Bar charts and risk Swans...Ch. 8 - Prob. 8.7PCh. 8 - Prob. 8.8PCh. 8 - Prob. 8.9PCh. 8 - Prob. 8.10PCh. 8 - Prob. 8.11PCh. 8 - Prob. 8.12PCh. 8 - Prob. 8.13PCh. 8 - Prob. 8.14PCh. 8 - Learning Goal 4 P8- 15 Correlation, risk, and...Ch. 8 - Prob. 8.16PCh. 8 - Learning Goal 5 P8- 17 Total, nondiversifiable,...Ch. 8 - Prob. 8.18PCh. 8 - Prob. 8.19PCh. 8 - Prob. 8.20PCh. 8 - Prob. 8.21PCh. 8 - Prob. 8.22PCh. 8 - Prob. 8.23PCh. 8 - Prob. 8.24PCh. 8 - Prob. 8.25PCh. 8 - Prob. 8.26PCh. 8 - Prob. 8.27PCh. 8 - Learning Goal 6 P8- 28 Security market line (SML)...Ch. 8 - Prob. 8.29PCh. 8 - Prob. 8.30PCh. 8 - Prob. 8.31PCh. 8 - Prob. 1SE

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Subject: Financial strategy & policy 8-2: PORTFOLIO BETA An individual has $35,000 invested in a stock with a beta of 0.8 and another $40,000 invested in a stock with a beta of 1.4. If these are the only two investments in her portfolio, what is her portfolio’s beta? 8-3: REQUIRED RATE OF RETURN Assume that the risk-free rate is 6% and the expected return on the market is 13%. What is the required rate of return on a stock with a beta of 0.7? 8-4: EXPECTED AND REQUIRED RATES OF RETURN Assume that the risk-free rate is 5% and the market risk premium is 6%. What is the expected return for the overall stock market? What is the required rate of return on a stock with a beta of 1.2?arrow_forwardProblem 1. A client invested $100 in a mutual fund at the start of the month. After 20 days, the portfolio gained 10% (i.e., value = $110), and the client added an extra $50 (total portfolio value=$160). From day 20 to day 30, the portfolio lost 9.09%--the final portfolio value is $160×(1-0.0909)=$145.46. Calculate the money-weighted return and time-weighted return. Which rate of should you use to evaluate the performance of the mutual fund manager?arrow_forwardfinancial advisor evaluates four stocks for inclusion in an investor's portfolio. A orrelation matrix showing each stock's correlation with the other stocks is shown below Stock ALK CMN BTY DLE ALK 0.40 0.58 1.00 -0.25 BTY 0.40 1.00 0.16 -0.04 CMN -.25 .16 1.00 .37 DLE .58 .04 .37 1.00 f the goal is to reduce the investor's overall portfolio risk, which two stocks should the advisor recommend? a. ALK and DLE b. ALK and CMN c. BTY and DLE BTY and CMarrow_forward

- In-class Example 4: Portfolio Risk Return Suppose that a portfolio of stocks has an expected return E(rS) = 12% and a standard deviation of returns sS = 20%. A portfolio of corporate bonds has an expected return E(rB) = 6% and a standard deviation sB = 9%. a) What is the expected portfolio return and portfolio standard deviation for an equally weighted combination of the stock and bond portfolio if the correlation between stock and bond portfolio returns, rSB, is -0.5? b) Suppose you require a portfolio expected return of 15% per year. What weights must you assign to the stock and bond portfolios to achieve this expected return? What is the standard deviation of returns for this combination portfolio if the correlation between stock and bond returns is -0.5? C) Suppose that the standard deviation of the market (sM) is 15% and the correlation between the stock portfolio and the market is 0.7. What is the beta of the stock portfolio?arrow_forwardStandard Deviation for portfolio of two risky investments: Mary Guilott recently graduated from college and is evaluating an investment in two companies common stock. She has collected the following information about the common stock of firm A and firm B: Firm A's common stock: 0.15 (expected return), 0.11(standard Deviation) Firm B's common stock: 0.11 (expected return), 0.06 (standard Deviation) Correlation Coefficient: 0.5 If mary decides to invest 10% of her money in Firm A's common stock and 90% in Firm B's common stock, what is the expected rate of return and the standard deviation of the portfolioarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:9781337514835

Author:MOYER

Publisher:CENGAGE LEARNING - CONSIGNMENT

Chapter 8 Risk and Return; Author: Michael Nugent;https://www.youtube.com/watch?v=7n0ciQ54VAI;License: Standard Youtube License