Videos

Intercorporate Inventory and Debt Transfers (Effective Interest Method)

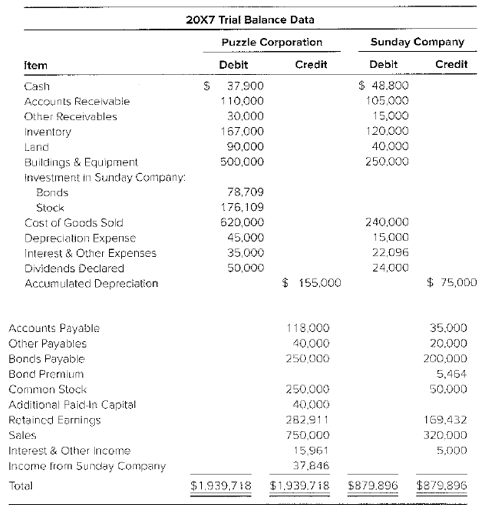

Puzzle Corporation purchased 75 percent of Sunday Company’s common stock at underlying book value on January 1, 20X3. At that date, the fair value of the noncontrolling interest was equal to 25 percent of Sunday’s book value.

During 20X7, Puzzle resold inventory purchased from Sunday in 20X6. It had cost Sunday $44,000 to produce the inventory, and Puzzle had purchased it for $59,000. In 20X7, Puzzle had purchased inventory for $40,000 and sold it to Sunday for $60,000. At December 31, 20X7. Sunday continued to hold $27,000 of the inventory.

Sunday had issued $200,000 of 8 percent, 10−year bonds on January 1, 20X4, at 104. Puzzle had purchased $80,000 of the bonds from one of the original owners for $78,400 on December 31, 20X5. Interest is paid annually on December 31. Assume Puzzle uses the fully adjusted equity method.

Required

a. What amount of cost of goods sold will be reported in the 20X7 consolidated income statement?

b. What inventory balance will be reported in the December 31, 20X7, consolidated

c. Prepare the

d. Prepare the journal entry to record interest income for Puzzle for 20X7.

e. What amount will be assigned to the noncontrolling interest in the consolidated balance sheet prepared at December 31, 20X7?

f. Prepare all consolidation entries needed at December 31, 20X7, to complete a three−part consolidation worksheet.

g. Prepare a consolidation worksheet for 20X7 in good form.

a

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

Amount of cost of goods sold to be reported in consolidated income statement.

Answer to Problem 8.25P

Cost of goods sold to be reported in consolidated income statement is $794,000

Explanation of Solution

| $ | $ | |

| Amount of cost of goods reported by P corporation | 620,000 | |

| Amount of cost of goods reported by S corporation | 240,000 | |

| Adjustment of unrealized profit on inventory purchased by P from S | (15,000) | |

| Adjustment of inventory purchased from subsidiary and resold 20X7 | ||

| CGS intercompany sales recorded by P | 40,000 | |

| CGS intercompany sales recorded by S | 33,000 | |

| Total | 73,000 | |

| CGS based on P’s cost 40,000 x (33,000 /60,000) | (22,000) | |

| Required adjustment | (51,000) | |

| Cost of goods sold | 794,000 |

b.

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

Inventory balance to be reported in consolidated balance sheet December 31 20X7

Answer to Problem 8.25P

Consolidated inventory balance to be reported in consolidated balance sheet is $278,000

Explanation of Solution

| $ | |

| Amount of inventory reported by P | 167,000 |

| Amount of inventory reported by S | 120,000 |

| Total | 287,000 |

| Less: Unrealized profit in ending inventory held by S | (9,000) |

| Consolidated inventory balance | 278,000 |

c.

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

Journal entry to record interest expenses by S

Explanation of Solution

| Particulars | Debit $ | Credit $ |

| Interest expense | 15,200 | |

| Bond premium | 800 | |

| Cash | 16,000 | |

| (Paid cash on account of interest expense) |

Computation of interest expenses

| Par value of bond issued | $200,000 |

| Annual Interest | $16,000 |

| Annual amortization of premium ($4,800 /6 years) | (800) |

| Interest expenses | $15,200 |

d.

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

Journal entry to record interest income for S

Explanation of Solution

| Particulars | Debit $ | Credit $ |

| Cash | $6,400 | |

| Investment in A company bond | 200 | |

| Interest income | 6,600 | |

| (Received cash on account of interest income and premium on bond amortized) |

Computation of interest income

| Annual payment received | $6,400 |

| Amortization of discount | 200 |

| Interest income | $6,600 |

e.

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

The income assigned to non-controlling interest in consolidated balance sheet

Answer to Problem 8.25P

Amount of income assigned to non-controlling interest $15,620

Explanation of Solution

| $ | |

| Net income reported by S | 48,000 |

| Adjustment for realization of profit on inventory sold to P | 15,000 |

| Adjustment of gain on bond retirement | (520) |

| Realized net income | 62,480 |

| Income assigned to non-controlling interest | 15,620 |

Computation of gain on bond retirement

| $ | $ | |

| Par value of bond | 200,000 | |

| Amortization per year | 800 | |

| Premium maturity value Dec 31 20X5 | 6,400 | |

| Book value of bond | 206,400 | |

| Book value of bond purchase | 82,560 | |

| Purchase price | (78,400) | |

| Gain | 4,160 |

f.

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

Preparation of consolidation entries needed at December 31 20X7 to complete consolidation worksheet.

Explanation of Solution

| Particulars | Debit $ | Credit $ |

| To eliminate income from subsidiary | ||

| Income from subsidiary | 36,000 | |

| Dividends declared | 18,000 | |

| Investment in S company stock | 18,000 | |

| (Income from subsidiary eliminated by reversal) | ||

| Assign income to non-controlling interest. | ||

| Income to non-controlling interest | 15,620 | |

| Dividends declared | 6,000 | |

| Non-controlling interest | 9,620 | |

| (Income assigned to non-controlling interest) | ||

| Eliminate beginning investment balance | ||

| Common stock S company | 50,000 | |

| Retained earnings January 1 | 170,000 | |

| Investment in A’s stock | 165,000 | |

| Non-controlling interest | 55,000 | |

| (Beginning investment in S stock eliminated by reversal) | ||

| Eliminating beginning inventory profit | ||

| Retained earnings, January 1 | 11,250 | |

| Non-controlling interest | 3,750 | |

| Cost of goods sold | 15,000 | |

| (Unrealized profit on beginning inventory eliminated) | ||

| Eliminating intercompany sale of inventory by P | ||

| Sales | 60,000 | |

| Cost of goods sold | 51,000 | |

| Inventory | 9,000 | |

| (Intercompany profit on sale of inventory eliminated) | ||

| Eliminating intercompany bond holdings | ||

| Bond payable | 80,000 | |

| Bond premium | 1,920 | |

| Interest income | 6,600 | |

| Investment on S company’s bonds | 78,800 | |

| Interest expenses | 6,080 | |

| Retained earnings, January 1 | 2,730 | |

| Non-controlling interest | 910 | |

| (Intercompany bond holdings eliminated by reversal) |

- Income from subsidiary is eliminated by debiting to income from subsidiary account.

- Assignment of income to non-controlling interest

Realized net income by S company

| Net income reported by S | $48,000 |

| Realization of profit on inventory sold to P(59,000 − 44,000) | $15,000 |

| Adjustment of gain on bond retirement ($4,160 / 8 years) | (520) |

| Realized net income | 62,480 |

- Common stock and retained earnings in the beginning of the year was $170,000 and 50,000 which is $220,000 eliminating by crediting to investment in S account and non- controlling interest account in the ratio of parental and subsidiary holdings.

- Beginning inventory profit of $15,000 is eliminated as required by debiting retained earnings at 75% and non-controlling interest by 25%.

- Intercompany sale of inventory is eliminated by posting reversal entry.

- Eliminating corporate bond holding

Bond premium:

| Bond premium given | $4,800 |

| P bond discount 80,000 − 78,400 | (1,600) |

| Net premium on bond | $3,200 |

Calculation of bond investment value:

| Bonds purchase consideration | $78,400 |

| Amortization of discount (1,600 / 8 years) | 200 |

| Bond investment value | $78,800 |

Calculation of interest expenses:

| $6,400 | |

| Less amortization of premium ($3,200 / 10 years) | (320) |

| Interest expenses | $6,080 |

g.

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

The preparation of consolidation worksheet for 20X7

Answer to Problem 8.25P

The following are the balances reported in consolidation work sheet for 20X7:

- Retained earnings $337,040

- Total Assets $1,274,700

Explanation of Solution

P Corporation and S Corporation

Consolidation worksheet

December 31, 20X7

| Elimination | |||||

| P $ | S $ | Debit $ | Credit $ | Consolidation $ | |

| Sales | 750,000 | 320,000 | 60,000 | 1,010,000 | |

| Interest and other income | 16,000 | 5,000 | 6,600 | 14,400 | |

| Income from subsidiary | 36,000 | 36,000 | |||

| 802,000 | 325,000 | 1,024,400 | |||

| Less: Cost of goods sold | (620,000) | (240,000) | 15,000 | ||

| 51,000 | (794,000) | ||||

| Depreciation expenses | (45,000) | (15,000) | (60,000) | ||

| Interest and other expenses | (35,000) | (22,000) | 6,080 | (50,920) | |

| Consolidated net income | $119,480 | ||||

| Income to NCI | 15,620 | (15,620) | |||

| Net income | 102,000 | 48,000 | 118,220 | 72,080 | 103,860 |

| Retained earnings Jan 1 | 291,700 | 170,000 | 170,000 | 2,730 | |

| 11,250 | 283,180 | ||||

| 393,700 | 218,000 | 387,040 | |||

| Dividends declared | (50,000) | (24,000) | 18,000 | ||

| 6,000 | (50,000) | ||||

| Retained earnings Dec 31 | 343,700 | 194,000 | 299,470 | 98,810 | 337,040 |

| Balance sheet: | |||||

| Cash | 37,900 | 48,800 | 86,700 | ||

| Accounts receivable | 110,000 | 105,000 | 215,000 | ||

| Other receivable | 30,000 | 15,000 | 45,000 | ||

| Inventory | 167,000 | 120,000 | 9,000 | 278,000 | |

| Land | 90,000 | 40,000 | 130,000 | ||

| Investment in S’s bonds | 78,800 | 78,800 | |||

| Investment in S’s Stock | 183,000 | 18,000 | |||

| 165,000 | |||||

| Buildings and Equipment | 500,000 | 250,000 | 750,000 | ||

| Less Accumulated Depreciation | (155,000) | (75,000) | (230,000) | ||

| Total Assets | 1,041,700 | 175,000 | 1,274,700 | ||

| Accounts payable | 118,000 | 35,000 | 153,000 | ||

| Other payable | 40,000 | 20,000 | 60,000 | ||

| Bonds payable | 250,000 | 200,000 | 80,000 | 370,000 | |

| Bonds premium | 4,800 | 1,920 | 2,880 | ||

| Common Stock: | |||||

| P company | 250,000 | 250,000 | |||

| S company | 50,000 | 50,000 | |||

| Additional Paid in capital | 40,000 | 40,000 | |||

| Retained earnings Dec 31 | 343,700 | 194,000 | 299,470 | 98,810 | 337,040 |

| Non-controlling interest | 3,750 | 9,620 | |||

| 55,000 | |||||

| 910 | 61,780 | ||||

| Total Liability and Equity | 1,041,700 | 175,000 | 1,274,700 | ||

Want to see more full solutions like this?

Chapter 8 Solutions

ADVANCED FINANCIAL ACCOUNTING-ACCESS

- Peanut Company acquired 80 percent of Snoopy Company's outstanding common stock for $300,000 on January 1, 20X8, when the book value of Snoopy's net assets was equal to $375,000. Peanut uses the equity method to account for investments. The following trial balance summarizes the financial position and operations for Peanut and Snoopy as of December 31, 20X9 Snoopy Company Cash Accounts Receivable Inventory Investment in Snoopy Company Land Buildings and Equipment Cost of Goods Sold Depreciation Expense Selling & Administrative Expense Dividends Declared Accumulated Depreciation Accounts Payable Bonds Payable Common Stock Retained Earnings Sales Income from Snoopy Company Total Peanut Company Debit $ 270,000 191,000 196,000 315,000 207,000 714,000 375,000 46,000 225,000 213,000 $2,752,000 Credit $494,000 56,000 133,000 493,000 656,600 842,000 77,400 $ 2,752,000 Debit $ 85,000 90,000 100,000 0 96,000 181,000 169,000 12,000 35,250 38,000 $ 806,250 Required: a. Prepare any equity method…arrow_forwardPie Corporation acquired 60 percent of Slice Company’s common stock on December 31, 20X5, at underlying book value. The book values and fair values of Slice’s assets and liabilities were equal, and the fair value of the noncontrolling interest was equal to 40 percent of the total book value of Slice. Slice provided the following trial balance data at December 31, 20X5: Debit Credit Cash $ 27,600 Accounts Receivable 64,900 Inventory 91,600 Buildings and Equipment (net) 216,000 Cost of Goods Sold 103,300 Depreciation Expense 24,450 Other Operating Expenses 31,060 Dividends Declared 15,800 Accounts Payable $ 32,000 Notes Payable 127,000 Common Stock 94,800 Retained Earnings 130,000 Sales 190,910 Total $ 574,710 $ 574,710 Required: How much did Pie pay to purchase its shares of Slice? Note: Round your answer to nearest whole dollar amount. If consolidated financial statements are prepared at December 31, 20X5, what amount…arrow_forwardPeel Corporation purchased 60 percent of Split Products Company's shares on December 31, 20X7, for $216,000. At that date, the fair value of the noncontrolling interest was $144,000. On January 1, 20X9, Peel purchased an additional 20 percent of Split's common stock for $97,000. Summarized balance sheets for Split on the dates indicated are as follows: Assets Cash Accounts Receivable Inventory Buildings & Equipment (net) Total Assets Liabilities & Equities Accounts Payable Bonds Payable Common Stock Retained Earnings Total Liabilities & Equities 20X7 $ 49,000 51,000 72,000 370,000 $542,000 December 31 20X8 Balance in investment account $ 79,000 91,000 102,000 350,000 $622,000 20X9 $ 99,000 121,000 162,000 330,000 $712,000 $ 77,000 $127,000 $167,000 105,000 105,000 105,000 155,000 155,000 155,000 205,000 235,000 285,000 $542,000 $622,000 $712,000 Split paid dividends of $22,000 in each of the three years. Peel uses the equity method in accounting for its investment in Split and…arrow_forward

- Assume that Birch made intra-entity inventory transfers to Aspen that have resulted in the following intra-entity gross profits in inventory at the end of each year: Date Amount 12/31/19 $13,000 12/31/20 23,300 12/31/21 30,200 On January 1, 2019, Aspen Company acquired 80 percent of Birch Company's voting stock for $500,000. Birch reported a $490,000 book value, and the fair value of the noncontrolling interest was $125,000 on that date. Then, on January 1, 2020, Birch acquired 80 percent of Cedar Company for $224,000 when Cedar had a $253,000 book value and the 20 percent noncontrolling interest was valued at $56,000. In each acquisition, the subsidiary's excess acquisition-date fair over book value was assigned to a trade name with a 30-year remaining life. These companies report the following financial information. Investment income figures are not included. 2019 2020 2021 Sales: Aspen Company $ 637,500 $ 650,000 $ 732,500 Birch…arrow_forwardPeanut Company acquired 80 percent of Snoopy Company's outstanding common stock for $260,000 on January 1, 20X8, when the book value of Snoopy's net assets was equal to $325,000. Peanut uses the equity method to account for investments. The following trial balance summarizes the financial position and operations for Peanut and Snoopy as of December 31, 20X9: Cash Accounts Receivable Inventory Investment in Snoopy Company Land Buildings and Equipment Cost of Goods Sold Depreciation Expense Selling & Administrative Expense Dividends Declared Accumulated Depreciation Accounts Payable Bonds Payable Common Stock Retained Earnings Sales Income from Snoopy Company Total Peanut Company Debit $ 264,000 204,000 184,000 325,600 213,000 719,000 325,000 42,000 214,000 214,000 $ 2,704,600 Credit $ 491,000 59,000 131,000 499,000 609,400 836,000 79,200 $ 2,704,600 Debit Snoopy Company $ 82,000 87,000 102,000 0 88,000 195,000 161,000 15,000 38,000 33,000 $ 801,000 Required: a. Prepare any equity method…arrow_forward4 Peanut Company acquired 80 percent of Snoopy Company's outstanding common stock for $300,000 on January 1, 20X8, when the book value of Snoopy's net assets was equal to $375,000. Peanut uses the eguity method to account for Investments. The following trial balance summarizes the financial position and operations for Peanut and Snoopy as of December 31, 20X9: Peanut Company Snoopy Company Credit Debit Credit Debit $ 272,000 $ 77,000 82, 000 Cash Accounts Receivable 200, eee Inventory 193,e00 319,800 216,e00 706,000 118,000 Investment in Snoopy Company Land 81,000 Buildings and Equipment 199, 000 155,000 13,000 54, 250 34,000 Cost of Goods Sold 375,000 Depreciation Expense Selling & Administrative Expense Dividends Declared 47,000 221,000 224,e00 $ 487,000 $ 39,e00 Accumulated Depreciation Accounts Payable Bonds Payable 55,000 39,e00 137,000 79,250 Common Stock Retained Earnings 491,000 682,400 187,e00 158,eee 319, e00 Sales 844,000 Income from Snoopy Company 77,400 Total $2,773,800…arrow_forward

- Required information On January 1, 20X2, Power Company acquired 80 percent of Strong Company's outstanding stock for cash. The fair value of the noncontrolling interest was equal to a proportionate share of the book value of Strong Company's net assets at the date of acquisition. Selected balance sheet data at December 31, 20X2 are as follows: Total Assets Liabilities Common Stock Retained Earnings Total Liabilities & Stockholders' Equity Multiple Choice O $35,200 Based on the preceding information, what amount should be reported as noncontrolling interest in net assets in Power Company's December 31, 20X2, consolidated balance sheet? $48,200 $76,800 Power $ 564,000 O $112,800 180,000 150,000 234,000 $ 564,000 Strong $ 216,000 65,000 80,000 96,000 $ 241,000arrow_forwardOn December 29, 20x1, ABC Co. acquires 1,000 units of an investment through a broker at P1.00 per unit, the quoted price on this date. Ownership over the financial asset transfers to ABC Co. on January 3, 20x2. The fair values per unit on December 31, 20x1 and January 3, 20x2 are P1.75 and P1.50, respectively Requirements: Provide the journal entries under the trade date accounting and the settlement date accounting assuming the financial asset purchased is classified as subsequently measured at: a. FVPL (held for trading securities), b. FVOCI (mandatory); and Amortized cost.arrow_forward2) On January 1, 20X5, Peery Company acquired 100 percent of Standard Company's common shares at underlying book value. Peery uses the equity method in accounting for its ownership of Standard. On December 31, 20X5, the trial balances of the two companies are as follows: Item Current Assets Depreciable Assets Investment in Standard Company Other Expenses Depreciation Expense Dividends Declared Accumulated Depreciation Current Liabilities Long-Term Debt Common Stock Retained Earnings Sales Income from Standard Company Peery Company Debit $ 238,000 300,000 100,000 90,000 30,000 32,000 Credit $ 120,000 50,000 120,000 100,000 175,000 200,000 25,000 Standard Company Debit Credit $ 95,000 170,000 70,000 17,000 10,000 $ 790,000 $ 790,000 $362,000 $ 85,000 30,000 50,000 50,000 35,000 112,000 $362,000 Required: 1. Prepare the consolidation entries needed as of December 31, 20X5, to complete a consolidation worksheet. 2. Prepare a three-part consolidation worksheet as of December 31, 20X5.arrow_forward

- On December 31, 20X8, Paragraph Corporation acquired 80 percent of Sentence Company's common stock for $136,000. At the acquisition date, the book values and fair values of all of Sentence's assets and liabilities were equal. Paragraph uses the equity method in accounting for its investment. Balance sheet information provided by the companies at December 31, 20X8, immediately following the acquisition is as follows: Cash Accounts Receivable Inventory Fixed Assets (net) Investment in Sentence Co. Total Debits Accounts Payable Notes Payable Common Stock Retained Earnings Total Credits Assets Paragraph Corporation $ 74,000 120,000 180,000 Total Assets Liabilities and Stockholders' Equity 350,000 136,000 $860,000 Total Liabilities and Stockholders' Equity $ 65,000 350,000 150,000 295,000 $860,000 PARAGRAPH CORPORATION AND SUBSIDIARY Consolidated Balance Sheet December 31, 20X8 Required: Prepare a consolidated balance sheet for Paragraph at December 31, 20X8. Sentence Company $ 20,000…arrow_forwardBronze Corporation agrees to acquire the net assets of Wall Corporation on January 1, 20X1. Wall has the following balance sheet on the date of acquisition: Wall Corporation Balance Sheet January 1, 20X1 Assets Liabilities and Equity Accounts receivable . . . . . . . . . $ 79,000 Current liabilities . . . . . . . . . . . . . . $145,000 Inventory . . . . . . . . . . . . . . . . . . 112,000 Bonds payable . . . . . . . . . . . . . . . 100,000 Other current assets . . . . . . . . . . 55,000 Common stock . . . . . . . . . . . . . . . . 200,000 Equipment (net) . . . . . . . . . . . . . 294,000 Paid-in capital in excess of par . . . 50,000 Trademark . . . . . . . . . . . . . . . . . 30,000 Retained earnings . . . . . . . . . . . . . 75,000 Total assets. . . . . . . . . . . . . . . $570,000 Total liabilities and equity . . . . . $570,000 An appraiser determines that in-process R&D exists and has an estimated value of $14,000. The appraisal indicates that the following assets have fair…arrow_forwardAAA acquired a 70% interest in BBB on January 2, 20x1 for $468,000 when BBB net assets had a book value and fair value of $790,000. During 20x1, AAA sold inventory items that cost $780,000 to BBB for $1,040,000 and BBB's inventory at December 31, 20x1 included 1/2 of the merchandise. BBB also sold to AAA an inventory for $15,000 with a cost of $12,500, 70% were sold to unaffiliated customers. AAA reported separate income from its own operation of $585,000 and BBB reported a net loss of P390,000. Compute for the consolidated net income.arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education