Concept explainers

Videos

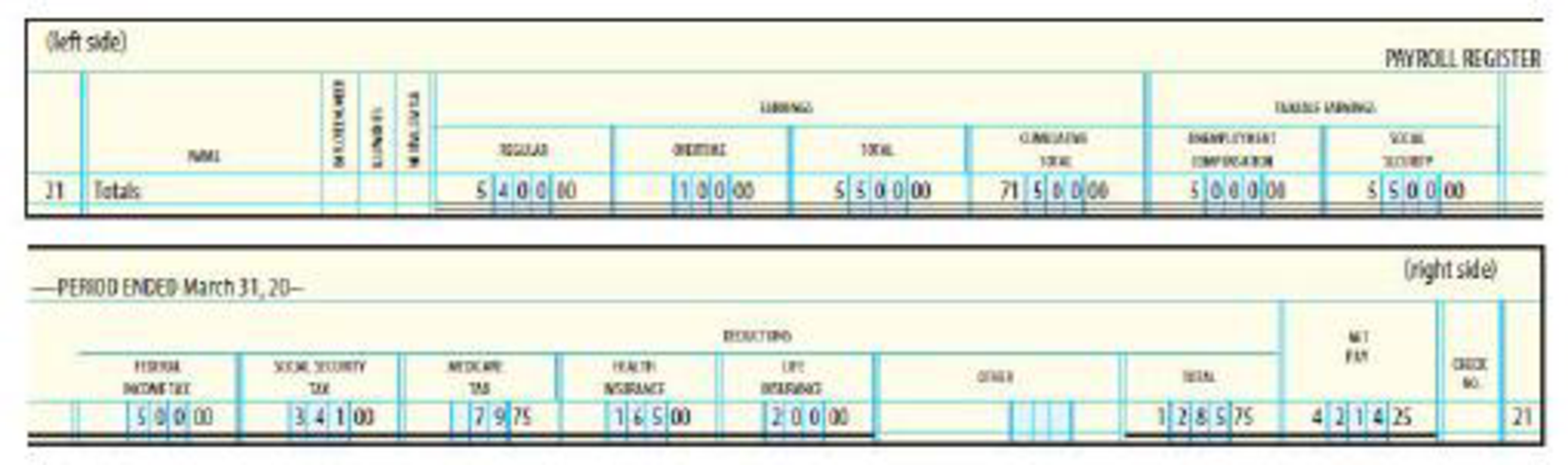

The totals line from Nix Company’s payroll register for the week ended March 31, 20--, is as follows:

Payroll taxes are imposed as follows: Social Security tax, 6.2%; Medicare tax, 1.45%; FUTA tax, 0.6%; and SUTA tax, 5.4%.

REQUIRED

- 1.

- a. Prepare the

journal entry for payment of this payroll on March 31, 20--. - b. Prepare the journal entry for the employer’s payroll taxes for the period ended March 31, 20--.

- a. Prepare the

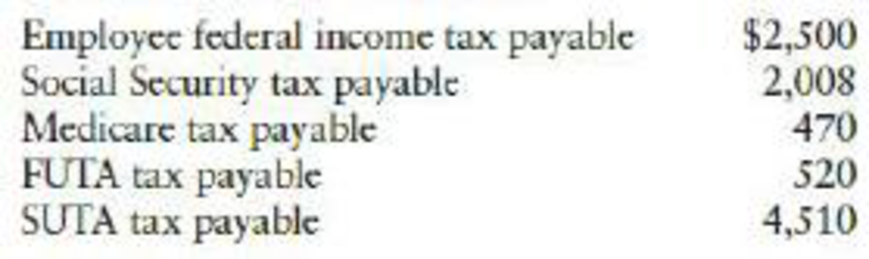

- 2. Nix Company had the following balances in its general ledger before the entries for requirement ( 1 ) were made:

- a. Prepare the journal entry for payment of the liabilities for federal income taxes and Social Security and Medicare taxes on April 15, 20--.

- b. Prepare the journal entry for payment of the liability for FUTA tax on April 30, 20--.

- c. Prepare the journal entry for payment of the liability for SUTA tax on April 30, 20--.

1.

a. Prepare the journal entry for payment of this payroll on March 31.

b. Prepare the journal entry for the employer’s payroll taxes for the period ended March 31.

Explanation of Solution

Payroll:

Payroll refers to the total amount that is required to be paid by the company to its employees during a week, month or other period. It is the financial record of the wages and bonus, net pay, salary and deductions of a company’s employees.

a. Prepare the journal entry for payment of this payroll on March 31, 20--

| Date | Account Title and explanation | Post. ref | Debit ($) | Credit ($) |

| March 31 | Wages and Salaries expense | 5,500 | ||

| Employee federal income tax payable | 500.00 | |||

| FICA-Social Security taxes payable | 341.00 | |||

| FICA-Medicare Taxes payable | 79.75 | |||

| Health insurance premium payable | 165.00 | |||

| Life insurance premium payable | 200.00 | |||

| Cash | 4,214.25 | |||

| (To record the payroll for the week ended March 31) |

Table (1)

- Wages and Salaries expense is an expense account and it is increased. Hence, debit wages and salaries expense with $5,500.00

- Employee Federal income tax payable is a liability and there is an increase in the value of liability. Hence, credit the employee Federal income tax payable by $500.00

- FICA tax – social and security tax payable is a liability and there is an increase in the value of liability. Hence, credit the FICA tax – social and security tax payable by $341.00

- FICA tax – medical tax payable is a liability and there is an increase in the value of liability. Hence, credit the FICA tax – medical tax payable by $79.75.

- Health insurance premium payable is a liability and it is increased. Hence, credit health insurance premium payable by $165.00.

- Life insurance premium payable is a liability and it is increased. Hence, credit life insurance premium payable by $200.00

- Cash is an asset and there is a decrease in the value of an asset. Hence, credit the cash by $4,214.25.

b. Prepare the journal entry for the employer’s payroll taxes for the period ended March 31, 20--

| Date | Account Title and explanation | Post. ref | Debit ($) | Credit ($) |

| March 31 | Payroll tax expense | 720.75 | ||

| FICA-Social Security taxes payable | 341.00 | |||

| FICA-Medicare Taxes payable | 79.75 | |||

| FUTA tax payable | 30.00 | |||

| SUTA tax payable | 270.00 | |||

| (To record the employer payroll taxes for the week ended March 31) |

Table (2)

- Payroll taxes expense is an expense account and it is increased. Hence, debit payroll taxes expense with $720.75.

- FICA tax – social and security tax payable is a liability and there is an increase in the value of liability. Hence, credit the FICA tax – social and security tax payable by $341.00.

- FICA tax – medical tax payable is a liability and there is an increase in the value of liability. Hence, credit the FICA tax – medical tax payable by $79.75.

- FUTA tax payable is a liability and it is increased. Hence, credit FUTA tax payable by $30.00.

- SUTA tax payable is a liability and it is increased. Hence, credit SUTA tax payable by $270.00.

2.

a. Prepare the journal entry for payment of the liabilities for federal income taxes and Social Security and Medicare taxes on April 15.

b. Prepare the journal entry for payment of the liability for FUTA tax on April 30.

c. Prepare the journal entry for payment of the liability for SUTA tax on April 30.

Explanation of Solution

a. Prepare the journal entry for payment of the liabilities for federal income taxes and Social Security and Medicare taxes on April 15.

| Date | Account Title and explanation | Post. ref | Debit ($) | Credit ($) |

| April 15 | Employee federal income tax payable (1) | 3,000.00 | ||

| FICA-Social Security taxes payable (2) | 2,690.00 | |||

| FICA-Medicare Taxes payable (3) | 629.50 | |||

| Cash | 6,319.50 | |||

| (To record the deposit of employee federal income tax and social security and Medicare taxes.) |

Table (3)

- Employee federal income tax payable is a liability and it is decreased. Hence, debit employee federal income tax payable by $3,000.00.

- FICA tax – social and security tax payable is a liability and there is a decrease in the value of liability. Hence, debit the FICA tax – social and security tax payable by $2,690.00.

- FICA tax – medical tax payable is a liability and there is a decrease in the value of liability. Hence, debit the FICA tax – medical tax payable by $629.50.

- Cash is an asset and there is a decrease in the value of an asset. Hence, credit the cash by $6,319.50.

b. Prepare the journal entry for payment of the liability for FUTA tax on April 30.

| Date | Account Title and explanation | Post. ref | Debit ($) | Credit ($) |

| April 30 | FUTA tax payable (4) | 550.00 | ||

| Cash | 550.00 | |||

| (To record the payment of FUTA tax) |

Table (4)

- FUTA tax payable is a liability and it is decreased. Hence, debit FUTA tax payable by $550.00.

- Cash is an asset and there is a decrease in the value of an asset. Hence, credit the cash by $550.00.

c. Prepare the journal entry for payment of the liability for SUTA tax on April 30.

| Date | Account Title and explanation | Post. ref | Debit ($) | Credit ($) |

| April 30 | SUTA tax payable (5) | 4,780.00 | ||

| Cash | 4,780.00 | |||

| (To record the payment of SUTA tax) |

Table (5)

- SUTA tax payable is a liability and it is decreased. Hence, debit SUTA tax payable by $4,780.00.

- Cash is an asset and there is a decrease in the value of an asset. Hence, credit the cash by $4,780.00

Working Notes:

(1) Calculate the employee federal income tax payable.

(2) Calculate the social security tax payable.

(3) Calculate the Medicare tax payable.

(4) Calculate the FUTA tax payable.

(5) Calculate the SUTA tax payable.

3.

Prepare the adjusting entry to reflect the overpayment of the insurance premium at the end of the year December 31.

Explanation of Solution

Prepare the adjusting entry to reflect the overpayment of the insurance premium at the end of the year December 31.

| Date | Account Title and explanation | Post. ref | Debit ($) | Credit ($) |

| December 31 | Insurance refund receivable (6) | 20.00 | ||

| Workmen’s compensation insurance expense | 20.00 | |||

| (To record the adjustment for insurance premium) |

Table (6)

- Insurance refund receivable is an asset and there is an increase in the value of an asset. Hence, debit the Insurance refund receivable by $20.00.

- Workmen’s compensation insurance expense is a component of stockholder’s equity and the expense has decreased. Hence, credit the workmen’s compensation insurance expense by $20.00

Working Notes:

(6) Calculate the total insurance premium owed.

| Particulars | Amount in $ |

| Actual amount owed | 400.00 |

| Less: Estimated premium paid | 420.00 |

| Refund due | (20.00) |

Table (7)

Want to see more full solutions like this?

Chapter 9 Solutions

Bundle: College Accounting, Chapters 1-27, Loose-leaf Version, 22nd + Cengagenowv2™, 2 Terms Printed Access Card For Heintz/parry's College ... Set For College Accounting, 22nd + Cenga

- On September 30, Hilltop Companys selected payroll accounts are as follows: Prepare general journal entries to record the following: Oct. 15 Payment of federal tax deposit of FICA taxes and the federal income tax. 31 Payment of state unemployment tax. 31 Payment of federal unemployment tax.arrow_forwardWallace Corporation summarizes the following information from its weekly payroll records during April. Prepare the two journal entries to record the payment of the payroll and the accrual of its payroll taxes for April. Assume an 8% FICA rate for both employees and the employer. Also assume a 5.4% state unemployment tax rate, a 0.6% federal unemployment tax rate, and that all wages are subject to all payroll taxes. Round to the nearest dollar.arrow_forwardOn September 30, Cody Companys selected account balances are as follows: In general journal form, prepare the entries to record the following: Oct. 15Payment of liabilities for FICA taxes and the federal income tax. 31Payment of liability for state unemployment tax. 31Payment of liability for federal unemployment tax.arrow_forward

- In the Illustrative Case in this chapter, payroll transactions for Brookins Company were analyzed, journalized, and posted for the third quarter of the fiscal year. In this problem, you are to record the payroll transactions for the last quarter of the firms fiscal year. The last quarter begins on April 1, 20--. Refer to the Illustrative Case on pages 6-27 to 6-33 and proceed as follows: a. Analyze and journalize the transactions described in the following narrative. Use the two-column journal paper provided on pages 6-73 to 6-77. Omit the writing of explanations in the journal entries. b. Post the journal entries to the general ledger accounts on pages 6-78 to 6-83. Narrative of Transactions: c. Answer the following questions: 1. The total amount of the liability for FICA taxes and federal income taxes withheld as of June 30 is................................................................................ ________ 2. The total amount of the liability for state income taxes withheld as of June 30 is................................................................................................................ ________ 3. The amount of FUTA taxes that must be paid to the federal government on or before August 1 (assume July 31 is a Sunday) is........................................ ________ 4. The amount of contributions that must be paid into the state unemployment compensation fund on or before August 1 is.................................................. ________ 5. The total amount due the treasurer of the union is........................................ ________ 6. The total amount of wages and salaries expense since the beginning of the fiscal year is ................................................................................................... ________ 7. The total amount of payroll taxes expense since the beginning of the fiscal year is ............................................................................................................ ________ 8. Using the partial journal below, journalize the entry to record the vacation accrual at the end of the companys fiscal year. The amount of Brookins Companys vacation accrual for the fiscal year is 15,000.arrow_forwardCALCULATING PAYROLL TAXES EXPENSE AND PREPARING JOURNAL ENTRY Selected information from the payroll register of Wrays Drug Store for the week ended July 14,20--, is shown below. The SUTA tax rate is 5.4%, and the FUTA tax rate is 0.6%, both on the first 7,000 of earnings. Social Security tax on the employer is 6.2% on the first 118,500 of earnings, and Medicare tax is 1.45% on gross earnings. REQUIRED 1. Calculate the total employer payroll taxes for these employees. 2. Prepare the journal entry to record the employer payroll taxes as of July 14,20--.arrow_forwardThe following information about the payroll for the week ended December 30 was obtained from the records of Qualitech Co.: Tax rates assumed: Social security, 6% Medicare, 1.5% State unemployment (employer only), 5.4% Federal unemployment (employer only), 0.8% Instructions 1. Assuming that the payroll for the last week of the year is to be paid on December 31, journalize the following entries: a. December 30, to record the payroll. b. December 30, to record the employers payroll taxes on the payroll to be paid on December 31. Of the total payroll for the last week of the year, 35,000 is subject to unemployment compensation taxes. 2. Assuming that the payroll for the last week of the year is to be paid on January 5 of the following fiscal year, journalize the following entries: a. December 30, to record the payroll. b. January 5, to record the employers payroll taxes on the payroll to be paid on January 5. Because it is a new fiscal year, all 675,000 in salaries is subject to unemployment compensation taxes.arrow_forward

- In the space provided below, prepare the journal entry to record the November payroll for all employees assuming that the payroll is paid on November 30 and that Joness cumulative gross pay (cell I13) is 85,000.arrow_forwardCALCULATION AND JOURNAL ENTRY FOR EMPLOYER PAYROLL TAXES Earnings for several employees for the week ended March 12, 20--, are as follows: Calculate the employers payroll taxes expense and prepare the journal entry as of March 12, 20--, assuming that FUTA tax is 0.6%, SUTA tax is 5.4%, Social Security tax is 6.2%, and Medicare tax is 1.45%.arrow_forward

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning