Concept explainers

Videos

Comparing Methods to Account for Various Levels of Ownership of Voting Stock

Company T had outstanding 25,000 shares of common stock, par value $10 per share. On January 1 of the current year. Company P purchased some of these shares as a long-term investment at $25 per share. At the end of the current year. Company T reported the following: income. $45,000. and cash dividends declared and paid during the year. $16,500. The fair value of Company T stock at the end of the current year was $22 per share.

Required:

- 1. For each of the following cases (Case A and Case B. shown in the tabulation), identify the method of accounting that Company P should use. Explain why.

- 2. Give the

journal entries for Company P at the dates indicated for each of the two independent cases (Case A and Case B). assuming that the investments will be held long term. If no entry is required, explain why. Use the following format:

| Case A: | Case B: | |

| 3,000 Shares | 8,750 Shares | |

| Tabulation of Items | Purchased | Purchased |

1. Accounting method?

2. Journal entries:

- a. To record the acquisition at January 1.

- b. To recognize the income reported by Company T for current year.

- c. To recognize the dividends declared and paid by Company T.

- d. To recognize fair value effect at end of current year.

- 3. Complete the following schedule to show the separate amounts that should be reported on the current year’s financial statements of Company P:

| Dollar Amounts | ||

| Case A | Case B | |

| Balance sheet | ||

| Investments | ||

| Stockholders’ equity | ||

| Income statement | ||

| Dividend revenue | ||

| Equity in earnings of affiliate | ||

- 4. Explain why assets, stockholders’ equity, and revenues for the two cases are different.

1.

Indicate the method used by Company P to account the investment in Company T under Case A and Case B.

Explanation of Solution

Available-for-sale (AFS) securities: The category of passive investments which are held as idle funds to serve the future operating and strategic purposes, are referred to as available-for-sale securities. The percentage of passive investments in debt or equity will be less than 20%.

Fair value method: The method of accounting the investments in short-term debt, and short-term and long-term equity securities, with an ownership of less than 20% of the outstanding stock of the investee, is referred to as fair value method.

Equity-method: The investments in stock securities which claim significant influence with an ownership of 20% to 50% in the outstanding stock of the investee company, are referred to as investments in stock for significant influence. The method of accounting such investments is referred to as equity method.

Method used to account the investments in Case A and Case B:

| Details | Case A: 3,000 Shares Purchased | Case B: 8,750 Shares Purchased | |

| 1. | Accounting method | Fair value method | Equity method |

Table (1)

Description:

Method used to account for Case A: Since the investor company, Company P purchased 12%

Method used to account for Case B: Since the investor company, Company P purchased 35%

2.

a.

Journalize the purchase of investment in Company T stock for Case A and Case B.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

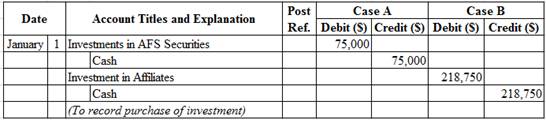

Prepare journal entry to record purchase of investment on January 1.

Table (2)

Description:

Case A:

- Investments in AFS Securities is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute cost of investment in AFS securities.

Case B:

- Investments in Affiliates is an asset account. Since investments are purchased, asset value increased, and an increase in asset is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute cost of investment in affiliates.

b.

Journalize the income reported by Company T, for Case A and Case B.

Explanation of Solution

Prepare journal entry for share of income received from Company T for Case A and Case B.

Table (3)

Description:

Case A: No entry is required for reporting net income of affiliate in fair value method.

Case B:

- Investments in Affiliates is an asset account. Since share of income received from investee increases the investment value, asset value increased, and an increase in asset is debited.

- Equity in Affiliate Earnings is a revenue account. Revenues increase stockholders’ equity value, and an increase in stockholders’ equity is credited.

Working Notes:

Compute amount of income received from Company T.

c.

Journalize the dividends paid by Company T, for Case A and Case B.

Explanation of Solution

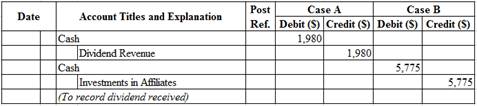

Prepare journal entry for dividends received from Company T.

Table (4)

Description:

Case A:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Dividend Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of dividend received.

Case B:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Investments in Affiliates is an asset account. Since stock investments are reduced as an effect of receipt of dividends, asset value decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of dividend received.

d.

Journalize the adjusting entry for the changes in fair value, for Case A and Case B.

Explanation of Solution

Prepare journal entry for adjusting the securities to the fair market value.

Table (5)

Description:

Case A:

- Net Unrealized Gains (Losses) is an adjustment account used to report gain or loss on adjusting cost of investment at fair market value. Since loss has occurred and losses decrease stockholders’ equity value, a decrease in stockholders’ equity value is debited. This loss is reported as component of Other Comprehensive Income (OCI) on the Statement of Comprehensive Income.

- Investments in AFS Securities is an asset account. The account is credited because the market price was decreased, and eventually the asset value decreased.

Working Notes:

Determine the unrealized gain or loss on investment in AFS securities.

Step 1: Compute the fair value of investment at the end of the year.

Step 2: Compute unrealized gain or loss on investment in AFS securities.

Note: Refer to Equations (6) and (1) for value and computation of fair value of investment and cost of investment.

Case B: Company P does not record any changes in the fair value of the investment at the year end because it is an equity-method investment.

3.

Complete the table for the investments of Company P for Case A and Case B.

Explanation of Solution

Complete the table as shown below:

| Details | Dollar Amounts | |

| Case A | Case B | |

| Balance sheet | ||

| Investments | $66,000 | $228,725 |

| Stockholders’ equity | (9,000) | None |

| Income statement | ||

| Dividend revenue | 1,980 | - |

| Equity in earnings of affiliate | - | 15,750 |

Table (6)

Working Notes:

Find the carrying value of investment by preparing Investment in Affiliates account (Case B).

| Investment in Affiliates | ||||||

| Date | Details | Debit ($) | Date | Details | Credit ($) | |

| Cash | 218,750 | Cash dividends | 5,775 | |||

| Equity in affiliate earnings | 15,750 | |||||

| Total | 234,500 | Total | 5,775 | |||

| Ending Balance | $228,725 | |||||

Table (7)

Note: Refer to Equations (2), (3), and (5) for equity-method cost of investment, revenue, and cash dividends value.

Description:

Investments:

- Case A investments are AFS securities and should be reported at fair value. (Refer to Equation (6) for computation of value).

- Case B investments are securities with significant influence, and should be reported at carrying value of investment in proportion to the net income reported and dividends declared by Company T. (Refer to Table (7) for computation of value).

Stockholders’ equity:

- Case A investments are adjusted to fair value every year-end, so the unrealized loss is reported as a component of stockholders’ equity under accumulated other comprehensive income. (Refer to Equation (7) for computation of value).

- Case B investments are not adjusted to fair value every year-end because they are reported by equity method.

Dividend revenue:

- The dividend revenue from Case A investments are reported on the income statement. (Refer to Equation (4) for computation of value).

- The dividend revenue from Case B investments are reported as cash received, but not revenue. Hence, not reported on the income statement.

Equity in affiliate earnings:

- The net income reported by the investee company is not recorded by the investor for Case A investments.

- The net income reported by affiliate is recorded as investment revenue for Case B investments. Hence, are reported on the income statement. (Refer to Equation (3) for computation of value).

4.

Explain the reasons for the differences between the Case A and Case B investments.

Explanation of Solution

The following are the reasons for the differences between the Case A and Case B investments:

- The treatment of fair value at the end of the year is different under two methods.

- The treatment of dividends received are different under two methods.

- The treatment of net income reported by affiliate are different under two methods.

Want to see more full solutions like this?

Chapter A Solutions

VALUE - FINANCIAL ACCOUNTING LL+ACCESS

- Selected transactions completed by Equinox Products Inc. during the fiscal year ended December 31, 2016, were as follows: a. Issued 15,000 shares of 20 par common stock at 30, receiving cash. b. Issued 4, 000 shares of 80 par preferred 5% stock at 100, receiving cash. c. Issued 500,000 of 10-year, 5% bonds at 104, with interest payable semiannually. d. Declared a quarterly dividend of 0.50 per share on common stock and 1.00 per share on preferred stock. On the date of record, 100,000 shares of common stock were outstanding, no treasury shares were held, and 20,000 shares of preferred stock were outstanding. e. Paid the cash dividends declared in (d). f. Purchased 7,500 shares of Solstice Corp. at 40 per share, plus a 150 brokerage commission. The investment is classified as an available-for-sale investment. g. Purchased 8,000 shares of treasury common stock at 33 per share. h. Purchased 40,000 shares of Pinkberry Co. stock directly from the founders for 24 per share. Pinkberry has 125,000 shares issued and outstanding. Equinox Products Inc. treated the investment as an equity method investment. i. Declared a 1.00 quarterly cash dividend per share on preferred stock. On the date of record, 20,000 shares of preferred stock had been issued. j. Paid the cash dividends to the preferred stockholders. k. Received 27,500 dividend from Pinkberry Co. investment in (h). l. Purchased 90,000 of Dream Inc. 10-year, 5% bonds, directly from the issuing company, at their face amount plus accrued interest of 37 5. The bonds are classified as a held-to-maturity long -term investment. m. Sold, at 38 per share, 2,600 shares of treasury common stock purchased in (g). n. Received a dividend of 0 .60 per share from the Solstice Corp. investment in (f). o. Sold 1,000 shares of Solstice Corp. at 45, including commission. p. Recorded the payment of semiannual interest on the bonds issue d in (c) and the amortization of the premium for six months. The amortization is determined using the straight-line method . q. Accrued interest for three months on the Dream Inc. bonds purchased in (I). r. Pinkberry Co. recorded total earnings of 240 ,000. Equinox Products recorded equity earnings for its share of Pinkberry Co. net income. s. The fair value for Solstice Corp. stock was 39. 02 per share on December 31, 2016. The investment is adjusted to fair value , using a valuation allowance account. Assume Valuation Allowance for Available-for-Sale Investments h ad a beginning balance of zero. Instructions 1. Journalize the selected transactions. 2. After all of the transaction s for the year ended December 31, 201 6, had been poste d [including the transactions recorded in part (1) and all adjusting entries), the data that follows were taken from the records of Equinox Products Inc. a. Prepare a multiple-step in come statement for the year ended December 31, 201 6, concluding with earnings per share . In computing earnings per share, assume that the average number of common shares outstanding was 100,000 and preferred dividends were 100,000. ( Round earnings per share to the nearest cent.) b. Prepare a retained earnings statement for the year ended December 31, 20 6. c. Prepare a balance sheet in report form as of December 31, 2016.arrow_forwardGiven the following year-end information, compute Greenwood Corporations basic and diluted earnings per share. Net income, 15,000 The income tax rate, 30% 4,000 shares of common stock were outstanding the entire year. shares of 10%, 50 par (and issuance price) convertible preferred stock were outstanding the entire year. Dividends of 2,500 were declared on this stock during the year. Each share of preferred stock is convertible into 5 shares of common stock.arrow_forwardStockholders equity accounts and other related accounts of Gonzales Company as of January 1, 20--, the beginning of its fiscal year, are shown below. (a)Received 20,000 for the balance due on subscriptions for preferred stock with a par value of 40,000 and issued the stock. (b)Purchased 10,000 shares of common treasury stock for 18 per share. (c)Received subscriptions for 10,000 shares of common stock at 19 per share, collecting down payments of 45,000. (d)Issued 15,000 shares of common stock in exchange for land with a fair market value of 290,000. (e)Sold 5,000 shares of common treasury stock for Si00,000. (f)Issued 10,000 shares of preferred stock at 11.50 per share, receiving cash. (g)Sold 3,000 shares of common treasury stock for 17 per share. REQUIRED 1. Prepare general journal entries for the transactions, identifying each transaction by letter. 2. Post the journal entries to appropriate T accounts. The cash account has a beginning balance of 300,000. 3. Prepare the stockholders equity section of the balance sheet as of December 31, 20--. Net income for the year was 825,000 and dividends of 400,000 were paid.arrow_forward

- CASH DIVIDENDS, STOCK DIVIDEND, AND STOCK SPLIT During the year ended December 31, 20--, Baggio Company completed the following transactions: Apr. 15 Declared a semiannual dividend of 0.65 per share on preferred stock and 0.45 per share on common stock to shareholders of record on May 5, payable on May 10. Currently, 6,000 shares of 50 par preferred stock and 70,000 shares of 1 par common stock are outstanding. May 10 Paid the cash dividends. Oct. 15 Declared semiannual dividend of 0.65 per share on preferred stock and 0.45 per share on common stock to shareholders of record on November 5, payable on November 20. Nov. 20 Paid the cash dividends. 22 Declared a 10% stock dividend to shareholders of record on December 8, distributable on December 16. Market value of the common stock was estimated at 15 per share. Dec. 16 Issued certificates for common stock dividend. 20 Board of directors declared a two-for-one common stock split. REQUIRED Prepare journal entries for the transactions.arrow_forwardOutstanding Stock Lars Corporation shows the following information in the stockholders equity section of its balance sheet: The par value of common stock is S5, and the total balance in the Common Stock account is $225,000. There are 13,000 shares of treasury stock. Required: What is the number of shares outstanding? Use the following information for Exercises 10-58 and 10-59: Stahl Company was incorporated as a new business on January 1, 2019. The company is authorized to issue 600,000 shares of $2 par value common stock and 80,000 shares of 6%, S20 par value, cumulative preferred stock. On January 1, 2019, the company issued 75,000 shares of common stock for $15 per share and 5,000 shares of preferred stock for $25 per share. Net income for the year ended December 31, 2019, was $500,000.arrow_forwardLongmont Corporation earned net income of $90,000 this year. The company began the year with 600 shares of common stock and issued 500 more on April 1. They issued $5,000 in preferred dividends for the year. What is the numerator of the EPS calculation for Longmont?arrow_forward

- Chen Corporation began 2012 with the following stockholders equity balances: The following selected transactions and events occurred during the year: a. Issued 10,000 shares of common stock for 60,000. b. Purchased 1,200 shares of treasury stock for 4,800. c. Sold 2,000 shares of treasury stock for 11,000. d. Generated net income of 94,000. e. Declared and paid the full years dividend on preferred stock and a dividend of 1.00 per share on common stock outstanding at the end of the year. Chen Corporation maintains several paid-in capital accounts (Paid-in Capital in Excess of Par, Paid-in Capital from Treasury Stock, etc.) in its ledger, but combines them all as Additional paid-in capital when preparing financial statements. Open the file STOCKEQ from the website for this book at cengagebrain.com. Enter the formulas in the appropriate cells on the worksheet. Then fill in the columns to show the effect of each of the selected transactions and events listed earlier. Enter your name in cell A1. Save the completed worksheet as STOCKEQ2. Print the worksheet. Also print your formulas. Check figure: Total stockholders equity balance at 12/31/12 (cell G21). 398,800.arrow_forwardChen Corporation began 2012 with the following stockholders equity balances: The following selected transactions and events occurred during the year: a. Issued 10,000 shares of common stock for 60,000. b. Purchased 1,200 shares of treasury stock for 4,800. c. Sold 2,000 shares of treasury stock for 11,000. d. Generated net income of 94,000. e. Declared and paid the full years dividend on preferred stock and a dividend of 1.00 per share on common stock outstanding at the end of the year. Chen Corporation maintains several paid-in capital accounts (Paid-in Capital in Excess of Par, Paid-in Capital from Treasury Stock, etc.) in its ledger, but combines them all as Additional paid-in capital when preparing financial statements. In the space provided below, prepare the stockholders equity section of Chen Corporations balance sheet as of December 31, 2012. Use proper headings and provide full disclosure of all appropriate information. Chens corporate charter authorizes the issuance of 1,000 shares of preferred stock and 100,000 shares of common stock.arrow_forwardContributed Capital Adams Companys records provide the following information on December 31, 2019: Additional information: 1. Common stock has a 5 par value, 50,000 shares are authorized, 15,000 shares have been issued and are outstanding. 2. Preferred stock has a 100 par value, 3,000 shares are authorized, 800 shares have been issued and are outstanding. Two hundred shares have been subscribed at 120 per share. The stock pays an 8% dividend, is cumulative, and is callable at 130 per share. 3. Bonds payable mature on January 1, 2023. They carry a 12% annual interest rate, payable semiannually. Required: Prepare the Contributed Capital section of the December 31, 2019, balance sheet for Adams. Include appropriate parenthetical notes.arrow_forward

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning