lue Rail produces handrails, banisters, and similar welded products. The p aw material is 40-foot long pieces of steel pipe. This pipe is custom cut anc ato rails. In addition, the final stages of production require grinding and sa perations, along with a final coating of paint (welding rods, grinding disks, re relatively inexpensive and are classified as indirect material within facto verhead) lue Rail measures its output in "sections." Some overage and waste is exp- o the need for an extra post at the end of a set of sections, faulty welds, ar ipe cuts. The company has adopted an achievable standard of 1.25 pieces ipe per section of rail. During August, Blue Rail produced 3,400 sections of ras anticipated that pipe would cost $80 per piece. he production manager was disappointed to receive the monthly perform eport revealing actuall matorial cort 000

lue Rail produces handrails, banisters, and similar welded products. The p aw material is 40-foot long pieces of steel pipe. This pipe is custom cut anc ato rails. In addition, the final stages of production require grinding and sa perations, along with a final coating of paint (welding rods, grinding disks, re relatively inexpensive and are classified as indirect material within facto verhead) lue Rail measures its output in "sections." Some overage and waste is exp- o the need for an extra post at the end of a set of sections, faulty welds, ar ipe cuts. The company has adopted an achievable standard of 1.25 pieces ipe per section of rail. During August, Blue Rail produced 3,400 sections of ras anticipated that pipe would cost $80 per piece. he production manager was disappointed to receive the monthly perform eport revealing actuall matorial cort 000

Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Don R. Hansen, Maryanne M. Mowen

Chapter4: Activity-based Costing

Section: Chapter Questions

Problem 36P: Reducir, Inc., produces two different types of hydraulic cylinders. Reducir produces a major...

Related questions

Question

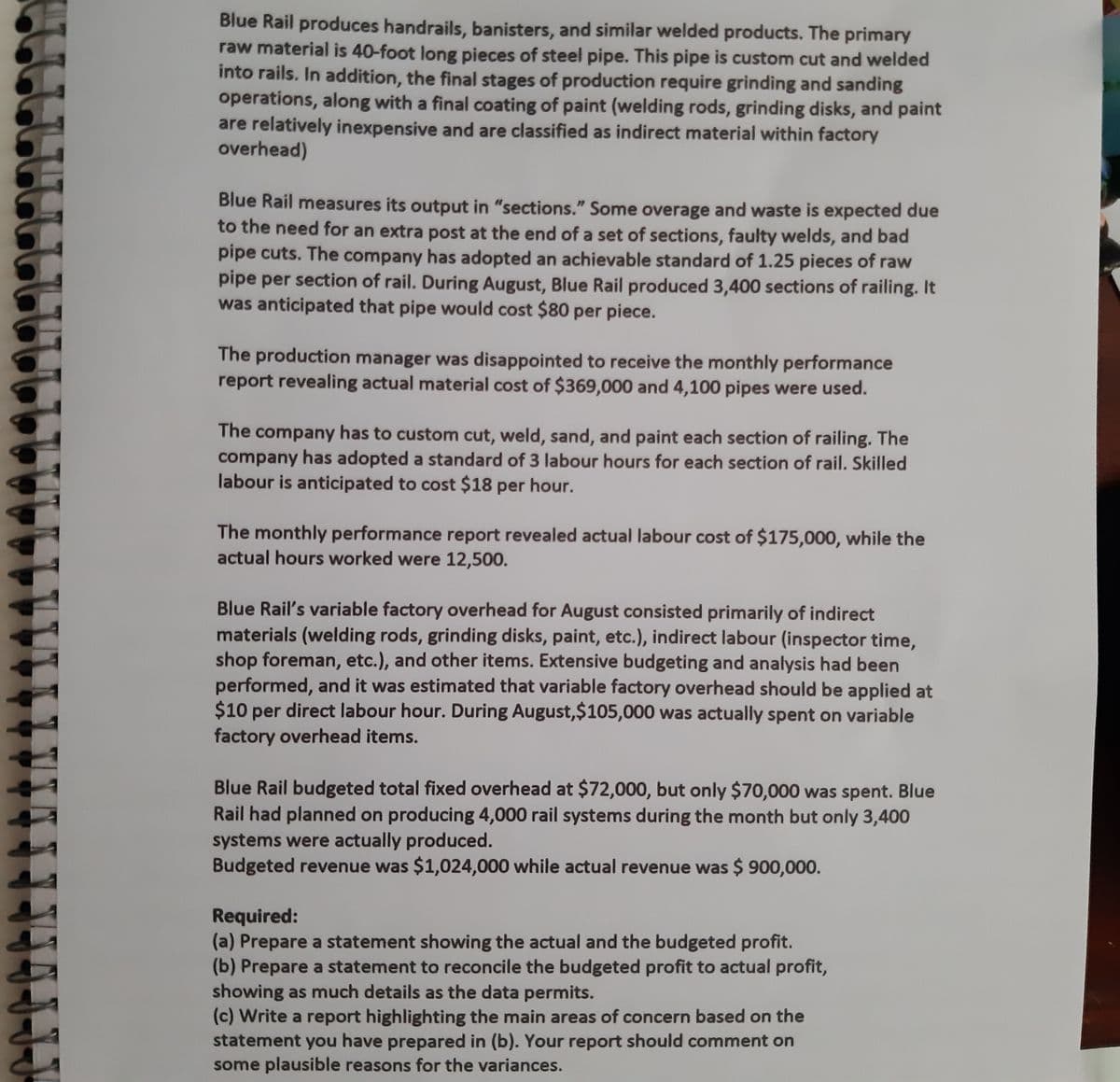

Transcribed Image Text:Blue Rail produces handrails, banisters, and similar welded products. The primary

raw material is 40-foot long pieces of steel pipe. This pipe is custom cut and welded

into rails. In addition, the final stages of production require grinding and sanding

operations, along with a final coating of paint (welding rods, grinding disks, and paint

are relatively inexpensive and are classified as indirect material within factory

overhead)

Blue Rail measures its output in "sections." Some overage and waste is expected due

to the need for an extra post at the end of a set of sections, faulty welds, and bad

pipe cuts. The company has adopted an achievable standard of 1.25 pieces of raw

pipe per section of rail. During August, Blue Rail produced 3,400 sections of railing. It

was anticipated that pipe would cost $80 per piece.

The production manager was disappointed to receive the monthly performance

report revealing actual material cost of $369,000 and 4,100 pipes were used.

The company has to custom cut, weld, sand, and paint each section of railing. The

company has adopted a standard of 3 labour hours for each section of rail. Skilled

labour is anticipated to cost $18 per hour.

The monthly performance report revealed actual labour cost of $175,000, while the

actual hours worked were 12,500.

Blue Rail's variable factory overhead for August consisted primarily of indirect

materials (welding rods, grinding disks, paint, etc.), indirect labour (inspector time,

shop foreman, etc.), and other items. Extensive budgeting and analysis had been

performed, and it was estimated that variable factory overhead should be applied at

$10 per direct labour hour. During August,$105,000 was actually spent on variable

factory overhead items.

Blue Rail budgeted total fixed overhead at $72,000, but only $70,000 was spent. Blue

Rail had planned on producing 4,000 rail systems during the month but only 3,400

systems were actually produced.

Budgeted revenue was $1,024,000 while actual revenue was $ 900,000.

Required:

(a) Prepare a statement showing the actual and the budgeted profit.

(b) Prepare a statement to reconcile the budgeted profit to actual profit,

showing as much details as the data permits.

(c) Write a report highlighting the main areas of concern based on the

statement you have prepared in (b). Your report should comment on

some plausible reasons for the variances.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College