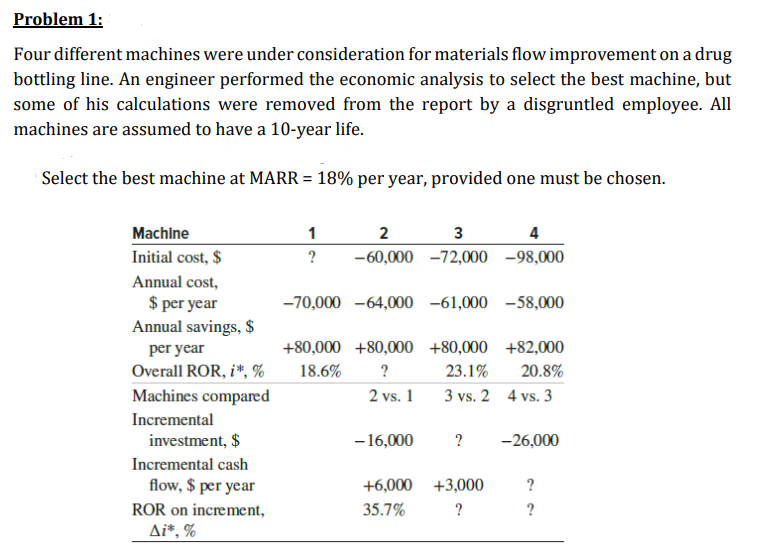

Problem 1: Four different machines were under consideration for materials flow improvement on a drug bottling line. An engineer performed the economic analysis to select the best machine, but some of his calculations were removed from the report by a disgruntled employee. All machines are assumed to have a 10-year life. Select the best machine at MARR = 18% per year, provided one must be chosen. Machine 1 2 3 4 Initial cost, $ ? -60,000 -72,000 -98,000 Annual cost, $ per year Annual savings, $ -70,000 -64,000 -61,000 -58,000 per year +80,000 +80,000 +80,000 +82,000 ? 2 vs. 1 Overall ROR, i*, % 18.6% 23.1% 20.8% Machines compared 3 vs. 2 4 vs. 3 Incremental investment, $ -16,000 ? -26,000 Incremental cash flow, $ per year +6,000 +3,000 ? ROR on increment, 35.7% Ai*, %

Problem 1: Four different machines were under consideration for materials flow improvement on a drug bottling line. An engineer performed the economic analysis to select the best machine, but some of his calculations were removed from the report by a disgruntled employee. All machines are assumed to have a 10-year life. Select the best machine at MARR = 18% per year, provided one must be chosen. Machine 1 2 3 4 Initial cost, $ ? -60,000 -72,000 -98,000 Annual cost, $ per year Annual savings, $ -70,000 -64,000 -61,000 -58,000 per year +80,000 +80,000 +80,000 +82,000 ? 2 vs. 1 Overall ROR, i*, % 18.6% 23.1% 20.8% Machines compared 3 vs. 2 4 vs. 3 Incremental investment, $ -16,000 ? -26,000 Incremental cash flow, $ per year +6,000 +3,000 ? ROR on increment, 35.7% Ai*, %

Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Don R. Hansen, Maryanne M. Mowen

Chapter12: Activity-based Management

Section: Chapter Questions

Problem 22E: The activity of moving materials uses four forklifts, each leased for 18,000 per year. A forklift is...

Related questions

Question

Transcribed Image Text:Problem 1:

Four different machines were under consideration for materials flow improvement on a drug

bottling line. An engineer performed the economic analysis to select the best machine, but

some of his calculations were removed from the report by a disgruntled employee. All

machines are assumed to have a 10-year life.

Select the best machine at MARR = 18% per year, provided one must be chosen.

Machine

1

2

3

4

Initial cost, $

?

-60,000 -72,000 -98,000

Annual cost,

$ per year

Annual savings, $

-70,000 -64,000 -61,000 -58,000

per year

+80,000 +80,000 +80,000 +82,000

Overall ROR, i*, %

18.6%

?

23.1%

20.8%

Machines compared

2 vs. 1

3 vs. 2 4 vs. 3

Incremental

investment, $

-16,000

?

-26,000

Incremental cash

flow, $ per year

+6,000 +3,000

ROR on increment,

35.7%

?

Ai*, %

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Managerial Accounting: The Cornerstone of Busines…

Accounting

ISBN:

9781337115773

Author:

Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning