ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

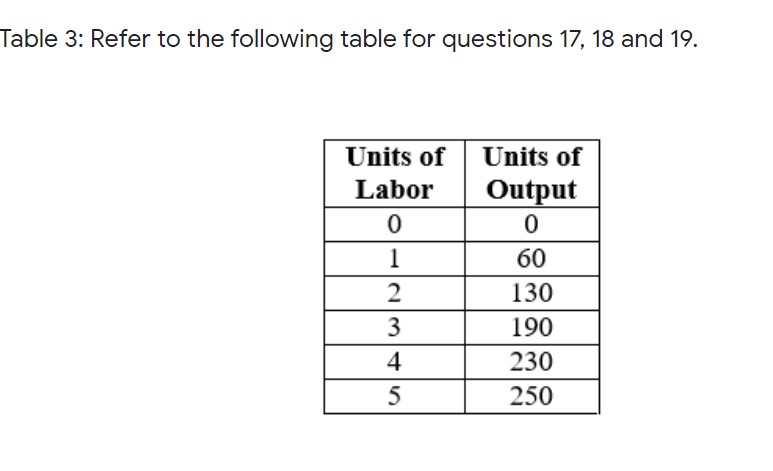

Q. Table 3 above shows how output varies with only one variable input used in production. If the cost of a unit of labor is $500, what is the approximate marginal cost of the 230th unit of output?

a. $2.50

b. $8.50

c. $12.50

d. $50.00

e. $100.00

Transcribed Image Text:Table 3: Refer to the following table for questions 17, 18 and 19.

Units of

Units of

Labor

Output

1

60

2

130

3

190

4

230

250

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider a small photography studio with 8 workers and 5 The total cost of labor and capital is $3,200. In order to reduce total operating costs, the owner leases 5 additional printers and fires 5 workers. After these changes, the salary of each worker increases by $30, the cost of using each of the printers (both new and old) remains constant, and the total cost of labor and capital decreases to $2,900. What is the cost of using one printer?arrow_forwardMoris just opened a chocolate place, it costs her $500 per day to pay for workers’ wages and an additional $2 for each chocolate they make. a. What are the total cost and average cost functions for Moris chocolates b. If Moris chocolate place is open 6 days a week and sells chocolates for $5 each, how many chocoolates does Moris place need to sell each week to break even on its accounting cost?arrow_forwardFill in the gaps in the table below. Quantity of Variable Input Marginal Product of Variable Input Average Product of Variable Input Total Output 1 225 2 300 3 300 4 1140 5 225 225 6arrow_forward

- 13. Suppose you have a production technology given by f(x1, x2) = min{2x₁, x2} and you are producing at the point where x₁ = 10 and x₂ = 20. (a) Explain in words what we mean (generally) by the ‘marginal product' of an input in production. (b) For the production technology in this question and the initial point x₁ = 10 and x2 = 20, what is the marginal product of a small increase in input 1? (c) Suppose input 2 increases and you are now at the initial point x₁ = 10 and x2 = 30. Relative to your answer in part (b), does the marginal product of input 1 decrease, increase, or stay constant? Explain briefly.arrow_forwardCalculate the value of total cost when average cost is $35 and the no of inputs employed is 5arrow_forwardIf the cost of an oven is $500, what is the marginal product per dollar spent on capital for the second oven? Read again before you answer. Labor Total Product Capital (ovens) (workers) (cakes) 8 6,000 8 10,000 8 13,000 Type your numeric answer and submit 123arrow_forward

- Explain why this statement is true or false: "If the labor cost per table is $20 and the material cost per table is $30, the short run average cost per table is $50."arrow_forwardFill in the missing data to solve this problem. Variable Total Average MarginalInput Product Product Product4 ? 70 ----5 ? ? 406 350 ? ? What is the total product for 5 units of input, and what is the marginal product for 6 units of input?arrow_forwardSuppose a publisher faces the following costs of producing 10,000 newspapers each month:$5,500 cost of labor; $2,200 monthly mortgage payment; $250 cost of electricity to run theprinting presses; $800 for ink and paper; and $200 in city property taxes (based on the valueof the building and land). Its total variable costs are: Group of answer choices $8,750. $8,950. $6,300. $6,550arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education