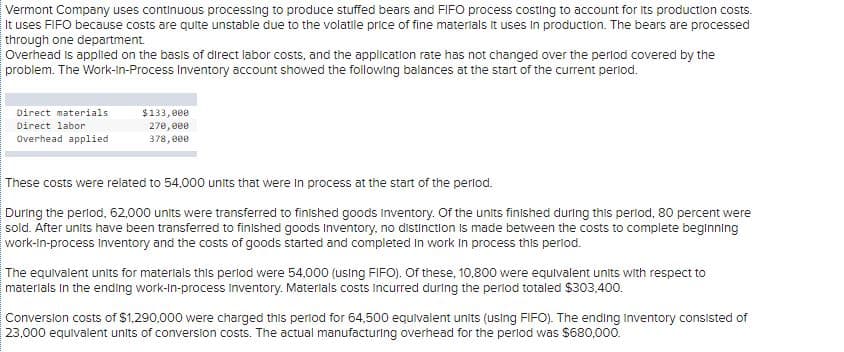

Vermont Company uses continuous processing to produce stuffed bears and FIFO process costing to account for its production costs. It uses FIFO because costs are quite unstable due to the volatile price of fine materials it uses in production. The bears are processed through one department. Overhead is applied on the basis of direct labor costs, and the application rate has not changed over the perlod covered by the problem. The Work-in-Process Inventory account showed the following balances at the start of the current perlod. Direct materials $133, 000 Direct labor 270, ee0 Overhead applied 378, eee These costs were related to 54,000 units that were in process at the start of the perlod. During the perlod, 62,000 units were transferred to finished goods Inventory. Of the units finished during this period, 80 percent were sold. After units have been transferred to finished goods Inventory, no distinction is made between the costs to complete beginning work-in-process inventory and the costs of goods started and completed in work in process this period. The equivalent units for materials this perlod were 54,000 (using FIFO). Of these, 10,800 were equivalent units with respect to materials in the ending work-in-process inventory. Materials costs incurred during the perlod totaled $303,400. Converslon costs of S1.290,000 were charged this perfod for 64,500 equivalent units (using FIFO). The ending Inventory consisted of 23,000 equivalent units of converslon costs. The actual manufacturing overhead for the perlod was $680,000.

Vermont Company uses continuous processing to produce stuffed bears and FIFO process costing to account for its production costs. It uses FIFO because costs are quite unstable due to the volatile price of fine materials it uses in production. The bears are processed through one department. Overhead is applied on the basis of direct labor costs, and the application rate has not changed over the perlod covered by the problem. The Work-in-Process Inventory account showed the following balances at the start of the current perlod. Direct materials $133, 000 Direct labor 270, ee0 Overhead applied 378, eee These costs were related to 54,000 units that were in process at the start of the perlod. During the perlod, 62,000 units were transferred to finished goods Inventory. Of the units finished during this period, 80 percent were sold. After units have been transferred to finished goods Inventory, no distinction is made between the costs to complete beginning work-in-process inventory and the costs of goods started and completed in work in process this period. The equivalent units for materials this perlod were 54,000 (using FIFO). Of these, 10,800 were equivalent units with respect to materials in the ending work-in-process inventory. Materials costs incurred during the perlod totaled $303,400. Converslon costs of S1.290,000 were charged this perfod for 64,500 equivalent units (using FIFO). The ending Inventory consisted of 23,000 equivalent units of converslon costs. The actual manufacturing overhead for the perlod was $680,000.

Principles of Cost Accounting

17th Edition

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Edward J. Vanderbeck, Maria R. Mitchell

Chapter6: Process Cost Accounting—additional Procedures; Accounting For Joint Products And By-products

Section: Chapter Questions

Problem 8E: Sonoma Products Inc. manufactures a liquid product in one department. Due to the nature of the...

Related questions

Question

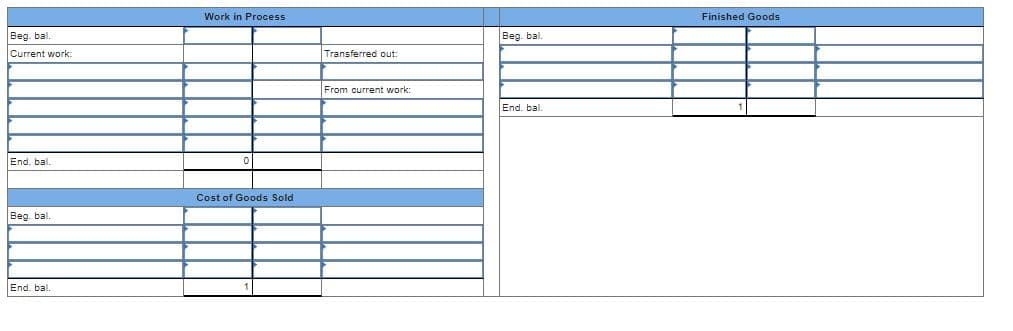

For this question I have to prepare T-accounts to show the flow of costs. (Any difference between actual and applied

In the given T-account each blue outlined box has a drop down menu with the given options:

- Conversion

- From beginning inventory

- From finished goods

- Materials

- Overapplied overhead

- To cost of goods sold

- Transferred in

- Transferred out

- Underapplied overhead

Transcribed Image Text:Work in Process

Finished Goods

Beg. bal.

Beg. bal.

Current work:

Transferred out:

From current work:

End. bal.

End, bal.

Cost of Goods Sold

Beg. bal.

End. bal.

Transcribed Image Text:Vermont Company uses continuous processing to produce stuffed bears and FIFO process costing to account for Its production costs.

It uses FIFO because costs are quite unstable due to the volatile price of fine materlals it uses in production. The bears are processed

through one department.

Overhead is applied on the basis of direct labor costs, and the application rate has not changed over the perlod covered by the

problem. The Work-In-Process Inventory account showed the following balances at the start of the current perlod.

Direct materials

$133,000

270, 000

378,000

Direct labor

Overhead applied

These costs were related to 54,000 units that were In process at the start of the perlod.

During the perlod, 62,000 units were transferred to finished goods inventory. Of the units finished during this period, 80 percent were

sold. After units have been transferred to finished goods Inventory, no distinction Is made between the costs to complete beginning

work-in-process inventory and the costs of goods started and completed in work in process this period.

The equivalent units for materials this perlod were 54,000 (using FIFO). Of these, 10,800 were equlvalent units with respect to

materials in the ending work-in-process inventory. Materlals costs incurred during the period totaled $303,400.

Conversion costs of $1,290,000 were charged this period for 64,500 equivalent units (using FIFO). The ending Inventory consisted of

23,000 equlvalent unlts of conversion costs. The actual manufacturing overhead for the perlod was $680,000.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Principles of Cost Accounting

Accounting

ISBN:

9781305087408

Author:

Edward J. Vanderbeck, Maria R. Mitchell

Publisher:

Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser…

Accounting

ISBN:

9781305970663

Author:

Don R. Hansen, Maryanne M. Mowen

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Principles of Accounting Volume 2

Accounting

ISBN:

9781947172609

Author:

OpenStax

Publisher:

OpenStax College